Europe’s Chip Strategy Should Build Power Through Indispensable Chips

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Europe should build chip power through indispensability, not full self-sufficiency The real strategy is to control key bottlenecks others cannot replace A stronger chip policy must focus on leverage, coordination, and industrial demand

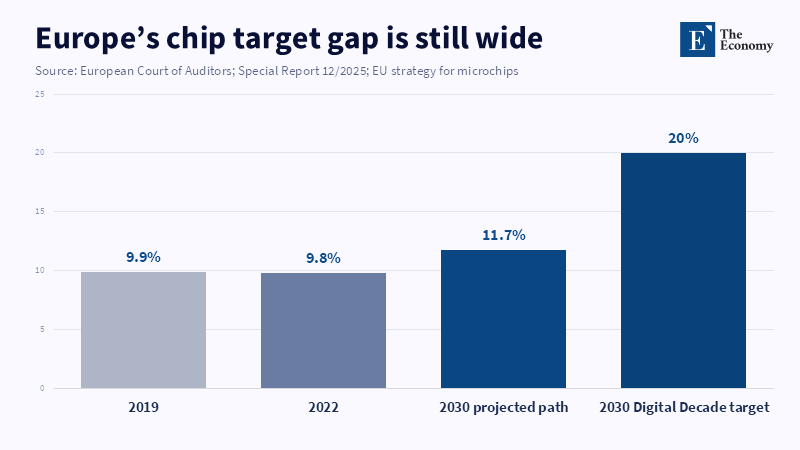

The figure that matters most in Europe's chip debate is neither 43 billion nor the obsolete 20 percent target. It is 11.7 percent: the proportion of world chip manufacturing value Europe might have by the year 2030, assuming the current position does not change. The difference between 20 percent and 11.7 percent is not only a failure to meet a target; it is also an indication that the European chip strategy has set itself the wrong question. The question is not whether Europe can copy Taiwan, the US, Japan, South Korea and China simultaneously. It cannot. The question is whether Europe can become so crucial to the chip chain that the rest can ignore it or kick it out only at their peril. To this end, a credible European chip strategy must evolve from an unrealistic vision of self-sufficiency to the tougher call for indispensability.

Why the European chip strategy has to go beyond self-sufficiency

The core argument is straightforward and pragmatic: semiconductor sovereignty should not mean producing every kind of chip in Europe but securing access by strengthening the parts of the value chain where Europe already matters. Instead, the goal should be to secure access by increasing the control, deepening and protecting the pieces of the value chain where Europe already means something." This broadens the discussion of "strategic autonomy" to the granular level. It perceives chips not as a static product, but as a dense chain of design tools, wafers, chemicals, optics, machinery, research laboratories, fabs, packaging, testing and end-consumers. There is no single player in control of the entire chain. Even the strongest actors depend on someone else. Europe's challenge is not to circumvent sharing, but to leverage its position of strength to participate in it.

The importance of this new framing is that the first European Chips Act was conceived in a very different time. In those pandemic shortages, the biggest concern was accidental interruption. Car plants slowed, medical devices were delayed and firms realized invisible chips could halt visible industries. It was only natural to reply to that shock with a target to ramp up European output. But the world of policy has shifted. Export controls, Taiwan risk, AI demand and subsidies both from Washington and Beijing now determine the market as much as shortages do. A European chip plan based on fabs alone is far too narrow for these conditions. Fabs matter, but they are only one physical claim. The most profound kind of power resides in bottlenecks where other players need them and cannot substitute for them quickly.

