Liquidity Stability, Not Static Liquidity, Is the New Fault Line in Digital Banking

Authored on

Modified

SVB failed because its funding was unstable, not just illiquid In digital banking, stability matters more than static ratios Banks must plan for speed, panic, and rapid outflows

Within a day, the deposits of SVB's customers had been pulled out of the bank by more than $42bn, nearly a quarter of its total deposits. The senior management anticipated that another $100bn could be pulled overnight. And this timeand here was no run,of,the,mill cash crunch: it was a failure of liquidity's stability. The bank, constructed through days of stress, had a funding base that could be emptied virtually instantly. Today in digital finance, liquidity no longer constitutes a portfolio of cash, reserves, and low-risk reserves: it is a race of how fast assets can be exhausted, of depositors' centrality, the quickness of information passing from person to person, the speed of CEO, CIO, and CFO decision making. A bank may still excel with traditional ratio analysis, yet fail to be equally robust if it is uninsured, catered to one special sector, or reliant on clients who share investors, information sources, and habits. That redefines the notion of a solid balance sheet. The challenge isn't just who has cash on paper, it's who has liquidity stability when confidence drops on the floor.

Liquidity Stability Is a Market Structure Variable

The standard or 'textbook' story of SVB is one of duration heading to a bank run, which describes what happened, but not entirely correctly. The key explanation is simply that liquidity went out the window first because funding didn't stay stable. This is what links the UK gilt market LDI event and SVB, though in vastly different parts of the financial system, both were on the same problem. As interest rates rose, corporate cash requirements outpaced the buffers available to meet them more rapidly. Clearly, in the UK, pension structures looked solvent, but were unprepared for the unexpected anticipation of margins and collateral calls. And in California, losses on their bonds led investors to suspect the worst and pull their cash at the worst moment. In both cases, however, the problem wasn't not having enough assets, but rather a lag in the obligation delivery rate vis,à,vis what's available in the way of liquidity.

In other words, liquidity was a structural market problem, not just a treasury one. SVB's deposit base was large, unsecured, but also highly concentrated within one venture ecosystem: clients shared investors, saw similar indicators, and were affected by a small group of trusted voices. More than 94 percent of deposits were unsecured at the end of 2022. Under those circumstances, time wasn't likely to correct the problem, only the speed of a possible collapse. Digital, in this instance, was only speeding up the collapse of an already fragile funding structure. It wasn't nearly 23cpa's ability to use their phone that was so damaging, as they all had their own, and far more disturbing was why that particular group all knew the reasons at the same time to do so.

And this matters because stable funding has become essential to product success: a deposit franchise's worth hinges not only on its size or its costs, but on the diversity and hence, the robustness of its bases: Customers whose cash needs happen to be uncorrelated. Firms that equate client intimacy with fund stability are making a serious mistake. Private bank lenders, crypto banks, and private bank wealth marketers may all grow rapidly by way of a handful of trusted clients. But they don't have stability on that account: private bank investors who are uninsured, highly informed, and accustomed to swift withdrawals view loyalty as yet another opportunity to move their money and are not exactly a reliable source of stable funding. Today, a franchise's quality is no longer reflected by average balances, but by the risk of same-day withdrawal.

