Jurisdiction Arbitrage: Why Borders Have Become the New Yield in Private Wealth

Authored on

Modified

Jurisdiction is becoming a source of return in private wealth Dubai shows that rules and tax regimes now shape asset allocation The winners will treat jurisdiction itself as part of the product

Global financial wealth rebounded by nearly 7 percent in 2023, reaching $275 trillion. This figure is more likely to be seen as a sign of how capital is being strategically managed and allocated than as evidence of capital flight. The wealthy aren’t just moving their assets to get better returns, security, and status. They are moving their wealth to obtain better legal systems, lower taxes, faster courts, more robust asset protection, greater privacy, and dependable contract enforcement. Essentially, they are applying jurisdiction arbitrage as a return mechanism. And that’s the new trend affecting private wealth. Arbitration of family and wealth disputes is an effect of this, not the cause. Family offices continue to pay close attention to the location of their assets and the laws that govern them while maintaining consistency in their investment strategies, even as geopolitical tensions and protectionist policies make cross-border considerations increasingly important.

Jurisdiction arbitrage went from a tax strategy to an investment strategy

The best way to reconceptualize this market is to cease to view legal and tax planning as an administrative appendage to 'actual' investing; for HNWI families, it is the investment itself. Today, nearly 23 million HNWIs collectively manage nearly $87 trillion according to DIFC's recent Global Wealth Report, and Deloitte predicts single-family office numbers will swell from 8,030 in 2024 to 10,720 in 2030 (managing from $5.5tn to $9.5tn, respectively). Once assets sit within structures of this magnitude, jurisdiction is no longer peripheral; it's on the expected return, the downside protection, the succession plan, the liquidity structure. A shift in tax residency, booking center, legal seat, or trust law can have a bigger impact on net results than an extra turn of leverage or an additional point of fund performance. The easy assertion that 'adding Dubai can add ten percent' is probably not that simple, but the intent is correct: even a point or two on a large and mobile balance sheet compounds quickly.

This shift is also reconfiguring bargaining power within the private wealth industry: firms that merely produce products are giving ground to those that can redesign ownership structures. A bank offering private market access but that cannot address treaty exposure, residence issues, governance, foundation law, digital asset custody, or dispute resolution planning is more replaceable than it used to be. The victors are the ones capable of offering a legal-tax operating system around a portfolio. Cost structures have shifted dramatically: rather than reliance on ongoing management and distribution fees, capital now goes to structuring, compliance, governance, substance, documentation, and cross-border management, all of which can be construed as transaction friction. In practice, for globally mobile families, they often function as conversion costs that turn gross wealth into durable, defendable net wealth. The industry is moving from product selection toward rules selection, and the margin pool is moving with it.

The point is that this migration is happening at the same pace that wealth is becoming both global and highly strategic in its employment of mobility. BCG estimates that two-thirds of new cross-border booked wealth will land in Switzerland, Hong Kong, or Singapore by 2029, whereas the UAE has already outpaced more established centers. The market is not differentiating between onshore investing plus a tangential offshore sleeve anymore. It differentiates between legal and booking frameworks. When this begins, jurisdiction arbitrage does not look like clever, radical, offshore manipulation. It looks like a straightforward, strategic asset allocation exercise. If a family will diversify its currency, political, and manager risks, it will want to diversify its legal and regulatory risks as well. The real issue for the industry no longer revolves around clients’ demand for this product, but around which firms will structure themselves to provide it without relinquishing control over the client.

How Dubai transformed jurisdiction arbitrage into a standardized, scaled service

Dubai’s significance to wealth management does not derive from the stereotypical perception of low tax levels. It emanates from the city's ability to turn jurisdiction arbitrage into a packaged product. There is generally no personal income tax levied in the UAE. Free zones like Dubai International Financial Center (DIFC) can offer zero percent corporate tax on income that satisfies the relevant criteria. Furthermore, a family foundation that qualifies under specific criteria can obtain fiscally transparent treatment, thereby preventing it from being taxed, by applying to the Federal Tax Authority. Alongside the offering of long-term residency and English-language legal documentation within a common law framework governed by DIFC’s courts, this provides more than a marginal offshore offering-it represents a comprehensive wealth management platform. Therefore, Dubai has relevance, offering a bundle of tax efficiency, legal certainty, access to financial institutions, and speedy administration from a single location.

The attraction is more than tax; wealthy families demand privacy, governance, and digital asset portability now as much as the nominal rate. DIFC caters precisely to that demand through its private register for suitable family arrangements and its privacy vault, which anonymizes shareholding and beneficial interest information from public access. Last year, it even implemented a Digital Assets Law for clarity to founders, investors, and family offices seeking to hold and structure tokenized or crypto-related wealth. Given that this market segment is undergoing a surge in activity as Henley's 2025 crypto wealth research reports an increase of 40 percent in global crypto millionaires to 241,700 within twelve months, any financial jurisdiction that can house and combine traditional wealth services with an authoritative legal framework is positioning itself to embrace next-gen mobile capital.

