Private Capital in Education Is Rewriting the Market

Authored on

Modified

Private capital is becoming a controlling force across education Schools gain funding, but often lose pricing power, data control, and strategic autonomy Policy must shape the terms of private capital in education before the sector is governed by it

Kirkland & Ellis reports that PowaSchool, a solution to run education online, is being snapped up by Bain Capital Private Equity for 5.6 billion dollars. Instructure has been acquired for 4.8 billion dollars. Nord Anglia has been acquired at a valuation of 14.5 billion dollars. This is not a tangential finance item. It is a call to arms. Private capital in education is no longer just coming in from the outside. It is pressing into the pipes, the platforms, the brands, the access points, to shape the way schooling is paid for and delivered. The images of markets as sidelines and public systems as the core story have long appeared comfortable. They now seem tired. The tougher question is not whether private money is coming into education; rather, it is the type of market, built on patient holds and bundled software, ongoing contracts and data collection, and personal quiet pathways of power.

Private capital in education is becoming the sector’s hidden governor

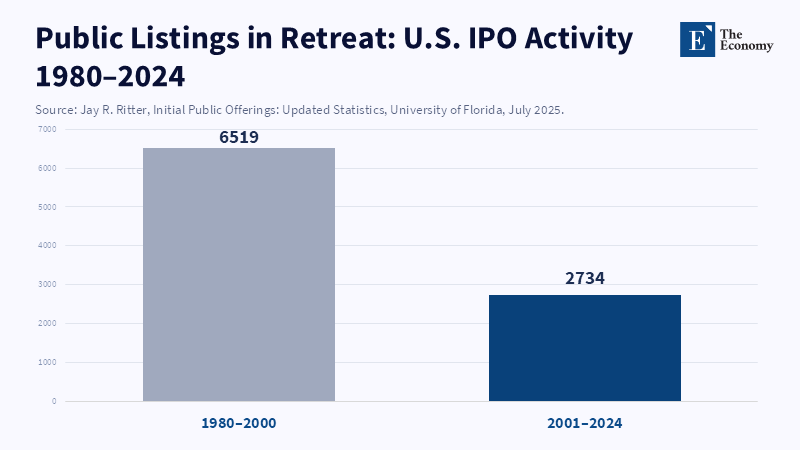

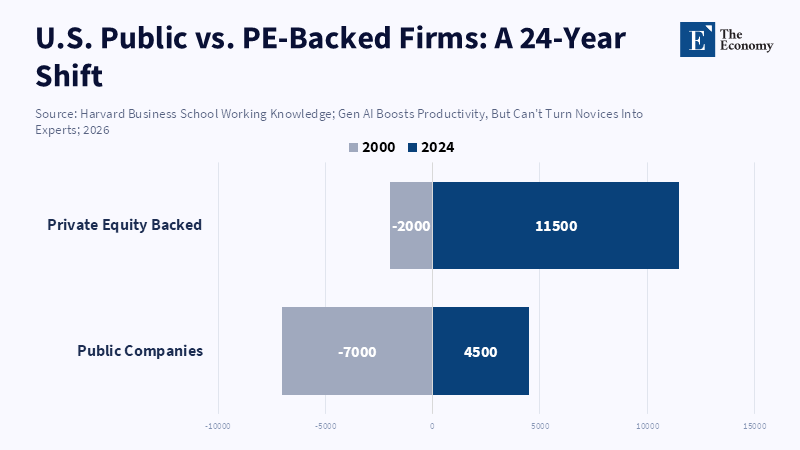

The familiar story is that private markets have expanded while public markets have contracted. That’s true, but it is too narrow for education. As of 2023, private equity and venture capital funding in the world's education services industry has shrunk to $4.60 billion, its lowest figure in three years, according to data from S&P Global Market Intelligence.25 As of the same year, they have huge sources of capital to rise to the surface. Conversely, the universe of public companies has shrunk, and companies tend to take longer to go public. This is especially important because several of the entities that are integrally related to current education are not necessarily required to use the public market as a source of capital. They may fill this need non-publicly, acquire competitors, utilize the potential to delay the process, and avoid costs and the public eye.26

The funding origin of that transition is strange as well. Some of it is public pension funds. Immense teacher and civil servant systems have taken on more significant risks in the private sector. CalPERS has increased its private market target allocation from 33 to 40 percent, as well as its private equity portion from 13 to 17 percent. Strange circle forward. Teachers, civil servants, and such oddities are funding the reserves, which then finance private initiatives looking for long-term supply-side finds. Many countries stubbornly remain convinced that private and government budgets are in opposition. Ironically, they are not.

