The AI Adoption Gap Is Really a Compute Sovereignty Gap

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI adoption measures use, but not control. Europe’s deeper weakness lies in foreign-owned compute, cloud and energy infrastructure AI compute sovereignty requires shared capacity, open access and democratic oversight

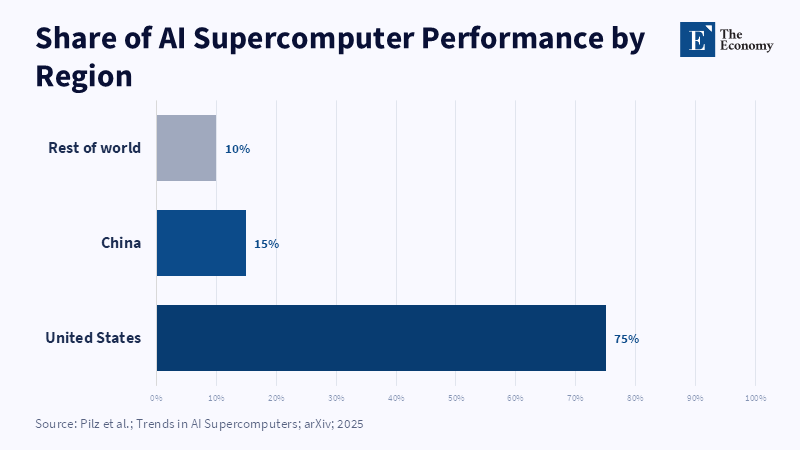

About three-quarters of the world's measured AI supercomputer performance was in the US in early 2025. This fact reveals the future balance of power far better than any count of chatbot users. Much debate focuses on AI's final stage of adoption: how many workers or firms use it. Yet AI adoption rests on a deeper infrastructure base. It comprises chips, power, data centers, cloud firms, networks, capital and law. A state could expand AI use while having nearly none of this infrastructure by becoming a capable buyer of foreign third-party systems. The true policy challenge is thus not AI use per se, but AI compute sovereignty, defined as sufficient control over core infrastructure to protect public choice, sustain critical services and prevent any one foreign supplier from dictating the rules.

AI Compute Sovereignty Is the Missing Measure

Recent survey data reveal a clear US advantage. In early 2026, 43 percent of US employees reported generative-AI use in the workplace. Across six European countries, the figure was 32 percent. Firm data showed a similar trend: 7 percent of American companies used AI in producing a good or service, compared to 4 percent in Europe. Between one-third and one-half of this gap can be explained by the types of workers and firms in different countries. US workers are concentrated in sectors and tasks where AI is being adopted. But work rules also play a role. US firms are more willing to provide their employees with approved AI tools. They are also more willing to support pilots. This is not solely a skills gap or a demand gap. It is a work organization gap.

That narrative is helpful, but it ends too early. A manager can switch to AI only if there are tools, cloud capacity, data and power behind the screen. AI compute sovereignty exposes this deeper layer. It asks where models are trained and where the servers are located. It asks who controls them, which laws apply and who can cut access. Those issues redefine what high use means. High use might reveal local capability. It might also reveal deep dependence on a handful of foreign firms. A survey can make it appear as if both cases are the same. The risks are not. A company might accelerate today, but face high costs later. A country might put AI into public use while shifting its key data onto a system that it cannot fully control. Use data should therefore sit side by side with data on ownership, jurisdiction, power, vendor choice and backup capacity.

Adoption Without Control Creates Dependence

The enormity of top AI systems makes it difficult to ignore this point. A 2025 survey of 500 AI supercomputers found that around 75 percent of total measured computational performance was in the US. The leading system in March 2025 used 200,000 AI chips, cost about $7 billion in hardware and required nearly 300 MW of power. This is not an everyday software system, but a huge industrial facility with the demands of an energy-intensive industry. The survey revealed that the computational performance of leading systems had doubled every nine months, with hardware costs and power needs doubling roughly once a year. While this pace may slow down, such tendencies are likely to persist. The top of AI is linked to huge resources, including scarce microchips, secure sites, cooling, grid connections and lengthy power-purchase agreements; nation-states that cannot access these resources will have little clout in dictating how they are used.

Simply establishing a domestic data center does not itself remedy this threat. A survey of 775 non-US data center projects found that US corporations operated 48 percent of them by planned investment. Planned investment, used only as a proxy for size, is less precise in this context, but the result persists. A location may be within a given state, but its operator, personnel, critical contracts and legal obligations point elsewhere. This is the difference between local hosting and operational control: Europe can host more facilities while still depending on a small number of foreign operators. This same phenomenon can be observed in chips, models, cloud platforms and services. The sovereignty of AI hardware, models and data must be addressed across the entire supply chain; AI compute sovereignty must enable a nation or company to scrutinize the setup, migrate its computing, switch vendors and maintain service continuity during conflict or outage.

