Japan Wage Growth Is Forcing a Choice About Which Firms Survive

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Japan wage growth marks a clear break from decades of stagnation Large firms can raise pay more easily than smaller businesses Policy must protect workers and viable firms during the transition

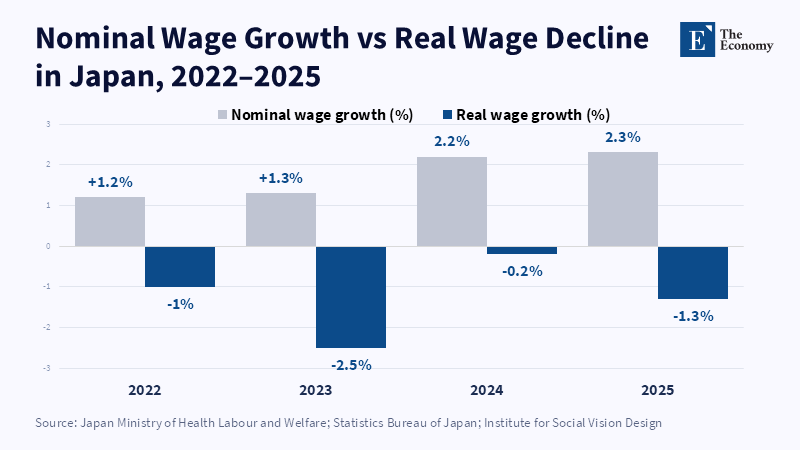

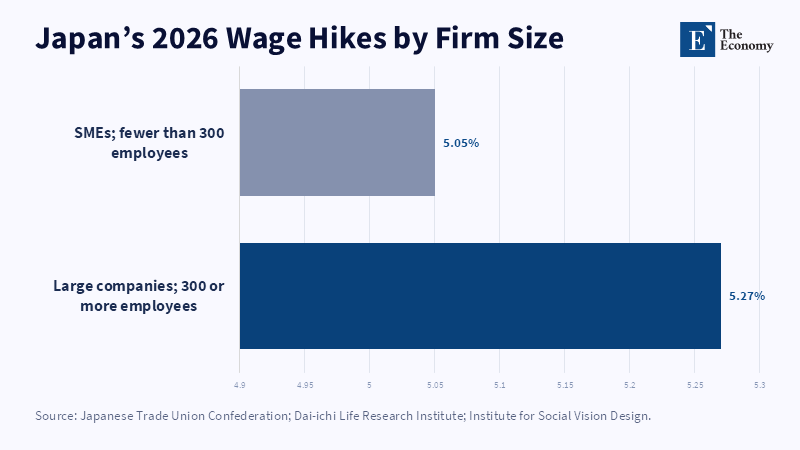

Japan has been in search of a stable path of wage and price change for more than thirty years. It is just back on it. They are gaining, though not in unison. In the 2026 spring wage round, the preliminary average hike was 5.26 percent, the third consecutive year above 5 percent. However, real wages declined 1.3 percent year on year in 2025. This is more than a statistical discrepancy. It indicates that Japan's wage hike has entered the most difficult phase of the post-deflation rebound. While large companies can raise wages, protect margins, and compete for a tight labor force, smaller ones cannot fulfill all three requirements. Therefore, wage divergence becomes a signal, implying where jobs, credit, and ultimately demand will be heading. The ultimate policy question is no longer about how to guard preexisting structures of the economy with minimal disruption. Rather, it should be about how to facilitate weak companies in closing down while not letting viable but exposed companies be shattered by buyer power, inappropriate pricing rules, or lack of transition support.

Japan Wage Growth Has Ended One Era, Not the Crisis

This has been a long-standing mystery: Why hasn’t tight labor pushed up wages? By 2017, unemployment was 2.5 percent, and yet nominal hourly wages rose by 0.8 percent.1 Low inflation expectations, sluggish productivity growth, a lack of labor mobility, and the expansion of lower-paid non-regular work all pushed wages lower. Non-regular work accounted for 38 percent of employment and paid wages about one-third less than regular workers; this pattern has begun to change. Inflation has been fairly steady, there is a shortage of labor, and the Bank of Japan has increased its policy rate from 0 to 1 percent. Employers can no longer assume that wages, supplier prices, and borrowing costs will follow fairly flat lines. This is a positive development. Capital, money, and labor cannot thrive in a market-based economy when prices have vanished. However, as in the rest of the economy, the re-emergence of prices will also bankrupt those firms that managed to survive through cheaper credit, constrained wage claims, and long-term contracts that held down supplier costs. Rising Japanese wages not only benefit families; they illuminate which firms could only exist under a deflationary economy.

