When the Dollar Leaves First: Foreign Currency Funding Risk and the Swiss TBTF Test

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Currency risk can turn liquidity into panic Credit Suisse exposed that weakness Swiss TBTF reform shifts the burden back to banks

Global foreign exchange reached $9.6 trillion dollars per day in April 2025, a number so large that it can make currency liquidity look almost limitless. If we consider the evidence of the infinite liquidity well, it looks like an amount of money cannot be found. It is never the average market that goes bankrupt. It is the specific moment in which the only currency that is needed cannot be borrowed, transferred, or exchanged fast enough. Credit Suisse exposed that weakness. Until the worst moment of the run, the bank provided sound liquidity ratios. It kept large buffers. It used derivatives to offset currency risk. When the currency confidence was broken, however, the buffers quickly transformed into 'choked off routes' because of the currency funding risk. The money was there, but not necessarily in the legal entity, currency, or time zone. This is why the next phase of the Swiss TBTF reform should not just be focused on the size of the balance sheet but on whether the foreign operations could survive a currency run without the official support.

This contains an even more direct policy message than most hedging debates. Banks have to hedge exchange-rate risk. That will not do. The hedging might not hold up when it has to be rolled over in an impossible market, or collateralized through a crisis, or replaced after counterparties have lost confidence and pulled away. Every global bank has to demonstrate that its own lines of credit, interbank payments and parent capital make sense when it is not believed by others. This provides the clearest framework to understand what is happening in Switzerland in the recent reform proposals. They are not simply a question of whether UBS should exist; they are an attempt to establish whether the true cost of foreign activity sits on the parent before a crisis or on the public balance sheet afterward. It should be about private discipline and not regulation for regulation's sake.

Foreign Currency Funding Risk Is a Liquidity Problem with a Capital Face

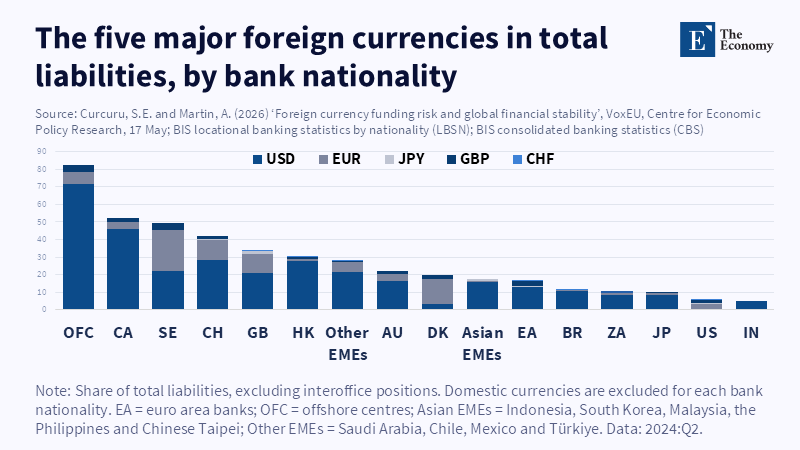

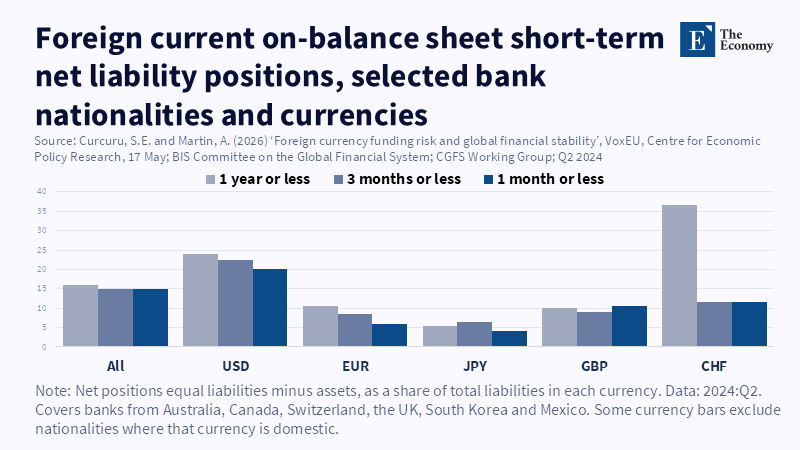

Could be described as a treasury problem, the foreign currency funding risk has much broader implications than at first glance. The problem belongs between the liquidity, capital, market access and group structure ones. Even with a fully liquid balance sheet, a bank might be dangerously short of the actual dollar funding it requires, having put on a hedge mismatch and still be under stress if it has to roll the hedge and cannot find a way to do it. Or have a dollar presence in a subsidiary bank, but in the wrong jurisdiction, at the wrong time, or in the wrong currency. A weak balance sheet line is not the key to it. The key is the gap between the legal entities, the currencies and the markets when the storm breaks out, that is easily forgotten during normal times as the global structure is built to transfer the money across the borders rapidly, but breaks down during stress when the regulators start ring-fencing the operations, the payment systems demand a higher amount of collateral and the swap markets dry out.