Why Static Ratios Fail to Capture Liquidity Stability

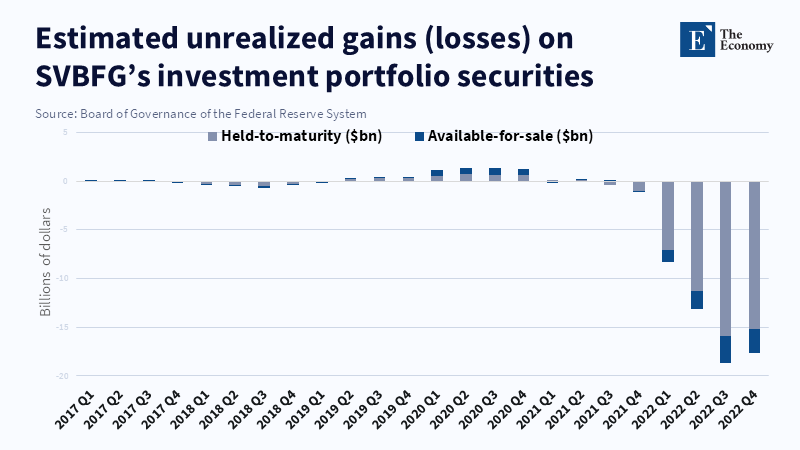

This is the pitfall of regular ratio analysis. In the post-mortem analysis by Greg Feldberg, had that been the mandated Liquidity Coverage Ratio, the LCR of SVB at the end of 2022 would have been only 75 percent, well below the 100 percent that would have kept its fingers away from the flames. That makes a persuasive case for more regulation and monitoring. But the same by Greg Feldberg also laid bare a crucial insight. Following the LCR alone would not have fixed the core problem at SVB. One can make the ratio look better by moving assets around into financial instruments, still accounting as high-quality liquid assets, but still at the mercy of fair value declines, confidence shocks, and an unwillingness to liquidate assets below their face value. A ratio can expose inadequate preparation, but it does not tell you when it becomes unmanageable.

In the same way, the Net Stable Funding Ratio suffers from the flip side of it. Using Feldberg's own subsequent calculation, SVB's NSFR would have been at 132 percent, well above the minimum. That should have been a comfort. Instead, it is proof that the scheme missed the one best indicator. In a bank that had seemingly strong funding, ultimately, there was failure because the market didn't see that funding as stable in a time of stress. The insured wholesale deposits were too lightly regulated. The assets held to maturity were too lightly regulated. It was assumed that depositor reactions would be slower, less networked, and less organized than they are in fact. The moral to draw isn't that ratios are useless. It is that, in companies where an abrupt rush for cash is possible and likely, absolute liquidity ratios won't be enough.

And this is the policy lesson. It's not just SVB. Static regulation relies on buckets, averages, and runoff rates based on previous stress tests. Funding crises in the digital age emerge differently. They focus on clusters, thresholds, and instant coordination. A regulation paradigm for a 30-day stress test might be helpful. But it will avoid firms whose default is caused by intraday moves rather than month-long attrition. And the next realm of capital thinking needs to straddle a little more closely with market structure. What needs to be asked is: What assets are liquid and can therefore be pledged or sold quickly without signaling trouble, how fast can that be, and is the liabilities side expected to shift before the managers do? Speed has become key to stability.

Who Reaps the Benefits When Liquidity Stability Is Absent

Once deposits can move at the pace of group messaging, the leverage of banking also moves. Investors who know they are going to have huge uninsured deposits have leverage. Venture capitalists, corporate treasurers, and certain informational nodes can have outsized power over cash flows. Equity and bond markets accelerate the deposit response rather than simply playing it back. Analysis of SVB and the combined regional bank strain found that banks with more previous susceptibility to Twitter faced a 4.3 point drop in value during the run. However, the most recent granular research also warns against an overly simplistic social media narrative. European Central Bank analysis shows that digital activity slightly increases extreme outflows in crises, but does not increase deposit volatility during normal times, and the social media effect is most severe in certain moments. Research from the Chicago Fed also finds that apps alone are not able to explain the speed of the 2023 collective withdrawals because large depositors could previously move their money instantaneously. The best answer is somewhere in the middle. Technology makes withdrawals faster, but those withdrawals are only sensible when the institution is at risk.

