When Everyone Has the Same Adviser: The Hidden Risk of AI Financial Advice

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI can make basic financial guidance cheaper and more personal Its advice often follows life-cycle theory but falls back on rough rules Public standards are needed before guidance becomes automated action

In July 2025, 51 percent of 4,000 American consumers questioned said they had relied on artificial intelligence for financial advice or information within the last three months. That is changing the question. The prospect of mass use is no longer a thought experiment. It is turning into a routine facet of household finance. An early indication can appear promising. An AI device may advise a young employee to improve an emergency fund, make sensible inroads into expensive debt, seek diversification, save cheaply through retirement accounts and finally, reduce investment risk with age. Those are sounder habits than spending every salary increase or buying into popular stocks. Nevertheless, the very extent that creates good habits also creates crude rules, weak facts or hidden errors. Therefore, the central question to ask should not be whether an AI financial adviser can outperform a human one. It should be whether hundreds of millions of households can apply the same small set of approaches without spreading the same financial errors at scale AI financial coaching should be a benchmark. It should not be an unverified code of supremacy.

AI Financial Advice Is Already a Mass Habit

The reasons are plain to see. Traditional financial advice is expensive, unequal and in many instances non-existent for lower net worth households. Chatbots can be accessible 24/7 and provide basic financial guidance. They can break down complex concepts into simple terms, suggest ways of saving efficiently and customize a household's budget for changing circumstances. In 2025, a UK survey found that 56% of adults had consulted an AI for money management in the previous year. That amounted to around 28.8 million people. Of those, 53% reported using AI for savings goals, 52% for budgeting, 39% for future planning and 37% for investment research. A third of this cohort reported seeking advice weekly from AI devices. The critical point is that AI financial support is no longer just a flash in the pan. It has entered people's lives regularly. An information portal accessed frequently is at the forefront of mind when a household contemplates a problem.

This is important because many households behave quite differently from those patient planning agents imagined by standard economic theory. The classic Campbell-Mankiwbar model estimated that about half of disposable income ended up with rule-of-thumb consumers, who consumed in line with current income. That was a measure in income share, not a count of reliably half of all people, but its public policy implications continue to resonate. Households have difficulty bridging living costs over time. The latest evidence suggests the problem persists. For instance, in 2024, only 63 percent of US adults reported being able to meet a $400 emergency expense with cash or equivalents, while only 35 percent of non-retirees felt the retirement saving target was attainable. AI can bring some of these long-term issues to people's attention right at the point of purchase, transfer, or loan decision. The potential is certainly there. As a starting point, the benchmark policy test should be whether AI financial advice enhances discipline, not whether it produces an optimal portfolio.

