China’s Subsidy Model Is Turning Growth Into a Political Liability

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

China’s tech-led growth shift is real, but its subsidy model is creating political backlash Europe now sees Chinese overcapacity as a trade and security problem Without fairer competition, China’s growth will face stronger barriers abroad

By 2025, the EU had imported 559.4 billion worth of goods from China, and exported to China only 199.6 billion. The rate was €359.8 billion. That is not a mere statistical figure. It is a political signal about power. China has shifted from a property-led boom to jobs in construction and real estate toward much more capital and innovation-intensive activities: advanced manufacturing, clean tech, batteries and electric vehicles, robotics, and data-intensive industries. Such a transition has implications for the entire globe. It can bring prices down, accelerate the green transition faster, and set higher standards for factory output. But China's industrial subsidies have altered the promise of such a transition. They not only strengthen the Chinese firms but also distort the dynamics of competition. And that has become clear in Europe and elsewhere. The more China resorts to a subsidized economy of scale, the more its growth exerts political costs.

Subsidies Are Changing The Meaning Of Growth

China's transition, as a matter of course, should not be used to define a threat per se. Large economies are entitled to transition away from cement, housing, and simple exports and upgrade into capital and more sophisticated manufacturing. The official data confirms this transition: in 2025, investment in real estate declined by 17.2%, while investment in manufacturing still increased by 0.6%, 3.5 percentage points above the overall growth. Industrial value added was 5.9 percent. High-tech manufacturing was 9.4 percent and equipment manufacturing was 9.2 percent. Production of new energy vehicles in 2025 was 25.1 percent above the previous year's level. Exports of high-tech products were 13.2 percent above the previous year's level. These absolute figures demonstrate a policy choice. Beijing is working harder to replace the excess land, leverage, and infrastructure-driven economy with a capital, patent, battery, electric vehicle, and big data-driven economy.

That change is a global good. Cheaper Chinese manufacturing has reduced the costs of solar panels, batteries, consumer electronics, and many industrial inputs. Cheaper Chinese production has also intensified the competition faced by slow firms in Europe, Japan, Korea, and the US. This part of the story is not unfair. Productivity growth should pressure weaker producers. Consumers are better off when prices fall, especially on green goods. Climate policies are better off when clean equipment is cheaper. The difficult question is different. Is all of China's advantage still attributable to the accumulation of scale, experience, and efficiency, or is it instead driven by a government-enabled system that drives down the costs of capital, sustains excess capacity and export dumping, and shifts the pain to offshore competitors? And this is where China's industrial subsidies take center stage.

Industrial Efficiency Is Becoming Political Risk

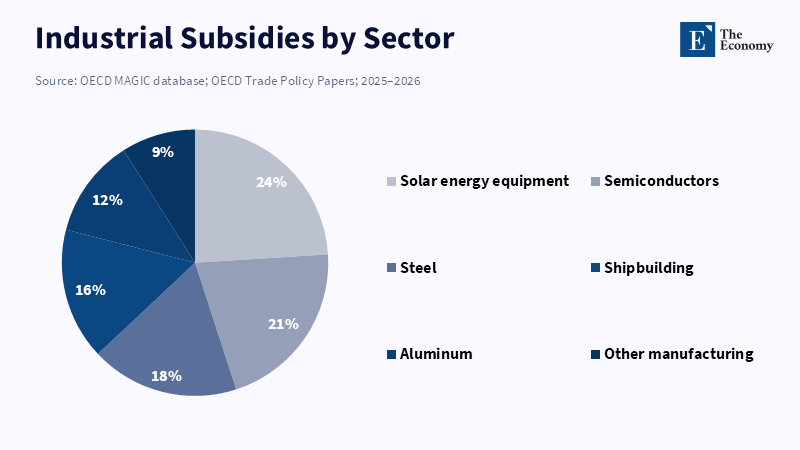

Newest evidence now points to a global investment subsidy event of significant magnitude: According to the latest OECD's 2026 MAGIC database, global industrial subsidies amounted to the unprecedented sum of US$108 billion in 2024, and have been surging since the latest global crisis. Among the highly subsidized sectors in 2005-2024 were solar energy equipment, semiconductors, aluminum, steel, and shipbuilding. Not just peripheral, modest industries. The essential process industries of the forthcoming premier trade governance. The same OECD piece also reports that Chinese-based manufacturers receive proportionately and substantially more support than their closest rivals based in other jurisdictions, mainly by way of grants and subsidized loans. This is important as these artificially-squeezed, below-market-rate finance distort production costs by hiding the true expense, and distort product markets by enabling the same for prices.

More fundamentally, subsidies do not always lead to true productivity. OECD's econometric work in 2025 finds that subsidies raise firms' global market shares but have no or negative impacts on investment and productivity. This is the most damaging point in China's case. If these subsidies made firms more productive, the political backlash would be weaker. But if it mainly helped firms get shares, lower prices, and scare rivals from investing, the case of China's industrial subsidies is not merely economic. They remain a political bother. Foreign governments will stop thinking of Chinese exports as normal competition. They will think of them as the outward expression of the domestic state. And this turns each cheap car, panel, battery, and machine into a political row.

