Family Office Segmentation Is Rewriting the Wealth Industry’s Power Map

Authored on

Modified

Small family offices are gaining ground through speed and focus Complex markets now reward agility over bureaucracy The strongest offices will be lean, vigilant, and digital

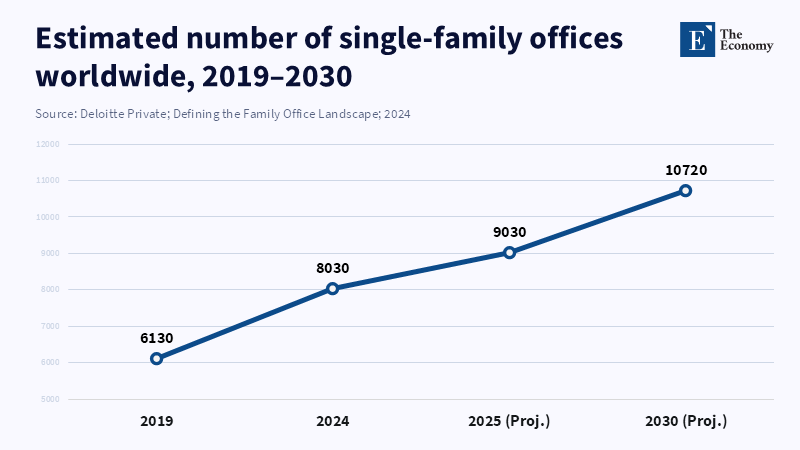

The most important figure in family office segmentation is not a rate of return; it's 8,030. That, according to recent industry analysis, is the number of single-family offices now managing wealth around the globe, an increase of over 1,900 since 2019, and a number projected to hit 10,720 by 2030. This is not just growth; it's a market being fractured into a thousand distinct pieces. Wealth is no longer accumulating quite so neatly within a few massive advisory groups, older private banking channels, or expansive multi-family office structures. Rather, it's being divided among more distinct ownership vehicles, more precise mandates, and more operating paradigms. That matters because family office segmentation redefines strength: in a market now defined by private investments, geopolitical turmoil, cross-border risk, and accelerating technological cycles, size is not necessarily success, and the old maxim of 'bigger is better' is beginning to falter. The most resilient structures for this era will likely not be the broadest or the oldest, but the most agile; the ones capable of rapid decision-making, early risk identification, and lean, efficient capital deployment.

Family Office Segmentation Re-Shapes the Role of Scale

The conventional interpretation of growth in family offices is that the industry is simply becoming more institutional. While that is indeed occurring, it is only half of the picture; family office segmentation is also resulting in increased diversity in the nature of the offices themselves, from purpose to staffing and service design. The number of single-family offices has increased from about 6,130 in 2019 to an estimated 8,030 today, and this figure is expected to reach over 10,720 by 2030, reflecting significant industry expansion and the continued evolution of single-family office structures and operations.

It is because of that divergence that the now more numerous, smaller family offices deserve a closer look. The fact of their smaller size is not what makes them stronger; they often lack real deal flow and have fewer employees and less internal research. Many smaller offices are underexposed to venture and growth due to a lack of capacity or process to sift the wheat from the chaff. Firms owned by single-family offices tend to have higher long-term debt ratios than other family-owned firms, suggesting a distinct capital structure that may influence how lean or focused these offices can be across different sourcing and decision-making environments. Large platforms may win on breadth of access, manager access, and formalized processes. Smaller offices may win on selectivity, discretion, and rapid deployment of capital. Given how much customization is worth now, this difference has become structural, not superficial.

Where the leverage is moving

The main development in family office segmentation is that leverage is now about controlling speed, service design, and cost flexibility rather than platform breadth. The emerging successful smaller family offices are not family retainers that rely on a trusted accountant and a spreadsheet. Rather, they are a lean, agile decision center that maintains proximity to the family but leases out specialists as required. A recent survey indicated that70%of all family offices are making direct investments, with 40% having increased their direct investing at least significantly in the past twelve months. These smaller offices are better positioned to compete in an environment where action is possible in weeks, rather than quarters, particularly when the family comes with industry expertise gained from running a business, a founder mentality, or strong, next-generation ideas. Smaller offices are well-suited to take advantage of these edge cases since there are fewer people and fewer silos to manage.

