EU Strategic Autonomy Is a Race Against the Clock

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

EU strategic autonomy depends on reducing critical bottlenecks, not cutting trade China-linked inputs matter most where Europe cannot switch suppliers quickly The answer is targeted de-risking, stockpiles and crisis planning

A small supply shock could be more costly than a large trade deficit. A European Central Bank experiment found that an upstream 50 percent disruption to China-linked inputs, under selected assumptions, could result in a 2-3 percent reduction in manufacturing value added for five euro area economies. This figure should lead the EU strategic autonomy debate. The threat is not total goods purchased from China; it is that a small upstream delay can unexpectedly shut down a large downstream system. A magnet, chemical, graphite product, or refined mineral may be a triviality in customs data but still hold up vehicles, wind turbines, motors, chips, or defense gear. EU strategic autonomy is therefore not a question of slogans but of time. How long can Europe maintain operations when one difficult-to-replace input ceases to function? Effective policy should reduce that margin without scaling up every supply chain in Europe.

EU Strategic Autonomy Starts With Time to Substitute

The typical starting point is to look at import shares. This is the wrong place to start. Large imports can be relatively simple to replace, while small imports may prove impossible to bring into line in a crisis. A better test asks whether production or processing is highly concentrated, whether the input is embedded within a broader industrial system, how long it would take to qualify a different supplier or redesign the product and whether political tensions could restrict access. EU strategic autonomy only becomes meaningful when these questions are analyzed at the product, plant and process level. It takes out the rhetoric about too much dependence; it also dispels the phony dilemma of open markets and self-sufficiency. Europe need not produce everything; it needs to understand which absent inputs and ingredients would halt production before a substitute could be brought online. It is not the export value of the good that matters, but the number of days between disruption and an adequate replacement.

The size of EU-China trade still counts, but it doesn't count by itself for political bargaining power. In 2024, the EU sold roughly 213 billion in goods to China and bought 519 billion in goods from China. The deficit was just shy of 306 billion. These figures demonstrate the importance of the relationship; they do not demonstrate how Europe might be compelled to shift policy. Firm-level input data is of greater value. According to the ECB analysis, about 17 percent of extra-EU imports were marked as foreign critical inputs and one-third of these were supplied by China. Such a concentration becomes critical when supplies are small and new suppliers require long incubation by quality assurance, adjustment of tooling, or regulatory holidays. EU strategic autonomy should initially target these slow-switching goods. A universal tariff on routine imports may increase costs and leave the initial struggle unchallenged. A narrow continuity plan might do the opposite.