This migration of power changes the way in which participants in the sector produce wealth. The winners are not the largest institutions. They are the ones that can combine scale with a breadth of funding base, reliable avenues of communication, and speed of execution. These benefits exist in firms with ho-hum, accepted payment streams, broad retail footprints, or large balance sheets that can sustain momentary depletion of confidence without appearing to be impaired. The losers are not all those financial institutions with narrow, heavily client-dependent story lines that don't understand that client dependence does not create funding durability. In the old economy, specialization might have allowed a professional independence from the sector. In today's world, specialization may only increase the risk of a run. In today's world, banking competition is not limited to service and spreads. It includes trust in survivability in a showdown.

And this has real commercial effects. A sector,specialized institution, under this new world ordering, faces a higher baseline cost of funding than was envisioned in the classical model, even if its deposit costs are cheap in a blissful lull. Resources, new capital, costs, etc., are needed to maintain the right liquidity profile. More buffers, more sympathetic Treasuries, better hedges, better depositor umbrellas, better collateral management, better communication, adding to costs and limiting deposit premiums, thereby limiting profitability, or requiring bigger deposits elsewhere to fund the deposit base, thereby limiting profitability. The juice has come from the big, existing universal banks, the banks in payments, the banks with the thickest retail plots. Smaller banks have a fighting chance. Regardless, a sector specialist today understands that sector concentration is no longer a means to an end for a bank. It is the cost of a bank. Other financial players, though not all, have adjusted a little in the face of this reality. The Fed noted in spring 2025 that most U. S. banks had high-quality liquid assets and stable funding, and dependence on uninsured deposits was down from the high in 2022–early 2023. Still another “but,” however, the FDIC recorded a bump of $214.7bn in uninsured domestic deposits between the end of 2024 and the end of 2025 quarters. Things are settling down, but it isn't totally costless or done.

What Banks, University Treasurers and Policymakers Should Assess Going Forward

The answer isn't to abandon liquidity standards but to stop assuming they are enough. A new set of indicators around liquidity end stability needs to be introduced by banks and supervisors. That means monitoring of the concentration of uninsured deposits by type of customer, overlaps in the deposit book, the percentage of balances that might exit within 24 hours, the maturity structure of presumed, liquid assets, the duration of collateral pledged and the likelihood that fast communication can generate renewed concern. It means asking if a contingency measure is really effective in a single day rather than just plausible in a month's time. The Financial Stability Board has already alluded to this. It warns that digital media and social networks could hasten future withdrawals and that financial firms and regulators may need to operate at a more rapid pace than even they do now. That's a wise concern. The next step is to bake that hunch into daily supervision, enhanced transparency, more rigorous pricing and stress tests that assume synchronized withdrawal behavior rather than linear averages.

Beyond SVB,there is another lesson this episode is supposed to convey. It's not that we shouldn't have liquidity standards. It's that we shouldn't pretend they are enough. It is to authorize and mandate, together with prudential indicators, a second try ahead of the first that will consider the adequacy of liquidity leniency. This entails monitoring the one's of well,defined age demographics, the granular concentration in uninsured deposits, the deposit overlap, the proportion of always,ready balances, the maturity schedule of ostensibly ready assets, the speed of ready collateral turning into pledged collateral, the feasability of making the second try within hours instead of single,mindedly calming worried neighbors for a month. The G20 Financial Stability Forum's report has already hinted in this direction. It issued contingencies for the enhanced intraday velocity of digital payment and social media outlets, pushing a future run on banks, and for whether the industry and authorities could converge sufficiently faster. That is the aptitude. The subsequent step is to convert that academia into a permanent supervisory identifier, a familiar messaging topic, and a new pricing rule, instantaneously, attempt stress tests based on concurrent withdrawals, instead of the hogwash of historical averages.

