Education Consulting After the Prestige Premium

Authored on

Modified

Consulting in education is shifting from prestige to practical results AI is weakening big-firm scale and strengthening focused expert teams Institutions should buy execution, not brand cover

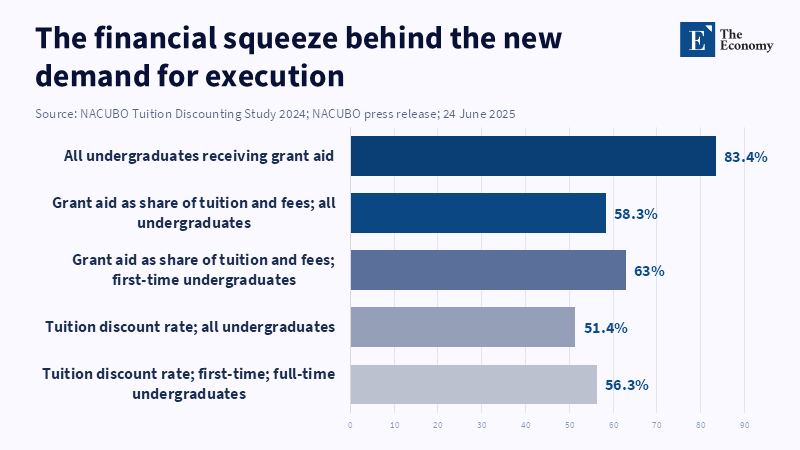

The most visible sign in education consulting, however, is neither high-profile platform launches nor slick strategy books. It is a margin fight. Going into the 2024–25 academic year, the private nonprofit 4-year college's first-time, full-time undergrad tuition discount rate was 56.3%. At the same time, the US is forecast to reach peak numbers of high school graduates in 2025, after which the pipeline is projected to decline for years. That silvercomb forces a rethinking of the sector's buying logic. When institutions are enrolling students and paying well above the sticker price for them, and future demand remains uncertain, education consulting stops feeling like a luxury purchase and turns into an operational decision. The old-world belief that a leading advisor brand signifies results continues to carry weight in the boardroom. However, it is losing strength in CIOs' budgets. Today, what matters is whether education consulting can eliminate inefficiencies, enhance conversion, deflect AI, related risks, accelerate workflow, and transfer skills back into the institution. In an AI era, any advice that does not embed itself into operations becomes an unaffordable luxury.

Why is education consulting moving from brands to delivery?

That's the real story of the change in framing. The problem is not that the supply of education advice has to try to compete in a value vacuum, nor that institutions have once again fled to the experts, but that the supply of generic counsel has to gain some new value metric. Higher education remains economically fragile but not in the same way: a 2025 NACUBO survey indicates that the No. 1 concern among financial chiefs today is that of the local unpredictable funding stream; overall higher education enrollment is riding a little higher but there is startling variation under the hood—community colleges and public four,year undergraduates were higher, but private non,profit four,year undergraduates were lower, and graduate school enrollment a little slower. That's exactly the kind of market that makes for a buyer's market: they end up spending less on comfort and more on verification. They want faster turnarounds, shorter-term assessments, clearer scope of work, and obvious benefits for operations.

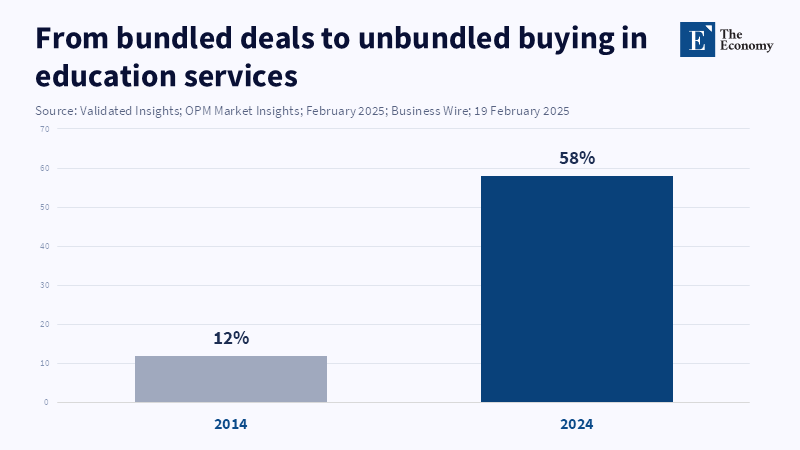

Evidence for this is not in marketing. It is in other parallel markets for educational services in which customers are already changing how they buy. Large, comprehensive, long,term, multi,year arrangements in the OPM market have begun yieldingsignaling a trend to fee, for, service work bought on a smaller scale. According to Validated Insights, the number of new OPM contracts fell by 42.1 percent in 2024, and 58 percent of new OPM contracts are now fee, for, service instead of revenue share. Institutions are unbundling. Rather than awarding a provider the entire, end,to,end service stack, they are designing their recruitment, marketing, market research, and program development inputs separately. The same lay strategy is occurring in education consulting. The winning firm is less likely to be the one that has the largest analyst pyramid and most prestige, and more likely to be the one that can fix advising systems, procurement models, AI governance, and student recruiting ROI without putting the client into a straitjacket,exhausting multi-year slumber.

