When AI Trading Turns Private Logic Into Public Risk

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI trading can turn private choices into one crowded move DQN tools may create stronger herding than LLMs The policy goal is market diversity, not just smarter trading

AI trading is moving beyond hedge funds, banks and dedicated desks. It is arriving through broker apps, chatbots, individual trading platforms, digital prompts, and agentic tools that can turn loose goals into trading rules in the hands of ordinary investors. That sounds democratic. It may also be dangerous. The historical market concern was that large institutions could move together, creating a liquidity drain. The newer worry is that millions of retail investors may act as one large fund, and not in a good way, because their AI machines draw on the same data, copy the same online prompts and find the same private exit. It is not just bad advice; it is market design. When AI-enabled private decisions look the same at scale, private optimization might turn into public instability.

AI Trading And The New Herding Problem

The real question is not whether AI trading will beat the market. That is far too narrow. Some models will do useful things to investors: decipher filings, find cross-asset relationships, do risk calculations and remove emotion from trading. Some will make terrible bets. Some will generate overconfident falsehoods. But this is an internal matter. The real policy issues are external to performance. They are about what happens when large groups of investors are all using similar machines to attack similar problems. Markets thrive on a lack of convergence. They need sellers and buyers, risk takers and hedgers, patient capital and impatient capital. Too much convergence is bad. Liquidity is not a problem when everything is busy in good times, but it can drop to nothing in a flash when the same thing is on everyone’s screens.

This is the point at which the Hirshleifer effect adds some nuance to the debate. Information that is privately valuable isn't necessarily socially valued. Certainly, the signal is worth something to an individual investor if it helps him avoid a loss. But if the same signal floods the market and masses, it can wipe out the insurance role that markets play as risk-takers hedge. There is a derivative hedge for what the investor does because there's a market of willing transactions in the other direction. If everyone gets the same news and sells, you have no market in the other direction. It's not just a re-pricing. The instrument can, in extremes, gap down. At that point, social utility might actually be negative, as the signal uncovered the diversification preconditions for the trade.

AI trading introduces this problem because it can amplify similarity. Human investors herd too, but with noise; they hear different signals, panic at different levels and make mistakes in different ways. AI systems could compress that variation. A retail trader who asks a bot for a "safe approach during a downturn" might be fed a program that looks very similar to another trader's. A customer who uses a popular trading prompt might copy not just a technique but a covert method of coordination. This is not collusion. It is accidental convergence. It is market crowding without a conference room.