The evidence of a European chip strategy of indispensability

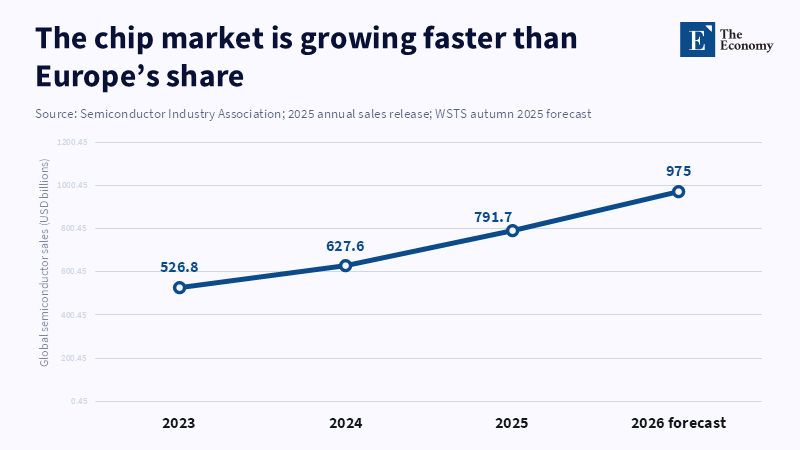

Market evidence backs this trend. After a weak 2023, global semiconductor sales hit a record high in 2024, above $600 billion. The next cycle is being led by AI, data centers, memory and high-end logic. Now forecasts point to a 2026 market nearing a trillion dollars. Such a growth does not make Europe's task any easier. It makes the target more difficult to reach because every other top region is also investing. If the overall market is growing rapidly, Europe will need to grow even faster in order to maintain its share. This explains the apparently unrealistic nature of the 20 percent target.

Europe's situation is actually mixed. It is not competitive in many areas of high-end chip design and advanced foundry production. It is dependent on foreign sources for many advanced chips and the digital hardware that embeds them. But it is not weak in all areas. For example, for the most advanced chips, nothing can be done without extreme ultraviolet lithography, in which ASML plays a key role. Europe has deep research capabilities, strong industrial users, power electronics industries, sensors, vehicle design and parts of the equipment and materials industries. Those do not assure self-sufficiency. They provide an advantage. That can be the starting point for a European chip strategy.

This also alters the meaning of successful. A new fab is beneficial when it addresses a specific niche, addresses the European market and links with local suppliers. It is undermining when not integrated with the chain, relying on foreign customers and enabling without affecting the entire chain. The situation is quite similar for research. Breakthroughs in a lab have their importance when firms can bring about acceptance, prove, certify and commercialize them. The policy problem is not research against production, it is the fragile link between the two. A better European chip policy could finance this link more effectively.

This is the measure of the advantage of the indispensability frame. It guides policy by criteria. Europe's funds should not be distributed to just any segments because they all seem strategic. They should reinforce positions where the European presence would be irreplaceable. That lends itself to three questions. Is the activity done close to any present real bottleneck in the global chain? Are European firms or research centers capable of establishing a lasting lead in such activities? Would losing this lead result in European access to chips falling below prestige? These are much more powerful filters than whether a project would allow the incremental production share to fill up. They tie resource flows to power.

But the same evidence also shows why 'made in Europe' is a misleading slogan. Many of the European industry uses are not the world's most advanced chips. Automotive, industrial machinery, energy, medical and defense markets regularly require robust, secure, application-specific chips: some are mature-node chips, some are power chips; some require close coupling of design, certification and software with the finished product. A European chip strategy that pursues only the state-of-the-art logic technology nodes may fail to attract the chips most vital to that industrial base. Indispensability is about defining significant roles, not finding symbolic targets

What the review gets right, what needs sharper boundaries

Of this argument, the sharpest point is its realism. It recognizes that the semiconductor chain is too expensive, too complex and too specialized to be reconstructed within a single region. It is not defeatist. It is a simple industrial fact. A big advanced fab can cost tens of billions of euros before it starts to get economies of scale. It needs people, power, water, suppliers, customers and a regular stream of new process innovations. Giving it a subsidy can help secure a project, but it does not automatically create a connected ecosystem. The review is right to argue that Europe should steer clear of chip policy becoming a battle of headline stories.

The point about the argument over dependency is also right to categorize it as something that runs both ways. A weak actor depends, but provides little. So, however interdependent the stronger is, it still retains something that is needed. This is the basis of sovereignty through indispensability. If indeed Europe remains a hub for the highest levels of advanced equipment, photonics, research, industrial applications and certain chip technologies, then those who want them down the line will need to keep Europe in the network. It's still a risk, but it's a different type of risk; a changed bargaining position. It effectively gives Europe the chair when the discussion on export controls, standards, supply assurances and investment decisions takes place over the course of the future.

The indispensability strategy requires boundaries. The indispensability strategy must have boundaries. A bottleneck becomes leverage only if Europe can defend it. That means more export-control capacity, more investment screening, cyber resilience, supplier mapping and a clearer picture of foreign pressure. It also means not relying too much on just one champion. ASML is a European bulldog worth protecting but no single firm can hold the fort for a continental strategy. Europe must defend the layers of suppliers, engineers and optics, the software and research links that make the formidable reputation possible.