It should be a lesson learned by every business school as well as every senior executive training seminar, which is why liquidity debates should not be left for bank treasurers or prudential authorities alone. Traditional finance courses continue to promote liquidity as if by rote, with the central learning being how to memorize ratios and rank assets. That is far from enough. The instability of liquidity continues to be an essential topic of every professional course in banking, treasury, endowment management and pension fund oversight, because in each case the timing challenge is the same. University finance boards, endowment fund departments and pension trustees should consider the UK LDI incident in parallel with SVB. A balance sheet can seem clean and solvent while being highly vulnerable, if the collateral has to be moved faster than the system, governance and counterparties can handle. The Bank of England's brief repo backstop during the LDI crisis was a civilized slapdown, reminding everyone that failures occur not just for want of assets, but also for lack of the trusted liquidity needed on the timescales that matter.

The first fact sheet is still correct because it describes the new economy better than any case study has yet done. One bank suffered $42 billion in withdrawals in a single day and was expecting a further $100 billion to follow it next, without that money disappearing anywhere but simply not being there anymore in the eyes of that bank. That distinction now has some significance in the financial world. One tweet is not more powerful than an objectively healthy balance sheet alone and trends on social media cannot always be traced back every time but simply relying on an insulated, widenetworked, and deepfunding base, on underwater, long,dated, assets, and a slowto,react leadership can transform an outlandish rumor, a capital injection, or an illadvised Tweet into an actual cash downpour. The foundational rule for modern-day liquidity management no longer is how much cash is reflected on the balance sheet, but what share of it is still being perceived as legitimate, accessible, and consummable when the messenger group in Telegram is slain. That is exactly what the guideline body of regulators should be on the lookout for. That's exactly what the banking fraternity should be pricing to the percentile levels. That's explicitly the lesson that would come through the doors of business schools and executive programs. Anything else would make the next run spiral out of control, even though it would seem so intuitive to all that it's due to unexpected incidence, that metaphorical Mexican wave crashing over the Rose Bowl, and that inability to recall the thousands of times before that we fought even harder.

References

Ananth, R. (2024) ‘Implications of the Silicon Valley Bank collapse on the management of held to maturity (HTM) assets and overall bank liquidity risk management’, 4most Insights, 3 January.

Barr, M.S. (2023) Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank. Washington, DC: Board of Governors of the Federal Reserve System.

Fascione, L., Jacoubian, J.I., Scheubel, B., Stracca, L. and Wildmann, N. (2025) Mind the App: Do European Deposits React to Digitalisation? ECB Working Paper No. 3092. Frankfurt am Main: European Central Bank.

Federal Deposit Insurance Corporation (2026) Quarterly Banking Profile: Fourth Quarter 2025. Washington, DC: Federal Deposit Insurance Corporation.

Feldberg, G. (2023a) ‘Lessons from applying the liquidity coverage ratio to Silicon Valley Bank’, Yale School of Management, Program on Financial Stability, 27 March.

Feldberg, G. (2023b) ‘Silicon Valley Bank’s liquidity, part two: what about the net stable funding ratio?’, Yale School of Management, Program on Financial Stability, 4 April.

Feldberg, G., Mott, C.K. and Cetina, J. (2025) ‘How US bank regulation failed SVB and its supervisors’, Journal of Financial Crises, 7(2), pp. 313–355.

Financial Stability Board (2024) Depositor Behaviour and Interest Rate and Liquidity Risks in the Financial System: Lessons from the March 2023 Banking Turmoil. Basel: Financial Stability Board.

Kodres, L.E. (2023) ‘Liquidity risk (mis)management: the failure of Silicon Valley Bank and the liability-driven investment episode in UK gilt markets’, MIT Golub Center for Finance and Policy Briefs and Blogs, 12 October.

Office of Inspector General, Board of Governors of the Federal Reserve System and Consumer Financial Protection Bureau (2023) Material Loss Review of Silicon Valley Bank. Washington, DC: Office of Inspector General, Board of Governors of the Federal Reserve System.

Rose, J. (2023) ‘Understanding the speed and size of bank runs in historical comparison’, Economic Synopses, 2023(12). St. Louis, MO: Federal Reserve Bank of St. Louis.

Similar Post