Educational transactions make this clear. PowerSchool, a key K-12 data service, has just exited the market in a $5.6 billion deal. Canvas provider Instructure was aiming to go private for similar sums. Meanwhile, international school provider Nord Anglia picked up big institutional investors (such as the Canada Pension Plan Investment Board) in a $14.5 billion transaction. It's not a backwater. As this report on private resources for education by Neuberger Berman Private Markets, EQT, and CPP Investments points out,the elevated level of private ownership (for example, Nord Anglia Education) is actively shaping what goes on in schools and how education is delivered, particularly at the high end of schooling, making market forces highly relevant.

The appeal of these markets to private capital in education

Private capital is looking for this stuff precisely because there are a great many realities of education that are more operational than philosophical. The academic product is relatively sticky. You won't suddenly be an operator that needs a new path because of a demand shift. Students who decide to go elsewhere don't simply vanish after a blog post. It may take a long time to roll out a new platform, cut a new hire, or shape a new team—shaping the culture along the way, but your product must soldier on. Contracts may be years in length. Entry and exit costs increase with a platform's importance to credit, sysadmin, admission records, compliance—structure, in short, it is broken up into pieces. Schools and colleges purchase loads of similar services. Consolidation is made easier. Software for progression optimization mops up admin and instruction. Entry is slow, but the entry can last.

As a result of these realities, private investors have implemented different funding trajectories in education than elsewhere. In 2024, for example, venture investors exposed one failure in EdTech after another, driving investment to its lowest level in a decade. The number of private equity transactions in education services dropped 40 percent to 190 in 2023, the fewest for the sector since at least 2019, according to S&P Global Market Intelligence. That's a normal private market sequence. After all, venture Angel funds still fly high in the tips of the winds. Private equity and private credit come in post-market when quality, verified customers, and high-margin, cash-flowing software and services are priced in.

This advantage holds true for education firms as well. Private capital investment in the global education services industry was cut in half to 4.60 billion in 2023, according to S&P Global, its lowest level in three years, with a dramatic decrease. This slowdown may lead to private capital expanding at a slower pace, as reflected in how long it takes for trust in education suppliers to develop among teachers and administrators, relative to expectations set by public markets, which are generally concerned with quarter-to-quarter results following their monthly and quarterly reports. Moreover, the public investors view campus change at a painfully slow rate, such that they can time buy cycles that can span a year. This is not a problem for many private investors who can buy when they are ready and wait much longer to sell, which translates even better in education. This is one of the reasons why market share in education is provided by the private markets after hot capital offerings sag significantly.

Another contributor to that advantage is that the operational realities at most schools and colleges demand more restrained planning and a smoother rollout of new offerings than consumer audiences tolerate. A listed company is expected to hit quarterly targets with purchase cycles that last a year or more. It can be expected to have to pitch to somewhat backward institutions that will test every price round and cast about for 18 months to buy another or ten more products, then another, while deploying A.I. tools and slashing costs, all without having to later sell investors on a ticker. That's one reason why the private markets have remained lively, despite the waning investor mania of 2024. Private investors are not just buying growth. They are buying the clock.

This is compounded by the intrinsic forces of the sector. For various reasons, schools and colleges are facing increasing pressure to deploy digital technology, adopt a recruitment strategy, implement AI, and cater to more and more types of students without additional funding. As a report from the Distance Learning Institute notes, 'Private sector investors also argue that digital solutions allow organizations to spread fixed costs by operating more efficiently and generating real value. Sometimes, it is simply a higher bar for paying customers, telling us to deliver online learning that, for a change, is worth the extra investment, and this kind of empowerment of end users will benefit software sellers more than we'd like to think. Either way, the winners will be those firms that own the interface, the data, or the Trailhead.

How teachers are affected negatively by the move towards privatization

The first source of damage is the negotiating leverage. While one is able to change textbook buying policies on campus days, one will find one is much less able to replace one's learning platform, student information system, applicant file system, digital exam content, or edtech contractor. Once those systems become interconnected, one doesn't buy a product; one signs a subscription. Though that stretches out decision timelines and initiates an entirely new perception that one's brick and mortar won't be buying one individual product, but creating a far-flung digital life system. That hurt price discipline and tender duration, while broadening partners' insight and rights. While one's school may seem autonomous, it may forfeit data rights and strategic independence.

Second, competition with private capital will move the public sector into the long-range planning schools and colleges' need for personnel. UNESCO's estimate of the need for 44 million additional primary and secondary teachers globally by 2030 has been widely propagated. As providers develop replacement systems, AI and automation are being touted as not only efficiency enhancers but as staff reduction supplements as well. That message is persuasive, and some research shows that our current bright AI's capabilities can digitalize some low-value activities. The research also reveals that success requires usage instructions, expert training, and project planning; otherwise, teachers can become too dependent, train too many students on weak media, and drop other professional tools in favor of "AI" displays. Competition from private capital will persist here because of market motivations, and the public sector will stand to cut costs even more detrimentally to the professional.

