Family Office Fragmentation Is the New Fight for Control

Authored on

Modified

Fragmentation is no longer a flaw but a market response The new edge is control, not broad service coverage The winners will turn complexity into resilience

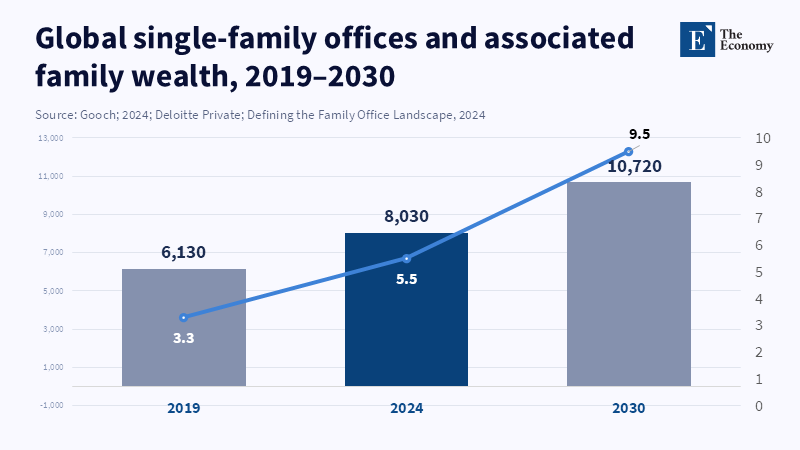

The old sales pitch of private wealth was tidy. A family office was the one-stop shop that could do it all for a rich family – investment, tax, trusts, cash, reporting, and even personal chores. The paradigm is not sustainable. The clearest market signal is scale. Deloitte calculates that 8,030 single-family offices (up from 6,130 in 2019) now oversee about $5.5 trillion of wealth. As the buyer base grows, service needs become more sophisticated. Families still want discretion, efficiency and autonomy, but they are no longer buying into the notion that one firm will do everything. They hire different firms for tax, governance, reporting, direct deals, trusts, banking and technology and attempt to weave them into one integrated system. The fragmentation of the family office is not just a problem; it is a reflection of how the market is rapidly evolving to meet complex, multifaceted demand.

Family Office Fragmentation Driven by Higher and Tougher Demand

It is too simple to see fragmentation as a problem of excess – too many advisors, too many banks, too many legal entities, too many files and spreadsheets. Instead, the division arises from changing requirements. Modern wealthy families require a level of support that extends well beyond a simple investment portfolio. They might require international tax advisory, trust and entity administration, support for direct deals, cash flow forecasting, cyber security, family governance, education of the next generation, philanthropic activity or management of real estate holdings and operating businesses. Once all of these additional services come into play, a narrow concierge service simply cannot cut the mustard. A service provider might still offer a wide array of services, but width alone does not compensate for a lack of depth.

Competition has caused that transition to accelerate. Independent multi-family offices, private banks, tax boutiques, reporting firms, trust specialists, and outsourced investment teams are all competing fiercely for the same wealthy clients. This is important because competition changes how buyers purchase. It causes them to unbundle mandates. According to Citi's 2024 family office survey, over 75% of family offices engage in direct investments. When a family office begins doing direct investments alongside funds, property, trusts, and banking, they are much more likely to purchase services in pieces. One company might be stronger at custody, while another might be better at tax or reporting. A report from PwC notes that while family office staff often bring experience in governance or deal work, it does not specify how many possess these backgrounds. Fragmentation in family offices increases because wealthier individuals now recognize that they can shop by function rather than by brand.

The increasing fragmentation is therefore not necessarily only a negative sign. For one thing, it demonstrates the market's need for more coverage than the old model could provide. Large service providers are still important; they continue to satisfy a large percentage of core needs and many families do not require anything more. Thus, the market will not suddenly descend into chaos. A split mandate does not necessarily indicate weak leadership. The old bundled offering is no longer automatically sufficient. According to a recent BlackRock report, families are now more likely to question whether a service provider truly excels in a particular area or if it is simply another item in their marketing materials. Once those questions are routine, unbundling is almost inevitable. Family office fragmentation is not solely a challenge to overcome but also a buying strategy.

