Labour Share in the AI Economy: The New Divide Between Work and Capital

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI is shifting gains from labour to capital Europe protects labour more; the U.S. rewards capital more Without new rules, AI will deepen the labour-share divide

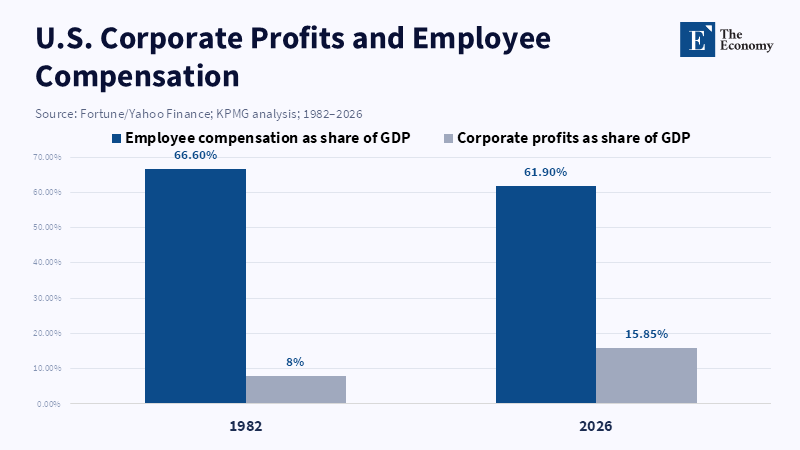

The most revealing statistic in today's economy is not the growth rate. It is the split. Corporate profits as a percentage of U.S. gross domestic product (GDP) have increased from approximately 8 percent in 1982 to 15.85 percent; on the other hand, employee compensation as a share of GDP has fallen from 66.6 percent to 61.9 percent. This gap is not only an American story. It is a clear indication of the distribution of the benefits of the current economic system. The labor share of income is no longer just an economic indicator; it is the stress test of the social contract. Although output increases, workers still feel poorer, less secure and easier to replace, leaving society feeling controlled, priced out and unnecessary. The old debate questioned Europe's over-protection of labor and America's high reward of capital; however, the impending evolution is whether AI will lead to a different new result: some having job security and others high capital rewards, the crowding-out of the middle class.

Labor Share Reveals the Real Philosophy of Capitalism

The transatlantic divide in labor share should be seen as a clash of economic logics, not just a contest of good labor against bad profit-making. Europe has treated work as a social anchor. Wages are important, but so are long-lasting jobs, bargaining institutions, sectoral bargains and the notion that companies have obligations that extend beyond quarterly profitability. The US has constructed a more flexible system. It rewards speed, capital mobility and profit capture. This system can produce rapid growth and giant firms. It can also allow advantages to go to the upper tail before workers can get their hands on them.

This does not imply that Europe is inherently fair or America is unfair by design. The picture is more mixed. Europe too experienced labor share pressure after the 1980s, not necessarily because of increased trade integration, but also because of the evolving nature of the labor market and employment growth. The U.S., on the other hand, experienced a more pronounced decline after 2000, primarily because firms to a larger extent relied on technological and automation advancements to increase output with less labor. The main distinction is not that one prefers the laborer and the other the capitalists. It is rather that, at the European extreme, adjustment is often channeled through the institutions, while, at the American extreme, market price signals usually determine who bears the burden.

That difference has significance as the economy is not just comprised of very large firms. Small and medium enterprises (SMEs) are also significant employers of workers across the Atlantic. Many are unable either to pay higher wages, cover costs, or scale automation. In the US, small firms employ nearly half of private-sector workers and in Europe, nearly all firms are small and medium-sized and they are still an integral part of employment. Any meaningful labor share policy must first and foremost ensure workers are protected without underplaying that not all employers have margins comparable to a Fortune 500 firm. A family bakery, a logistics contractor, or an equipment or supply chain enterprise is not going to be paid the same as a platform giant.

The error is to consider "capital" as one pure category. A multinational on the global tech market, a pension fund on the capital markets, a local shoe factory, or a restaurant owner sitting in a small office are on the same side of the account. They do not have the same power. A few own data, patents, platforms and pricing channels. All but one own very few "machines" and rent. This explains why a reform of the labor share must be delicate. It must go to any increased power of the workers where markets are concentrated. It cannot deprive small firms already exposed to tight costs and credit constraints.

Labor Share Is Falling Because Bargaining Power Is Uneven

The first lesson to take from the increasing labor share gap is that profits and wages are not, by default, supposed to coincide. They only move together if it is through institutions, a tight labor market, law and worker strength. In OECD countries, union density has declined from about 30 percent in the mid-1980s to 15 percent in 2023/24. Coverage of collective bargaining has also declined from 47 percent to a third, roughly. In the U.S., the union density was 10 percent in 2025 and in the EU, six out of ten workers are still under collective bargaining coverage, but coverage rates differ sharply across countries.

That gap also makes a difference in how firms respond to real pressure. When demand decelerates, the more powerful U.S. Firm is more likely to seek margin protection by laying off staff, outsourcing, sluggish wage settlement, or greater automation speedup. The less powerful European employer operating under a more balanced bargaining system is more likely to put a premium on employment, shorter hours and slower wage adjustment. This is how Europe can seem less dynamic and more persistent, while America can seem more profitable and more delicate. The labor share is not just a measure of income. It is a history of who could say no.