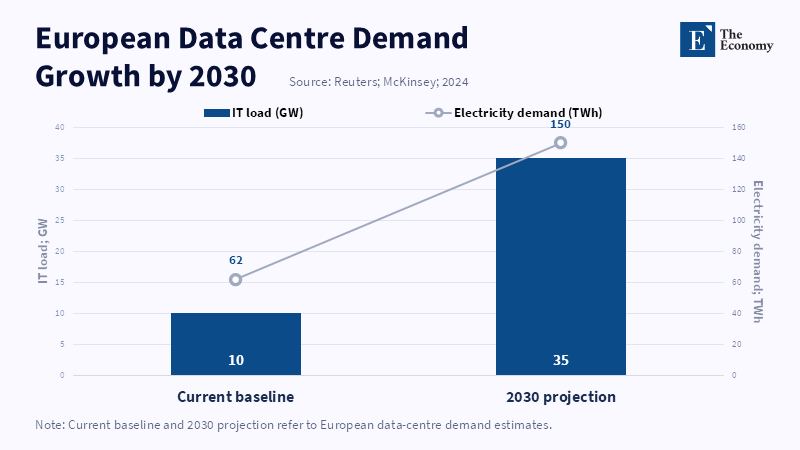

Power imposes another constraint. Data centers consumed some 415 TWh in 2024 -that's close to 1.5 percent of global demand. The International Energy Agency projects that demand will reach about 945 TWh by 2030. Grid access is already a key factor in the location decisions of new AI sites. The UK’s 2025 compute plan made the same constraint clear. "The UK may require at least 6 GW of AI-ready data center capacity by 2030, three times the level then available," it said. AI policy can no longer be confined to a tech office. Grid companies, urban planners, financial executives, security bodies and market regulators all determine the national AI capacity The adoption gap really is a power gap, a land gap, a finance gap and a speed-to-build gap.

Europe Needs a Compute Plan, Not a Copy of America

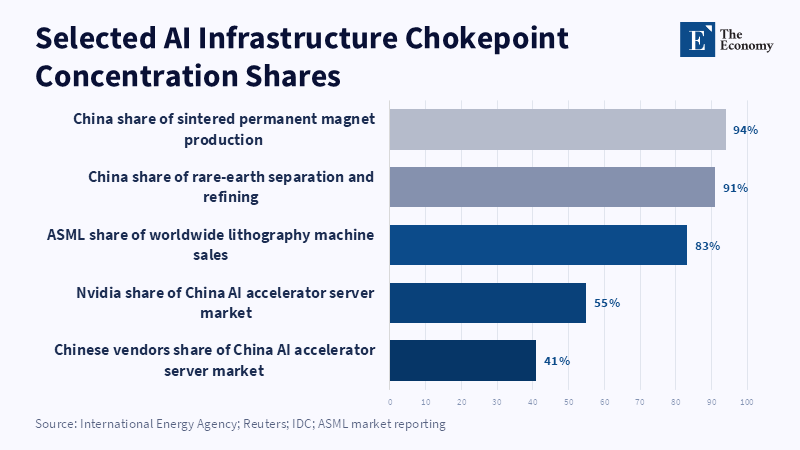

Europe cannot replicate the entire US tech stack. Achieving end-to-end self-sufficiency in all fields of AI would come at too high a cost. Instead, Europe should seek a foundational level of AI compute sovereignty, ensuring sufficient domestic and allied supply to sustain critical services. This requires providing room for leading researchers and true options for businesses. It does not mean isolated markets or prohibiting US cloud companies. Instead, it entails reducing the risk of a single firm, state, or supply route halting essential work. Europe's existing strengths in foundry tooling, factory systems, power equipment, science and parts of the cloud stack should serve as foundations.

Europe is also beginning to reach out. By March 2025, over a dozen AI Factories had been identified under the EuroHPC scheme: the approach being to link large computers with data and support for the end user. That will be a useful starting point. But a string of sites will not build a market: public systems have failed where access is slow, or there is provision of machine time without much assistance with data or code. The real test is straightforward: if the firm finds it easy to transition from a test to production environment, if the public body operates a sensitive model without lock-in, if the business has the capacity to move work if prices or regulation change, then access is at the right level; if not, then while the hosting site may add status, it will not add significant power.

A better approach would concentrate demand before releasing funds to supply. Governments, hospitals, universities, banks, armed forces and major corporations already buy massive quantities of cloud space. Coordinated purchasing could consolidate that fragmented demand into enduring contracts. Public funding should be conditional on targets for low-carbon power, water efficiency, cybersecurity, open access and vendor switching. Contracts would include exit strategies. Public funds should not support isolated national prestige projects that cannot interoperate. Europe should use public money as a catalyst to create a common network with shared standards, spares and a straightforward upgrade path, linking nations and strategic allies with core chip and cloud expertise. It is important for smaller participants. That creates Europe at scale, but without unnecessary duplication.

