The Unemployment Rate Is Not Enough When Labour Market Signals Break

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Unemployment alone can hide a weak labour market Payrolls, participation and hours reveal the real bottleneck Policy must treat labour supply as a moving target

Back in June 2022, the U.S. appeared to be close to full employment when viewed through the lens of the unemployment rate. It was at 3.6 percent, nearing the 3.5 percent nadir that prevailed before the pandemic. Yet labor force participation was still more than a percentage point below its February 2020 level and payroll employment was still 524,000 jobs short. That was the real warning. A low unemployment rate can hide a smaller labor force, underemployed hours, weak hiring and firms unable to find workers. It can turn a bottleneck into a strength. The key policy insight is straightforward: labor market indicators have to be interpreted as a system of information, not through a single headline number. When labor supply shifts substantially, the unemployment rate ceases to be a reliable indicator of slack. It becomes one signal among many and sometimes a misleading one.

Why Labor Market Signals Broke After the Pandemic

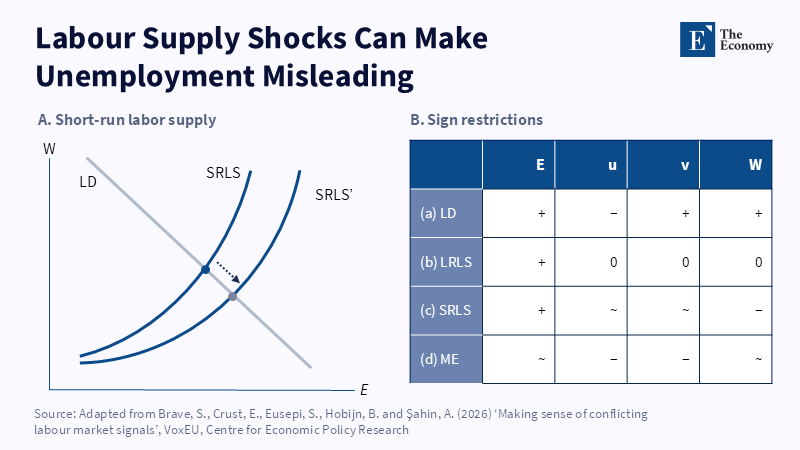

The old labor-market rule was simple: when unemployment was low, the labor market was tight and when unemployment was high, the labor market was slack. This rule was closer to true when labor supply fluctuated slowly: when most workers sought jobs in the same way, when transport remained unchanged and when hours, health risks, caring responsibilities and location were not abruptly re-evaluated. The pandemic shattered these assumptions: it didn't just temporarily wipe out jobs; it altered the available number of workers and the range of hours and locations they would find acceptable.

Hence, the signals from the labor market started to become more deceptive than before, with a booming firm saying demand was high and jobs were available, while employment was expanding at a sluggish pace. The central bank registering low unemployment could be faced with rising wages. The government saw an official healthy rate of unemployment decline, even as areas of public services, care, transport and restaurants and hotels were very short of workers. The headline number looked calm, since some workers were not counted as unemployed if they were not in the labor market. Similarly, if a worker could find only part-time work, the problem would appear as underemployment, not unemployment. Equally, if a firm chose to keep a vacancy on its books, then in all likelihood it would not contribute to the unemployment rate.

This had become obvious during the early post-pandemic recovery, with demand in the U.S. and UK rebounding more quickly than labor supply. Firms were eager to recruit, but workers had switched careers, moved to another country, faced health limits, adjusted their care schedules and refused jobs that no longer suited their lifestyles. UK vacancy numbers reached historic highs (1.318m between late 2021 and early 2022) and economic inactivity increased while employment trailed pre-pandemic levels even after unemployment declined. These were not mere statistical anomalies. They were evidence of a redesigned labor market.

