Family Office Private Markets Are Becoming an Access Business

Authored on

Modified

Family offices now compete through deal access Private credit is replacing venture as the practical core The best offices win on customization and networks

The current estimate of 8,030 single-family offices is 31% up from 2019; Deloitte forecasts that they will number 10,720 in 2030. According to the UBS Global Family Office Report 2023, total family wealth managed by family offices is approximately US$5.5 trillion, with around US$3.1 trillion of that amount currently under management and continuing to grow. This demonstrates that the family office sector is a significant and rapidly expanding area within wealth management. The family office private markets now look like less of a back office for established fortunes and more like a new lane in private capital. The business of the office no longer revolves around asset management and its preservation alone; it is about having exclusive access: identify, screen, structure, and syndicate private transactions that don't make it to the market. Once access becomes the business, the office switches from being a passive client of the bank to a rival lane into private capital.

The Business of Family Office private markets is no longer about wealth preservation

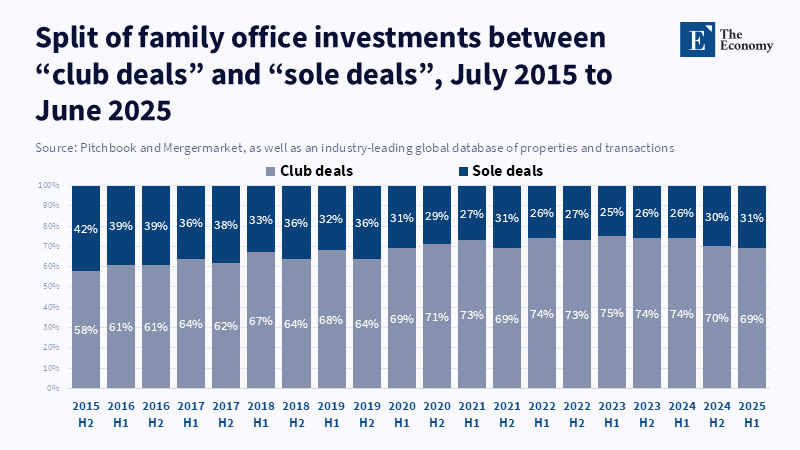

The established narrative is that family offices shifted from wealth preservation to wealth generation. This is certainly true, but perhaps understates the situation; a more accurate reading is that family offices have shifted from wealth balance sheet guardians to access platforms. In a survey by Citi in 2025, 70% of family offices had been involved in direct investing, 40% increasing the volume of activity considerably in the previous year. This does not look like client behavior when waiting to see what the private bank has on offer; rather, it resembles firm behavior wishing to create its own private markets access channel. In reality, this translates into an increase in the volume and breadth of co-investments, special purpose vehicles, cross-border structures, internal sourcing, and demand for investment advice and connections, in addition to the classical portfolio construction skills.

The point is that the blockage is not modeled. Good offices can buy models, hire experienced personnel, or use outside resources for parts of the diligence process. What good offices cannot easily buy is trust and access to good, scarce deals. It was access to managers and founders; now for private equity, it is access to sector operators, independent sponsors, and private transactions before they become public to the market; and for private credit, it is lenders and managers who know how to do real underwriting, not just "yield stories." This increases the value of relationships, reputation, and curation beyond plain asset allocation. An office that can turn trust into deal flow has power; otherwise, they continue to pay a full price for the feeling of exclusivity.

The shift is also creating a change in value capture. The previous model saw the private bank "win" by gathering assets, charging advisory fees, and surrounding the family with service. The newer model has a winning hand closer to the origination side. The winner is the institution that hears about the deal, can evaluate it in time, and brings the partners for the deal without losing a piece of the pie. This is why family offices are becoming a more modest private capital platform. Some are becoming a very focused private banker approach, and none are trying to recreate Wall Street, but rather seize both the client relationship and the access point in unison. This is a more potent proposition than simple wealth preservation, and it also explains the growth in competition among family office private markets.

