Energy Inflation Is a System Risk, Not a Price Spike

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Energy inflation can turn a medium shock into a wider economic risk Oil and gas shocks spread fast because energy sits inside almost every price Policy must contain the pass-through early before inflation becomes self-reinforcing

A shock need not be huge to be dangerous. Euro area inflation hit 3.0% in April 2026; the more relevant indicator is the figure it contains: energy inflation was 10.8%, more than twice the March figure. This is the warning sign. Energy inflation does not normally linger within the fuel bill when it is sustained long enough. It passes through freight, food, chemicals, wages, credit and confidence. It also influences behavior within firms. A small shock can be tolerated. A medium shock can be managed. A large or persistent shock has the power to change the entire paradigm of pricing itself. The policy dilemma, then, is not whether the current Middle East shock just underway is once again translating itself into another 2022. It is whether Governments and central banks are moving quickly enough to prevent energy inflation from translating into one. The peril is not only that of oil prices. It is the point at which the entire economy begins to weigh as if oil will be permanently high.

Energy inflation is at this stage a regime test

The biggest policy error is to treat every energy shock as the same kind of event, just a matter of size. It is appealing to have one simple explanation for all shocks, but that is not what happens. Energy inflation looks more like a threshold problem. Consumers and producers hold back in response to some point and firms absorb more of the cost increases and households cut somewhere else. After some point, firms reprice more vigorously and consumers broaden the index of prices they expect to rise and the shock intensifies. It is not a smooth transfer from oil to consumer prices. It is a bend in the curve. When policy must respond, that bend is where to look. The issue is not whether the initial surge in energy prices was indeed temporary. The issue is whether the price rise had enough staying power to alter the culture of re-pricing.

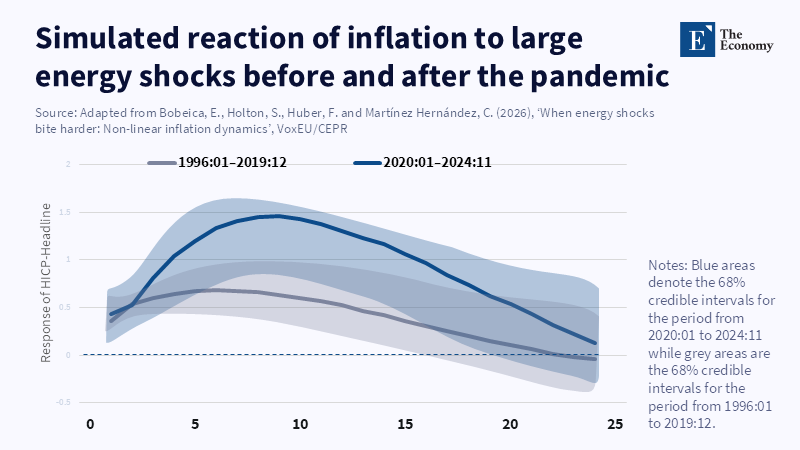

This is relevant today because the current shock occupies a precarious middle ground: not yet the full-blown energy frenzy that followed Russia's invasion of Ukraine, not a run-of-the-mill oil adjustment. Forecasts indicate that in 2026, energy prices will increase by 24%, with Brent Crude averaging 86 dollars per barrel, in contrast to 69 dollars in 2025. European gas prices are likely to experience a steep increase as well. The baseline presupposes a subsiding of the worst perturbation and the resumption of Gulf exports. That presumption might be accurate. However, it provides a shaky foundation for policy when inflation risks are titled upward and when energy inflation has once more penetrated the core of the value system. It may appear prudent to wait for certainty. By then, it may indeed be a more sedate way of avoiding the issue.

The growth side of the story complicates matters. The euro area faces no benign inflation shock in a thriving economy. Already, forecasts are for softer growth in 2026, partly as high energy prices depress incomes, confidence and capital spending. That combination generates the quintessential policy dilemma. Tighten too much and the demand weakens further. Tighten too little and energy inflation risks passing into wages and services. The solution is to jettison both urges. Policy should neither crush demand to combat imported oil nor shun the notion that imported oil cannot turn into domestic inflation. Rather, it should revolve around the pass-through avenues where the shock is made endogenous, in which the transience of the initial outlet may turn intractably inflationary.

