The Tariff Stagflation Trap Is Now a Policy Choice

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Tariffs can create inflation and weaker growth at the same time Modern supply chains turn border taxes into domestic cost shocks Tariff stagflation makes rate cuts risky and policy credibility essential

A tariff rate that was last seen in the era of early mass production should not be mistaken for modern growth policy. In 2025, American tariffs reached the average effective tariff rate levels of 1909 and the old protectionist deal did not work once and for all. We were told the following: raise tariffs on imports, increase domestic production and make the bank keep interest rates lower. Instead, we had tariff stagflation. Imported products got more expensive at the cash register. Imported inputs got more expensive inside the factory. Metals, machinery, chemicals, parts and components fuelled domestic production costs. Hence, the shock has been so devastating: it has not only increased prices on foreign products, but it has also increased costs domestically and depressed output. A tariff wall cannot simultaneously lower prices of other goods and raise output and justify lower interest rates.

Tariff stagflation begins before retaliation

The old justification for tariffs is based on a simple tale. Higher import prices mean higher domestic demand. Higher domestic demand means higher total production. Higher production means more factory employment. More employment means higher wages. Higher wages lead to a reduction in the trade deficit. This is not an entirely false story, but it is woefully inadequate for the economy we now have. Contemporary firms are not just competing with imported goods; they also rely on global production and finance networks. An automobile factory may be entirely home-based, but the electronics, steel grade input, tooling, sensors, or machine elements it uses must cross borders hours and hours before being finally assembled into the end product. A tariff, in the above scenario, does not just impose a tax on the foreign competitor--it imposes a tax on the domestic producer who uses foreign input. This is precisely why tariff-induced stagflation begins even when trading partners do nothing in kind.

Certainly, this price-shock, the 2025 tariff shock, demonstrated that effect with remarkable force. The first round of estimates suggested that, in the wake of the April package, the average effective tariff rate reached some 22.5%, that is, the weighted average tariff rate paid by consumers and by firms on their inputs, since 1909. Subsequent estimates, this time after the various product-specific exemptions, the tariff pauses, the legal changes and the changes in demand and consumption choices, confirmed. The tax was sizeable, in the mid-teens of its effective rate. Yet these numbers, useful as a lesson in tariff policy, are more a macroeconomic story. A tariff of this size is not just a trade policy tool. It becomes a price level shock. It directs households to cut back on mid-priced purchases or to buy lower-priced options. It guides firms to suffer higher costs, to operate at lower margins, to postpone their investments and to have a more cautious approach to hiring.

This is the key lesson from the policy perspective. Tariff stagflation does not need a trade war. Retaliation can make it more severe, but the first shock originates with the domestic firm. When imported input prices increase, you face a choice whether to raise prices and squeeze margins, or lower prices and shrink output, or delay your plans. If your imported final goods increase in price, then your household experiences a loss of real income. Both channels depress demand, but in two different ways: one through the shopping basket, the other through the factory floor. And both together undermine the simple presumption that tariffs are simply a transition from foreign to domestic supply.

This is also the reason that the political promise of tariffs is so deceptive. A tariff appears simple because it appears at the border and does not appear as a sales tax in a check-out receipt. But the border is only an accounting point. The real tax comes in higher prices, fewer product choices, lower firm profits and less investment. If the shock is large, the economy cannot re-allocate resources by patriotic substitution – it takes too long for all those complex suppliers to replace complex suppliers. It takes too long for those families to replace a pair of shoes just auctioned in the market with new money to change an equivalence label on the shoebox. Tariff stagflation occurs where the political promise is kept only in the structure of the economy.

How tariff stagflation undoes the rate cut promise

The most dangerous element of the 2025 experiment was not simply the rise in tariffs but the clash between stagflation risk and Fed policy. It was the conjunction of that tariff hike with the push for lower interest rates. That conjunction is the policy paradox at the core of tariff stagflation. The function of tariffs is to raise prices. They do this deliberately. By making imports more costly, they introduce inflation. If, on the same policy platform, you then simultaneously demand cheaper loanable funds, you are effectively asking monetary policy to offset the inflation you are bringing into being. That is not coordination. That is conflict.

This spells the worst combination on the Phillips Curve for a central bank. A demand-led slowdown would leave policymakers more scope to act. Lower growth, easing inflation and rate cuts can all support activity. A pure supply shock is more difficult, but it might fade as long as expectations remain anchored. Tariff stagflation is worse still, since it has both ingredients. It raises costs just like a supply shock, but then destroys actual spending capacity just like a demand shock. The economy is left with weaker activity and higher inflation at the same time. In that climate, a rate cut might prop up asset prices temporarily, but it may also underpin higher inflation expectations and erode faith in the currency.

Market concern in 2025 was consequently credible, as three macro scenarios showed how tariff-driven stagflation could hit both bonds and equities. In the scenario analysis, stagflation proved to be more damaging than a normal recession, as not only could bonds lose their safe-haven status, but even equities would decline. One of the adverse scenario had U.S. equities plummet by no less than 35%, from pre-announcement values, with inflation proceeds to creep up as growth stalls. This could not have been an implemented prediction. It was a stress test of the policy mix. The point was in the conclusion: tariffs keep pushing prices up and monetary easing can no longer be presented as harmless help. It is an attempt to fix a supply-cost problem due to demand growth.