The first green shoots matter. Real pay increased 1.9 percent in April 2026 from a year earlier, rising for a fourth consecutive month. Regular earnings grew 3.4 percent in April. The base pay for full-time workers has grown for the fourth month in a row by more than 3 percent. These improvements are important because one cannot continue building on the same export results, weak yen, or asset prices. It is essential to strengthen household purchasing power. However, a strong run of monthly data does not conclusively prove the issue. The 2025 spring wage round resulted in an average increase of 5.25 percent, but only 4.65 percent for trade unions with fewer than 300 members. The gap is only six-tenths of a percentage point but it could widen quickly as minimum wages, input costs and debt payments rise.

This is why the current upturn cannot be judged by the headline spring wage settlement figure alone. The yearly bargaining cycle primarily indicates organized labor and firms with access to formal bargaining. It rarely reflects pay in small retailers, neighborhood services, family companies, or irregular employment. Japan's wage growth could be high in the national average, yet still be uneven across sectors. The real test is whether higher base pay reaches firms that lack powerful unions, export income, or market power. It must do so long after food and energy shocks decline, subsidies end, and interest burdens increase. A definitive end to stagnation would see persistent, not short-term, real wage gains. In the latter respect, the change is real but incomplete.

The Japan Wage Growth Gap Is Also a Pricing-Power Gap

Small and medium-sized firms make up 99.7 percent of all firms in Japan and around 69.7 percent of all employment. That scale rules out any easy suggestion that small firms can be merely counted as a minor, weak tail; they are the labor market. They also incorporate suppliers with special skills, local courier firms, health and social service utilities, retailing, and manufacturing firms supporting larger corporate conglomerates. Ironically, numerous firms run with much less scope to increase prices. Japan’s 2025 SME White Paper found that the labor share at smaller firms was already close to 80 percent. Put simply, an enormous proportion of the value they produce is already delivered to employees. A further increase in wages without higher sales, stronger prices or greater productivity per worker can therefore arise from profit, investment, or proprietors' income. That can work for a year. It cannot function as a sustainable national wages policy.

The strain shows in the behavior of firms. The December 2026 JCCI LOBO survey found that 35.5 percent of smaller firms increased wages as a defensive move despite no improvement in their business situation. While rational in the presence of labor shortages, such measures do not constitute a sign of a virtuous wage-price cycle – indeed, this can merely be a symptom of stress. The same applies to the ability of costs to pass through to prices. A September 2025 survey found that just 50 percent of higher labor costs found their way into selling prices. Many firms are paying for the national wage policy out of margins already suffering from considerable stress. Large buyers may praise higher wages while resisting price increases from suppliers. Consumers can reiterate their position that pay is higher, while they otherwise switch away to another shop when prices rise. Public bodies may stipulate nominally high minimum wages while they subsequently buy from the lowest bidders in their contracts. Ultimately, the system imposes the adjustment of the small business sector, yet customers, lead firms, and government purchasing are all unwilling to fund it.

Labor shortage sharpens this pressure. The rate of unemployment was 2.5 percent in May 2026, and the ratio of vacancies to applicants was nearly 1.2 in fiscal 2025. The national population declined to approximately 122.85 million as of June 2026. Workers will move towards firms offering higher wages. Young workers will be able to compare initial pay with much stronger confidence than their parents. Big business will be able to pay higher wages, provide better training, and offer more definitive career paths. Small businesses will lose workers, reduce hours, or shut down. Some adjustments make sense. Labor should be hired where it can be utilized efficiently. However, a process of waste occurs when an efficient provider is shut down because a commercially dominant purchaser blocks price increases or when an important local service slips away because its social value is not incorporated into its billing. Hence, the pay gap is not only a productivity gap, but also a bargaining power and valuation gap.