That matters because advisory brands have never been purchased just on competence. They have been purchased for political cover: boards, presidents, and provosts used large companies to demonstrate a seriousness, take the fall, or support an already made decision. That continues, but now confronts more difficult economics. When the discount rates are everything, staffing lines are being cut, and the demographic outlook is dimming, having that brand alone no longer is a good enough reason to pay for a weak operational plan;education consulting no longer has the luxury to be a smart optional course. It's facing the same challenge all school software vendors are: what exactly changes on Monday morning,and after the deal, and how much savings are going to come out of this system?

In AI, the education consulting market requires a deeper and narrower skill set

This makes the transition even more painful, because AI depends on devaluing the middle way in which consulting is produced. Consulting firms once had a competitive edge where they could deploy stick and carrot junior labor for research, benchmarking, slide wrangling, and project execution; generative and agentic AI speed some of that up, and are about to change the rest (though that does not mean these skills, judgment, or change management no longer matter). But rigid analysis will be less rare, as a McKinsey projection estimated: 92% of organizations will accelerate AI investment in the next three years, but only 1% will have a "fully mature" deployment; PwC transpired: by looking at bots and gig data, skillsets are growing fatter, and those with AI skills earn distinctly more. Schools are simply becoming candidates for a market in which high-end labor is more costly, and low-end labor is more fungible. It is a hard place for kilogram,billing outfits, and tougher for kilogroup businesses with intimacy in smaller, richer teams.

Higher education is no longer seeking permission, however. In the 2025 HEPI/ Kortext student survey of 5,187 respondents, 92% of full-time students had worked with some kind of AI in the past year, and 88% had used generative AI for assignments. But there was almost no institutional help: just 36% said their institution helped them develop AI skills, and only one in 13 had no policy on the subject. This is a new opportunity for the education sector consulting. It doesn't need another raft of speeches on how AI will transform education. It needs education consultancy that can integrate policy into learning workplaces, upskill trainers, renegotiate assessment, create ways to benefit from risk, tackle vendor negotiations, and establish differences between gains and issues of privacy, security, and legal compliance. The successful consulting firms will be able to move across the campus educational structure—covering pedagogy, campus IT, privacy requirements, procurement, student experience, and financial assumptions—in one group of actions.

This is where the old doctrine that bigger equals better begins to break down. Not all incumbent management consultancies will lose out, but they will have to narrow their scope to a handful of scenarios where they can scale, for instance, huge ERP conversions, cyber security, or regulation compliance, data security, or trans, national planning where agencies and insurance are involved. The point is not that specialist boutique consultancies will always win but that AII makes the economy of scale shortcut, which implies staff size will be less distinctive than insights. Many large firms are fragmented powerhouses, with large staffs in niche areas. Some boutique outfits will compete on the other axis: a handful of expert hands who work from oversight, process, tech, and implementation step by step, flexibly. Someone who knows registrar workflows, financial aid planning, student messaging, faculty oversight, and AI policy can now produce outcomes that once needed a full brigade. This 'superhuman staff' may be short-lived; it will be the outcome of pairing experienced operators with smart, cheap AI.

Hierarchy of negotiating power in higher education

The implications reach beyond consulting into higher ed pricing in general. Because their markets are shrinking, even their most expensive clients are getting more discriminating. WICHE projects that the number of high school graduates will decrease 13% from a 2025 peak to a 2041 trough. (That doesn't mean every individual school will shrink at the same rate, but it does mean expensive colleges will have a continuing war of attrition with one another over fee income, place attractiveness, and market bandwidth.) Against those forces, outside consultants are no longer priced against peer firms but against employing and training a great internal expert, sharing services with other schools, working with consortial groups, or using artificial intelligence to power internal research and projections that can do quadrillions of calculations a moment, much faster than humans can.

Thus, operational consulting is taking precedence over elevated concept strategy. The most innovative schools will not need deep diagnostics of demographic shifts, digital disruption, and student expectation changes. They already have those. What they are seeking is algorithms and best practices to optimize schedule construction, advising bandwidth, buying habits, attribution modeling, not on website marketing, transfer incentives, financial aid models, and faculty workflows. Deloitte summed up this move in its 2025 higher ed trends report by its insistence on "systemness," shared capabilities, and operating systems. EDUCAUSE's latest survey found similar issues on the technology side: while many more colleges have opened their students' access to AI tools, only a handful fully trust their privacy, security, and data governance policies, and very few think those policies are sufficient for the theoretical risk. They are turning to the handful of auditors empowered to translate those technology spends into operational redesign and risk reduction, not just articulate an "AI vision."