The cost case deserves a direct answer. Compute costs are high. But so is dependence-and its price. Dependence costs look like sky-high fees, poorly managed data, sluggish research and rushed emergency spending after a shock. The choice is not between public spending and no spending. It is between planned investment now and higher costs later. That downside risk is growing. Even if the supply side is weak, new firms will be delayed and public services will be insecure. Around $52.7 billion was already allocated for chip subsidies and new technology in the US CHIPS and Science Act. Chip supply had grown too crucial to risk relying solely on signals of short-term prices. Europe must fund chip capacity enough to alter where firms locate. Yet those funds would need to be linked to streamlined permissions, firm grid plans and open access.

Europe also needs partners. No democracy manages every aspect of the AI chain. The United States leads in chip design and hosts the world’s largest cloud companies. Europe still has vital production capabilities in chip manufacturing, factory equipment and power infrastructure. Japan and South Korea provide considerable strength in materials, memory and chip manufacturing. A compute compact might tie together these assets. Joint tests can demonstrate whether stopgap measures will prove to be effective prior to an actual shortage occurring. They could host a temporary center, contribute clean power, develop safe communications channels, or operate a trusted public cloud processing operation. This would distribute risk while providing a utility to each other. Confidence must be substantiated. The aim is not absolute self-sufficiency. It is a network in which no single failure can take the entire system down.

A Democratic Bargain for AI Compute Sovereignty

Building more sites also means more local impacts. Bigger data centers can tip the balance of supply, water use, land use, or bills; new sites should meaningfully contribute clean power, energy storage, or flexibility. Market pricing must prevent new demand from shifting unfair costs onto residences and should transparently track power and water consumption. Local communities should share in grid investment, tax revenues, reusable waste heat, or added skills and expertise.

Public oversight must address privacy, security and equitable access. These rules can hold back weaker proposals and accelerate healthier ones. AI compute sovereignty has little value if it weakens public trust. Clear decisions, independent oversight and fair local benefits are needed to secure consent; public support should purchase public value beyond server racks.

Rules must go further than the site and public buyers should know which firms can access or operate a workload. They should receive clear logs showing which people or software accessed or altered their data. They should know where backup copies are hosted and what foreign legislation may have jurisdiction over them. A rule in a contract is not sufficient; market rules should treat open links, transparent pricing and simple data movement as safety features. Security checks should cover remote access, software updates, processors and model supply as one chain. These are the rules that determine who maintains control in the event of a system crash or disagreement. A free system does not mean the state has to own every site. It means the state does have the power to examine, move, replace and govern production services without having to approach a single vendor for permission.

The opening fact should remain the test. In early 2025, around three-quarters of the power for the most capable AI systems was concentrated in a single country. Europe cannot close that gap overnight. Policy must ensure AI adoption never becomes structural dependence. That requires a clear map of critical workloads, coordinated purchasing, faster grid connections, allied chip and cloud agreements and reserve compute capacity that works in a crisis. Governments must track ownership, operational control, grid capacity, vendor concentration and access. AI adoption reveals demand. AI compute sovereignty reveals whether that demand rests on systems a society can still govern and replace. That freedom is at the heart of economic liberty. It will determine growth, safety and public-law scope for generations. Policy must close both gaps.

This article is based on an original research article published by The Economy Research. For the original version, please refer to The Geopolitics of Compute: Sovereignty, Power and Strategic Dependence in the AI Infrastructure Race.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bick, A., Blandin, A., Deming, D.J., Fuchs-Schündeln, N. and Jessen, J. (2026) ‘Mind the Gap: AI Adoption in Europe and the United States’, Brookings Papers on Economic Activity, Spring conference draft.

Bick, A., Blandin, A., Eberly, J.C., Patnaik, S. and Steinsson, J. (2026) ‘Why Is the U.S. Outpacing European Countries in AI Adoption?’, Brookings Institution, 28 May.

Department for Science, Innovation and Technology (2025) UK Compute Roadmap. London: UK Government.

European High Performance Computing Joint Undertaking (2025) ‘EuroHPC Supercomputers Put Europe at the Forefront of Global Supercomputing’, 10 June.

International Energy Agency (2025) Energy and AI. Paris: International Energy Agency.

Phillips-Robins, A., Tawil, T. and Winter-Levy, S. (2026) The Compute Coalition: How to Build the Future of AI in the Free World. Washington, DC: Carnegie Endowment for International Peace.

Pilz, K.F., Sanders, J., Rahman, R. and Heim, L. (2025) ‘Trends in AI Supercomputers’, arXiv preprint arXiv:2504.16026.

Reuters (2025) ‘Global Trade War May Produce Headwinds for Nascent AI Sector, IEA Says’, 10 April.

Richardson, A., Yi, H., Nie, M., Wisdom, S., Price, C., Weijers, R., Veld, S. and Baker, M. (2025) ‘How Sovereign Is Sovereign Compute? A Review of 775 Non-U.S. Data Centers’, arXiv preprint arXiv:2508.00932.

The Economy Research Editorial (2026) ‘The Geopolitics of Compute: Sovereignty, Power and Strategic Dependence in the AI Infrastructure Race’, The Economy Research, 18 June.

United States Congress (2022) CHIPS and Science Act of 2022, Public Law 117-167. Washington, DC: United States Congress.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.