Education Market Risk: The New Price of Geopolitics

Authored on

Modified

Geopolitical shocks now reshape education risk Funding, mobility, and costs are more fragile than they look The Iran episode shows shocks can exceed the models

With 6.9 million students now studying abroad and with U.S. colleges and universities alone extracting 42.9 billion dollars from foreign cohorts, the macro of the education market risk is no longer a macro story with a delay. It is a live pricing factor embedded inside the education market. This is the big insight opened by recent episodes in Iran. Markets did not wait until raw supply was totally dismantled before repricing; they repriced in threat of disruption, expectation of higher gas, lagged disbelief that rate cuts might not unfreeze quickly enough, and dread that ships, insurances, visas, and social confidence might all tighten at once. Such circuits are now the same inside the global modern education system: the free flow of mobile people and the imported social,physical, funded, technological, and strategic goods. For years, many educational sectors and systems treated geopolitically induced shocks as externalities, interferences that only impacted the rare campus that was itself right in the war. The lesson of broad application is over. The education market has now become so intertwined with repricing that one distant war can shift enrollment, costs, research, jobs, research funding, and public budget across the same reporting quarter.

Education market risk may now be a balancing sheet question

Analysts and policymakers alike default to policy questions on how war disrupts learning, access, and well-being. Those are survivalist and necessary questions. But the sharper policy question today is how geopolitical shocks are rebalancing the education sector. No longer immune to global revaluation, education has become embedded in it. From the Russian invasion of Ukraine in 2022, but especially from the 2026 escalation of the U.S. and Iran standoff, the mistaken idea that warfare is wholly a regional supply, gate episode has been exploded. A report by the IMF indicates that energy-fueled shocks now resonate as currency debasements, export mafias, or other broad global disturbances do, and that countries' education systems often track these price shocks in their own distinctive channels. A university or university system that earns tuition fees from cross-border students, imported laboratory equipment, cloud providers, debt,funded trickery, new builds, and, in general, a wide and global faculty is surely managing a financial sector balancing question, whether they admit it or not. The same principle applies across education providers whose budgets dwell on a portfolio of transfers linked to a single nearby energy or mortgage glut.

This paradigm shift alters the bargaining power across the provider state counterparty spectrum. Countries and colleges boasting large student pools, stable funding sources, liquid reserves, and buffers in delivery modes should gain bargaining leverage. They can counter shocks and cushion shocks. Those relying on just one supply country, one source of support, or just lower-cost energy, transport, and finance will now struggle to maintain some of their leverage. The same is true across polities. The heavy reliance of Australian (an example) universities on foreign students and what that dependency entails, kinship and agency, wise, for their achievement will erode their market clout should the world turn sour. The situation at home looks vulnerable as well. The Oxford-based researcher Pollard assessed that one in four providers participating in England may face a deficit since there were no contingency plans, and that almost one in six did not possess 30 days of cash equivalent enough to meet a physics book sale, or suchlike. The dependence of the United States, Australia, and other high-income systems on foreign students as an observable proportion of their corresponding public budgets is increasing even further now, as the data from the OECD suggests that two-thirds of countries estimate that tuition built into the premium these students pay exceeds the domestic fees by at least 20 percent. Education market risk is an educational demand shock. But it is also a measure of the strength of that country or institution's potential to fund the openness to which they were always dedicated.

Repricing of the worldwide dependence on the education sector

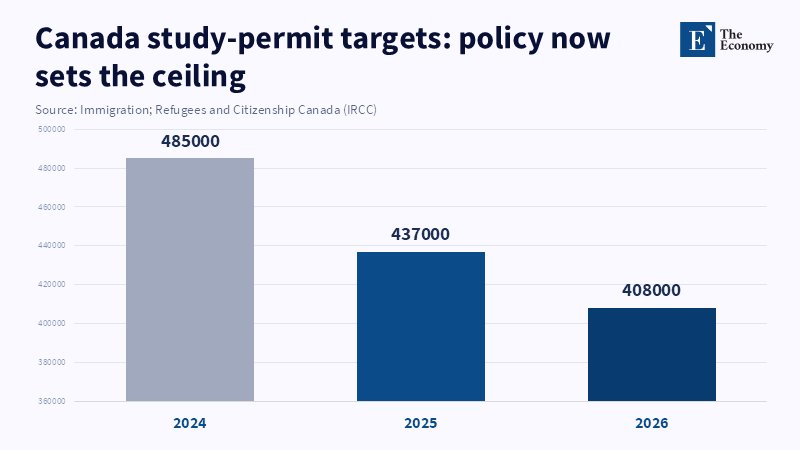

Repricing ensues from international mobility in hard numbers. To date, international rates have tolerated many interpretive masks: much of international schooling as a symbol of cultural soft power and a ringing guarantee of conversational skill, a global speech exercise, and a class conflict alleviation practice; but also a major export specialty, a high-tech assembly line, and a financial edge, calculant. While US cross-border students were above one million, Australian numbers for 2025 did reach 846,260, even as their upwardly adjusted enrollments declined by 15 percent. And Canadian goals of 437 thousand or so study permits by 2025, and to 406,40 or so by 2026, are a fundamental pivot from keying expansion on the pull of huge borders and towership alone toward explicitly setting caps on investment in these areas. These are deliberate systemic adjustments, revealing that governments are finally accounting for cross-border mobility in the same terms they do in their housing, infrastructure, diplomacy, and migration calculations. Once that principle becomes settled, providers will no longer control how huge they get in the market; their scale will be partly unwilled and depend on border processing, the work mood, opinions on cross-border mobility, and political opinion capacity.