A challenge may be that we've always had to do consulting with some guidance, so none of this will be earth-shattering. The real difference is the speed at which this market is developing. AI is not just another product; it is already revealing the very extent to which the calculus of consulting profits is rooted in information distortions and deck circles, and that, driven by constrained demand and squeezed budgets, these clients are less likely to pay for it and more likely to ask awkward questions in the RFP. How does this product team interact with our existing enterprise software suite? How will workflows and people be left behind? Who owns the data? What measures of attainment will change in a quarter, or a single admission cycle? Just as with students and faculty, these institutional clients will soon need less blank paper and more product first before they will pay. If the big consulting accounts want to monopolize on this long term, they will have to be more realistic about scope (or scope better).

How will faculties buy education consulting in the coming new era

How to use this as a starting point? Don't hop, skitter, or skip aimlessly from very large consulting brands to boutique shops to highly specialized consulting firms. Instead, base your decisions on consulting goods or services around the types of decisions you make for your students. How about grouping decisions into modules based on bottlenecks? I'm sure administrators would have time to investigate their survey of tertiary education offerings and compare bottleneck to bottleneck their estimates for how much you and many others can buy back access or B2. If you twist this: Can this particular expert interrogator unpack my decision needs for this one specific academic product or process, and can he show how AI both decreases and inflates that process, then I can choose whether to buy or not? Do I want my bundle to actually reduce something I care about, or just to come up with a chunk more of it? And, how soon will I be able to see the change? Let me compare that against my preferences for certain scopes, like short, shorter, smaller, and simpler. When a college is able to see if its consultant can make a very narrowly focused decision, then the college can begin to lean less on that aspirational name and more on a consultant who is hungry to be a little less and a little less necessary.

While these dynamics are certainly true for hard definitions, they are equally applicable to soft ones. For educators, consulting is going to be a much more ingrained part of the assessment strategy, syllabus development, academic integrity policy, student advising, and learner endorsement systems. Which means you will need to designate faculty and support staff as critical, and actively include them in the outreach rather than just list them after the provider nets the official education contract. Because if they are not involved until after the contract is announced, it sure is going to hurt their contribution to the learning enhancement effort. Instead, savvy operators will use the consulting relationship to bring policy into practice: the point where AI has gone far enough, the point where the learning objectives finally get achieved, the point where training comes in, the point where visions must be clarified, the point where discretion must be exercised. There is nothing anti about consulting about that. There is an anti-abstract about it.

Finally, and perhaps more critically, policymakers will increasingly need to buy or evaluate work from consulting services in AI implementation. Smaller, lower-funded schools might fall victim to a further digital divide if they are unable to either buy skilled AI services or evaluate their quality. According to UNESCO, many non-OECD schools are devising AI policies—but not enough, and institutional and policy capacity remains. We thus need a policy that somewhat diminishes the language for AI: incentives for developing common contractual templates, tools blocking over,expensive procurement; support for schools unable to re,learn present internal knowledge, and well-resourced research consortia. The field does not need more money for PowerPoint—she needs a policy that reduces the price of securing good implementation services.

And yet in spite of this most warning statistic, should anyone conclude that schools should stop buying education consulting for having it as a goal? When a school must discount 56.3% of a US private college's tuition, that's a huge chunk of money for every outside contract to make a statement about its conviction that this new system will really work. Education consulting will thrive in this environment, and even expand, but its economics will change. The winners won't be the firms with the biggest signs and the biggest faces. The winners will be the ones best at translating knowledge into improved staffing choices, furniture specifications, governance structures, more decisive governance, more efficient decision cycles, and operational cost reductions. In the longer term, they won't kill the consulting industry in education; they'll just punish the irrelevant scale and reward being able to convert specialized administration knowledge into high-impact consulting that achieves the efficiency of artificial intelligence. Those willing to buy the name first will pay for yesterday. Those who buy execution now will be ready for tomorrow.

References

Clark, C., Cluver, M., Fishman, T. and Kunkel, D. (2025) 2025 Higher Education Trends: A Look at the Challenges and Opportunities Shaping America’s Higher Education Sector. Deloitte Center for Government Insights.

Freeman, J. (2025) Student Generative AI Survey 2025. Policy Note 61. Higher Education Policy Institute and Kortext.

Grajek, S., Pelletier, K. and Freeman, A. (2025) ‘AI procurement in higher education: Benefits and risks of emerging tools’, EDUCAUSE Review, 11 March.

Lane, P., Falkenstern, C. and Bransberger, P. (2024) Knocking at the College Door: Projections of High School Graduates. Western Interstate Commission for Higher Education.

Mayer, H., Yee, L., Chui, M. and Roberts, R. (2025) Superagency in the Workplace: Empowering People to Unlock AI’s Full Potential. McKinsey & Company.

Millerd, P. (2024) ‘The cliches of consulting vs the reality’, StrategyU, 11 March.

National Association of College and University Business Officers (2025) NACUBO Study Finds Private Colleges and Universities Are Offering Record Financial Aid to Students. 24 June.

Pierce Washington (n.d.) ‘Big consulting vs boutique—Which is best for you?’, Pierce Washington Blog.

PwC (2025) The Fearless Future: PwC’s 2025 Global AI Jobs Barometer. PwC.

Validated Insights (2025) OPM Market Insights: February 2025 Edition. Validated Insights.

Similar Post