AI Financial Advice Can Improve Basic Financial Planning

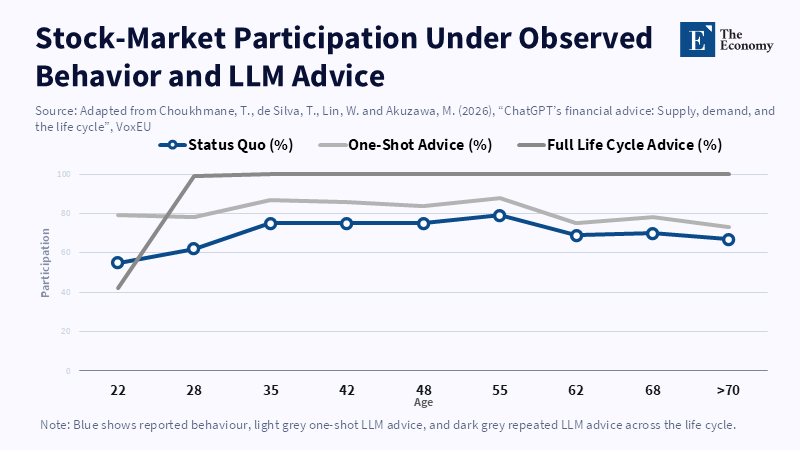

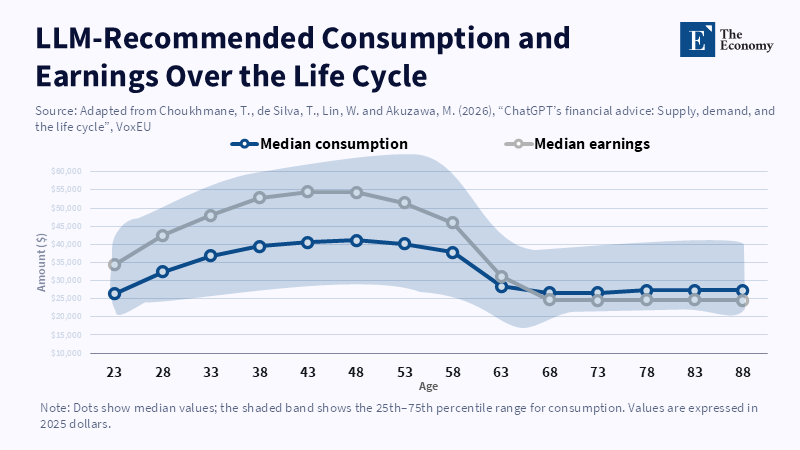

The best evidence suggests cautious optimism. A contemporary life-cycle experiment asked about a thousand US individuals to set out the questions that they would use to guide spending and investment advice. The experimental project then imported those actual questions into a model that simulated the life cycle of households from early in life to retirement. One third of respondents holding no equities, while the average equity share was about 30%. With continuing AI analysis, over 99 percent of simulated households entered the share market, most via a broadly diversified fund. AI-recommended share amounts increased by as much as 40 percentage points, then declined with age. The model also promoted increasingly large amounts of readily available cash. These simulated outcomes were not gains observed in real bank accounts and indicate the potential significance of financial advisors driven by artificial intelligence. They can translate fundamental life-cycle financial principles for populations that would otherwise never crack an economics book.

Other experiments follow the same path, but with limitations. An experiment exploring 32 language models over 64 investor scenarios discovered that most models tailored market and risk appetite to the stated needs of the investors. Historical backtests of the proposed portfolios were similar to industry-standard funds. Larger foundation models also did better at predicting the investor personality. However, some did exhibit home bias and high performances were conditional on the provided profile. Which is the key advantage of AI financial advice: it allows a general principle to be adapted to a specific household. A laborer with irregular income needs to hold more liquid savings than a stable civil servant. A family with a high upcoming college bill does not want to have the same equity risk as a carefree young rental-tenant with no children. Personalization has its merits, but only when the model has access to reliable, up-to-date information.

That condition is often overlooked. A household might ask how much to save each month without mentioning high-interest debt,tax circumstances, pension rights, the risk of losing their job, medical expenses, or plans to emigrate. The model then fills in the gaps with deductions. The answer may seem intimate because it applies to the respondent's salary and age, yet still ignores the factors that determine whether the advice is reliable. This is not always a hallucination. A hallucination is a mistaken report, such as a purported tax law or an incorrect pension ceiling. A heuristic is a rule of thumb, such as saving 10 percent or withdrawing 4 percent each year. The two errors require distinct amounts of regulation. False claims need cross-checking. Heuristics demand context, ranges and definite thresholds. Addressing every weak answer as a hallucination conceals the more general problem: a shortcut can still be wrong for the household in front of it.

The Heuristic Trap Becomes a System Danger

The life-cycle evidence shows how extreme that trap can be. Roughly a third of all recommended savings rates were multiples of 10; more than 98 percent of all retirement drawdown recommendations adhered to the classic 4 percent rule in one version of the study. It also responded badly to job loss. When earnings fell by around half, the model often advised households to cut outgoings to compensate, even where they were holding savings designed precisely to cushion the shock. Portfolios were permitted to meander according to market performance, rather than being methodically rebalanced. They are not wildly inaccurate; they are the well-worn, classic proverbs of popular investment. That makes them more, not less, dangerous. An ultra-confident, proprietary solution can engender distrust. A concise explanation, based on generations of experience, can feel reassuring. Once it is wrapped up in an individualized discussion, the individual concerned may be unaware that it is actually a more or less general principle.

The risk grows at scale. Shared advice can help when it spreads diversification, emergency savings and low fees. The same advice can reduce useful differences when it drives many older users towards assets that have reacted in precisely the same way to the same markets. This pushes many young investors into the same funds. It may repeat the same withdrawal rule despite high inflation or weak markets. This is not to say that advice is the same as given orders and not that each lead will move the market. Households have different incomes, accounts and confidence. However, the trend is there: the Financial Stability Board has indicated how "common" models and data can increase correlation in markets. The pattern is already visible in AI trading. It should now be taken into household advice until chatbots are connected directly to brokerage, pension and bank systems.

Prompt inequality is another dimension. In the life-cycle experiment, wealth at age 60 was about 4-6% lower when advice was based on prompts written by women, people with lower financial literacy or those without prior AI-finance experience. Most of that differential was due to what users asked. Some prompts provided less context or more cautious advice. Some of that differential was also due to the way the model responded to similar inputs. So, gaining access to a model is not enough to offer equally personalized advice. The user who already has the terminology, the knowledge of risks and missing facts will be able to get a better answer. The user who needs the most help will potentially receive the crudest personalization. A free chatbot could therefore lower the cost of good advice while preserving a new divide: not gaining access to the model but gaining the ability to efficiently supply it.

The obvious response is that human advisers are also imperfect. That is true. Audit studies have found that advisers occasionally endorsed return chasing and expensive actively managed funds even when clients had diversified low-fee portfolios. Another study showed misconduct records for approximately 7 percent of US advisers, although at some large firms the rates were much higher. Recent evidence also showed that in one large advisory setting, women were more likely than men to be given recommendations for expensive bank-linked products. These results call into question the purity of human advice as the benchmark. Certainly, they do not show that a chatbot should displace it. Human advisers can pose follow-up questions, detect family discord, carry out legal duties and take responsibility. The appropriate comparator is not perfect human advice versus imperfect AI advice. It is one fragile system versus another.