Europe Is Moving From Openness To Retrenchment

Europe's response is no longer hypothetical. In 2024, the European Commission applied final countervailing duties on Chinese battery electric vehicles for five years. The rates were 17.0% for BYD, 18.8% for Geely, 35.3% for SAIC, 7.8% for Tesla Shanghai, 20.7% for other cooperating firms, and 35.3% for non-cooperating firms. The EC found that the investigation showed unfair government subsidies in the Chinese battery electric vehicle production chain and a threat of injury to EU producers. This is noteworthy as it sets a policy precedent. The EC is not implying that Chinese firms may not gain market entry; only that subsidized competition on a manufacturing scale should not be treated as ordinary market competition.

The trade numbers make the politics even more trenchant. Eurostat figures show that the EU’s goods deficit with China stood at €359.8 billion in 2025. In the first quarter of 2026, the deficit reached €98 billion, the highest quarterly gap since the third quarter of 2022. The big categories are machinery, vehicles, electrical equipment and manufactured goods. This is not an indication that all Chinese exports are unfair; it does explain why European forbearance is waning. Even a large deficit can be sustained when two parties view the arrangement as a level playing field. It is less sustainable when one party feels it is being heavily subsidized by state-backed capacity. Such a view now underpins the European debate on cars and chemicals to clean energy and digital platforms.

European actions today show how much the mood has changed. The EU’s review of JD.com’s proposed acquisition of Ceconomy reflects a broader effort to stop foreign state support from distorting the single market. At the same time, Europe is easing pressure on its own heavy industries through free emissions allowances as energy costs, weak demand and Chinese supply gluts squeeze factories. This is the political cost China is underestimating. Subsidies do not only attract tariffs. They invite investment screening, merger barriers, carbon rules, procurement limits, anti-circumvention tools and industrial rescue measures. Once trade becomes a security issue, China loses the soft legitimacy that once made its exports easier to accept.

Subsidies Need Rules, Not Retaliation

The most serious criticism is surely that Europe and the United States also subsidize. Certainly. Tax credits, tariffs and industrial laws have been used in the US. Green funds, free emissions allowances, or support schemes at the national level are examples in Europe. However, this does not wipe out the China problem. It simply changes the policy test. The question is not debating whether subsidies are present, but whether they are clearer, limited, tied to public targets and constrained by market exit. An early demand renewable subsidy does not have the same implication as an artificial capacity scenario once the demand is saturated. A back-end temporary grant does not make the same impact as years of subsidization below-market. A transparent US tax credit does not have the same impact as hidden local support, subsidized state-bank loans, cheap land, or directed procurement schemes.

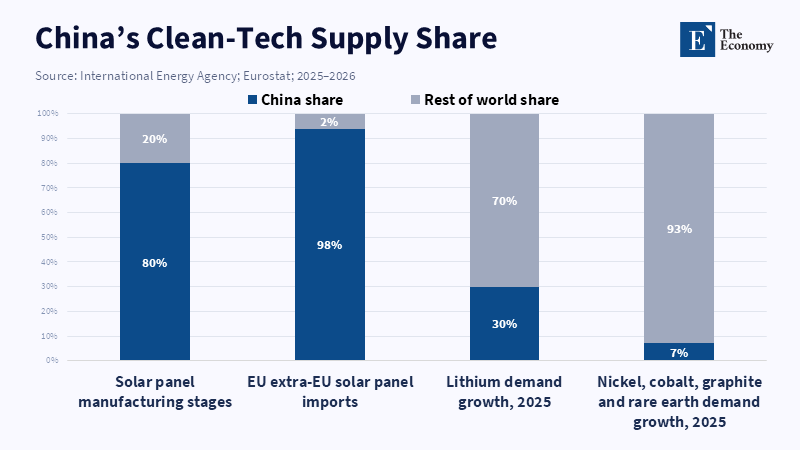

The problem for China is not just that it subsidizes. It is that subsidized growth continually turns up abroad as too much capacity. The problems with solar panels reveal the danger. The International Energy Agency found that in every significant part of the value chain, China's market share in the production of solar panels is over 80 percent. Eurostat found that 98 percent of EU imports of extra-EU solar panels in 2024 came from China. Abundant, cheap panels advance climate objectives. But such near-total reliance discourages industrial options. The same was true for key minerals. In 2025, lithium consumption increased by almost 30 percent, while demand for all other key minerals of nickel, cobalt, graphite and rare earths increased by 6-8 percent. When China tightened control over exports of rare earths and magnets, global automakers and their suppliers alerted the world to looming shortages and a standstill. Price is no longer the whole story. Control is.