Money Is Flowing to the Operating Layer

According to Deloitte’s Family Office Handbook, as family offices become more complex and work can be distributed among multiple providers, the real challenge shifts from the range of available services to effective coordination. Success depends on building management structures that can synchronize the activities of various independent teams as a unified operation. Thus, the operating layer is now central to the process. Systems for reporting, treasury, data flow, entity mapping, rule approvals, and data inputs are no longer administrative, but are deciding factors on whether a family office can quickly perceive and act on its current exposure or be confident in its provided financial information. A family may be able to retain brilliant attorneys, bright deal teams, and shrewd tax advisers, but if their data arrives in an unstructured manner, late and manually, then this family has purchased intellect without control.

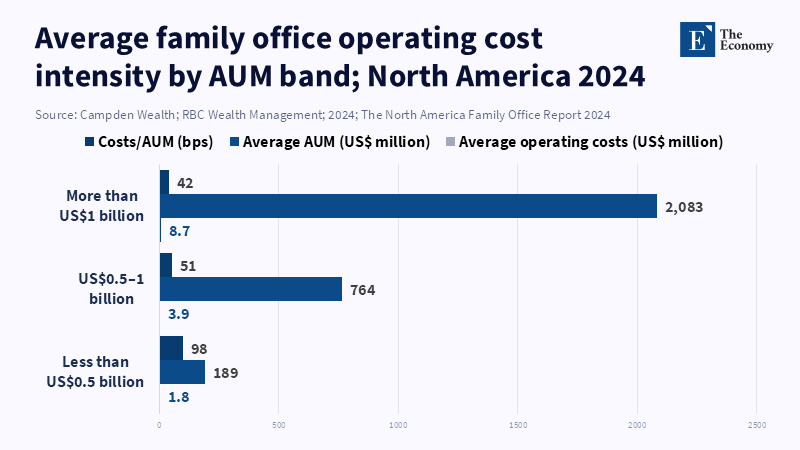

The cost figures emphasize the aforementioned. While a family office with under 500 million dollars under management averaged costs of about 98 basis points relative to assets, one with over 1 billion dollars managed approximately 42 basis points in costs. Typically, smaller entities average around 6 employees; larger ones may employ significantly more, along with more comprehensive internal teams. Small entities utilize larger external inputs into their costs. Market structure is a direct beneficiary of this phenomenon; small entities find it difficult to sustain full internal teams for investing, tax, reporting, and administration concurrently, so they outsource a portion of their services. The more outsourcing agreements a family office is part of, the greater the demand for a coherent system to manage relationships among vendors, banks, advisors, and asset managers. The price is higher for weak coordination within family offices.

It’s also clear from a headcount perspective and why many offices feel stretched even as asset values soar. Wharton’s 2024 family office study showed that roughly one-third of offices have just four to seven staff members, and just over one-quarter have more than a dozen. That’s not a huge internal brain trust to cover public investments, private placements, taxes, trusts, philanthropy, family meetings, and personal administrative support. In practice, what we are seeing is small cores plugged into vast networks. So what’s happening today is that the best advisors are selling not just knowledge, but process. They’re selling workflow, clean data, pace, and clear responsibilities. The product itself, ultimately, is the system that makes advice consumable.

Large Firms Still Have Their Place

None of which should signal the decline of large, broad players. The large private banks and the big family office business segments of firms like BlackRock, Northern Trust and J.P. Morgan continue to play an important role by integrating custody, lending, trade execution, manager access, and much of the reporting needs into a single solution. And to many families, that's just easier. As large as family offices are becoming, their fragmentation is still only partial. It is common for one of the big firms to handle the vast majority of the day-to-day work when families are largely investment-focused and don’t have very complex asset bases. That's why we believe the future will be less a dichotomy between giants and boutiques and more of a multi-tiered structure where the large provider houses the core and families add on top of that layer where needed to bring in more depth or where there's an identified conflict in using a broad platform.