Why energy inflation turns non-linear

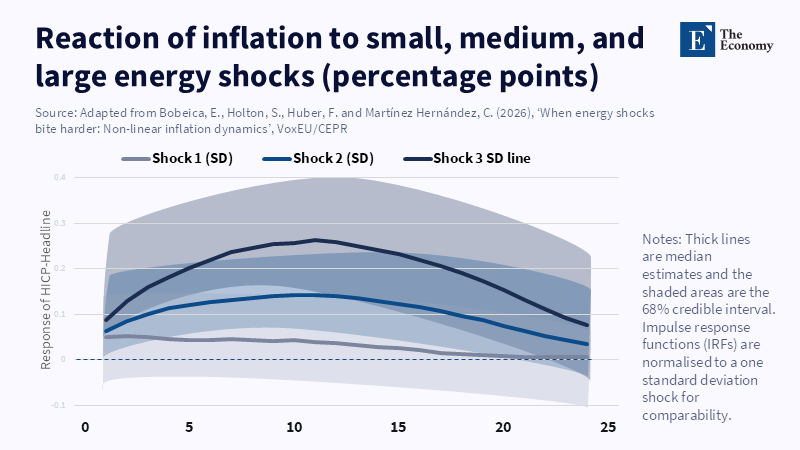

Energy inflation becomes non-linear because energy isn't simply another item in the basket. It's an input to almost everything. Oil shifts goods. Gas warms houses, energizes industry and determines the price of a significant share of chemicals. Fertilizer links energy to food. Energy carries a relatively small weight in the euro area consumer basket, around one tenth in 2026, but its influence extends far beyond its formal weight. When energy costs rise only slightly, firms can sit on their hands. When they go up by a lot, or remain elevated for a time, inaction is too expensive. The same shock then propagates at a greater speed because more firms are modifying their prices. This is how a sector shock can turn into a broad-based price inflation event. It's also why headline inflation can underestimate the near-term danger.

This is the important takeaway from recent research on non-linear inflation dynamics. In the 2022 energy shock, firms were not just raising prices normally and on schedule. They were changing more rapidly. Large cost shocks drove prices away from their target margins and firms responded more quickly. In one firm-specific study, gaps of around 20% or more led to a much steeper zone for adjustment. A standard model with preset pricing dates would be consistent with more normal times, but not with such a large inflation blowout. This is why energy inflation can seem like a relatively gentle rise at first and then get out of control. The transmission mechanism under strain is changing. Price stickiness is weakened when firms can no longer treat the cost shock as a form of noise.

Endogeneity is the hidden accelerator

The fundamental problem is endogeneity. Large energy shocks do not merely hit the economy from outside. Once it hits, it changes the economy it affects. Firms update pricing rules. Workers seek to protect real wages. Banks reassess risk. Governments move from normal budgets to emergency support. Importers face weaker terms of trade. These responses are individually rational; in aggregate, they can magnify the original shock. This is why large shocks can generate large effects; they can generate a new inflation regime. Energy inflation becomes harmful because it triggers reactions that, in turn, make inflation more likely and when this happens, the shock is no longer just out there among the data but embedded in behavior, in contracts and in politics.

2022 is an example of this difference in the euro area. A non-linear approach to modeling energy supply shocks concluded that without them euro area inflation by mid 2022 would have been far lower than the actual 8.3%. A linear approach would have failed to capture much of this difference. The point is not that every future shock will be just as impactful as those in 2022. Rather, it is that high-inflation conditions heighten the impact of the same shock. Once energy inflation has pushed up the general level of concern, subsequent spikes in prices shift down expectations and, under sticky-cost assumptions, leave less of that impact in the form of higher prices to be run through the system. That's why judging the current event by the reading in minutes is wrong; the implications for inflation and profit margins have to be estimated in terms of their effect on anchored expectations and prevailing contracts.

Oil prices offer false comfort

A common response is that oil has not returned to the extremes of 2022 and that futures curves often point to relief. That is a useful signal but it is not a safe policy anchor. Oil is a market of thin margins; short-run demand is price inelastic as we cannot quickly substitute transport, heating, petrochemicals and freight. Analysis suggests that short-run oil demand elasticities are low, frequently in the -0.3 to -0.1 range. In other words, once a price rise has occurred, demand does not react strongly enough to restore the balance immediately; adjustment occurs through income effects, substitution and forced constraints. This takes time. That process can result in energy inflation crossing through to prices that do not then revert as rapidly as the Brent.

That is why the oil price itself is not linear. Under normal conditions, a tiny shock can be absorbed by inventories, or spare capacity, or weak demand. Under conditions of a large shock, buffers matter less. Storage declines, risk premia rise, shipping costs escalate and customers bid for security in barrels. Energy-intensive firms cut back production before consumers can fully cope. A 1% decline in supply triggers a greater price response in a stressed market than in a slack one. This is not speculation, but a consequence of the nature of oil demand. The more inelastic the demand curve, the more severe the price response to a squeeze in the supply side. Oil is thurfore not just a trigger for energy inflation. It can also amplify the shock.

