AI Export Controls Need an Alliance Price: Why South Korea’s Submarine Deal Matters

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

South Korea bears real costs from US AI export controls The AI memory boom has provided temporary compensation Submarine cooperation adds a major strategic return

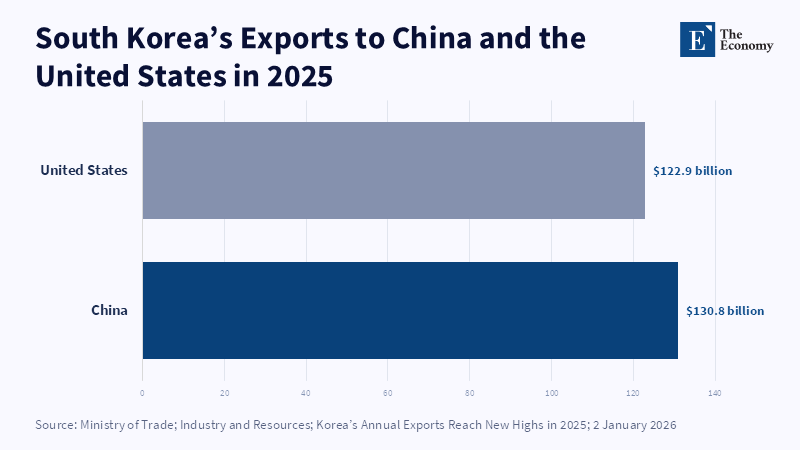

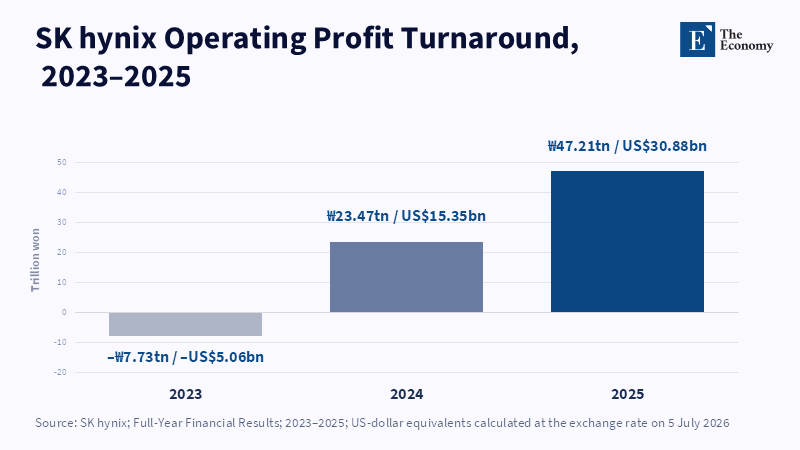

In 2025, South Korea shipped $130.8 billion worth of goods to China. In 2025, three years after the start of the trade deficit with its biggest market, the figure still captures the weak point in the strategic support that Washington seeks in the AI export controls. The policy can be portrayed as a test of strategic obedience. In practice, it amounts to a demand that an ally learn to live with lost sales, idled factories, reduced upgrades and a narrower future in the Chinese technology market. Seoul apparently shares the strategic objective. That support is not free. The spike in AI memory prices has eased the burden temporarily. SK hynix turned an operating loss of 7.7 trillion won in 2023 into an operating profit of 47.2 trillion won in 2025. But a commodity boom is not a treaty and high prices are not a lasting form of compensation. The core policy trade is thus not proving that South Korea supports the US. It is proving that the price of this support has been fairly calculated.

AI Export Controls Need an Alliance Balance Sheet

The key error in the current debate has been to think of export controls on AI as a benign border intervention instead of an alliance tax. Washington writes many of the rules because it controls so much of the supply chains in its software, chip design and fabrication equipment. Yet the economic impact is not limited to American businesses. South Korea supplies the memory required by world-leading AI. Japan and the Netherlands control critical equipment. Taiwan bears much of the capital deployment risk. Every partner concedes a different combination of income, market penetration and investment flexibility. A control may appear focused in Washington while reshaping much of a foreign company's factory plan. That distance matters because export controls work only if allied firms continue to respect them after the initial political signal. To achieve transparency, a resilient system must therefore identify who loses what, when, in return for what geopolitical benefit.

South Korea is the most obvious example because its exposure is both significant and quantifiable. Total Korean exports hit a record $709.7bn in 2025. China was the top destination at $130.8bn, ahead of America at $122.9bn. Exports of semiconductors hit a record $173.4bn and rose by more than 22 percent. These numbers show a country that has not left the Chinese market. They show a country whose growth depends on chips and whose biggest client is still China. Seoul incurred an $18bn goods deficit with China in 2023, then a deficit of about $6.9bn in 2024 and an $11.2bn deficit in 2025. That shift resulted from fewer Korean exports outside the chip sector, rising Chinese manufacturing and the reconfiguration of regional trade patterns. Restricting the sector's exports further would only increase that problem, even if the strategic argument for more controls remained valid.