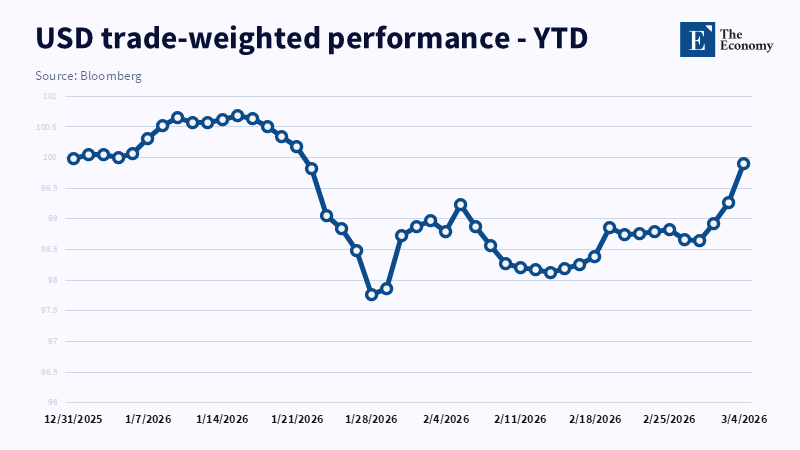

Second, the costs will escalate: persistently upward,energy, biased inflation expectations, and higher interest rates are comparable to the resilience experienced from currency, consumption, and insurance markets, and that adjustment in turn is reflected in every cost index of the control sector. Institutions will continually be heating domes, running lighting, moving trains, managing networks and markets, always moving lab supplies, cooking for students, and managing debt. When increased rates take hold, every investment in this area shrinks; every change in international demand patterns will be felt first in procurement knockthroughs, then in purchasing timing and contractual conditions. How fast was the book order on the International campus? Did it arrive at the expected schedule and order? A new study by the banker, M. M., said that how swiftly forward prices turned or vanished when watching the Western interstate wars turn off or pause oil markets or the despair in swap graphs on the dollar and yen swap charts in days. Oil prices were put to the test, and instead of falling, they jumped higher. Institutions should look to this as a predictor. The eras of empty international goods flowed completely untroubled, while the demand for education goods was already waning. The second bite was going to be paid in hedging cost, uninterruptedness of openness, diversification, subtle changes in compliance, and the sequencing of acts.

Thirdly, institutional finances, or the public budget, are the resting spot for this new force level. The test here may remain incremental, with confused inflation and employment, wheat, inflation, and it will be worse polls, a stretched fiscal gap, or a distant ballot. According to the virtual teacher, Shreeraj Khatiwada in the University of Europe's Yearbook of Education 2024, for example, the technological, forced life of the student, the repeated plunge steepness of the coverage for universal pre, kindergarten, or the massive effort to reduce the digital divide, may remain favorable if schools and schooling can make better workers for the shiny uncertain era in which we are emerging. Yet from the literature, the pace of donor aid has sharply diminished in 2024, with a further 28 percent downward trajectory projected by 2027, quickly translating into austerity that makes the sharp cost a reality. When wars turn global, police and coast guard are assigned more fuel and paper; officials work on new guidelines; the aid texture shifts; taxpayers are asked for more. It is not only a wheel of one. The matrix of austerity, public sector belt-tightening, publics' affections, and institutions trying to compensate for each other's austerity is much greater.

What cannot a simple date take and have?

Conventional approaches run into policy-relevant blind spots; each can be useful. The Caldara‐Iacoviello Geopolitical Risk Index uses reference checkers to survey the press for war, platoon, and terror mentions; together they condense a result into one index of geopolitical danger that can be validated by the tightening of investments and employment of that era. The new World Uncertainty Index collates the same assessments of danger from 180-odd nations by combining summaries from the Economist and three other giant corpora. Secondly, compilations of select economic policy uncertainty measures find the same trends of heightened uncertainty; implied volatility, credit spreads, oil prices, and swap rates indicate how quickly risk is materializing across other models. They aid our understanding of how the damage occurs, but many models are asking about systems that are out of scope for the question. What is the problem? You call the insurance giant U.S. to report rising geopolitical warfare risk, they memorize it, but ignore the fact that their fishing sector has just been banned in Iran; they do not mention that you are going to cancel the big conference if the visa gets banned and the Iran project closes. Certainly, this is not the right goal, but it is how deep we still imagine the world of damage is that you do not need to know: market composure and momentum, systemic or sector levels of attack, or the timeliness of public,sector COVID alert threshold. Second worst, you are not recognizing the extra, long-term effects that you may see in a month, but years out can take a while to feel as action in inflation, gross, and investment. Should we have known this from the Iran experience: that we appeared to over-regulate, to carry ahead the losses (predicting dates)? I think the nonlinear fever in prices has just proven that institutions think in an infinite cycle of time, but carry out in series.