The key movement in family office segmentation is that leverage has been shifted away from pure platform width toward control over speed, service design, and cost flexibility. The future winners in small office configuration are less likely to be traditional retainers managing their own spreadsheets and relationships, and more likely to be tightly controlled decision centers managing closely with the family and renting capacity when they require specialists. According to the Family Office Direct Investing Report, 70 percent of surveyed family office respondents participated in direct investments, and 40 percent of those who invest directly said they had increased or significantly increased their direct investment activity in the past year. The report also notes that this trend tends to benefit smaller family offices that can move quickly, especially when they have specific industry expertise from prior business or entrepreneurial experience, or have firm next-generation investment beliefs. The leaner nature of smaller offices can allow them to move more quickly at these edges because there is less sign-off involved and fewer siloes to navigate.

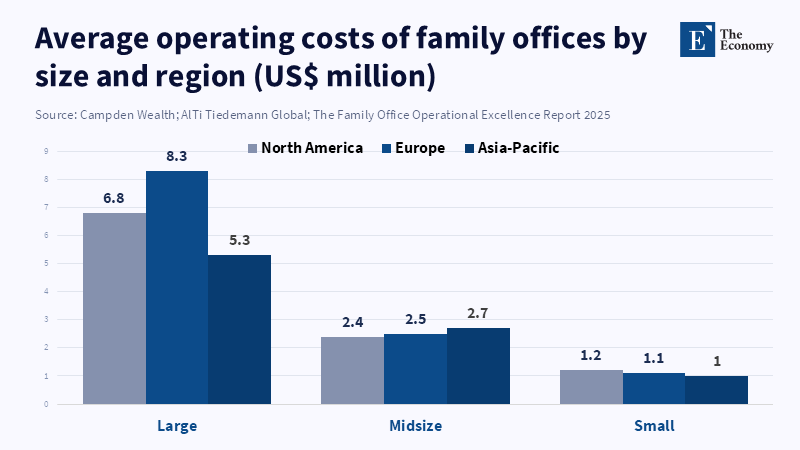

Nothing here signals that a move away from scale is occurring; scale itself is just being reevaluated. Recent operational research shows an average operating spend of roughly $1 million for smaller offices and $3.6 million and $11 million for mid-size and large offices, respectively. In basis points, the cost for smaller offices is much greater than that for larger offices. Larger offices continue to benefit from better cost efficiency, more expertise on hand, and more formal controls. According to the Global Family Office Industry Research Report 2023, mid-size family offices face challenges because they are often either too small to operate with fully institutionalized processes or too complex to maintain agility. The report suggests that focusing on operational efficiency, rather than just increasing size, will be a key competitive advantage in the future. This is likely to create a market dynamic where both large, highly integrated offices and smaller, flexible offices thrive, while those in the middle may find it harder to compete.

Technology is lowering the minimum efficient scale, but only for disciplined offices

And that is precisely the point where the AI narrative needs to be examined more coolly. Small family offices are not getting stronger because of a wider range of tools to work with; they will get stronger when a tool allows fixed cost overhead to become a flexible capability. A recent piece of industry commentary captures the problem eloquently: "AI cannot help an office that still relies on stale data, manual workarounds, and problematic reconciliation." Recent operational data does a lot to underline the warning. A third of offices still require >50% manual labor to generate reports, and the use of spreadsheets and manual data collection remains one of the leading causes of technology problems for them. And yet the very same survey suggests that smaller, newer offices are somewhat more prone than larger ones to adopting leading-edge systems (presumably because they are more willing to outsource, rather than cling to old internal technology stack).

Why that should be the case is that the segmentation in the family office world is becoming about the ability to buy capabilities without the bureaucracy. In one survey of technology within family offices, nearly every office had less than five employees, a full 84% claimed to rely heavily on technology, and more than half said they had considered or utilized outsourcing in order to mitigate risk stemming from "key person risk" with regard to the technology function of their firm. Few family offices had implemented artificial intelligence within their operations, highlighting a notable trend in the sector. The competitive advantage of today's family office is not its quick adoption of cutting-edge functionality; it's clean data, reliable reporting, a secure workflow, and a crisp differentiation of what must remain in-house from what can be purchased as a service. An office that considers technology an operating architecture rather than a marketing tool, regardless of headcount, can punch a lot further. But the most cogent objection to the case for the small office remains true: a very small office is indeed fragile, if one trusted employee leaves or one provider becomes unstable. But that exactly describes the kind of operation the winners from today's change are NOT; they are lean offices, highly controlled with standard procedures, and with outside capacity added to mitigate weaknesses well before they become visible.