This problem starts to become urgent now because AI export controls are expanding beyond the most advanced chips. The US December 2024 rules imposed controls on some high-bandwidth memory products and extended the territorial scope of American law through foreign direct product rules. Guidance from May 2026 clearly stated that licensing responsibility can follow Chinese-headquartered firms outside China. The rationale is straightforward. Advanced chips, memory and model access can help militaries in planning and cyber tasks and in conducting surveillance. Adversarial model distillation provides an evasion route in which any licensed party can attempt to emulate the behavior of a more advanced system through mass prompting. However, broadening the control net also entails higher costs for allies. It can block normal commercial activity, increase the cost of compliance and discourage long-term investment. The solution is not the abolition of controls. It is to make clear that allied support is not free.

South Korea Still Has a China Market to Lose

The idea that Korea no longer ships much to China except semiconductors is incorrect. Korea still supplies China with a large share of its petrochemicals, machinery, displays, electronics components and industrial inputs, albeit some of these markets have weakened. More important is the fact that this trade has become less symmetrical. Korean exporters once supplied China with many of the parts that facilitated China's industrial rise. Today, Chinese firms compete with Korea in batteries, steel, chemicals, displays, vehicles and machinery. Conversely, Korea is increasingly importing finished and intermediate Chinese goods while struggling with non-chip exports. Semiconductors are now the stabilizer in a relationship that is otherwise turning unfavorable for Korean producers. It is precisely for this reason that export controls over AI products will have an impact beyond one product category. If access to the chip market is tightened, Seoul will have lost one of the few domains in which it previously enjoyed substantial pricing power vis-à-vis China.

That does not mean that every semiconductor sale should continue. High-bandwidth memory is not an ordinary good. It is at the heart of next-generation accelerators and of large AI systems. Washington is correct to focus specifically on those stages in the chain that best support frontier computing power. It is also correct to eliminate obvious diversion paths through offshore entities. But controls must be restrained. A broad-brush rule where mature memory, regular equipment maintenance, or low-risk customers are concerned will penalize allied companies without a commensurate security benefit. It may also accelerate China's drive towards foreign equipment independence. The best policy is a narrow, well-defined line: clear technical thresholds, public licensing requirements, fixed-length review periods and stable treatment with allied factories already in China. Uncertainty itself is an economic cost. It is easier for a company to adapt to a ban when the ruling is clear, rather than having to guess what it will be in six months' time.

The problem is the Chinese plants that Samsung Electronics and SK hynix own. These locations are the outcome of years of sunk capital and support large shares of the world memory market. Washington has signaled that existing operations will be kept alive via licenses, while expansion and major upgrades will be subject to tighter restrictions. This may delay the changeover of technology, but it also leaves South Korean firms with legacy assets that will take years to amortize. A fair partnership strategy would need to make a distinction between halting new leading-edge capacity in China and forcing allies to devalue longstanding investment rapidly. The former can be a security decision. The latter is a hidden transfer of wealth from a business partner to a policy-maker. If the US hopes Seoul will back that loss, it should make the exchange clear by providing replacement capacity, demand guarantees, tax incentives, or other key strategic assets.

The AI Memory Boom Has Paid South Korea, but Only for Now

The best argument against a formal compensation package is that the market has already done the job. There is real substance behind that argument. Global semiconductor sales hit almost $796 billion in 2025, up by more than 26 percent. Computer-related demand grew by more than 60 percent as data centers and AI systems drove a massive increase in orders for logic and memory. Korea's chip exports hit $173.4 billion. SK hynix, the leading Korean memory producer, produced one of the most dramatic turnarounds in recent history. It turned its 7.7 trillion won operating loss in 2023 to a profit of 23.5 trillion won in 2024. It doubled that again to 47.2 trillion won in 2025. The company linked this result to high-value AI products from HBM to server memory. Demand from American cloud companies and chip designers helped drive the recovery, even though the final trade flow passed through Taiwan or another assembly hub.

This boom shifts the political balance. South Korea has not just sacrificed its China sales. Its top memory producer has reaped enormous US dollar-denominated gains from the AI expansion led by America. Higher prices have also boosted its trade position. In early 2026, the monthly trade balance with China turned into a surplus. By June, total Korean semiconductor exports were almost three times what they were this time last year, with exports to both China and the US. In that narrow sense, the alliance bargain has succeeded. The US has limited some Chinese access, while the US-based AI investment cycle has raised the value of memory sold elsewhere, providing useful indirect compensation. Clearly, this is a form of indirect compensation that is even more powerful than simply remitting cash to a government, since it rewards technology, scale and delivery, not just political cooperation.

Still, a price boom cannot sustain alliance policy. Memory markets are cyclical. Today's scarcity can become tomorrow's glut. Customer concentration can also give rise to a new dependence. Export controls on AI should have at least a standing allied adjustment system. It doesn't have to pay firms for every abandoned order, but it should support predictable access to US demand, accelerate approval of allied investment, fund joint research, provide equal tax treatment and pay the firm to relocate equipment away from restricted sites. Affected firms should also be paid for demonstrated loss, but without providing a blank cheque. However, allies should not have to hope for the next AI wave to come on schedule.

