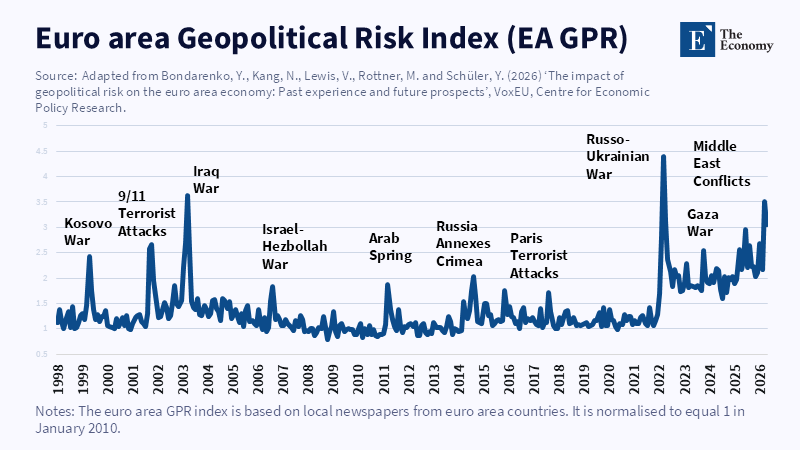

Regional Geopolitical Risk Is Not a Single Number

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Regional geopolitical risk is not a smaller version of global risk News-based indices measure exposure, language, attention and bias at the same time Europe needs a dashboard that compares global attention with local economic impact

Five countries - Germany, France, Italy, Spain and the Netherlands-collectively generate nearly four-fifths of euro-zone output. But a large part of the world still perceives geopolitical risk through a more limited window: English-language news outlets, many driven by US or broader Anglosphere interests. This discrepancy is not a side note. It alters the empirically estimated magnitude of a shock. It alters the policy response. It renders a war on Europe's doorstep a faraway diplomatic event that European firms and families will experience in the form of higher gas bills, supply disruptions, weaker confidence and upward pressure on prices. Regional geopolitical risk, therefore, does not exist alongside global risk; it constitutes the actual measure of risk for decisions in a "real" place. The important issue is not whether one index is "correct"; rather, it is which risk one would want to be exposed to, in what language and with what kind of fear built into the signal.

Regional Geopolitical Risk Needs a Local Lens

Why use a risk index? They turn a chaotic world into a time series; they offer a clear pointer to central banks, finance ministries, investors and business administrators to monitor developing peril. But they are not thermometers stuck outside a window; they are mirrors held up to news systems. A global index compiled from newspapers published in English captures genuine information, but also captures the news values of those sources. It reveals what editors cover, the slant those outlets take and how much space they devote to one conflict while another remains buried. That does not rob the global index of all usefulness. It makes it partial. A Washington-centric or Anglosphere-oriented measure may be a useful monitor of global attention, American market concern, or broad investor sentiment. It will be less compelling when the decision at stake involves a regional issue.

A euro-area shock that primarily hit the European energy markets the European supply chains, or European public confidence, should be assessed in the same way from the European vantage point. Geopolitical risk at the regional level should be considered a distinct perspective: not a miniature version of the broad global lens. One event can simultaneously have one global connotation and several regional meanings. That reverses the focus of the policy debate. The difficulty is not so much that older geopolitical risk indices were poorly constructed: many were carefully built and have been instructive over long time series. The issue is that they were asked to do too much. A global index may illustrate that the world is on edge. It cannot always predict where the edge will bite first, which price risks it will push, or which consumers will be hit first. That middle tier, at the regional level, falls in between global fears and national/sectoral policy in the euro area.

Proximity Changes the Economic Channel

Geographic proximity does not mean that every country nearby is under an immediate threat of attack. France, Germany, Greece, or Japan probably will not have any realistic possibility of coming under fire from Russian missiles during any given war. But that is not the correct economic question. Risk first passes through other gates. And it is through gas contracts, shipping lanes, food prices, insurance expenses, public budgets, bank credit and household anticipation. A war near Europe may, in fact, seem more present in the European press because European firms and voters are exposed to more immediate channels. That may be an emotional investment, but it is an economic one too. And it could change the way firms price energy, the way households interpret inflation and the way governments prepare aid across borders.