This unbundled market also reorders bargaining power. The power of scale itself benefited the service provider in the old system. In the new system, power shifts to the family most able to switch one provider without disabling the entire setup. According to Citi Private Bank's 2024 Global Family Office Survey, the use of an outsourced CIO model varies significantly by region, with 16% of Asia Pacific family offices and just 3% of those in Europe, the Middle East and Africa relying on this approach, while Latin America and EMEA are likeliest not to have a CIO at all, at 38%. Families are happy to buy outside expertise, but they are uncomfortable buying outside judgment. They want the ultimate call, final view, and rules of the road close to home. That is why the independent, multi-family office is gaining traction, not because they will perform every function more effectively than global investment banks, but because they can sit on top of a varied provider set while keeping client interests paramount.

There is a fee story here as well, and it plays an increasingly important role. With a bundled approach, one did not worry about weaknesses that were masked by the total cost of the relationship. With an unbundled market, it is easier to put each function under a magnifying glass. Is the family overpaying for custodianship due to weak reporting, or for estate work with insufficient depth to plan for a cross-border life? Does an investment committee truly add value beyond what can be gleaned with simple access to the underlying? That puts pressure on not just boutiques, but also on large firms to improve what they do best, rather than rely on their breadth. The name of the game now is not the longest service menu; it is ownership of services for which a family simply will not compromise.

The Next Edge Is Control, Not Coverage

In addition, as the family office landscape gets more fragmented in the future, it's more likely to be execution, not returns-driven. As families become more global and their investments more heavily in private assets and information becomes more and more fluid, the control of the balance sheet is under threat. According to a 2025 survey from Citi Wealth, 71 percent of families have some international dimension to their family office structure. While many services are outsourced, especially beyond direct principal investment and real estate, only half of these families have a disaster recovery plan and many face additional operational challenges. As the number of wealth managers in the market continues to grow, it is clear that there are ample advisory services available, but robust organizational controls remain limited.

These facts clearly tell family heads and politicians alike that providers are no longer just about financial advice, but rather about efficient and clear implementation, cleanliness of data, clarity of responsibility and an office's control over all aspects. Family office heads and their teams should question if they have a holistic view of their cash, liabilities, capital calls and entity exposure. Furthermore, they must establish who governs the data, who has the responsibility to check the figures, who takes charge of the situation during a cyber-attack, and the ease with which a problematic vendor can be removed. Politicians don't have to view family offices as simply another retail bank to address their concerns. Rather, politicians should be concerned as a lot of family money sits in complex financial webs supported by a plethora of financial institutions with differing standards for data management, control, and oversight.

The most compelling objection is simple to state. According to BlackRock's 2025 Global Family Office Survey, while large family offices are bringing many services in-house, many still rely on a small group of external providers due to gaps in internal expertise, especially in areas like reporting, deal-sourcing, and private-market analytics, so fragmentation remains a significant part of the industry landscape. What it lacks is context. The trend isn't linear, from one provider to many. It's one of the broad-to-focused controls. And it is that latter change that matters. The premium is no longer with the firm that can offer a holistic solution. It's with the family office that has the expertise to differentiate between the essential internal control points and the external expertise to procure and manage all other services. That is the challenge of today: develop that control before the next crisis compels it. In the coming decade, those family offices will win by turning family office fragmentation into speed, discipline, and resilience.

References

BlackRock (2025) Rewriting the rules: 2025 Global Family Office Report. BlackRock.

Campden Wealth and RBC Wealth Management (2024) The North America Family Office Report 2024. Campden Wealth and RBC Wealth Management.

Gooch, R. (2024) Defining the Family Office Landscape, 2024. Deloitte Private.

Henning, B. (2026) ‘From fragmentation to control: Why Gulf family offices are rebuilding their operating model’, Hubbis, 16 March.

Hofmann, H., Monnier, A. and Kamath, A. (2024) Global Family Office 2024 Survey Insights. Citi Private Bank Global Family Office Group.

IQ-EQ (2025) ‘From fragmentation to focus: A $200M portfolio transformation’, IQ-EQ, 1 October.

Private Wealth Desk (2026) ‘Top 25 Independent Multi-Family Offices 2026’, HNW Ranking, 3 March.

Wharton Global Family Alliance (2024) The Wharton 2024 Family Office Survey: Executive Summary. The Wharton School, University of Pennsylvania.

Similar Post