Indeed, the world perspective reveals exactly why this cannot be simply an Atlantic dispute. According to data from the International Labor Organization, the international labor income share in the world economy declined from 53.9% in 2004 to 52.3% in 2024. Such a slight reduction may appear to be trivial, but it is not, as on the scale of the world economy, a 1-2 percentage point difference equates to hundreds of billions of dollars. This means that growth alone will not be able to rectify the distribution issue, as an economy can grow, productivity increases, but workers can still end up worse off comparatively.

One of the critiques goes that the labor share is too wide to steer policy. It lumps wages, benefits, self-employment, capital consumption allowances, profits and national accounts. And it is right. But that is the message. Labor share is instructive because it summarizes the whole bargain, not just the wage line printed on the payslip. It gives an indication of whether growth is being shared or not at all before the corrective mechanisms of Taxes and Transfers are mustered to undo the wrongs. If pre-tax market income continues to lurch toward capital, welfare institutions will have to work flat out every year. That is not a steady state. It is a repair shop for a machine that keeps breaking.

AI Will Split Labor Share Inside the Workforce

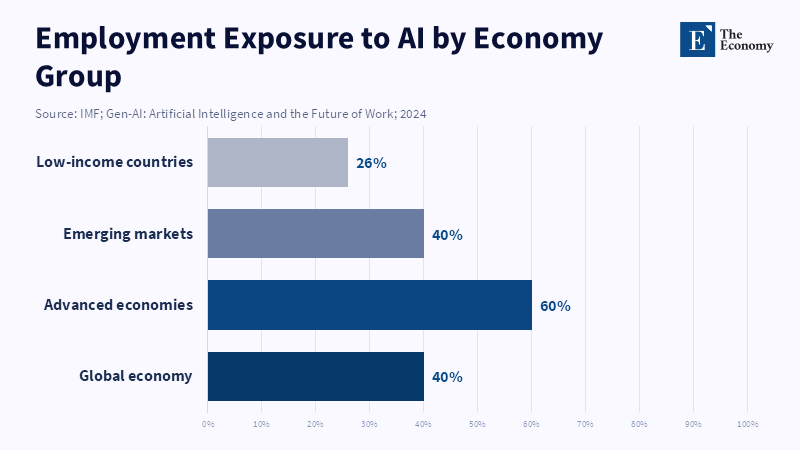

AI sharpens the labor share question because it alters the form of substitution. In previous episodes of automation, the automation was largely completed when the robot or computer replaced routine factory or clerical work. Generative AI enters domains that previously have been human-only: writing, coding, design, financial analysis, legal research, call center work, logistics and management support. According to an IMF study, it reaches nearly 40 percent of world employment; in advanced economies, it is exposed to nearly 60 percent. OECD trends analysis indicates that 'white collar' , highly educated occupations are also at risk, because AI can substitute for those non-routine cognition functions. The old career safety rule, “get more education and move up”, no longer works on its own.

But this does not imply that mass unemployment is inevitable. The exact statement above is a stronger and more accurate one. AI is capable of increasing output while simultaneously decreasing labor's claim on that output. Data from various European regions shows that higher levels of AI patent intensity are concurrently associated with a lower labor share, with the strongest evidence in industrial regions. A doubling of AI patent intensity is correlated with a decrease in the labor share of between 0.5 and 1.6 percentage points. This is not a prediction of gloom. It is an indicator that AI can be capital-biased innovation, allowing a firm to reallocate value towards owners of models, data, infrastructure, intellectual property rights and distribution networks.

At ground level, the dynamic is straightforward. In the sectors where AI makes a difference, the ordinary worker may need to become scarce and the premium can go to a handful of high-skilled employees, who operate the models, drive redesign of their workflows, secure data and convert automation into market power. These became the "super-human labor." It might be rewarded with high wages and stock-based incentives. But this does not show that labor overall has been winning. It demonstrates that the labor share can be fractured within labor itself. A handful becomes more capital-like. Others can experience weaker-than-average wage growth, declining access to entry-level roles categories and saturated fallback sectors.

The least hit sectors might then tend to fill up again. Sectors such as care, hospitality, cleaning, delivery, local service, maintenance and general public-facing work still require human interaction. If the volume of displaced workers in the office sector increases the number of workers in those sectors then the supply of labour will increase. Unless there is a corresponding increase in bargaining power, wages may ease. This is therefore how an affected sector may appear to be more American with high returns to capital, but is represented by staffing levels, while unaffected sectors appear more European with more labor continuity but fragile wage growth. The world is then not one labor market but a two-zone one.

Labor Share Policy Must Protect Workers Without Punishing Small Firms

The policy response cannot be nostalgia. It can't be a catch-all tax on technology or asking every company to hold onto every job. AI adoption is taking off now. OECD stats suggest that the use of AI in firms more than doubled among reporting nations, from 2023 to 2025. U.S. Census data from late 2025 to early 2026 suggest that use of AI has remained close to one-fifth of firms, with much higher use among larger firms. McKinsey's global survey shows that 78 percent of respondents' organizations used AI in one or more business functions in 2024. The question isn't whether AI reaches the workplace. The question is who wins.