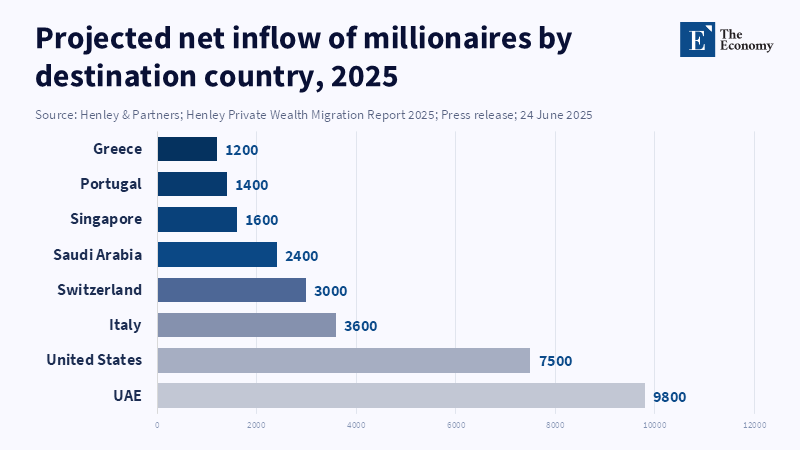

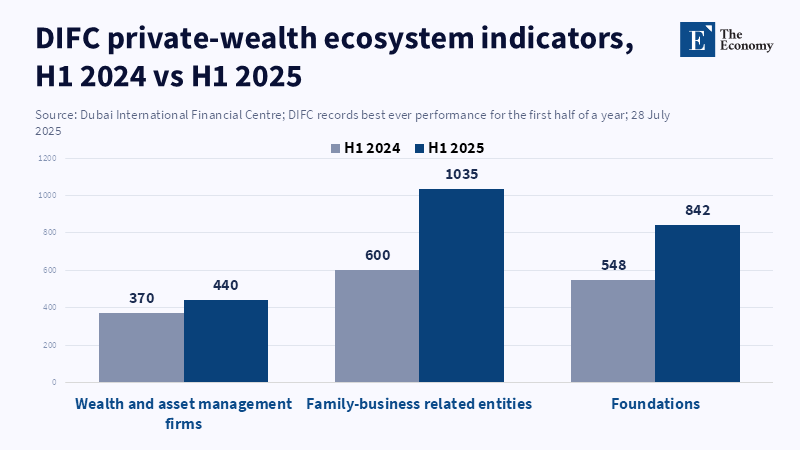

The market response to demand can be demonstrated by looking at statistics; in 2025, DIFC registered over 500 wealth & asset management firms (+22% YoY) and recorded 1,289 family-related entities (+61%) and 1,115 foundations (+66%). The latest projections for Henley anticipate that 9,800 millionaires will migrate to the UAE in 2025, bringing over $63 billion in investable assets. Taken together, this information reveals that Dubai is not only capturing the capital of millionaires, but demand for a new type of wealth service where jurisdiction itself is added value; this is why new wealth hubs now grow faster than established ones that still consider law, tax, and mobility as back-office functions instead of a primary strategy.

The advisory stack now monetizes jurisdiction arbitrage

That is what the advisory stack can be said to do now: price jurisdiction arbitrage. The market itself is what reveals this; that most recent HNW Ranking tables differentiate cross-border tax specialists, offshore and international structuring lawyers, and family office legal and structuring advisers is telling more than branding. It is evidence of a unique revenue pool, founded on the sale of jurisdiction arbitrage, that has emerged. Whereas the former private-wealth value chain tended to grant pricing authority to private banks, portfolio managers, and a limited group of trust providers, the current model is more complex. Tax counsel, structuring lawyers, arbitrators, governance advisers, digital asset teams, and relocation companies all carve out their piece because they individually offer expertise at specific levels of jurisdictional optimization. And once private wealth clients are inclined to see domicile, situs, trust seat, arbitration seat, and reporting requirements as investable options, the industry develops modular products, leading to niche players that can more effectively price for specific expertise.

Arbitration works as it does here because dispute design is an element of wealth design. Private wealth is now more international, more reliant on vehicles, and, than ten years ago, is typically dispersed across a variety of trusts, foundations, operating companies, and digital assets. This places private wealth litigants before longer, more unwieldy, and potentially more detrimental court processes, especially if a degree of privacy or enforceability is desired. The enactment of the Supplemental Swiss Rules for Trust, Estate, and Foundation disputes on July 1, 2025, illustrates the trend. As of the effective date of the Rules, the jurisdiction recognized arbitration clauses in trust deeds, foundation statutes, and wills, and the practice among private sector advisors in London, Dubai, Singapore, Hong Kong, and the Cayman Islands to incorporate arbitration into family office structures is growing rapidly. This indicates that something greater than simple dispute resolution is at stake; the arena of future disputes is now actively planned, rather than merely a contingency to which one resorts after everything has broken down.