Small Inputs Can Create Large Political Power

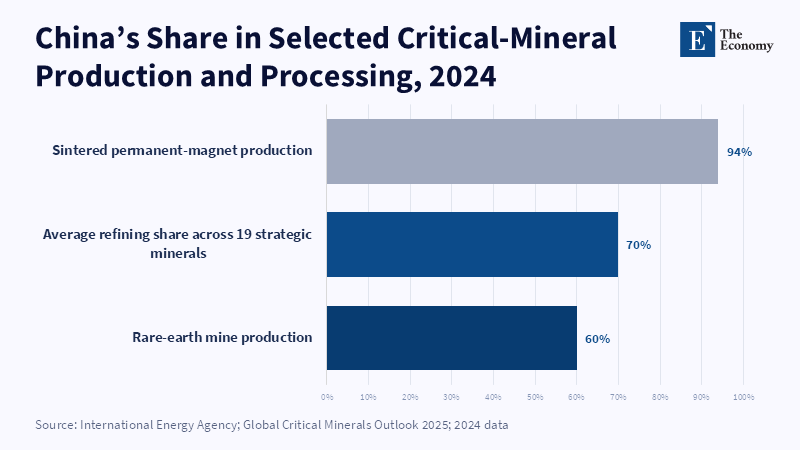

China is strongest at the center of critical supply chains. It is the world's dominant refiner of 19 out of 20 strategic minerals, across the minerals assessed, with an average share close to 70 percent by value; and in 2024 it accounted for roughly 60 percent of rare-earth mining and for 94 percent of sintered permanent-magnet production. The leap from mining to processing and magnets is of critical importance. A mine operator can set up in some other country and supply the ore, but it might depend on Chinese separation, refining, equipment, or technological know-how. This is why a sign on a plant does not equate to control. The acid test is whether production would keep flowing without one country's feedstock, licenses, software, machinery, or expertise. EU strategic independence calls for a complete picture of this supply chain. Domestic assembly is of limited value if the hard stage still remains firmly in a foreign land.

Statecraft is less likely to require a full ban. Licensing mechanisms can be used to bring pressure through delay, uncertainty and imbalanced approval. China introduced controls on gallium and germanium in 2023, graphite in late 2023, antimony in 2024 and rare-earths and their processing in 2025. Licensing restrictions represented 16 percent of the trades of the monitored critical materials in 2024. Shares of some minerals were much higher. This again does not establish that each rule was written with the aim of intimidating Europe. Consideration of national security, industrial policies and local supplies may also explain restrictions. Intent, however, is not everything. Capacity counts. A government that can impede a key material has other options it can factor into its decisions. The right reply is not to panic but to de-link the exposure, disruptive potential, actual coercion and projected intent. Combining those four categories causes policy to be either too meek or too excessive.

The dispute over Lithuania illustrated why a narrow form of coercion warrants more attention than bellicose discourse about economic war. Chinese customs and commercial practices were accused of discriminating against Lithuanian products and components assembled elsewhere with Lithuanian content. The dispute was not concluded in a definitive legal judgment and the case did not produce a final ruling. Despite this, the event demonstrated how pressure can take effect through a common production network. A government need not blockade each border. Instead, it can curtail the benefit of using a country's components, disrupt businesses and compel investors to pressure a government into reversing trends. Deep commerce ties may discipline such mobilization because China also depends on the European market. Nonetheless, discipline is not safety. A limited stick may be easier to maintain than a comprehensive embargo because it applies duress without wrecking the entire relationship.

The Zone of Dependence Is a Portfolio Problem

Still, the most hazardous dependencies for Europe occupy a sector of reliance where the industrial stakes are high, but public trust is low. It is misleading to think of that sector as made of 'unfriendly states', because it varies with the product concerned and even within each product from stage to stage of production. China is a fragile supplier for magnets, graphite anodes, or certain refined commodities, but a safe one for consumer or mass-market goods, with abundant competition and modest switching costs. India, Brazil and other middle powers can contribute to mixing the sources, but none is an ideal clone. Accumulated reliance could be made safer without being automatically riskier. The same applies within Europe. Foreigner-owned yellow or greenfield plants may still face exposure if they rely on imports of ownership books, feedstock, equipment, or patents. In 2021, China represented approximately 52 percent of the import value tied to 137 products labeled as strategic dependencies. A more recent EU approach calculated the existence of 204 dependency-rated industrial products that proved relevant in sensitive industrial systems. These are simply indicative alerts and not a fixed rating.