Why DQN And LLM Systems May Create Different Risks

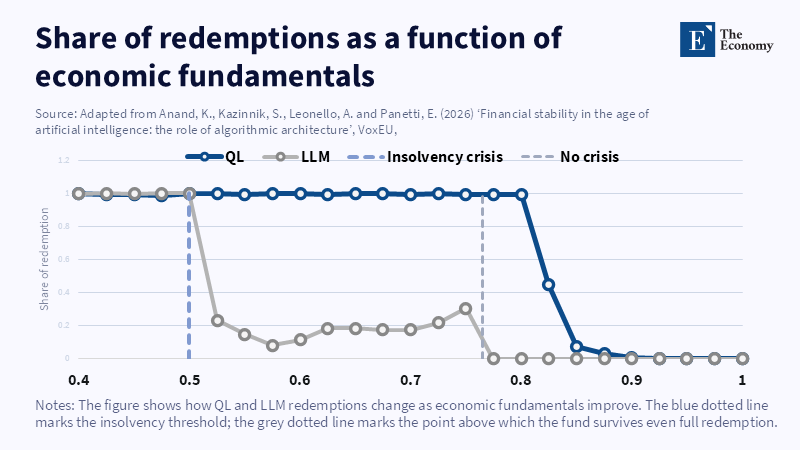

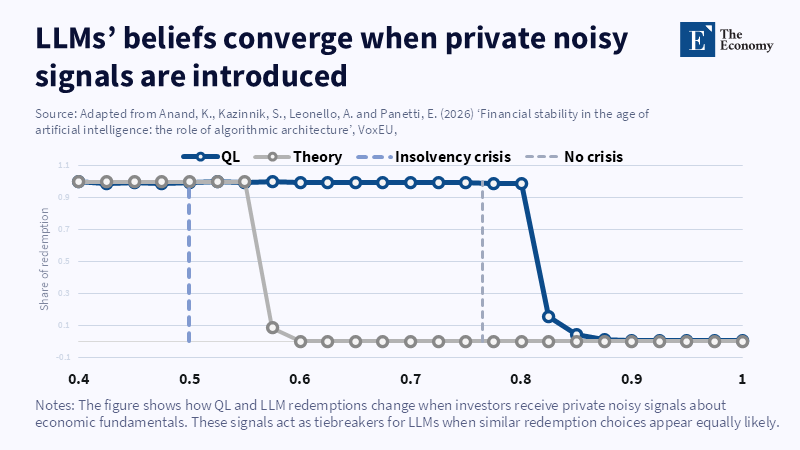

The policy distinction between reinforcement learning systems and large language models matters because they fail in different ways. A DQN-style system learns through cycle after cycle of probes and Paythru-show me where the action that preserves Paythru at a given environment is. Over the redemption or sell decision, that kind of model may learn that to get out early is safer than to expose oneself. Having learned that lesson, the model can operationalize it again and again, as long as fundamentals aren't pushing agents to panic. If a good number of similar agents have learned the same lessons through similar stress episodes, the same reflex can spread: the private logic of the model is Leave before others leave-the public consequence as seen through a wholesale selling behavior is worse, so despite the fact that by any measure things aren't actually worse, each agent tries to use the collective behavior to shape their own: take yourself out a little earlier and the exit shrinks to nothing.

This is not how LLMs function. They do not optimize via the narrow form of trial and error. Instead, they think through prompts, context, examples and language cues, which can introduce more variability. One investor may be interested in a long-term forecast. Another may be interested in dividend security. Yet another may be interested in a stop-loss plan, etc. Even if the output all came from the same foundation model, the context of the prompt has the capacity to bend the responses to different central tendencies. While this heterogeneity might make the risk of a single, clean, coordinated run go down, it will not eliminate systemic risk. Instead, LLMs can be unstable in a different way. They can sound confident when they are wrong. They can overreact to headlines. They can magnify weak signals by turning them into robust guidance. They can also converge when they are used by similar online communities.

This difference is important. DQN systems could generate a more concentrated threat of collective exits because their incentives tend to push them toward the same call for defense. LLM systems could generate a less concentrated but more diffuse threat because they influence beliefs and incentives through language. A market full of DQN-style agents may resemble a crowd trained to run for the same door. A market full of LLM-guided traders may resemble a crowd listening to different speakers who draw from the same library of stories. The first risk is mechanical coordination. The second is narrative coordination. Both matter, but the policy response should not treat them as identical.

Panic case is when that bifurcation breaks down. Normal markets, in other words, the market structure may dictate whether new traders synchronize or differentiate. But in falling markets, indeed, terror itself may be the "common" trigger. Then a user need not have a sophisticated set of moves, fresh out of the dramaturgy manual. Once the portfolio glows red, the social media simulations glow red and the chatbot asks, "Sell this one before it gets worse?" Under duress (as during fishing trips), LLMs may converge because their users are convergence-prone. DQN trade systems will sell because the learned utility points toward selling. LLMs may recommend risk reduction because the human prompt penalizes loss. Different architectures can thus "converge" in the same place: synchronized selling.

The SVB Lesson For Retail AI Trading

Silicon Valley Bank demonstrated how quickly modern coordination can operate. It was not an AI trading event, but it was a reminder about the speed, networks and digital exits. A culture of concentrated depositors, digital channels, mobile banking and collective fear transformed a threat into a rush in a time frame that traditional bank regulation simply was not designed to cope with. The market takeaway is simple. To act in a coordinated way, a system does not need one in control, but rather shared levels of vulnerability, rapid lines of communication and a shared motivation to act. AI trading could complicate this pattern by turning a collective fear into actionable portfolio decisions.