The policy risks of jurisdiction arbitrage are real, but the trend will survive

There is a very simple criticism of the obvious ones: Is it just tax evasion in different clothes? Sometimes it will be. Some structures will not hold up to substance tests, some relocations will only be window-dressing, and some marketing about sovereign diversification will really be just glitz. However, to use these observations as an argument against the trend as a whole misses the point about what has changed in the market. The success isn't about countries that enable absolute non-transparency-it's about the ones that allow a controlled blend of tax-effectiveness, binding law, specialist courts, clear rules on digital assets, Arbitration facilities, and sufficient physical substance to enable it. That is fundamentally a different proposition from old-school offshore structures. It is sophisticated (if ultimately legal) arbitrage in laws and regulations. It is what's going to last-structured, evidenced, and defendable.

That has serious implications for everyone in the market. Private banks and wealth managers have to take jurisdictions out of the compliance footnote and turn them into core products in their own right, with different models covering tax residency, jurisdiction in dispute resolution, location of assets, compliance and reporting obligations, and treatment of digital assets. Family offices are making major changes to their investment strategies and placing greater emphasis on mastering jurisdictional choices, rather than relying on a single legal opinion. Having a comprehensive overview helps them understand how much of their investment performance comes from their own decisions versus the advantages offered by their chosen jurisdictions. And there's a far more stark message to politicians-the movement of wealthy capital isn't simply motivated by a lower rate of tax elsewhere, it is often a vote for countries which are agile and not lethargic, noisy and unstable, or digitally slow and confused by the new classes of assets. If you want to attract capital, you must have speed in your civil justice, clarity on your international tax liabilities, and credibility in your estate and wealth planning; you must have modern legal frameworks governing trusts, foundations, and digital assets. Slow administration is now a disadvantage.

The larger argument, of course, circles back to that first figure. A $14.4 trillion world of cross-border financial wealth is not one in which geography is becoming less salient; it is one in which geography is being commodified. That is why jurisdiction arbitrage merits recognition as a primary layer of private-wealth strategy, not merely a neat trick for tax attorneys. The family office of 2020 and beyond will not simply allocate between public equity, private equity, real estate, and cash. It will allocate between legal regimes, regulatory environments, arbitration locations, and rules governing digital assets. The firms that fail to counsel across that terrain will appear underequipped regardless of the quality of their investment offerings. Governments that aim to compete on tax rates alone will also fail. The jurisdictions of tomorrow will be those that translate law into infrastructure, those that convert borders into yields.

References

Boston Consulting Group (2025) Global Wealth Report 2025: Rethinking the Rules for Growth. Boston, MA: Boston Consulting Group.

Burroughes, T. (2026) ‘Arbitration gains traction in private wealth wrangles’, WealthBriefing, 1 April.

Chambers and Partners (2026) Private Wealth Disputes 2026. Global Practice Guides. London: Chambers and Partners.

Dubai International Financial Centre (2026a) ‘DIFC report: High-net-worth-individuals with USD 87trn in wealth are reshaping global investment priorities’, 24 February. Dubai: Dubai International Financial Centre.

Dubai International Financial Centre (2026b) ‘Dubai International Financial Centre announces landmark annual results for 2025’, 5 February. Dubai: Dubai International Financial Centre.

Falkof, G. (2025) ‘Introduction: The growth of international arbitration for private wealth disputes’. In: The Guide to High Net Worth Clients and Arbitration. First edition. London: Global Arbitration Review.

HNW Ranking (2026a) ‘Top 20 Cross-Border Tax Law Specialists 2026’, Ranking News, 1 March.

HNW Ranking (2026b) ‘Top 20 Family Office Legal & Structuring Advisors 2026’, Ranking News, 1 March.

Henley & Partners (2025a) The Crypto Wealth Report 2025. London: Henley & Partners.

Henley & Partners (2025b) The Henley Private Wealth Migration Report 2025. London: Henley & Partners.

Perkins, T. (2025) ‘Arbitration for family offices’, Expert Insights, Charles Russell Speechlys, 17 June.

Snider, T.R. (2025) ‘Arbitrating private wealth disputes’, Expert Insights, Charles Russell Speechlys, 24 June.

Swiss Arbitration Centre (2025) ‘New Supplemental Swiss Rules for Trust, Estate and Foundation Disputes (TEF Rules) to Enter into Force on 1 July 2025’, 22 May. Zurich: Swiss Arbitration Centre.

Volek, D. (2025) ‘The digital offshore and the future of cross-border wealth’. In: The Crypto Wealth Report 2025. London: Henley & Partners.

Similar Post