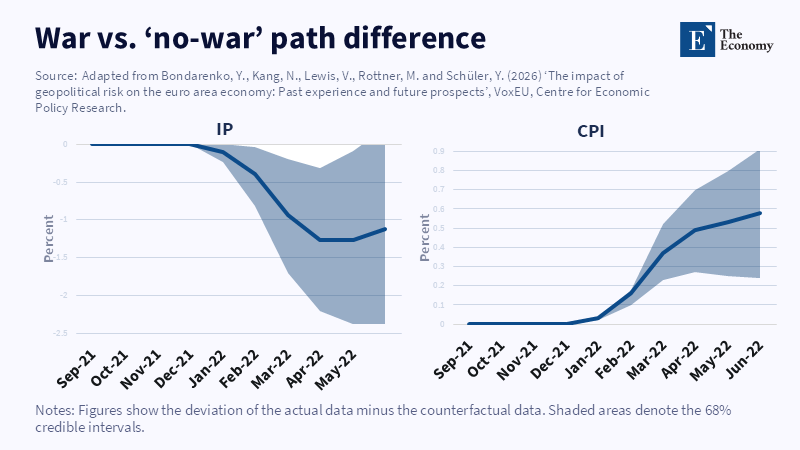

Hence, the reason regional geopolitical risk may change the estimate of macroeconomic damage. From a euro-area counterfactual perspective, conditional on the regional risk index remaining at its December 2021 level, the surges in Ukraine-war risk appear to have resulted in industrial production roughly 1.3 percent lower on average through May 2022. Similarly, consumer prices averaged about 0.6 percent higher through June 2022, while core prices averaged 0.3 percent higher. While these are modest effects in absolute terms, they are huge at the start of a shock. Then again, wider trade evidence seems to support the same point. Recent gravity-model estimates suggest that global spikes in geopolitical risk can reduce trade by roughly 30-40%, as much as a 14% increase in global tariffs. Until risk finds new routing, finance, trust and transit time channels, it acts as a form of hidden trade tax.

Market dashboards add yet another layer. Some risk tools measure market attention in brokerage reports and financial media. They can apply machine learning, sentiment scores and a chosen set of risk scenarios. They can produce very different results than a newspaper-based regional index because they are measuring a different audience. A market index asks what investors are watching. A regional news index asks what a region is living through or being told it is living through. Both may be correct. Neither should be considered the definitive voice of the world. Regional geopolitical risk is most valued when contrasted with the others, not when considered in isolation. That is why reputation is not equivalent to accuracy. A well-known global source can have huge accuracy for global attention but poor accuracy for local shock. A less well-known local source can be inconsistent, but can still provide the signal needed to price local shocks.

Regional Geopolitical Risk Still Depends on Imperfect News

The strongest possible case for regional geopolitical risk is also the weakest. Local news is closest to the shock, but it is not automatically cleaner; European media might portray the war in Ukraine with greater immediacy than Asian or US media simply because the war is closer, sources easier to reach and the economic consequences more apparent. This immediacy might convey valuable information. Or it might be home bias. A local press can exaggerate the risk to its own readers just as distant media may understate it. French newspapers might appear more panicked than Japanese papers even when the missile risk is by definition zero for both. Tone is not necessarily the same as probability in fact.

This is important because news content is never neutral raw data. Trust in the news remains both low and uneven. As shown in the 2025 Digital News Report data, trust in news in markets averaged 40%. The spread of outcomes was wide: Finland landed near the top at 67% and Greece or Hungary landed near the bottom at 22%. These outcomes can matter for a news-based index. If confidence is low, or polarised media is entrenched, or editorial control and neutrality are weak, these local conditions may so alter a risk-oriented index that it reports not just risk but also media tension. The context of war may have so distorted fear, national interest, or moral shock to be conspicuously present in coverage that a regional index may incorporate metrics of fear, fatigue, or political framing along with hard exposure. A regional index can thus be more personally relevant and potentially more biased at the same time.

The answer is not to dismiss regional news. The answer is to audit it. A robust system covering regional geo-political risk would indicate the newspapers considered, detail the languages included, show source weightings and identify whether tabloids and highly partisan or campaign-driven outlets are excluded. It would examine whether state-linked media signal differently to the regional press, compare signal frequency to sentiment and check if the index is driven by energy prices, freight delays, credit spreads, trade flows and inflation expectations. There is another problem hidden within the regional approach: economic weighting. GDP would help quantify the euro-area aggregate output and inflation. But it doesn’t account for frontline risk within smaller countries and sub-regional indices can identify the geographical hot-spots of political pressure and security risk. They can also distinguish euro-area inflation from national security concerns, a crucial differentiation when policy tools are common, while anxieties are not.

Policy Should Use a Dashboard of Disagreement

The biggest policy mistake is asking what index is one hundred percent right. Instead, ask why the indices disagree. If the global index remains calm, for example, while the regional index rises sharply, it can suggest that the shock is localized enough in its economic effects that it is not fully recognized by global markets. Conversely, if the global index rises sharply but regional indices remain calm, it could suggest that investors are responding to a broad explanation that regional firms have yet to experience. In either case, disagreement is not just noise; it's information about where attention, confidence and fear are not aligned. Knowledge about these differences can guide policymakers as to whether the shock is mostly a faraway market story, a local supply story, or a public confidence story. The spread between indices should be carefully monitored as a flashing light. It signals that an event is being priced, explained and experienced differently.