Why the new market rewards vigilance more than breadth

The argument for smaller family offices is not that they are as competent as big ones in all that they do. That's impossible. The argument is that in today's market, alertness pays off more than scope. Recent global data shows that some family offices have been buying developed market equities and private debt while selling down private equity from their 2023 highs. That same data source points out that some smaller family offices have been paring private equity because they do not run internal direct programs and find themselves stuck with slow exits. That is a great piece of reality about the enthusiasm. Small offices aren't better than big ones across the asset spectrum. They are better at keeping close to the deal and far from general ownership. Where valuations are unclear and liquidity is patchy, a family office that can easily show why it owns an asset can outperform one that owns a tangled asset structure just because that's its long-term commitment.

This transition will have an impact that extends beyond portfolio management. It will affect power across the wealth business. Private banks, larger advice firms, and multi-family offices will still be the default go-to clients for financing, safekeeping of assets, connections to money managers, estate administration, and detailed process design. But as family offices begin to bifurcate, some power will shift back to the family office, enabling clients to unbundle advice. A well-run small family office with strong connections to firms that have relevant expertise can source the reporting from one place, legal advice and structuring from another, taxation input from a third, and due diligence on investments from a fourth. This makes existing bundled solutions less central and highlights the significance of well-considered decision-making within the family office. Finally, this process gives rise to a policy debate. If investment capital increasingly moves into leaner, technology-powered family offices not conventionally covered by advice regulation, operational resilience will then have less to do with top-line figures and more with corporate governance, digital safety, accuracy in reports, and client management.

The market is evolving toward a barbell structure and policy has to follow

The practical outcome of the stratification of family offices is a barbell market. At one end are large, highly capitalized offices and major multi-family office platforms. The model allows for fixed-cost spreading and a broad suite of specialized services. At the other end are smaller, niche offices which remain purposefully specialized, preserve owner control, and utilize technology, outsourced services, and strategic partnerships to maintain their agility. Between these extremes lies a thinner middle. It is characterized by sufficient complexity to require structured operations, but is often unable to capture economies of scale or impose the rigor of a lean model. These offices suffer from "manual creep, rising costs, and strategic drift." Families often feel that they are paying heavily for structures they do not feel result in proportionally enhanced speed, service, and transparency.

The takeaway for the principal of a family office is clear. Be skeptical of institutional theatre that does not result in a robust service. Do not ask whether an office appears large; rather, ask whether its structure results in decisions made swiftly with minimal friction. Service providers will receive a similar directive. The next expansion market for service providers is not to market glamour and comprehensive service to all wealthy families, but rather, to enable different types of family offices to purchase the capabilities they truly require, and to assist them without imposing a one-size-fits-all model. Policymakers should focus on operational soundness, not necessarily a regulatory free-for-all. The regulatory framework for family offices in the United States is based on the premise that regulated entities manage solely private family assets and do not provide public advisory services. As the industry grows, perhaps the greatest concern should not be the risk of brand contamination, but the possibility of uncontrolled expansion within tightly staffed structures managing increasingly significant amounts of capital.

The starting number still counts, but it is more than just growth. It counts dispersal. More family offices mean larger capital bases, more decision-makers, and increased competition in service offerings. Segmentation of the family office world is the real story, then. Because it’s a fragmented market, the small office is no longer merely a lower cost or early phase copycat to the larger office; it’s a strategic form of its own, one which, if carefully constructed with clarity of purpose, a specific mission, and an up-to-date technology base, could ultimately compete better than its heavier competitors hampered by bureaucracy. The future successes in the world of private wealth will not necessarily be defined by their scope but by how well each office manages a firm's central functions (whereby a firm's functions are in-house, farmed out, or avoided in the first place if they are a constraint on decisive action).

References

Block, J., Fathollahi, R. and Eroglu, O. (2024) ‘Capital structure of single family office-owned firms’, Journal of Family Business Strategy, 15(3), article 100596. doi:10.1016/j.jfbs.2023.100596.

Campden Wealth and AlTi Tiedemann Global (2025) The Family Office Operational Excellence Report 2025.

Deloitte Private (2024) Defining the Family Office Landscape, 2024.

Flohr, M.J. (2026) ‘The invisible segment: why smaller family offices remain under-allocated to venture and growth opportunities’, LinkedIn, 23 March.

Gooch, R. (2024) Digital Transformation of Family Office Operations, 2024. Deloitte Private.

HB Wealth (2025) ‘Pros and cons of a single-family office (SFO) vs. a multi-family offices (MFO)’, 14 May.

Henning, B. (2026) ‘Why family offices need more than AI hype: building the digital core for a more complex wealth future’, Hubbis, 20 March.

Private Wealth Desk (2026) ‘Top 25 Independent Multi-Family Offices 2026’, HNW Ranking, 3 March.

UBS (2025) Global Family Office Report 2025.

Similar Post