Do Not Save Every Firm; Stop Destroying Viable Ones

The usual answer is that unproductive firms should be allowed to go bankrupt. And there is an important grain of truth in this. It is hard to see how Japan will narrow the productivity gap with other rich countries by resuscitating every low-production enterprise. Blanket grants will prolong work in dead industries, insulate poor management, and pass on the cost to taxpayers. Easy money can buy time, but not the workers. The white paper on small and medium enterprises of 2026 is right to advocate the use of new technology, restructuring enterprises, passing businesses on, and promoting cooperative relationships. Larger entities, through merger, back office pooling, use of robots, and tight cost control, will raise individual outputs. Some businesses will close, and free up workers and capital for better employment. Others can be combined with superior firms before employees' and consumers' preferences change. An economy coming out of deflation requires more movement, not another form of autonomous bailout.

But "let the market decide" is not an entire policy. Markets only decide when prices include genuine cost, or contracts are fair. Japan's old deflationary system often hid labor costs in suppliers' margins, paid off suppliers who held back on prices, and failed to pay expansionist firms that had just survived by keeping pay low. It also regarded many local services as private trades, regardless of how much the economy depended on them as civic services. To inherit these regulations when support was cut would not refine the market selection: it would produce chance selection. Firms with limited cash or highly entwined networks would go first, not always firms with the least social or economic worth. The challenge the politicians face is to distinguish three types of firms: those that can grow into more competitive, viable firms with a worse deal, and a model that simply does not work anymore. Different reforms are required for each. The Bank of Japan's own local data confirms that delayed cost pass-through, not lagging behind the bargaining of wages, is already discouraging many small firms.

For the first group, aid should be temporary and related to measurable changes. Support for software, equipment, energy efficiency, training, and shared services should be conditional upon a productivity plan consisting of higher value added per worker. The government already has a five-year wage agreement for small firms and a major productivity program. The next step should be stricter oversight. Aid should not encourage the purchase of a machine that remains inactive. It should reward lower hours per unit, more sales per worker, or a sustained increase in base wages. For the second group, cost pass-through should become a strict rule rather than a polite request. Major contractors must declare how the wages paid to their suppliers are financed. Public procurement should tend towards automatic price adjustment when, at the same time, the legislated minimum wages, energy prices, or commodities change significantly. For the third group, the policy has to facilitate a well-ordered exit, sale, or transfer. The ultimate objective is not to preserve each company’s name. It is to defend valuable capital, human assets, and skills.

A Managed Exit from Deflation

A worker-centric transition is what is missing in Japan's wage growth strategy. Firm support is tractable in the budget and observable in loan terms. Worker flows are not. They require portable training, income support through job transitions, subsidies on housing and transport, and better matching of local workers to expanding firms. Parts of the older workforce and those in small family businesses may acquire practical skills without certification. Short, visible certificates reveal their expertise. Community budgets should include free-access maps of the local infrastructure. How much service will run to the edge of an unprofitable supermarket, bus line, school clinic, or home care firm at the fine points of market taxation? Then, an open public-service contract provides value-for-money against the loss of unrecognized under-priced output. It allows new entry.

The more difficult question is who pays. Higher wages cannot be paid for by small firms alone. Some must be passed on to customers via prices. Part must come from large firms through fairer supplier terms, part from the state where public value is clear and part from owners through lower profits, new investment or exit. This sharing of the pain would go down badly; it would make inflation more apparent and the failure of firms more the subject of political debate. But it was the price paid for preserving the old system in which consumers paid the cost through low prices, and workers paid it through low pay, and small firms through thin profit. That system helped maintain prices at rest, but it may have also contributed to an era of persistent weak demand and a lack of renewal. A fair recovery cannot keep shrouding the bill in its most wretched balance sheets.

