Exchange Rate Communication Is Not Cheap Talk Everywhere

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

ECB communication moves markets mainly through interest rates, not exchange-rate remarks Asia shows that currency words matter more when intervention is credible The ECB case is important, but not universal

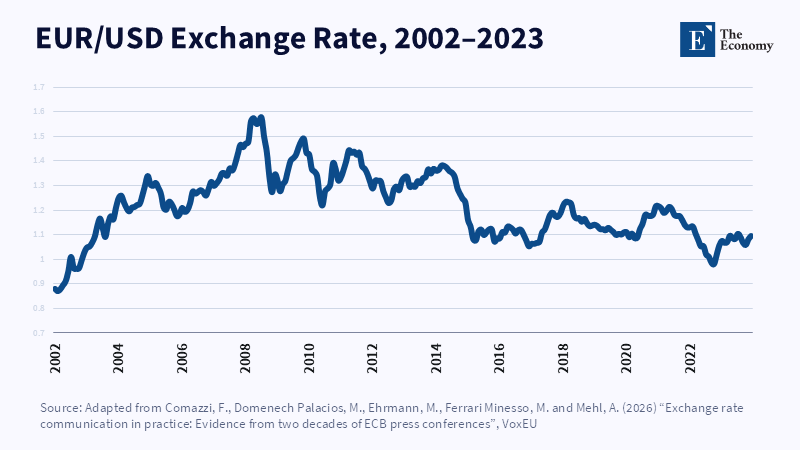

Between the end of April 2026 and the end of May 2026, Japan spent 11.7 trillion (about $73.5 billion) to defend the Yen. Only a month later, the yen had sunk to 162.66 per dollar, its lowest level since 1986. That may sound like clear evidence that official action can't beat the market. Traders did not ignore Tokyo's warnings the cold shoulder. They monitored every official note , analyzed the likelihood of a fresh intervention, reduced or hedged short positions and kept a wary eye on the tight trading intervals in which authorities might leap in again. That is the central question in the debate about exchange rate communication. A policy signal can be effective even if it does not steer a long-term trend. A study of European Central Bank press conferences shows that interest rate announcements have a greater impact on the euro than do comments about the exchange rate. The result is statistically significant in ECB data, but should by no means be assumed to hold everywhere. Exchange rate communication depends on the regime underlying the words and those regimes vary widely in Europe and Asia.

Exchange Rate Communication Depends on the Regime

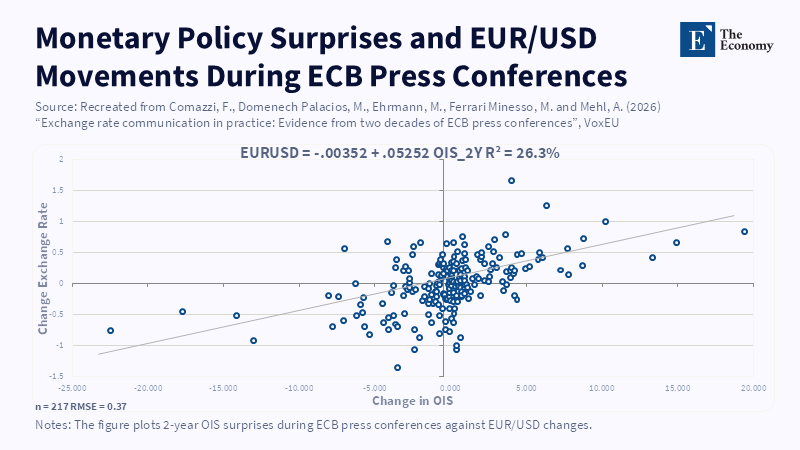

A recent research paper by Fabio Comazzi, Mar Domenech Palacios, Michael Ehrmann, Massimo Ferrari Minesso and Arnaud Mehl looks at European Central Bank press conferences (2002 to June 2023). It finds almost 100 exchange rate comments in opening statements and hundreds more during journalists' questions. Using high-frequency data and language analysis, it separates exchange rate comments from monetary policy surprises. And its primary finding is straightforward. It finds that a surprisingly significant share of euro movements on ECB press conference days, 16%, comes from monetary policy and ECB information shocks, with very little contribution from exchange rate comments. When exchange rate comments do move the euro, the response is small and generally temporary, declining by nearly half in the course of a week. The effect was also weaker after interest rates hit their zero lower bound. This is rigorous work that makes an important conclusion: the ECB's exchange rate guidance is, on its own, not an effective exchange rate policy.