Retail AI trading also exacerbates the scope. The bulk of one retail investor will not destabilize the market; what will be destabilizing might be a large set of one million retail investors who use the same group of tools. The proliferation of broker-integrated assistants, natural-language trading tools, robo-advisers and user-shared prompts means the retail layer is likely to become more automated without ever seeming institutional to regulators. They know to watch the big funds because they are visible, leveraged and systemically important. But a cluster using the same tools can become systemically relevant without any of the users being large; this is the hard part. The risk spreads at the level of the user, but converges at the level of the model.

A frequent critique is that the retail investor remains too small to matter in deep markets. That judgment is too complacent. Retail flows already matter in some stocks, other options markets, crypto assets, thematic ETFs and stress-sensitive names. AI-driven trading may also make markets more efficient in calm periods but more volatile during stress. They matter more still in conjunction with market makers, margin calls, social media and bank-like products that offer instant liquidity. AI trading may not shift the entire Treasury market tomorrow. But it can first move to congested virtual corners of the market. From those points, shockwaves can reach through ETF holdings, derivatives, collateral values and market apprehension. Financial panics often originate in pockets that appear minuscule until the chain reaction gets underway.

A second argument is that AI could improve diversity by offering more customization of portfolios. This is an argument not to be dismissed. For example, a convincing LLM adviser could try to probe questions about time horizon, income needs, tax position, debt, age, liquidity requirements and risk appetite. It may need to slow people down. It could prepare clients for the value of not panicking and selling out. It could bring more patient retail capital to markets. But you need to engineer this; it will not happen automatically. If your model incentivizes additional page views, clickthrough, hanging in there for answers, even if they make no sense at all, the AI trading tools will be encouraging that customer type toward activity, not patience and restraint. Customized investing must be real, not just a marketing flap offering a new label applied to the same old model.

What Regulators Should Measure Before The Next Shock

The first policy step should be to begin treating AI trading less solely as an investor protection issue. Suitability remains important. Fraud remains important. Hallucinated advice remains important. But the larger concern is correlation. That concern is part of the wider debate on AI-related financial stability risks. Policymakers should look at whether a range of models are pointing toward the same trade when the market conditions are identical. They will need a new kind of stress test. Instead of simply asking if a model achieves high accuracy, they should ask how a basket of models performs when given identical and dissimilar prompts.

The comprehensive test ought to produce different results for DQN-style and LLM systems. For reinforcement learning tools, overseers should check rewards, training environments, stop-loss behavior and learned exit rules. A model that continuously learns to bail out early when in doubt may be privately reasonable but conversely fragile in society. For LLM tools, overseers should examine prompt sensitivity, reluctance, confidence, source filtering and panic-inducing advice. The crucial issue is: does the model reassure, uniquely diversify, or unavoidably stiffen one's exit? A polite answer that says "sell now" is not necessarily a destabilizer.

Disclosure must change as well. Platforms should not be able to simply state that they are using AI. Investors and regulators should be told what kind of AI is used, what the tool is designed to do, whether it can trade, whether it shares a model with other tools, how standardized prompts are and whether the provider monitors correlated outputs. Giving these high-tech products a simple label can distinguish between information tools, recommendation tools, strategy tools and execution tools. This would make it possible for investors to recognize when they are reading analysis and when they are being nudged toward action; for regulators to see where automation begins.

Market design must then take over some of the burden. This matters for capital markets because liquidity depends on diverse positioning, not only faster execution. Circuit breakers, volatility halts, margin rules, redemption gates, liquidity buffers-these were designed for the pre-AI iteration of speed. They may have to be redesigned for AI reaction time. Exchanges and brokerages should observe not only order flow but model-linked order flow whenever feasible. If a substantial fraction of similar orders is arriving following a common AI-generated cue, it should be detectable by a supervisor. Privacy must be maintained, but the proliferation of models can be monitored at the aggregate level. The end goal is not to monitor the prompts issued by individual users. The end goal is to monitor the end result in the aggregate, so that the market is not transforming itself into one oversized computer.