Policy response should not default to protection at any cost. Such tariffs would drive up costs, slow climate investment and impose costs on consumers. It would also shelter weak domestic industries from reforms needed to foster innovation and productivity. The optimal approach is to tailor protection according to the criteria of market viability. Markets should be protected against dumping of excess supply if they are competitive and supplied by multiple sources of low-cost supply; they should be protected when state support is creating excess capacity; they should be protected if they supply a critical input that cannot be substituted in a timely manner; sectors important to the energy, military, transportation, health and information systems should be protected if they are overwhelmingly supplied by a single country. Trade remedies should also be faster and more discriminating. Anti-subsidy measures should be based on the presence of harm, not on preference; rules of origin should, in effect, incorporate measures of imported input dependency at the second and third tier rather than at the final point of entry.

For policymakers, the challenge is to separate cheap trade from unfair trade. That requires the right evidence, not the loud slogans. Customs data needs to be integrated with evidence on subsidies, capacity, prices and firm injury. Public officials need to start thinking of resilience not as a line on a speech but as a budget item. If a country wants certain types of batteries, magnets, chips, or clean equipment to be secure, it has to pay for capacity ahead of time. That means long-term purchase contracts, speedier permits, collective stockpiles, recycling mandates and support to allied supply. It also means a clear rule to not subsidize every losing firm or to politically block a strong foreign firm. The distinction must be bright and transparent. Subsidized effort is fine when it is the result of competition. Hard to explain and even harder to rationalize when it is determined by secret support and the losses are exported.

China must choose restraint before barriers Fair Competition Must Come Before Barriers Harden

That is a choice China must make. It can continue to argue that the surge in exports and China’s high savings are due to transitory protectionism, but every year that argument becomes less convincing as the erosion of rivals occurs, with surging supply, collapsing prices, hurting trading partners and the political backlash. Or China can recognize that a large and growing economy requires some restraint. A less distorted future would incorporate more complete declarations of subsidy, tighter local-government credit control, real bankruptcies of weak companies and exporting that is not weaponized. That would not damage China’s strongest companies; it would bolster confidence in their market dominance. And that is what China needs most.

The world does not need China to cease to grow. It needs China to cease to export the political costs of how it grows. A construction-led China previously ferried steel, cement, land and debt through its own economy. A tech-led China now ferries batteries, panels, cars, machines and standards around the world. That is a much greater challenge. If China's industrial subsidies remain the hidden engine of this transition, the next phase of globalization will become even more inward-looking, with barriers to entry hardening around it. The United States has already taken the plunge. Europe is now moving in its wake. Other advanced nations will also follow. The danger for Beijing is not that its rivals will fail to grasp the new phase in China's growth. It is that they will grasp it a little too well and decide that liberalization without fairness is not worth the cost. That cost is now rising.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Delaney, S. (2026) ‘Facing the Loss of Europe After America: EU Raises Barriers Against Chinese Low-Cost Exports as Beijing’s Subsidy-Driven Economy Faces a Boomerang Effect’, The Economy, 1 June.

European Commission (2024) ‘EU Commission Imposes Countervailing Duties on Imports of Battery Electric Vehicles (BEVs) from China’, Access2Markets, 12 December.

Eurostat (2026) ‘Trade in Goods with China in 2025’, Eurostat News, 10 April.

Eurostat (2026) ‘EU Trade with China — Latest Developments’, Statistics Explained.

Hansbrough, T. (2026) ‘“From Fines to M&A Roadblocks”: EU Raises Regulatory Barriers Against Chinese Companies While Loosening Restrictions on Intra-European M&A’, The Economy, 29 May.

International Energy Agency (2022) Solar PV Global Supply Chains. Paris: International Energy Agency.

International Energy Agency (2025) Global Critical Minerals Outlook 2025. Paris: International Energy Agency.

Millot, V., Rawdanowicz, Ł., Sauvage, J. and van Lieshout, E. (2025) ‘The Market Implications of Industrial Subsidies’, OECD Trade Policy Papers, No. 296. Paris: OECD Publishing.

National Bureau of Statistics of China (2026) ‘National Economy Pushed Forward with Innovation-led and High-quality Development and Expected Targets Achieved Successfully in 2025’, 19 January.

Nicholson, A.-M. (2026) ‘EU Expands Free Carbon Allowance Allocations for Industry, Pressing Ahead with Preferential Support for Domestic Companies Despite Potential Trade Frictions’, The Economy, 1 June.

Organisation for Economic Co-operation and Development (2026) OECD MAGIC Database of Industrial Subsidies. Paris: OECD Publishing.

Shepardson, D. and Martina, M. (2025) ‘Car Makers Warn China’s Rare-Earth Curbs Could Halt Production’, Reuters, 30 May.

Waldersee, V. and Steitz, C. (2025) ‘China’s Rare Earth Export Curbs Hit the Auto Industry Worldwide’, Reuters, 4 June.

Zhou, Y. (2026) ‘China’s Growth Transition Has Global Consequences’, East Asia Forum, 26 May.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.