Why Private Credit Took the Lead

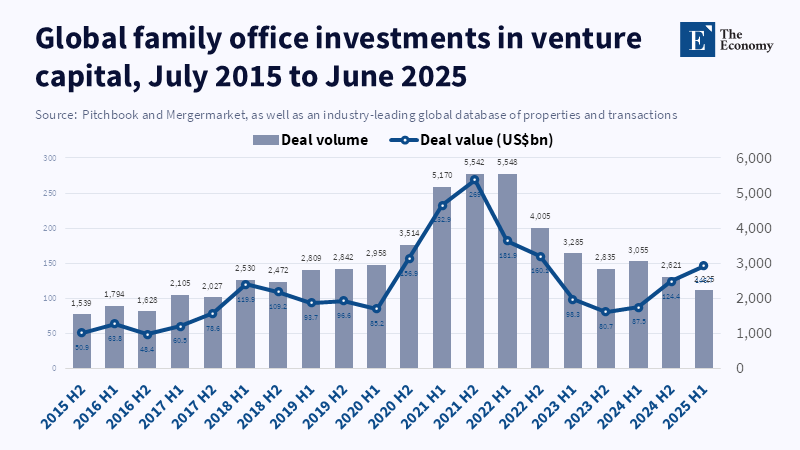

The moment chosen for this last transition is not random. Silicon Valley Bank failed on 10 March 2023, and the venture market took two years to digest and then navigate the environment it created; one of tight funding, difficult exits, and a discriminating LP pool. Data from PitchBook and NVCA illustrate how, in 2024, 30 firms that raised over $500m received 68% of new venture commitments, while emerging managers raised just $15bn - a figure not seen since 2015. This concentration is a game-changer for family offices; it increases the premium value of elite access and turns the mid-venture market into an uncompromising game where deep connections or niche knowledge are critical, and liquidity is more tenuous than most family offices experienced over the prior decade.

Private credit filled this void because it tackled several problems simultaneously: yielding income at sustained high interest rates, providing more downside protection than venture, and giving principals a more tangible 'story' of visible cash returns instead of yet more potential future upside. Average family office allocations to private markets have remained high in 2024 at 21 percent, but those planning changes for 2025 expect to reduce this share to 18 percent on average, mainly by lowering direct investments as capital markets activity and acquisitions slow and financing costs remain high.t is no longer simply tactical but a sustainable strategy offering clear control over risk and return.

This doesn't mean there is no venture. It just means that venture is no longer the status symbol. Family offices still put private equity and venture near the top of the charts for long-term risk-adjusted return. According to a report from UBS, private markets continue to make up around 30 percent of a typical North American family office portfolio, although family offices are now planning the biggest shift in strategic asset allocation in several years. Venture remains the asset of aspiration. Private credit is the asset of operation. Venture gives you a story upside-down, network prestige. Credit gives you cash flows, leverage in negotiations, and a better pitch to the investment committee. In an era when families want to know what an allocation does, not what it means, credit is the better pitch.

The strongest rebuttal is that private credit is simply the latest in a parade of crowded trades, and family offices are simply chasing after them. There is something to this; private credit spreads will narrow, disclosed volatility can disguise illiquidity, etc. However, this argument misses the point about the underlying market structure. Family offices are not flocking to credit because it looks cool on a fact sheet, but because the entire private capital structure now allows people willing to sacrifice some upside to do more of the things family offices actually want (more cash, leverage, exit independent cash flow, lower dependence on exit cycles or manager "story"). That fit still remains, perhaps better than it did in the zero-interest-rate era.

The New Competitive Map: Banks, Sponsors, and Independent Offices

This is where things become more interesting than the allocation argument. If family office private markets are now an access play, then family offices no longer compete with each other exclusively. Instead, they compete with private banks, general partners, independent sponsors, alternative asset managers, outsourced CIO platforms, and multi-family offices for the ability to be closest to the principal at the point of decision. Private banks retain relationships and a service layer, but lack the customization to address the desire to source personalized deal flow rather than a product. Sponsors have both origination and execution, but are transactional; there is also a likely mismatch in time horizon and a price tag for this service. The sweet spot platform is a family office that is able to combine both independence and customization with enough process to protect a principal.