Here is the most important rule-it's the simplest: AI trading systems must be designed to protect and maintain disagreement. The systems should not be set up by default to lead to generalized strategies. The systems should introduce friction and noise during high-stress times. The systems should pay attention to the pain of compounding and rapid loss. They should measure the impact of trembling and knee-jerk selling relative to appropriate rebalancing, holding, or hedging strategies. They should display that impact when users are considering trade decisions. They should discourage crowding by issuing strong warnings before triggering a trade. They should separate education from trading execution so that an nervous investor browsing a platform cannot click from a terrified state right into a trade with one click. And whether it ultimately makes trades or not, good AI in finance should sometimes slow down.

The Real Test Is Social Optimization

AI trading will not and should not be banned. It can democratize diagnostics, reduce search costs and improve long-horizon intertemporal welfare for households. The danger is that all tools are held accountable solely according to their private performance. A trading rule that helps one investor may be a source of market fragility. A signal that optimizes to perfect efficiency is still potentially destabilizing. Selling rules designed to protect one account are still potentially harmful when disseminated among thousands of investors. That is the essence of the core insight of the Hirshleifer effect ('25) form. Information and optimization are not in themselves equivalent to stability.

Thus, the next frontier of regulation should move from "Is this AI system fair to one user?" to "What happens when many users rely on similar AI systems at once?" That is where financial policy should focus. That is the bridge between retail decision-making, the model architecture, the use platform interface and the liquidity of markets. That is the incremental step regulators could take to expand the requirements of the Model Concentration regulation, impose the appropriate stress test on correlated outputs, encourage the categorization of AI trading system types and introduce rules preventing aggregation of similar systems that would cost us a diverse market. The next iteration won't start in the bank lobby or even around the trading room table. It will begin with a similar prompt, dispensed onto a message board, answered by parallel machines, executed before the crowd even gathers.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Abbas, N., Cohen, C., Grolleman, D.J. and Mosk, B. (2024) ‘Artificial intelligence can make markets more efficient—and more volatile’, IMF Blog, 15 October.

Advisory Ranking (2026) ‘Top 20 Capital Markets Advisory 2026’, Advisory Ranking, 28 April.

Anand, K., Kazinnik, S., Leonello, A. and Panetti, E. (2026) ‘Financial stability in the age of artificial intelligence: The role of algorithmic architecture’, VoxEU, Centre for Economic Policy Research, 21 May.

Brennan, A. (2026) ‘Could a Second SVB Crisis Emerge? High-Risk AI Trading Standardizing Investor Strategies Puts Regulators Worldwide on Alert’, The Economy, 26 May.

Calvano, E., Calzolari, G., Denicolò, V. and Pastorello, S. (2020) ‘Artificial intelligence, algorithmic pricing, and collusion’, American Economic Review, 110(10), pp. 3267–3297.

Financial Stability Board (2024) The Financial Stability Implications of Artificial Intelligence. Basel: Financial Stability Board.

Financial Stability Board (2025) Monitoring Adoption of Artificial Intelligence and Related Vulnerabilities in the Financial Sector. Basel: Financial Stability Board.

Hansen, A.L. and Lee, S.J. (2025) ‘Financial stability implications of generative AI: Taming the animal spirits’, Finance and Economics Discussion Series. Washington, DC: Board of Governors of the Federal Reserve System.

Hirshleifer, J. (1971) ‘The private and social value of information and the reward to inventive activity’, American Economic Review, 61(4), pp. 561–574.

International Monetary Fund (2024) Global Financial Stability Report: Steadying the Course: Uncertainty, Artificial Intelligence, and Financial Stability. Washington, DC: International Monetary Fund.

Office of Inspector General, Board of Governors of the Federal Reserve System and Consumer Financial Protection Bureau (2023) Material Loss Review of Silicon Valley Bank. Washington, DC: Office of Inspector General.

U.S. Securities and Exchange Commission, Division of Examinations (2026) Fiscal Year 2026 Examination Priorities. Washington, DC: U.S. Securities and Exchange Commission.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.