The logic is identical to trade policy. A government can point to tariffs as a source of revenue but the same tariffs can slow growth and reduce other tax income. As well as with the argument of a falling dollar rebounding tariffs can revive fickle factories but at the same time cause input costs for those factories to rise. Also, with subsidized oil, lower interest rates can soften the blow, but then the easy money makes the inflation problem impossible to contain. Tariff stagflation is not a mistake. It is a package of unfocused trade policy, budgetary politics, and monetary policy.

Supply chains transform border tax into a domestic cost shock

The best evidence for tariff stagflation is the channel through which costs flow across supply chains. The border is only the first step. Once a taxed input is integrated into a domestic production network, the price is transmitted onward from one supplier to the next. A machine shop will pay more for metal and an automaker will pay more for the part. A retailer will pay more for the finished good. Some firms will bear the pain at the source, while other firms will push higher prices downstream. The passthrough is partial at first, but may gradually increase as old contracts lapse and inventories are rebuilt. This is why the inflationary impact may persist beyond the tariff headline.

By the end of 2025, real-time price analysis showed that tariff pass-through had already appeared in consumer prices. On average, tariffs had contributed about 0.5 percentage points to headline PCE annualized inflation during June through August 2025 and 0.4 to core PCE annualized inflation. Over the 12 months to August, tariffs accounted for over 10.9% of headline PCE inflation. These figures are not dramatic on their own. They are dramatic because they were a policy decision, not an oil embargo, not a war-damage shock and not a pandemic supply freeze. The tariff was voluntary.

Output estimates told a different story. By Nov. 2025, it was estimated that the tariff measures would reduce by around 0.5 percentage points the growth of the real U.S. GDP in 2025 and by around 0.4 percentage points in 2026. Output estimates told the other side of the story. By November 2025, tariff measures were estimated to cut real U.S. GDP growth by about 0.5 percentage points in 2025 and 0.4 percentage points in 2026. Payroll employment was also estimated to be hundreds of thousands lower by the end of 2025 than it would have been without the tariff shock. The long-run economy was expected to be smaller as well. That is tariff stagflation in practice: a price rise large enough to matter, paired with a growth loss large enough to show up in income and jobs.

The worldwide spillover is just as important because tarrif shocks also weaken national competitiveness. The big economies do not set broad tariffs in a global vacuum. They have big effects on exchange rates, trade volumes, profit margins and investment plans already abroad. European modelling found unilateral U.S. Tariffs could reduce U.S. GDP by about 0.6- 1.0%, some of that through subdued internal demand, falling exports and a rising REER. A broader multi-country model with over 60 economies and 16 sectors found broader output falls, particularly for the U.S. and its close trading partners, such as Canada and Mexico. This is a warning label for the global economy. Supply chains convert a national tariff into an international shock.

The exchange-rate channel complicates matters further. In a standard model, unilateral tariffs can appreciate the country doing them in part as they reduce imports and cause monetary policy to tighten against the inflationary impetus. But tariff uncertainty might undermine the case for currency appreciation. If investors start to incorporate into their expectations the policy risk, fiscal stresses and slowing growth, the value of the currency can behave erratically. That is significant because the exchange rate affects prices. A stronger dollar might offset some of the import reduction. A weaker or more volatile dollar adds to that effect. Tariff stagflation is perilous because the channels that affect the exchange rate change as potential futures shift in traders' expectations.

The sole way out of tariff stagflation is credibility

The first is that tariffs remain effective for strategic industries. This is true in isolated examples. No credible policy position would refute the assertion that some industries have strategic utility. Semiconductors, high-tech inputs, pharmaceuticals and energy can all tolerate precaution. However, a strategic tariff cannot equate to a tariff barrier encompassing all sectors. The former is selective, transitory and linked to capacity preparations. The latter is a blanket tax on domestic production and consumption. Should all sectors be recognized as a strategy, there is no concept of special cases, no delimitating principle.

The second counter: Tariff revenue can finance public priorities or compensate for tax reductions. That argument serves even less during stagflation. While tariffs can generate revenues, they do so indirectly by taxing households and businesses through prices. Such taxes tend to be regressive, as lower-income consumers tend to dedicate a larger share of their income to consumption. Tariff revenue also erodes as imports decline, supply chains shift direction and output crumbles. A tax that yields revenue while shrinking the tax base is no free lunch. It is a fiscal instrument with an inflation premium.

Administrators and policymakers must clarify more starkly the distinction between resilience, protection and macroeconomic stability. Resilience entails identifying robust essentials, in what areas supply shocks can occur and which internal capacities should be safeguarded. Protection involves erecting a Tariff barrier to obscure the lack of an industrial scheme. The former is quantifiable. The latter can be felt mainly after the harm manifests. A credible scheme would set tangible targets, review costs regularly and cut tariffs that do not work. It would also safeguard the independence of the central bank, since rate movements cannot address a cost shock that trade policy sustains.