Maybe the sector could perform a reverse stress test of this sort. The European Central Bank announced it will deliver reverse stress tests on stress scenarios for its planning. Under this concept, banks would estimate the worst scenario for their portfolio and identify what strange events lead to it. Course administrators should seriously want that sort of analysis. Instead of worrying if an Iran-related war today drives the cost structure up by 1 or 2 percent, they should focus on how such a sequence can cause production to collapse. Suppose the supply shocks of the Russian-Ukrainian war cycle, oil prices shoot up, local currencies get battered, aid is reduced, and then an operational crisis hits. If the top variable,shock, what would happen? Or, if a hacker in a prominent locker chair sits in a digital agency, what will happen? These are not flights of speculation. They are appraisals to be done much faster in open sector management teams. They should aim not to have blind spots on what the next crisis can become in the next few months, regarding vulnerability. The goal is not to be able to forecast that thinghot pair before the rest of the world; the goal is to hang the hole in the whole world in time.

What should policymakers and educators do?

Institutional policy, administrators should be ready to change. One lesson of the new geopolitics is that the education market risk ought not to stay inside the confluence of the compliance team, the global admissions scheme, or the risk management group. Instead, it must visit the soul of the institution. That means halting reputation metrics with supermarket regression line calculations, or redefining "blessed" as analysis of cross-issue structural exposure ratios. Leaders should recognize the extent of their own income at risk from individual nations, vendors, and schemes. They should predict cash flow stability a period ahead of when enrollments are concerned. They should organize diversity in their sources, modalities, and modes of delivery (consider remote campuses and near, field partner campuses, remittance streams, and second-generation demographics). They should revise purchase practices that maximize redundancies, and they should piece together institutional input inventories one step at a time.

The same applies to policymakers. If reliance on a foreign influx of students is overstated as an imperative to cover persistent financial deficiencies, we build an education sector with pro-cyclicality and a dramatic squeeze of the education budget, even with moderate austerity. Resilience is not just about adding new floors to what is already there; it also translates as your distant and close heavens. You cannot be caught off guard and open at the same moment. Why be able to not proclaim a lock? Why begin to make systematic, accurate, centric checklists to prepare for future financial wars in higher education? Some may say that this reversion is yet another retreat into fortress worlds. They are wrong. Larger resilience as a consequence of geopolitical factors is also an appeal to preserve kinds of international mobility. It is also a commitment to interpret the link between rising air fares and the expansion of the education market. If you want a robust expansion of global conversational flows, be serious about how risk and construction constrain the firepower that ought to undergird such an expansion. Finally, the premise (that global speakery flows are so robust that others can do with less risk,sensitivity, and more risk,acceptance) is unlikely in the new era. If your ideal system is to enjoy a flavor of mental freedom and global speech economy, then you strive to optimize global cross-border channels and afford to be restrained in some markets.

The ominous error in the existing analysis is that it has made us feel too comfy. No matter what we say through a universe of indices and comparisons, we have an emerging, base, carry, over, flag, numerical sense of our safe area of openness and in which timetable to implement our investments and whatever the twenty indices measure, they do not persuade us how many blind spots there are in the next course. We got to try. Perhaps it is the best way to approach, not hoping for the next super episode: know the negative scenario, and try to draw what predicts it.

References

Banks, R. (2025) Benefits from International Students: The United States of America. Washington, DC: NAFSA: Association of International Educators.

Bloomberg (2026) USD trade-weighted performance - YTD. Bloomberg Terminal data.

Bowie, J. (2026) ‘Geopolitics, inflation expectations, and the repricing of rate risk’. Chatham Financial Insights, 3 April.

Caldara, D. and Iacoviello, M. (2022) ‘Measuring geopolitical risk’, American Economic Review, 112(4), pp. 1194–1225. doi:10.1257/aer.20191823.

Connolly, M. (2026) ‘Super-Prime Market Intelligence: The geopolitical premium – risk is repricing global assets’. The Super Prime, 9 March.

Department of Education, Australian Government (2026) International student monthly summary and data tables. Canberra: Department of Education.

Immigration, Refugees and Citizenship Canada (2025) 2026 provincial and territorial allocations under the international student cap. Ottawa: Government of Canada.

OECD (2025) Education at a Glance 2025: OECD Indicators. Paris: OECD Publishing.

Office for Students (2025) ‘Significant challenges continue to face higher education finances – with nearly half facing deficits in 2025-26’. Press release, 20 November. Bristol: Office for Students.

World Bank, Global Education Monitoring Report Team and UNESCO Institute for Statistics (2024) Education Finance Watch 2024. Washington, DC: World Bank.

Similar Post