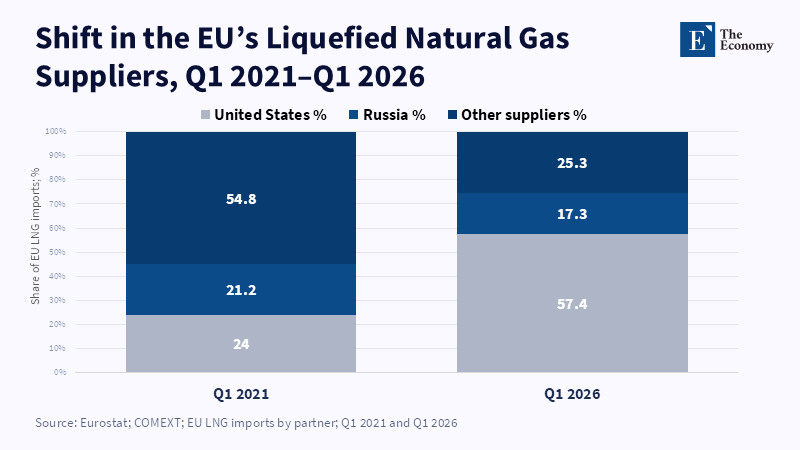

Allies also create dependence. In 2025, the US was the provider of nearly 58 percent of the EU's additional liquefied natural gas imports. That reliance isn't the same as dependence on China. Security bonds, legal channels, common institutions and crisis consultation make it more controllable. Still, friendship doesn't erase commercial risk or policy changes. EU strategic autonomy should thus avoid two over-simplistic schools of thought. One sees all foreign providers as threats. The other considers the alliance as always and automatically a safe option. The benchmark is between uncontrolled concentration and under controlled dependence. A supplier relationship becomes safer if treaty conditions put the alignments in priority, if standards ensure that it can turn easily elsewhere, if multipath ways and planning structures are in place and if allied countries maintain a crisis policy. Politics is put next. Yet, the setting counts more. Strategic autonomy means keeping options alive should a major power alter its direction.

EU Strategic Autonomy Needs Managed Interdependence

Today, the same is true for artificial intelligence. Sovereignty is commonly explained as 'a nation's control of chips, clouds, data centers, models, data and talent'. Very few countries can own all these layers. An analysis of AI infrastructure projects concluded that in early 2026, 52 percent of the world's tracked projects made use of hardware manufactured by Nvidia. India has access to around 38,000 GPUs, which are made by American companies. Yet this did not render its domestic AI policy ineffective. It demonstrated that it is possible to maintain sovereignty over specific layers while remaining reliant on others. States can exert control over local data, influence social applications, develop language models, establish security protocols and bargain for access to foreign computing. The pertinent lesson from Europe's physical supply chains is simple. EU strategic autonomy should focus on maintaining sovereignty over core processes, not every element. Managed "interdependence" may offer more options than costly pursuits of absolute sovereignty.

Such a policy relies upon practical tools. Firstly, the EU needs a supply-chain observatory of a small selection of system-crucial inputs. It should show custom data, firm sourcing, inventory, certification issue, ownership and technological links. Secondly, alternative suppliers must be commercially sustainable prior to a crisis. Long-term purchase agreements, European Investment Bank backing, common standards and pooled demand can preserve second sources when Chinese prices are more competitive. Thirdly, stocks are merely a buffer, not a substitute for markets. They should compensate for the delay for firms to switch, close, redesign, or cut use. The Critical Raw Materials Act is moving toward this direction as, through 2030 targets, it promises 10 percent of domestically mined, 40 percent of processed and 25 percent of recycled raw materials. Those should be defined as risk boundaries and never be converted into a promise of autarky.

Needs also need practice. A paper plan can fall apart if ministries, firms, ports and regulators find themselves in disagreement over facts or rules. The EU should conduct planned crisis simulations for magnets, battery materials, semiconductors, medicine and a handful of energy supply chains. Each simulation should establish how quickly the vehicles of information, authorization and production are deployed; who recognizes the shortage first; how quickly stocks can be released; who receives priority; and how quickly a substitute obtains the necessary approval. Co-production arrangements with partner states should include provisions for handling emergencies, binding schedules, quality of information transfer and arrangements for delivering and contemplating holding stocks. Otherwise, diversification could migrate a bottleneck without alleviating it. EU strategic sovereignty depends on these unspectacular, perhaps tedious, details. A second source can only be counted on when it can deliver the precise level and quality of inputs required, in a timely fashion, in a crisis.