The hedge is the leap from a good result to a broad claim. This one tests a single central bank, a single currency area, a single communications context and a single primary event. The research applies narrowly to words delivered in scheduled press conferences at the ECB. Does not check if the finance ministry is capable of asking for direct intervention in half an hour. It does not check a central bank reliably announcing a daily reference rate. It does not test a state capable of availing itself of public banks, pension funds, reserve sales, capital-flow restrictions, in combination with public announcements. It also does not check all possible market responses. A memo that fails to budge a spot rate for a week may profoundly shift costs of putting on a one-year out-of-the-money radio option, intraday cash, interbank carry-indebtedness, cross-market spread opportunities, or the price of betting short. The proper inference is limited. Pure exchange rate communication has scant durability when markets do not see a consensus explanation in the near future.

Why the Euro Makes Exchange Rate Communication Look Weak

The euro is not stable because Europe has a rigid and completely underused debt rule. The membership protocol does have 60 percent debt limits and a 3 percent deficit limit. However, the euro area public debt was about 87 percent of GDP in 2024. Greece was over 150 percent, Italy over 135 percent and France over 110 percent. These historical numbers do not support the hypothesis that a hard debt ceiling is all the currency needs. Several larger countries are well over the ideal benchmark, but this has not resulted in a long-standing euro crisis. On the contrary, the rules do matter, for they give shape to expectations and prompt debate over adjustment. They are part of the logic. They are not amorphous shields and are often shrugged off, delayed, or revised. The euro's structure works better. It is issued for a huge economic zone, traded in deep markets and remains the world's second main reserve currency. Its share of global reserves rose towards 20 percent in 2024. Nearly all euro-area government debt is issued in euros, which limits the direct balance sheet damage from sliding against the dollar. The ECB also has a clear price stability mandate. Exchange rate policy is embedded within layers of law and politics and direct intervention happens infrequently. The Eurosystem can intervene; however, markets do not normally take a comment at a press conference as a sign that a bout of big euro buying or selling is imminent. This tenuous link between words and an explicit tool makes many utterances seem more like description than promise.

Interest rate communication is different; the ECB is talking about the side of the balance sheet it has ultimate control over. A shock to the policy rate affects the cost of borrowing, bond yields, bank funding and decision-making and the portfolio choices of investors, as well as long-run expectations in an enormous market. The exchange rate then moves in that context. In contrast, a comment that the euro is unattractive or being watched is not necessarily associated with a novel response function: traders are unsure what the likely response might be, which institution and what magnitude. The ECB answer shows as much about institutional disposition as it does about the markets. Markets respond to words when words reflect a likely move in policy,so they move, save, or ignore the words.

Asia Shows What Credible Intervention Risk Looks Like

Japan provides the best example of the counterexample, but once again, it must be correctly characterized. The Foreign Exchange was under the direction of the Ministry of Finance, but the Bank of Japan acted as agent. The separation was not permitted to limit the market impact. It provided official comments in a well-known operational way. In April and May 2026, Japan spent ¥11.7349 trillion to support the yen, roughly US$73.7 billion. The impact subsequently eroded and the yen slumped to a 40-year low in June. However, the prospect of renewed intervention affected trades. Three topics loaded into the potential for an intervention: risk, potential time-scale of a future move and the risk of a sudden loss on short-yen bets. Not the ability to control the interest rate differential with the US was the issue. A policy risk was created that investors had to price. Long-term control is not the same as market power.

South Korea has a comparable story. In the first three months of 2025, it sold $2.96 billion, in the second $800 million and in the third $1.745 billion. Admittedly, these figures alone total around $5.5 billion, just over the first three quarters, according to the reported quarterly balance of payments figures. Nonetheless, the won weakened 3.7 percent against the dollar in the third quarter. Again, the intervention did little to change the trend. But official communication on exchange rates had weight because it could be quite immediately followed by dollar sales, liquidity indicators, pension-fund hedging, or adjustments in market regulations. An agreement with the United States from 2025 provided that intervention was to be used solely for addressing marked instability and disorderly price movements rather than trade gains and called for more transparent reporting. That very agreement shows the point: both traders and policymakers regard intervention as a simple tool of policy in Korea.

The biggest gulf from the ECB architecture is China. The IMF has described China's de facto exchange rate system as a crawl-like framework. China should be defined as under the official and managed renminbi/USD exchange rate. The authorities managed it with a time-fixed grid, a more comprehensive system of macro-prudential measures, market interventions and a raft of other financial restrictions. In January 2026, the US Treasury designated China, Japan and Korea on its surveillance list, as well as seven other economies. It did not report a single major partner as a currency manipulator during the review. China was already officially designated in August 2019, but that label is a rare and legally distinct from monitoring. This is an important distinction. The strongest and fairest case is that the United States' perception of each country's manipulation dynamics as a potential process has been persistent and legitimized, because policy was forthcoming, discernible and robustly material.