AI Financial Advice Requires a Public Standard

Policy should start with spelling out the role that is intended clearly from the outset. General-purpose AI should remain as a financial reference layer unless it is operating as a regulated advice system, presenting one choice as the answer. That layer is equipped to highlight options, run test scenarios and help prepare questions. It should not be pressuring a decision at the parcel level. Any true recommendation should display what assumptions were adopted and what facts could not be checked, the date of market data and tax data and one other scenario. The product should complete a structured intake before providing tailored guidance, namely the certainty that income will be maintained, current debt costs, emergency savings, dependents, planning horizon, tax jurisdiction, pension rights and sets of known future expenditure are not optional. The burden of constructing a complete prompt should rest with the system, not the user.

Finally, a single public testing standard should evaluate more than accuracy, whether by helping firms and regulators test predictions by repeated runs, or by urging firms to check the same household profile after model updates. They should also test consumption smoothing after job loss, debt priorities, diversification, rebalancing, retirement withdrawals, fee awareness and the treatment of tax uncertainty. The outcomes should be analyzed by gender, income, age, language and financial literacy. High-stakes movements should be red flags. A model might enable an investor to compare options, but a large pension transfer, leveraged position, or full portfolio sale should require a pause, a new data review and if necessary, expert human supervision. This doesn't inhibit innovation, but it safeguards what is most valuable: cheap, personal, behavior-changing guidance without trying to pass off rhetoric as reasoned judgment.

The opening statistic should now function as a warning and an opening. With 51 percent of customers already using AI for financial information or advice, policy can no longer wait for a definitive judgment on whether machines are better than advisors. AI is becoming the first draft of household choices. Its broad reach could lead millions of people to save more, diversify thoughtfully and think further ahead than their next paycheck; its simple instructions might anchor the common spirit of tens of thousands of households. The policy choice is not blind trust or restriction, but a safe fence around reference and recommendation, based on testing against real household jolts. Any algorithm that might influence money should be able to reveal what it knew and assumed and how its solutions varied with facts. That is how AI can spread household discipline without turning one model into every household’s silent adviser.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Board of Governors of the Federal Reserve System (2025) Report on the Economic Well-Being of U.S. Households in 2024. Washington, DC: Board of Governors of the Federal Reserve System.

Bucher-Koenen, T., Hackethal, A., Koenen, J. and Laudenbach, C. (2025) ‘Gender differences in financial advice’, American Economic Review, 115(12), pp. 4218–4252.

Calvet, L.E., Campbell, J.Y. and Sodini, P. (2009) ‘Fight or flight? Portfolio rebalancing by individual investors’, Quarterly Journal of Economics, 124(1), pp. 301–348.

Campbell, J.Y. and Mankiw, N.G. (1989) ‘Consumption, income, and interest rates: Reinterpreting the time-series evidence’, in Blanchard, O.J. and Fischer, S. (eds.) NBER Macroeconomics Annual 1989. Cambridge, MA: MIT Press, pp. 185–216.

Choi, J.J. (2022) ‘Popular personal financial advice versus the professors’, Journal of Economic Perspectives, 36(4), pp. 167–192.

Choukhmane, T., de Silva, T., Lin, W. and Akuzawa, M. (2025) AI Financial Advice: Supply, Demand, and Life Cycle Implications. Working paper.

Choukhmane, T., de Silva, T., Lin, W. and Akuzawa, M. (2026) ‘ChatGPT’s financial advice: Supply, demand, and the life cycle’, VoxEU, 30 June.

Cocco, J.F., Gomes, F.J. and Maenhout, P.J. (2005) ‘Consumption and portfolio choice over the life cycle’, Review of Financial Studies, 18(2), pp. 491–533.

D’Acunto, F., Prabhala, N. and Rossi, A.G. (2019) ‘The promises and pitfalls of robo-advising’, Review of Financial Studies, 32(5), pp. 1983–2020.

Egan, M., Matvos, G. and Seru, A. (2019) ‘The market for financial adviser misconduct’, Journal of Political Economy, 127(1), pp. 233–295.

Fieberg, C., Hornuf, L., Meiler, M. and Streich, D.J. (2025) Using Large Language Models for Financial Advice. CESifo Working Paper No. 11666. Munich: CESifo.

Financial Stability Board (2024) The Financial Stability Implications of Artificial Intelligence. Basel: Financial Stability Board.

Lloyds Banking Group (2025) ‘Over 28 million adults now using AI tools to help manage their money’, press release, 3 November.

Merton, R.C. (1969) ‘Lifetime portfolio selection under uncertainty: The continuous-time case’, Review of Economics and Statistics, 51(3), pp. 247–257.

Mullainathan, S., Noeth, M. and Schoar, A. (2012) ‘The market for financial advice: An audit study’, American Economic Review, 102(3), pp. 590–600.

White, J. (2025) ‘As more U.S. consumers struggle with rising prices, many turn to artificial intelligence for financial advice’, J.D. Power Banking and Payments Intelligence Report, 28 August.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.