EU Strategic Autonomy Needs a Crisis Clock

Yes, critics are right to believe the case for resilience is costly. Additional suppliers increase unit costs. Redundant certification takes time. Public help to keep weak firms alive. Chinese investment can provide a European company with jobs, capital and useful capacity. European inter-dependency still restricts the potential benefit of unrestricted trade conflict. The key test is practical. How much would the risk of disruption cost in the long run?

There must be lifelines if substituting production in another location is sluggish. The form of policy must fit the form of cause. When mispricing and subsidizing occur, action belongs to public policy. When trying to control critical assets, screening of investments is a must. When trying to induce political change, the Anti-Coercion Instrument is a head. When shocks are short, stockpiles are at hand. For Europe's industrial future to be dubbed strategic, every problem would need to be strategic. For Europe's strategic future to be protected, powerful weaknesses would need to be ignored until a crisis.

The first number now has sharper connotations. A 2–3 percent decline in manufacturing value added is not a prediction of doomsday. It indicates how quickly a high concentration of inputs can do damage. The aim is to prevent that first jolt from becoming a political constraint. Every vital supply route should have a crisis clock: days of stock, time to allow another supplier, time to alter a design, time to resume output. Where the clock is too short, government intervention is justified. Where firms can switch easily, international trade should be maintained. Europe does not require a withdrawal into economic self-sufficiency from China and the US, nor from its other trading partners. It needs sufficient options to refuse cooperation where access is contingent upon coercion. Only then can Europe's promised strategic autonomy be trusted: businesses able to take a hit and politically able to choose. Preparation should start now.

This article is based on an original research article published by The Economy Research. For the original version, please refer to [EU vs. China] When Supply Chains Become Statecraft: China and the Geopolitics of EU Strategic Autonomy.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Aguilar, P., Darracq Pariès, M., Jouvanceau, V., Meunier, B. and Spital, T. (2026) Global Implications of Export Controls on Rare Earths: A Model-Based Assessment. ECB Occasional Paper No. 384. Frankfurt am Main: European Central Bank.

Arjona, R., Connell García, W. and Herghelegiu, C. (2023) An Enhanced Methodology to Monitor the EU’s Strategic Dependencies and Vulnerabilities. Brussels: European Commission.

Essers, D., Lebastard, L., Mancini, M., Panon, L. and Timini, J. (2024) ‘Critical inputs from China: How vulnerable are European firms to supply shortages?’, The ECB Blog, 9 October.

European Commission (2021) Strategic Dependencies and Capacities. Commission Staff Working Document SWD(2021) 352 final. Brussels: European Commission.

European Commission and High Representative of the Union for Foreign Affairs and Security Policy (2023) Joint Communication on a European Economic Security Strategy. JOIN(2023) 20 final. Brussels: European Commission.

European Parliament and Council of the European Union (2024) Regulation (EU) 2024/1252 Establishing a Framework for Ensuring a Secure and Sustainable Supply of Critical Raw Materials. Official Journal of the European Union.

International Energy Agency (2025) Global Critical Minerals Outlook 2025. Paris: International Energy Agency.

International Energy Agency (2026) Designing an Effective Strategic Stockpiling System for Critical Minerals. Paris: International Energy Agency.

Joshi, S. (2026) ‘Early Lessons in the Pursuit of Sovereign AI’, Carnegie Endowment for International Peace, 17 June.

Organisation for Economic Co-operation and Development (2026) Critical Raw Materials Face Rising Export Restrictions, Increasing Risks to Global Supply Chains. Paris: OECD.

The Economy Research Editorial (2026) ‘The Geopolitics of Compute: Sovereignty, Power and Strategic Dependence in the AI Infrastructure Race’, The Economy Research, 18 June.

The Economy Research Editorial (2026) ‘When Supply Chains Become Statecraft: China and the Geopolitics of EU Strategic Autonomy’, The Economy Research Series.

World Trade Organization (2022) China—Measures Concerning Trade in Goods and Services: Request for Consultations by the European Union. WT/DS610/1. Geneva: World Trade Organization.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.