Labor Market Signals Need Payrolls, Participation and Hours

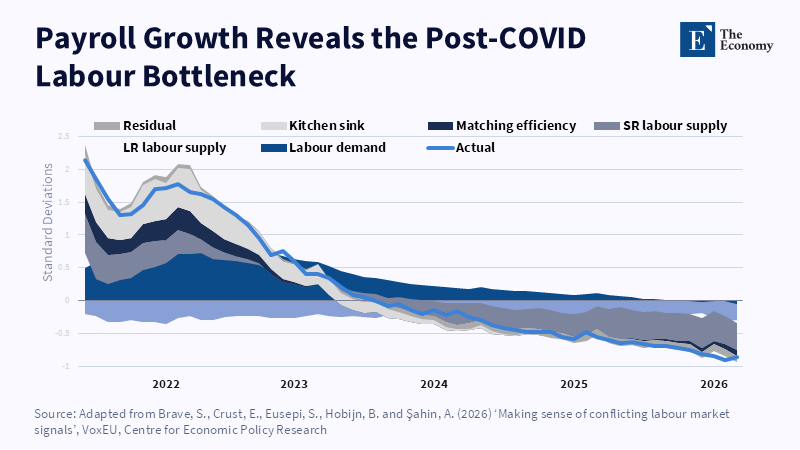

A better way of looking at things begins with the labor force. Participation is important because unemployment counts people in the labor force who are actively seeking work. If people exit the labor force, unemployment can fall while the economy has yet to regain its true amount of work. This is precisely why the steep decline in participation in 2020 was so relevant. The U.S. labor force participation rate fell from 63.4 percent in February 2020 to 60.2 percent in April 2020. Over the following two years, partial gains were made. As of June 2022, it was just 62.2%.

The payroll matters for the same reason. They reveal whether jobs are actually being filled. A low unemployment rate combined with tepid payroll growth is not a tell-tale signal of solid growth. It can be a sign that fewer people are available, or firms are recruiting from a narrower pool, or that the matching process has become more difficult. The payrolls reveal sector imbalances. In June 2022, U.S. employment in leisure and hospitality remained substantially below its pre-pandemic level, while employment in transportation and warehousing had exceeded its pre-pandemic baseline. One headline report on the U.S. labor market could not reveal such a change. The economy was not only rebounding. It was reallocating workers between sectors.

Hours count too. A worker is not only a person in or out of work, but also a number of hours supplied. Research from survey data on desired hours revealed that willingness to work declined even more than labor-force participation did. Desired hours declined by roughly twice as much as labor force participation between 2013 and 2021. This is relevant for wage pressure. If experienced workers demand fewer hours while deterred job seekers are less willing to take jobs, firms may face shortages even when unemployment is low. Labor market signals need to include hours, not only persons.

Remote Work Made Labor Market Signals Harder to Read

Work-from-home introduced a second dimension into the data. It altered the nature of the job itself. At the time of the pandemic, the location of employment was often treated as fixed. Subsequently, place became part of labor compensation, productivity and labor market supply. Studies of telecommuting predict that about 20 percent of all full work days will be supplied off-site in the wake of the pandemic (compared with roughly 5 percent pre-pandemic). That is not a negligible advantage at the margin of the labor market. It is an enormous reduction in the cost of employment, predominantly because it alters commute time, family management and the hassles of daily office attendance.

This aspect may clarify why job market indicators were so ambiguous during the return-to-office. Not all workers were turning away from work itself. Many were turning away from a changed bundle of work. An arrangement that was acceptable with remote work might seem less so with long commutes. A parent, older worker, worker with a disability, or someone with an off-the-charts transport burden may participate only when the work remains so flexible. When firms pulled away that offer, at least part of the supply became a contingent decision. This is not a cultural sideline. It alters the effective supply curve confronting firms.

The policy mistake is to consider working from home solely as an employer preference. It is a labor market infrastructure. It has implications for who can work, for how many hours they can offer and for what kind of jobs they can access. That doesn't imply all jobs can or should be remote. Childcare, construction, logistics, retail and almost all services can't be shrunk into a laptop. But it means that policymakers must distinguish between the two shortages. A skill shortage and a job design shortage are situations in which, for an existing workforce, the job package no longer exists to clear the market.

Labor Market Signals Should Guide Supply Policy

An integrated labor market dashboard should not be densely complicated; it should answer one practical question. Is the economy short of jobs? Short of workers? Short of hours? Short of matching, since these yield different policy responses. Shortage of jobs is a demand-side problem. A worker shortage requires participation policy, migration channels, health support, childcare and better transport. Short of hours requires optimizing job design, more flexible scheduling and reward systems for extra work. Short of matching means credentials transfer enhancement, local employment, speed of certification and reskilling programs.

For administrators and training providers, the lesson is to stop treating labor demand solely as unemployment. Program planning should not be solely guided by unemployment but should have regard to vacancies,wage growth, employment by sector, employer surveys and regional participation. A region with low unemployment and a high number of vacancies requires a different response from a region with a high degree of unemployment and weak vacancies. The former may need nursing placements, links to transit, planned migration, or additional childcare places. The latter will require demand-side support and perhaps job creation initiatives. Both should not be treated as the same problem.