The same chains extend beyond crude. Gas provides the energy for power bills and fertilizer. Fertilizer supplies the farm’s operating costs. And the farm supplies food prices with a lag. Fertilizer prices are forecast to rise 31% in 2026 and even more in urea prices. From there, food prices may not jump as much as they did in 2022 because the direct supply shock focused on grains and therefore food, directly. But the chain is still significant. A food system depending on gas-fed fertilizer is still incorporated into energy inflation. It enters through a different door. Policymakers should follow the second door, not just the gasoline pump. An overly narrow focus on oil could overlook a more gradual but more stubborn inflation corridor.

The best policy response is not to panic. It is containment before confirmation. Central banks should not overreact to every increase in energy inflation as evidence that headline inflation is unmanageable. But they should be prepared to act before second-round effects become evident in an increase in all wages and all service prices. By that point, the behavior change is complete. Monetary policy should be sending a message that temporary energy shocks will be permitted only so long as expectations remain anchored, non-energy wage growth corresponds to headline prices and non-energy inflation remains well observed. This message should be unmistakable but subdued. The most credible message is one that is mundane, unwavering and early. It should defuse the drama. It should not accentuate it. And it should leave no ambiguity over the target.

The challenge for fiscal policy is even more severe. Wide-ranging subsidies can mitigate measured inflation, but they also push demand upward and undermine the price signal. The right approach is targeted assistance to lower-income households, temporary liquidity support to viable, energy-using firms and hastening permits for fuel switching, storage and grid investment. Governments should avoid tax reductions that cheapen energy for everyone. They should also be wary of blanket support promises that convert any future price increase into a pre-emptive claim on the public purse. Recognizing the shock is not the aim. The aim is to prevent the shock from becoming the common currency of all prices. Energy inflation policy must protect the vulnerable without eroding the incentive to exercise energy efficiency. That will be hard, but it is imperative.

A common pitfall of early containment is the fear of overkill. And in some cases, a ceasefire may come. Oil prices may retreat. Headline inflation may slow. This pitfall is understandable, but shallow. It costs less to stop a gradual early response than to deal with the mess after inflation accrues. The 2022-24 fracas revealed how hard it is to undo inflation once it enters the broad economy, housing, food, services and everything else. Real incomes fall before core prices do. Public bitterness intensifies before core prices do. Tight monetary policy then has to do more work, through slower demand growth. In a supply-shock case, this is a poor remedy. It turns a price shock into a social shock.

Institutional speed is the real challenge. All finance ministries and all central banks should now measure the energy price shock through freight, fertilizer, wholesale power, margins, wage claims and short-term expectations. Stress-test thresholds-not averages-should be relied upon. Contingency budgets should have been assembled before the next surge, not after and they should be narrow and time-limited. Most importantly, policymakers should approach energy inflation as a systemic threat. The opening figure was 10.8% energy inflation. It is not destiny. It is a warning. The task is to keep it as a warning, before the economy chooses a new language. That would entail a ceasefire where politics can secure it, unambiguous monetary signals where expectations can still wander and targeted fiscal policies where households are unprotected. The point, however, is simple: contain the pass-through before it writes the next inflation episode.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Baumeister, C. and Peersman, G. (2013) ‘Time-varying effects of oil supply shocks on the US economy’, American Economic Journal: Macroeconomics, 5(4), pp. 1–28.

Bobeica, E., Holton, S., Huber, F. and Martínez Hernández, C. (2026) ‘When energy shocks bite harder: Non-linear inflation dynamics’, VoxEU/CEPR, 20 May.

Bobeica, E., Holton, S., Huber, F. and Martínez Hernández, C. (2025) Beware of large shocks! A non-parametric structural inflation model. ECB Working Paper Series, No. 3052. Frankfurt am Main: European Central Bank.

Burian, V. (2026) ‘Non-linearities in oil prices: Which conditions matter?’, ECB Economic Bulletin, Issue 2/2026.

Caldara, D., Cavallo, M. and Iacoviello, M. (2019) ‘Oil price elasticities and oil price fluctuations’, Journal of Monetary Economics, 103, pp. 1–20.

Cavallo, A., Lippi, F. and Miyahara, K. (2024) ‘Large shocks travel fast’, American Economic Review: Insights, 6(4), pp. 558–574.

European Central Bank (2026) Economic Bulletin, Issue 2/2026. Frankfurt am Main: European Central Bank.

Eurostat (2026) ‘Annual inflation up to 3.0% in the euro area’, Euro Indicators, 20 May.

Gagliardone, L., Gertler, M., Lenzu, S. and Tielens, J. (2025) ‘Micro and macro cost-price dynamics in normal times and during inflation surges’, VoxEU/CEPR, 6 June.

World Bank Group (2026) Commodity Markets Outlook: April 2026. Washington, DC: World Bank Group.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.