The correct answer is not naive free trade. It is disciplined resilience. Governments should re-establish a firewall between security policy and politics; replace broad tariff shocks with focused investment, swifter permitting, calculated stockpiles, reliable-import-partner sourcing, and transparent sunset provisions. We should not ask central banks to new-deal growth from a trade-war inflation sphere authored by elected officials. Firms value concrete rules more than they value loud threats. Consumers value affordable prices more than they value the free-world global narrative. The line from the preceding figure still applies. A tariff-hike from the medieval global supply-chain frontier cannot sustain a modern-growth story. Tariff-frenzied stagnation is the consequence of an administration attempting to finance imports, bolster confidence, and inflate interest rates all at once. The solution has to begin with acknowledging you cannot do all three.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Dvorkin, M.A., Leibovici, F. and Santacreu, A.M. (2025) ‘How Tariffs Are Affecting Prices in 2025’, Federal Reserve Bank of St. Louis: On the Economy, 16 October.

European Commission, Directorate-General for Economic and Financial Affairs (2025) ‘The Macroeconomic Effect of US Tariff Hikes’, European Economic Forecast, Spring 2025.

Gourinchas, P.-O. (2025) ‘The Global Economy Enters a New Era’, IMF Blog, 22 April.

Kalemli-Özcan, Ş., Soylu, C. and Yıldırım, M.A. (2025) Global Networks, Monetary Policy and Trade. NBER Working Paper No. 33686.

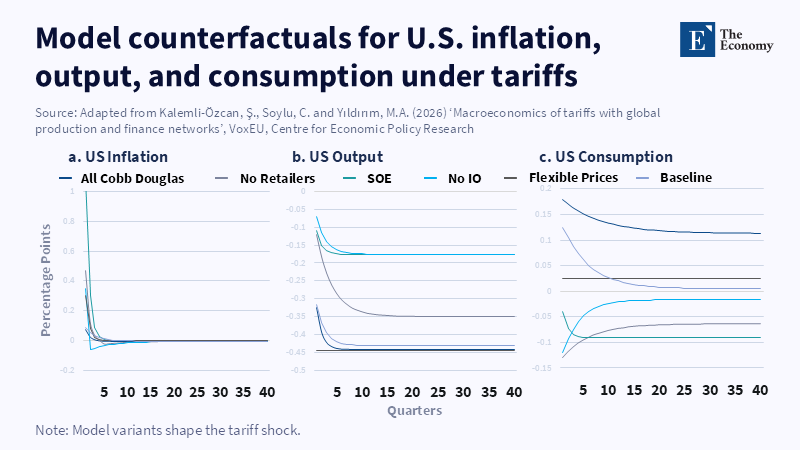

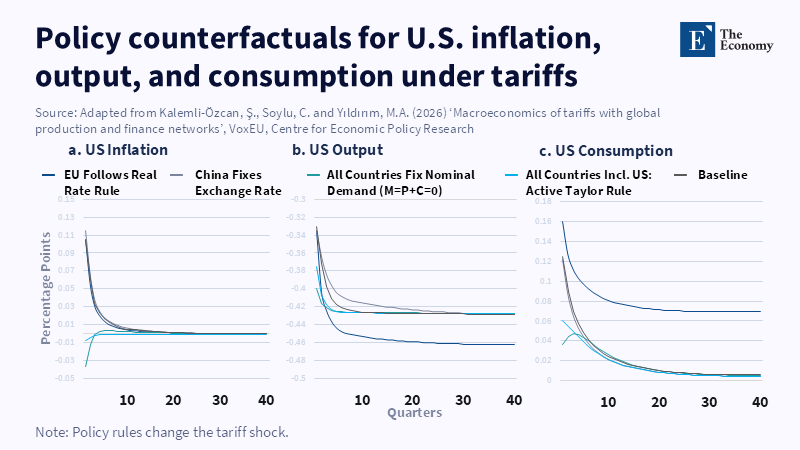

Kalemli-Özcan, Ş., Soylu, C. and Yıldırım, M.A. (2026) ‘Macroeconomics of Tariffs with Global Production and Finance Networks’, VoxEU, Centre for Economic Policy Research, 18 May.

Morris, D. (2025) ‘Tariff Escalation, Stagflation Risk and Fed Policy’, BNP Paribas Asset Management: Front of Mind, 16 October.

Minton, R. and Somale, M. (2025) ‘Detecting Tariff Effects on Consumer Prices in Real Time’, FEDS Notes, Board of Governors of the Federal Reserve System, 9 May.

Szikszai, M., Gupta, L., Verbraken, T. and Bookstaber, R. (2025) ‘Tariffs Raise the Specter of Stagflation: Three Macro Scenarios’, MSCI Research and Insights, 22 April.

The Budget Lab at Yale (2025) ‘State of U.S. Tariffs: November 17, 2025’, 17 November.

Zhao, H. (2025) Assessing the Macroeconomic Impacts of the 2025 US Tariffs. BIS Working Paper No. 1316, Bank for International Settlements.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.