Monetary authorities should incorporate regional geopolitical risk indicators as a default input into inflation analyses. A regional shock that increases prices but tightens output is difficult to diagnose with typical demand-side instruments. Raising rates can prevent second-round effects; however, it cannot produce gas, ships, semiconductors, or safe passage. Finance ministries and agencies should test fiscal buffers, energy support measures and procurement arrangements by overlaying regional risk indices. Business managers should determine when to diversify suppliers, stockpile inventories and hedge transportation costs. The goal is not to forecast the next war; the goal is to anticipate when a political war is turning into an economic constraint. It also changes public communication. Officials should publish brief risk reports that display global, regional and market-focused measures together with a transparent explanation of their divergence. This would not eliminate uncertainty. It would make uncertainty visible enough to be manageable.

Regional Geopolitical Risk Must Become Policy Infrastructure

There is an obvious critique: a regional index can overreact. The regional index might overly magnify. That is correct, but it is not a full critique. A regional measure is only as effective as the responses it elicits. Households may overreact, firms may overinvest or underinvest, banks may increase credit limits or grant fewer loans-the fact of all of the above makes perception as much of a shock as hard events. Sure, an index that measures fear specifically might be inaccurate without the recognition that fear can itself be a source of shock. So whether it is in fact a mistake to measure fear does not condemn the news-based measure of local tone. It might simply be an indicator that the policy community has overlooked and all it needs. The second possible failure of a local measure is that it may be too exciting for policy via dramatic headlines and reputational pressure, which can fuel overreaction. While this risk is high, it can be muted through explicit decisions about source selection, transparent emphasis and a healthy cross-reference to hard data. The third potential failure of a news-derived indicator is that it is too flimsy for central banks. But contemporary financial systems have long operated on illusion-survey expectations, business-round surveys, carrytrade gloom and market sentiment, all of which have a profound influence on policymaking. No single source of information must be perfect or complete; the real test is whether it is useful.

A regional geopolitical risk index passes that test if it accounts for output, prices, shortages, or trade stress more accurately than a global indicator alone. It must still be questioned, examined and corrected. It just cannot be ignored in its current form. The first statistic brings us to the core point. If five economies account for nearly 80% of eurozone output, how societies interpret threats is not just a media narrative. It is a macroeconomic factor. Regional geopolitical risk should be incorporated into central bank models, fiscal stress tests, trade policy and corporate resilience planning. Not as a forecasting machine. Not as a boast. As a systematic approach to correlate international headlines with domestic risks. The next shock should not be shrouded by a single media universe and deemed truly international. Policy needs a clearer map. That map must clarify where the threat is global, regional and already a cost.

Regional Geopolitical Risk Must Become Policy Infrastructure

A regional index can overreact, but that is not enough reason to dismiss it. Households, firms and banks also react to fear, and those reactions can become part of the shock itself. The useful test is not whether regional geopolitical risk is perfectly neutral. The useful test is whether it explains prices, output, shortages, trade stress and confidence better than a global index alone.

If five economies account for nearly 80% of euro-area output, the way those societies read danger is not just a media story. It is a macroeconomic signal. Regional geopolitical risk should be built into central-bank models, fiscal stress tests, trade policy and corporate resilience planning. The next shock should not be filtered through one media universe and called global truth. Policy needs a clearer map of where risk is global, where it is regional and where it is already becoming a cost.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

BlackRock Investment Institute (2026) Geopolitical Risk Dashboard. New York: BlackRock Investment Institute.

Bondarenko, Y., Kang, N., Lewis, V., Rottner, M. and Schüler, Y. (2026) ‘The impact of geopolitical risk on the euro area economy: Past experience and future prospects’, VoxEU, Centre for Economic Policy Research.

Bondarenko, Y., Kang, N., Lewis, V., Rottner, M. and Schüler, Y. (2026) Geopolitical Risk in the Euro Area: Measurement and Transmission. BIS Working Paper No. 1348. Basel: Bank for International Settlements.

Caldara, D. and Iacoviello, M. (2022) ‘Measuring geopolitical risk’, American Economic Review, 112(4), pp. 1194–1225.

Caldara, D. and Iacoviello, M. (n.d.) Geopolitical Risk Index. Dataset and documentation.

Geopolitical Futures (n.d.) How Geopolitical Risks Influence the Global Community. Austin, TX: Geopolitical Futures.

Mulabdic, A. and Yotov, Y.V. (2025) Geopolitical Risks and Trade. Policy Research Working Paper No. 11219. Washington, DC: World Bank.

Newman, N., Fletcher, R., Robertson, C.T., Ross Arguedas, A. and Nielsen, R.K. (2025) Reuters Institute Digital News Report 2025. Oxford: Reuters Institute for the Study of Journalism.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.