Enrollment management automation presents an analogous conundrum. The data that surprised observers by tracking the first uptick in U.S. undergraduate enrollment since the pandemic hit, despite online learning having entered the general value system of a stand-up student body. But it also illustrates it is a marathon to gain enchantment over a business enterprise that combines content, analytics, and the summit of degree branding in a product. According to S & P Global, private equity and venture capital investment in global education services fell extensively in 2023 to less than $4.60 billion, the platform’s lowest yearly sum in three years. This abnormal change in flagging activities can influence how preschool vendors focus on tutorial and employment, potentially making it clear,cut the mix of tutorial goals, technology applications, and merchandiser solicitations. The report states that a major way the flagging market load is imposed upon the last sector is through demands in order to speed up change.

According to a report by the U.S. Department of Education Office of Innovation and Improvement, College enrollment in the United States has improved since the pandemic, but it still has not recovered to pre-2020 levels, and the number of schools qualified for federal student aid has decreased by roughly 2 percent from 2022–23 to 2023–24. That's not an apocalypse. However, it fosters a dire combination of demand pressure and organizational instability that can make a lot of campuses attractive cases for institutional partners. Consequently, private operators can quickly persuade them and establish high prices. That contributes to capturing market share, even if public institutions are still adjusting to the circumstances.

A policy stance not to exclude private markets but to make the most of them.

A grounded, hearty criticism would be if. We might in fact want more investment in schools, not less. Than we did yesterday. We don't need to keep private capital out; we need to stop talking lightly about whether investments are overall inaccessible. The real question is how private money is used, what the margin is id, and who is keeping the lead over data, fees, and mission. Certainly, private trainers—those who make schools more efficient, help realize a long-term vision, and cut component costs—have value; private partners—those who inflate margins for every advantage, keep users hostage to their systems, and treat operational data like a hedge fund—can sabotage the entire education sector. Public guidance should therefore serve to illuminate how the markets in education are created, what they should be, and how they can be steered, not exclude private investment.

Public authorities will need to require extensive disclosures on publisher ownership structures, billing and domain arrangements, subcontracting structures, and commercial conflicts in order to provide more pointed advice on which kinds of ownership and succession authorship would be sustainable. National and accreditation authorities should seek portability of data and platform standards for open-source infrastructure, and partner with unions, community groups, and other investors to consider how college subsidies could support collective consumer investments and new provider alliances, rather than private investors broadcasting capital across regions. The aim is not to exclude private investors. It is to prevent them from having an overwhelming influence, just because governments do not plan collaboratively.

However, there are some parts of education leadership that should investigate further into the areas where dependence on the marketplace has become overwhelming. A board or governing body can ask if the vendor has at such an extent become the heart of the system that "switching" cannot be done; trustees need to decide whether the provider has gained a data monopoly or a hold on the state of delivery that might eventually dislodge the public's hold on the methodology of education and therefore its influence upon society: the deeper such central functions as recruitment, testing, scheduling and facilitation of the system become dependent upon individual private suppliers, the more risk there is to the applicant that they will be vulnerable to change.

The bottom line is that public policymakers or school executives must separate out their interest in whether private investment is percolating into education from their knowledge of how to grab its opportunities and avoid its drawbacks. One is theoretical and disconnected, the latter is practical and specific. Both are important. In neglecting the former, education is pushed back by the margins of market reports or the back end of the discussion. If the latter isn't addressed, the sector might turn private policy into a very functional justification for sector hegemony.

References

Alternative Investment Management Association (AIMA) (2025) ‘Public vs Private Markets – A Shifting Equilibrium’. London: AIMA, 8 July.

BlackRock (2025) Private Markets Outlook 2026. New York, NY: BlackRock, 18 November.

CalPERS (2024) ‘CalPERS Will Increase Private Markets Investments’. Sacramento, CA: California Public Employees’ Retirement System, 19 March.

CLFI Team (2025) ‘Private Equity’s Power Shift: From Public Markets to Private Giants’. City of London Finance Initiative, 3 August.

Education Intelligence Unit (2025) ‘EdTech VC reached ∼$2.4B for 2024, representing the lowest level of investment in a decade’. HolonIQ, 15 January.

Imtiaz, M. and Sabater, A. (2024) ‘Private equity investment in education services falls to 3-year low’. S&P Global Market Intelligence, 29 May.

OECD (2024) Education Policy Outlook 2024: Reshaping Teaching into a Thriving Profession from ABCs to AI. Paris: OECD Publishing.

Ritter, J.R. (2026) Initial Public Offerings: Updated Statistics. Gainesville, FL: Warrington College of Business, University of Florida.

S&P Global Market Intelligence (n.d.) ‘Private Markets’. S&P Global Market Intelligence.

UNESCO (2024) Global Report on Teachers: Addressing Teacher Shortages and Transforming the Profession. Paris: UNESCO.

Similar Post