There is also another risk. Indispensability can sound like a polite alternative to monopoly. That would be a mistake. The objective should not be to turn every European strength into a weapon. The objective should be to make access to Europe so valuable that pressure on Europe itself is too expensive. This is a defensive strategy, rather than a bid for dominance. It requires confidence among friends, including the United States, Taiwan, Japan, South Korea and other like-minded economies. It also requires a credible China strategy, because many European firms sell into China and depend on global demand. That is why geopolitical risk must sit inside chip policy, not outside it. A credible European chip policy must sustain impact while not shutting Europe off from the markets that provide funding for innovation.

Lessons that policymakers should learn from this European chip strategy review

The first policy lesson is that Europe needs a better map before it can secure another grand objective. The EU should be concentrating on mastering the points at which European firms, labs and suppliers are hard to substitute and those at which Europe is catastrophically vulnerable. That map must cover design software, equipment subsystems, advanced packaging, compound semiconductors, power electronics, strategic resources, testing and end-market demand. It should not languish in a filing cabinet. It should not be used to justify allocating funds, trade policy, skills policy, public procurement, or crisis responses. Without that map, Chips Act 2 will risk inheriting the vague language of Chips Act 1.

The second lesson is that money has to be more coordinated. Europe is not short of ambition. What it is short of is a clear linkage between EU-wide goals and national policies. Where member states compete and put public money into the same few big projects, it costs more and gets more fractured. A more ambitious European chip strategy would direct EU funds, where appropriate, towards cross-national assets that no single state can assemble alone. Pilot lines, advanced packaging platforms, shared design infrastructure and supplier-upgrade funds all fit the bill. Though rather less eye-catching than a mega-fab announcement, they may prove better at delivering an entire ecosystem.

The third lesson is that demand matters. Europe cannot build a chip base only by funding supply. Link the chips policy with industrial use. Automobiles, robotics, clean energy, health tech, aerospace, telecoms and defense have a right to participate in the debate on what European chips should be. Markets should be used by public procurement in the field of security; standardization in the area of trusted and low-power chips; universities and technical institutes in the field of training engineers as designers of industrial chips. The skills gap does not arise in education alone. It is part and parcel of the production base.

The temptation probably is that this strategy simply is too modest for a harsher worldly age. That temptation, too, has its point, but it is pointing in the wrong way. A self-sufficiency race can not make Europe safer; rather, it would do so if it drew resources to fragile positions while its current assets just wither away. Resilience comes from diversified access, trusted alliances and control of critical nodes. It also comes from scaling only where Europe has a real market, a real capability and a real strategic reason to invest.

The final lesson returns to the 11.7 percent warning. If the only yardstick by which Europe's performance is ranked remains the share of global production, what may be a victory could be a tragedy and what may be a tragedy could, in some respects, be a victory. A larger share is a boon only if it brings with it better access, security and industrial strength. The acid test is whether Europe controls enough choke points along the chain of a semiconductor to be safeguarded in a crisis and be able to define the rules of the game in normal times. That is the key to the review. Europe must not settle for a chip strategy that aims at doing everything but for a chip strategy that aims at making Europe unmissable.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

ASML Holding N.V. (2024) Annual Report 2024. Veldhoven: ASML Holding N.V.

European Commission (2023) Regulation (EU) 2023/1781 Establishing a Framework of Measures for Strengthening Europe’s Semiconductor Ecosystem. Brussels: European Commission.

European Commission (2026) European Chips Act. Brussels: European Commission.

European Court of Auditors (2025) The EU’s Strategy for Microchips: Reasonable Progress in Its Implementation but the Chips Act Is Very Unlikely to Be Sufficient to Reach the Overly Ambitious Digital Decade Target. Special Report 12/2025. Luxembourg: European Court of Auditors.

Poitiers, N.F. and Schenk, T. (2026) Revamping Europe’s Chips Strategy: Indispensability, Not Self-Sufficiency. Brussels: Bruegel.

Semiconductor Industry Association (2025) Global Semiconductor Sales Increase 19.1% in 2024; Double-Digit Growth Projected in 2025. Washington, DC: Semiconductor Industry Association.

World Semiconductor Trade Statistics (2025) Global Semiconductor Market Approaches USD 1 Trillion in 2026. Frankfurt: World Semiconductor Trade Statistics.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.