The Asian evidence also throws a monkey wrench into a simple narrative of export subsidies. Japan and Korea have recently sold foreign currency to defend their currencies, not to devalue them. Their expressed worries encompass imported inflation, disorderly movements and financial stability. A weakening yen or won benefits exporters, adds energy and food costs and squeezes household purchasing power. China's regime presents different questions because it intervenes more tightly in the exchange rate and because its policy process is more opaque. The two should be kept separate and not combined into one story. What they have in common is not a single plan to cheapen exports. It has a greater ability to affect the currency market with instruments other than the policy rate. This larger ability affects how investors interpret official words.

A Better Test for Exchange Rate Communication

A natural disaggregation for those who wish to compare exchange rate communication is by the transmission mechanism. The first group is pure commentary - no actions are clearly associated with it. The second group consists of conditional guidance on monetary policy with a currency effect through anticipated interest rates. The third group has direct intervention guidance with reserve vehicles and a track record. The latter two are linked to institutions as capital rules, the prestige of fixing strategies, or held-back adjustments. The study of the ECB provides strong evidence on the first two groups for the euro area. Japan, Korea and China are partly represented in the third and fourth groups. Covering these four groups with one blanket or in combination would obscure what is causing different reactions in the market and it would muddy currency guidance that uses an instrument versus one that simply describes current realities.

Beyond measuring the direction of the spot, the potential of a warning to matter also involves the other ways a warning can matter:price volatility, trading volume, bid-ask spreads, option and forward markets, closing leveraged positions, etc. It can work only under certain conditions. When speculative positions are crowded and reserves are abundant, when markets are thin and when a credible statement in a recent official act makes the threat credible, intervention risk is high. When policy is designed to combat a large monetary interest rate cycle or a large dollar cycle, intervention risk is weak. These conditions show why exchange rate communication can bring a sudden intraday move but then not change the monthly trend: for banks and firms with open positions, even a momentary move can mean large losses or margin calls, which produce analogous pressures.

The message for policymakers is that there should be no more talk. The policy message has to be made clear. ECB should continue to communicate how the euro influences inflation and growth, without any insinuations that it is targeting a specific exchange rate. Japan and Korea should make timely intervention data available and clarify whether the intervention is intended to combat disorderly market conditions, inflation, or financial stress. China should give more transparency to the fixing process, reserve market operations and the role of state institutions. US Treasury should lean on the line concerning a monitoring list and the submission of a manipulation case. Vague labels attract media attention but diminish analytical usefulness. Transparency, on the other hand, would help firms distinguish between explicit political risks and "routine" political pressures.

The 11.7 trillion, or $73.5 billion, Japan spent failed to lift the yen. It did something narrower but still useful: It provided proof that the official currency action was in place, costly and replicable. That evidence altered the risk investors faced even after the currency was falling again. Thus, the ECB illustration should be viewed as a lesson about the institutional environment, not a general judgment on all central banks. Interest rate dialogue wins when it is the most plausible means available. Exchange rate discussion has a greater impact when relevant reserves, fixings, public funds, or direct involvement are openly communicated. Banks of the future must consider not just what words moved money but what equipment supported those words. Absent the latter, a euro result will continue to be mistaken for a global rule.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Brettell, K. and John, A. (2026) ‘Yen stumbles to 40-year low as clock ticks on intervention’, Reuters, 30 June.

Comazzi, F., Domenech Palacios, M., Ehrmann, M., Ferrari Minesso, M. and Mehl, A. (2026) ‘Exchange rate communication in practice: Evidence from two decades of ECB press conferences’, VoxEU, 30 June.

Comazzi, F., Domenech Palacios, M., Ehrmann, M., Ferrari Minesso, M. and Mehl, A. (2026) ‘ECB exchange rate communication’, CEPR Discussion Paper, No. 21606. London: Centre for Economic Policy Research.

European Central Bank (2025) The International Role of the Euro. Frankfurt am Main: European Central Bank.

Eurostat (2025) ‘Government debt at 87.4% of GDP in euro area’, Euro Indicators, 22 April.

International Monetary Fund (2026) People’s Republic of China: 2025 Article IV Consultation—Staff Report. Washington, DC: International Monetary Fund.

Kim, C. (2025) ‘Bank of Korea sold a net $1.745 billion for FX intervention in Q3’, Reuters, 31 December.

Lee, J. (2025) ‘US, South Korea agree not to target FX rates for trade advantage’, Reuters, 1 October.

Ministry of Finance Japan (2026) Foreign Exchange Intervention Operations. Tokyo: Ministry of Finance.

Nelson, R.M. (2025) Exchange Rates and Currency Manipulation. CRS In Focus IF10049. Washington, DC: Congressional Research Service.

United States Department of the Treasury (2019) ‘Treasury designates China as a currency manipulator’, 5 August.

United States Department of the Treasury (2026) Macroeconomic and Foreign Exchange Policies of Major Trading Partners of the United States. Washington, DC: United States Department of the Treasury.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.