A stronger policy frame begins with bargaining coverage, not just unionization. Europe's most powerful insight is that worker representation can function outside firm-to-firm conflict. Sectoral bargaining, minimum wage levels, industry training funds and social dialogue can prevent competition from killing small firms that strangle their workers the hardest. The United States should not replicate Europe by copying it too simply. Yet here is the lesson. Labor share protections are most effective when they establish affordable "just" floors within a particular sector, so that decent employers are no longer disincentivized from doing the right thing. This is critically important for small businesses with narrow profit margins.

AI policy needs to distinguish productive adoption and labor substitution. Pro-AI policy must be linked not only to worker retraining and job redesign but also to profit sharing and transparent accounting of effects on employment. No tax system should treat machines as better than workers. If software, datacentres and automation are treated as better than worker retraining and labor investment, then policy is secretly discouraging firms from co-investment with workers. The test is straightforward. When public policy is reducing AI costs, it should be improving the worker share.

The most probable criticism is that tougher labor regulations will inhibit innovation. This is a relevant danger if the regulation is overbroad. But lax labor regulation has its own disadvantages. It can give rise to low-trust firms and workplaces, weaker demand, raising political fury and forcing the firms to maximize margins and not productivity. The goal is not to hold back the economy. It is to make innovation earn its licence. This means portable training accounts, sectoral wage boards with little bargaining power, profit-sharing schemes for firms using AI subsidies, new, stringent merger screening for markets high in data and public procurement standards that prefer AI that enhances human skills.

The debate about the labor share was always about who gets paid. In an AI-shaped economy, it is about who still belongs. Society may be able to stomach billionaire founders, rising profits and new machines. It cannot, however, stomach a growth model within which workers are called upon to applaud output that further depresses their bargaining power. Europe should not hide behind outmoded institutions and America should not hide behind the marketplace. Both require a new bargain for AI: support for SMEs, enhanced worker voice, a fair capital tax and productivity gains visible in wages, security and mobility. Ignoring the labour share will not make the machine work better; it will only render the next divide more ungovernable, harder to finance and harder to defend.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bergholt, D., Furlanetto, F., Maffei-Faccioli, N. and Pappa, E. (2026) ‘The transatlantic divide in labour’s share of income’, VoxEU, 30 May.

Bergholt, D., Furlanetto, F., Maffei-Faccioli, N. and Pappa, E. (2026) ‘Understanding the transatlantic divide in labor income shares’, CEPR Discussion Paper, No. DP21436.

Cazzaniga, M., Jaumotte, F., Li, L., Melina, G., Panton, A.J., Pizzinelli, C., Rockall, E.J. and Tavares, M.M. (2024) ‘Gen-AI: Artificial intelligence and the future of work’, IMF Staff Discussion Note, SDN/2024/001.

Eurofound (2025) ‘Collective bargaining’. Dublin: European Foundation for the Improvement of Living and Working Conditions.

International Labour Organization (2025) ‘Policy measures to address inequalities and increase the labour income share’, G20 Technical Paper No. 2. Geneva: ILO.

Lane, M. (2024) ‘Who will be the workers most affected by AI? A closer look at the impact of AI on women, low-skilled workers and other groups’, OECD Artificial Intelligence Papers, No. 26. Paris: OECD Publishing.

Ma, J. (2026) ‘The record gap between corporate profits and worker pay has an “undercurrent of betrayal,” top economist warns’, Fortune, 23 February.

Minniti, A., Prettner, K., Venturini, F. and Bloom, D.E. (2026) ‘AI and the distribution of income between capital and labour’, VoxEU, 3 March.

Minniti, A., Prettner, K. and Venturini, F. (2025) ‘AI innovation and the labor share in European regions’, European Economic Review, 177, 105043.

Organisation for Economic Co-operation and Development (2025) The Adoption of Artificial Intelligence in Firms. Paris: OECD Publishing.

Organisation for Economic Co-operation and Development (2025) Membership of Unions and Employers’ Organisations, and Bargaining Coverage. Paris: OECD Publishing.

Schulze Brock, P., Katsinis, A., Lagüera González, J., Di Bella, L., Odenthal, L., Hell, M., Lozar, B. and Secades Casino, B. (2025) Annual Report on European SMEs 2024/2025: SME Performance Review. Luxembourg: Publications Office of the European Union.

Singla, A., Sukharevsky, A., Yee, L., Chui, M. and Hall, B. (2025) ‘The state of AI: How organizations are rewiring to capture value’, McKinsey & Company, 12 March.

United States Bureau of Labor Statistics (2026) ‘Union membership rate 10.0 percent in 2025’, TED: The Economics Daily, 24 April.

United States Census Bureau (2026) ‘AI use at U.S. businesses’, America Counts, 26 May.

United States Small Business Administration Office of Advocacy (2024) 2024 Small Business Profile: United States. Washington, DC: SBA Office of Advocacy.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.