The Submarine Deal Is Part of the Price

This aspect of the bargain is not financial at all. In late 2025, Washington approved Seoul's pursuit for conventionally armed, nuclear-powered submarines and agreed to talk about fuel and other requirements. The result was South Korea's nuclear-powered submarine program, with the first vessel targeted for the mid-2030s. There is no explicit statement in either agreement that this acts as payment for a semiconductor agreement. It would be wrong to say it is an established one-for-one exchange. But strategic bargains rarely are. The approval came in the course of a wider period of trade, investment and security negotiations. It provided Korea with something it had wanted for years. It met an essential national interest that money by itself could do nothing about. In alliance accounting, that makes it part of the compensation package, whether officials choose to put it that way or not.

The defense benefit is real but should not be overstated. Nuclear propulsion allows submarines to remain submerged for longer patrols, sustain high speeds without having to surface and recharge batteries. The result is increased survivability, longer patrols and the ability to monitor North Korean submarine and missile tests. It would also enable Seoul to extend its undersea reach and share some of the burden now borne by US vessels. Two or three such boats would not make an invasion impossible. They would not obviate the need for air power, satellites, anti-submarine aircraft and sensors, or conventional subs. But they could complicate North Korean commanders' calculations and provide Seoul with a more permanent tool for observing coastal and undersea activity. That is not a symbolic gain. For a country with a nuclear-equipped neighbor, the capability is long overdue.

Critics will say that linking submarines to AI export controls fuels risky strategic bargaining. They will cite proliferation, the costs and an Asian undersea arms race. Those threats are real. The project, still requires a separate legal route for military-use nuclear fuel, policed by tough safeguards and a hard ban on nuclear weapons. It would take years and probably far more than its forecast costs. But those fears do not negate its rationale. Washington wants South Korea to bear more of the regional burden while blocking China's access to advanced computing. A conventionally armed submarine project can play both those roles. It offers Seoul a prized sovereign defense capability while strengthening the US alliance in the undersea realm. There may be a safer path. But it is not to hide the exchange. It is to accept it publicly and impose non-proliferation measures, cost limits and a unifying purpose.

AI Export Controls Must Price Allied Sacrifice

The broader lesson is this. AI export restrictions cannot be based on orders from Washington and quiet losses in allied capitals. They need an alliance balance sheet. For South Korea, that balance sheet already lists three items: less room in China, record profits from the AI memory surge and a strategic possibility of developing nuclear-powered submarines. While the current balance appears favorable, it is not immutable. Prices can collapse. Licenses can freeze. Submarine approval can stall in Congress or in nuclear diplomacy. Washington and Seoul should therefore institutionalize the informal bargain into a lasting structure. Limits on the export of AI should be narrow and stable. Verified losses should activate economic adjustment measures. Credible security gains should be long-term and legally ratified. The opening figure remains the benchmark: US$130.8 billion of Korean exports to China is not a detail. It is the market risk driving the policy. An alliance that prices that risk honestly will endure. One that considers it a debt of loyalty may not.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Alexis (2026) ‘AI geopolitics: Washington’s AI kill switch broke the alliance’, AI Weekly, 21 June.

Bureau of Industry and Security (2024) ‘Commerce strengthens export controls to restrict China’s capability to produce advanced semiconductors for military applications’, US Department of Commerce, 2 December.

Gupta, R., Walker, L. and Reddie, A.W. (2024) ‘Whack-a-chip: The futility of hardware-centric export controls’, arXiv preprint, arXiv:2411.14425.

Lee, J. (2026a) ‘South Korea exports post strongest growth since 1978 on AI chip boom’, Reuters, 1 July.

Lee, J. (2026b) ‘South Korea aims to launch first nuclear-powered submarine by the mid-2030s’, Reuters, 26 May.

Liu, J. and Lee, J.-A. (2026) ‘Strategic stalemates: The paradox of export controls in the US–China AI race’, arXiv preprint, arXiv:2605.23475.

Lopes Maldonado, M. (2026) ‘The United States needs a strategic response to adversarial AI distillation’, Center for Data Innovation, 26 June.

Ministry of Trade, Industry and Resources (2026) ‘Korea’s annual exports reach new highs in 2025’, Government of the Republic of Korea, 2 January.

Nellis, S. (2026) ‘Global chip sales expected to hit $1 trillion this year, industry group says’, Reuters, 6 February.

Park, S. (2026) ‘Washington needs allies to make AI export controls work’, East Asia Forum, 26 June.

Republic of Korea Ministry of National Defense (2026) Basic Plan for the Development of Nuclear-Powered Submarines. Seoul: Ministry of National Defense.

SK hynix (2024) ‘SK hynix reports fourth-quarter and full-year 2023 financial results’, 25 January.

SK hynix (2025) ‘SK hynix announces fourth-quarter and full-year 2024 financial results’, 23 January.

SK hynix (2026) ‘SK hynix posts record annual financial results in 2025’, 28 January.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.