This is why independent, as well as multi-family, offices are on the rise. A recent report from HNW Ranking highlights how independent multi-family offices in 2026 are expanding their role to adapt to global financial changes, which include higher interest rates and more opportunities in private investments. These offices are focusing on offering coordinated services across investment management, estate planning, tax oversight, philanthropy, and family governance, while managing exposure to both public and private markets. Larger offices are more cost-efficient relative to assets, with less reliance on external service providers and more sophisticated, institutionally modeled technology that smaller offices often struggle to replicate on their own. According to a report by John Smith and Jane Doe, fully bespoke family offices often come with high costs, while offices that are too standardized may struggle to stand out as true advisors instead of just intermediaries.

Average annual operating costs for single-family offices with more than $1B in assets have climbed to over $6.6M, according to J.P. Morgan. The 2025 survey from Heidrick & Struggles also highlights the speed at which the sector is creating a deeper investment professional talent pool, both in the US and Europe. This does two things. On one hand, it further stratifies the field, raising the hurdle to entry for smaller single-family offices aiming for institutional-grade capacity on institutional-grade budgets. On the other hand, it is effectively turning talent into a power commodity. A highly credible chief investment officer, private-credit underwriter, or operator with existing live sponsor relationships can move the economics of an office more dramatically than any alternative consulting deck. The family office space still speaks about capital; increasingly, however, the conversation has morphed into an arms race for talent.

What This Means For Talent, Education, and Policy

The implications for practice are straightforward. Families ought to move from a question about whether they require more private market exposure to asking about what type of access engine they currently command. A firm unable to source, evaluate, and monitor complex private deals needs to confront that limitation head-on and select partners based upon that reality. This could mean having a lean team within the office focused more narrowly on specific sectors rather than attempting to be all things to all asset classes, outsourcing to independent sponsors for private equity or specialist managers in credit, or utilizing multi-family office platforms for certain operational and governance needs. For educators and curriculum designers, the message is similarly evident. The current talent pipeline to pursue wealth management or investment careers still overwhelmingly focuses on public-market analysis and basic corporate finance. The decade ahead requires individuals who can blend sourcing, governance, illiquidity management, family psychology, and the exercise of good judgment across these disciplines. These skills have evolved from esoteric niceties to essential market infrastructure.

This transition should also be apparent to policymakers. Family offices are no longer "institutional enough" as active allocators into private markets to even warrant asking the question. They already are. The policy question now has shifted from whether to how much opaqueness the expanding private-capital channel should maintain as it competes for influence against regulated intermediaries. A forced convergence with a bank model is misguided and could undermine the patience they provide; a more measured approach to governance, valuation, conflicts of interest, suitability, and cross-border reporting, where appropriate, is better, as family offices begin playing larger market roles. This has implications for families themselves as well: it is no longer sufficient for family office private markets to only "protect capital"-now, it's the coordination of trust, talent, and deal flow that provides an institutional franchise. The old promise of wealth preservation has been replaced with access architecture.

References

Citi Wealth (2025) Global Family Office Report 2025. Citi Wealth.

Cuccinello, H. (2025a) ‘Family offices double down on private credit and infrastructure during private equity slump, survey finds’, CNBC, 26 June.

Cuccinello, H. (2025b) ‘Family offices flock to private markets with allocations surging over 500% in nearly a decade’, CNBC, 15 August.

Deloitte Private (2024) Defining the Family Office Landscape, 2024. Family Office Insight Series – Global Edition. Deloitte Private.

Editorial Staff (2025) ‘Going direct: The evolution of family office private market investing’, Family Wealth Report, 2 December.

Flack, J., Rettig, J., Janson, E. and Bodner, T. (2025) Global Family Office Deals Study 2025: From Family Wealth to Global Reach: How Family Offices Are Adapting Capital Deployment in Uncertain Times. PwC.

HNW Ranking Private Wealth Desk (2026) ‘Top 25 independent multi-family offices 2026’, HNW Ranking, 28 March.

Majic Predin, J. (2025) ‘From wealth preservation to value creation: family offices’ venture capital revolution’, Forbes, 13 March.

McCabe, C. (2026) ‘How the family office is quietly reshaping global investing’, Forbes, 12 February.

Russo, J. (2025) ‘How the family office has evolved into a strategic engine room for private capital’, LinkedIn post.

Schellenberg, L. (2025) ‘The family office of the future: from custodian to value creator’, H.I. Executive Consulting (H.I.E.C).

UBS AG (2024) UBS Global Family Office Report 2024: Balance Is Back. Zurich: UBS AG.

Similar Post