As a result, training systems enter this debate only through the labor-market pipeline, rather than as a distinct issue area. Colleges, technical colleges and adult skills units should be judged on whether they are contributing to repairing real shortages and that could mean providing quicker routes into health care, care work, digital help, construction, transportation and public services where local evidence highlighted big shortfalls. It could also mean cutting back on regular employability courses that lead to certificates but no job offers. When signals from the labor market reflect skills shortages, the solution must be targeted, rapid and employer-focused. When signals from the labor market reflect poor working conditions, training alone will be pointless: a worker cannot be up-skilled into accepting a job that is poorly paid, hard to reach, or caused by rushed schedules that conflict with other care responsibilities.

The perspective is also straightforward for the central bank. If an unemployment rate lower than that predicted by a normal Phillips curve resulted from a smaller labor force, the rise in wages could be seen too early. If recent growth in payrolls is restrained by the supply side, then raising rates could have the effect of reducing demand but not removing the actual constraint. Monetary policy cannot police the nurses, reopen the crèches, reduce the commute, or cure inactivity sickness. It can only deter. Hence, labor market intervention should distinguish between excess heat and input shortage, ensuring that a rate change based on unemployment only is not belated, too harsh, or misdirected.

Policy Must Treat Labor Supply as a Moving Target

The key argument against too broad an approach, say skeptics, is that it can dilute the message. Decision-makers like one number because it travels well. The unemployment rate is simple, current and known. A dashboard can look cluttered. But the post-pandemic labor market has demonstrated that an illusion of simplicity can be more damaging than a gestalt of complex factors. One number can be easy to communicate and yet wrong for the decision. The solution in a new age of information is not to bury policy-makers in too many indicators. Rather, it is to craft a disciplined index that encompasses four blocks: spare workers, filled jobs, unfilled jobs and available hours.

A second critique is that shortages should be resolved by wages. Better pay is needed and no sector with poor conditions and low pay should be shielded from wage pressures. But wages alone cannot restore every missing worker. They will not resolve chronic ill health, changing age-structures, high housing costs, migration regulations, childcare gaps, or stressful office mandates. The OECD has documented further persistence of shortages, for example, in health care and information technology, even after the most cyclical slack had begun to shrink. That is the point. Some shortages are price signals. Others are capacity signals. A robust policy system must therefore identify which is which.

The much bigger lesson is that labor supply is no longer a quiet background variable. It responds to health, age, migration, care systems, remote working, transport and worker preferences. It can decline even when unemployment seems low. It can recover in one industry and be marooned in another. It can look normal in headcount and tight in hours. The next recessions or expansions will again signal labor market ambiguity. The appropriate policy response is not to wait for the confirmation from the unemployment rate on top of the headlines of payrolls, job ads, participation rates and hours. The call to action is clear: make the labor market dashboard the default image and interpret unemployment as one of many indicators, not the final verdict.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Advisory - Strategy Desk (2026) ‘Top 20 Workforce Strategy Advisory 2026’, Advisory Ranking, 1 April.

Barrero, J.M., Bloom, N. and Davis, S.J. (2021) ‘Why working from home will stick’, NBER Working Paper No. 28731, National Bureau of Economic Research.

Brave, S., Crust, E., Eusepi, S., Hobijn, B. and Şahin, A. (2026) ‘Making sense of conflicting labour market signals’, VoxEU, Centre for Economic Policy Research, 7 June.

Faberman, R.J., Mueller, A.I. and Şahin, A. (2022) ‘Has the willingness to work fallen during the COVID pandemic?’, Labour Economics, 79, 102275.

Forster van Aerssen, K., Gomez-Salvador, R., Soudan, M. and Spital, T. (2021) ‘The US and UK labour markets in the post-pandemic recovery’, ECB Economic Bulletin, Issue 8/2021.

Healthcare - Hospital Desk (2023) ‘Hospitals, Clinics & Care Providers Outlook 2023’, Healthcare Ranking, 31 January.

HNW - Aviation and Mobility Desk (2026) ‘Aviation & Mobility Outlook 2026: Private Aviation Resilience, Luxury Mobility Integration, and the Infrastructure of Ultra-High-Net-Worth Travel’, HNW Ranking, 1 January.

OECD (2024) ‘Understanding labour shortages: The structural forces at play’, in OECD Economic Outlook, Volume 2024 Issue 2: Resilience in Uncertain Times, OECD Publishing.

Office for National Statistics (2022) ‘Labour market overview, UK: May 2022’, Office for National Statistics.

Ranking News Editor (2026) ‘Composite Indices: The Statistical Foundations Behind Modern Rankings’, The Ranking News, 16 March.

U.S. Bureau of Labor Statistics (2022) ‘The Employment Situation — June 2022’, U.S. Department of Labor, 8 July.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.