The 5.26 percent is therefore a starting signal rather than a final victory. Japan has finally facilitated the circulation of wages, prices, and interest rates after a long pause. The next risk is the potential fragmentation of this movement: real gains for employees in large firms, defensive wage increases in small firms, and bottlenecks that hollow out local economies. Japan's wage growth will only be sustainable if policy ensures fairness in its deployment. Price pass-through should be closely monitored. Resources for productivity enhancement should be committed only when results are delivered. Employees need to be safeguarded if plants are closed. Critical services should be purchased openly rather than maintained through hidden sacrifice. Recovery beyond the bubble will require pain; however, that pain should not be bid for by market power or left to chance under political neglect. Japan's final step out of deflation is not merely higher wages; it is about finally entering a modern economy in which some firms must change, others will close and some will be too important to lose.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bank of Japan, Research and Statistics Department (2025) Firms’ Stance on Wage Growth for Fiscal 2026: As of 3 December 2025. Tokyo: Bank of Japan.

Cabinet Office, Government of Japan (2025) Basic Policy on Economic and Fiscal Management and Reform 2025: Toward a Society in Which People Can Feel “Tomorrow Will Be Better Than Today”. Tokyo: Cabinet Office.

East Asia Forum (2026) ‘Japan’s wage revival spells trouble for smaller businesses’, East Asia Forum, 27 June.

Healthcare Ranking, Hospital Desk (2026) ‘Hospitals, Clinics & Care Providers Outlook 2026: Care Model Redesign, Margin Pressure, and the Institutionalization of Patient-Centered Delivery’, Healthcare Ranking, 31 January.

Japan Chamber of Commerce and Industry (2025) LOBO Survey: Quick Survey System of Local Business Outlook, December 2025. Tokyo: Japan Chamber of Commerce and Industry.

Japan Finance Corporation (2025) Guide to the Operations of the Small and Medium Enterprise Unit 2025. Tokyo: Japan Finance Corporation.

Japan Institute for Labour Policy and Training (2026) ‘Wage increase rate exceeds 5% for a third consecutive year: Rengō’s first tally of the 2026 spring labour offensive’, 27 March. Tokyo: JILPT.

Meunier, B. (2018) ‘Japan: when full employment does not equate to wage growth’, Eco Notepad, no. 89, 9 October. Paris: Banque de France.

Ministry of Health, Labour and Welfare (2026a) Monthly Labour Survey: Annual Results for 2025. Tokyo: Government of Japan.

Ministry of Health, Labour and Welfare (2026b) Monthly Labour Survey: Preliminary Report for April 2026. Tokyo: Government of Japan.

Shinke, Y. (2026) ‘Three consecutive years of 5% wage increases within reach: Rengō’s first 2026 tally’, Economic Trends, 23 March. Tokyo: Dai-ichi Life Research Institute.

Small and Medium Enterprise Agency (2025a) 2025 White Paper on Small and Medium Enterprises in Japan. Tokyo: Ministry of Economy, Trade and Industry.

Small and Medium Enterprise Agency (2025b) Price Negotiation Promotion Month Follow-Up Survey: September 2025. Tokyo: Ministry of Economy, Trade and Industry.

Small and Medium Enterprise Agency (2026) 2026 White Paper on Small and Medium Enterprises in Japan. Tokyo: Ministry of Economy, Trade and Industry.

Statistics Bureau of Japan (2026a) Labour Force Survey: Monthly Results, May 2026. Tokyo: Ministry of Internal Affairs and Communications.

Statistics Bureau of Japan (2026b) Population Estimates, June 2026. Tokyo: Ministry of Internal Affairs and Communications.

Sugiyama, S. (2026) ‘Japan’s real wages extend gains, consumer spending decline slows in April’, Reuters, 5 June.

Yamada, H. (2026) ‘Spring wage hikes signal shift in Japanese economy: But small businesses struggle to meet costs’, Nippon.com, 12 May.

Yamazaki, M. and Sugiyama, K. (2025) ‘In labour-starved Japan, workers land another bumper pay hike’, Reuters, 3 July.

Yamazaki, M. and Sugiyama, K. (2026) ‘Japan firms agree to wage hike of more than 5% for third year, top union group says’, Reuters, 23 March.

Yokota, N. (2026a) ‘5.26% wage hike, fourth straight year of negative real wages—how Japan’s triple squeeze works’, Institute for Social Vision Design, 5 May.

Yokota, N. (2026b) ‘¥1,500 minimum wage target: 45% of SMEs already forced to raise pay, but price pass-through stalls at 50%’, Institute for Social Vision Design, 22 May.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.