A case in point can be found in Credit Suisse in 2022, where this was starkly demonstrated. Despite the fact that it was categorized as a global systemically important bank and maintained around two-thirds of its leverage exposure in foreign currencies (with FX derivatives used to reduce currency mismatches), the bank was still exposed to a severe confidence and liquidity crises. It had significant liquid assets (roughly 30 percent of its assets as of the end of September 2022) and a liquidity coverage ratio of 191 percent, they were still unable to intervene during a time of crisis to help out. These figures, while healthy enough during the calm, are not a plan of action to intervene if the markets freeze and they are unable to transfer dollars through the payment systems or reinstate the confidence of the banks' counterparties. It was not so much the availability of the liquidity but where it was placed and how quickly it could be moved that was the issue, not even whether the markets would convert it to the desired currency.

The first stage of the stress was in October 2022, triggered primarily by negative market publicity and rumors leading to outflows (primarily from international wealth management clients, many in foreign currencies), after which there was a second stage in March 2023, triggered following the collapse of two US banks, after which markets searched for the next weak institution. This second stage was more broad-based as both domestic and international clients responded. The need to fund domestic payments, to satisfy clearing requirements and regulations and time zone complexities reduced the available pool of foreign currencies to be moved around the group. The Swiss National Bank then injected CHF 168 billion of liquidity in Swiss Francs, Euros and US dollars; in order to obtain dollars for this purpose, it collateralized US Treasury Bonds to the value of USD 75 billion through the FIMA repo facility of the Fed, a public rescue of private funding channels.

Swiss TBTF Rules Now Make Foreign Currency Funding Risk a Parent Bank Duty

This is at the core of the reform in Switzerland that is being proposed to address yet another potential weak point in the system. The reform calls for systemically important Swiss banks to fully back the carrying value of their foreign subsidiaries with Common Equity Tier 1 capital (which was, until recently, only 60%). By 2025, the Swiss Federal Council predicts that the CET1 requirement for the UBS parent bank will be approximately $20 billion higher, although with existing buffers, the gap is closer to $9 billion. There will be a seven-year lead time to implementation should the parliamentary process not prove lengthy, but the rationale behind this change is quite simple: in a crisis, if the foreign subsidiary poses liabilities for the parent, the parent bank ought to be responsible for them.

Foreign currency funding risk meets TBTF here. Since the parent bank's consolidated financials only show one balance sheet, the foreign subsidiaries' exposure to the parent is slightly less transparent. Loans, guarantees, capital locked up elsewhere, local regulations and domiciliary liquidity are all likely to imply an obligation on the parent to stand behind the foreign subsidiary in a crisis. Though a parent is obviously expected to stand behind its foreign subsidiaries, in terms of capital burden, this is not necessarily obvious until it is looked at on a case-by-case basis. The path to 100% CET1 backing should make transparent the implicit obligation and give the parent bank the ability to sell, shrink, or support these foreign subsidiaries, without the bank's own capital levels excessively suffering when the markets are under stress, just like Credit Suisse.

There are costs to these reforms. UBS believes the rules are overly restrictive and not aligned with international standards. Allowing full deductibility of investments in foreign subsidiaries would, at a minimum, add $20 billion to the CET1 of UBS's parent, with even higher amounts under broader proposals. UBS also warns that the zero-value policy on foreign subsidiaries would impose efficiency costs and could increase the cost of credit. The policy has to avoid overreacting because it would have the unintended consequence of pushing risk-taking into the shadows.

However, the group liquidity plans that founder in crisis reveal the need for policy change to require banks to have unambiguous plans to cover their foreign unit losses and how they will fund or sell them, without endangering the parent bank, even if the market pressures them to do so. If banks cannot be explicit, then it signals a public threat that policy has to resolve. This explains why Swiss TBTF reform remains continuous and targeted.

A New Test of Usable Resilience in a Panic

The core criticism of the Swiss proposal relates to its focus on pure capital thickness rather than effectiveness or resilience. Additional CET1 capital for the parent does not give you virtual dollars, but it cannot reopen currency swap markets or dismantle legal hurdles to cross-border capital movement either. Nor, of course, does it remedy cultural or strategic shortcomings-for example, Credit Suisse was not just a victim of currency mismatches but of years of scandal, mismanagement, inadequate control and repeated failure. So capital may not substitute for a good organization and culture, but funding design cannot be divorced from y the question of funding design from its effects on culture or strategy, particularly the speed with which a diminution of trust can turn into a demand for foreign currency.

However, it is impossible to prescribe a single ratio that would assure stability, because there are numerous sources of failure. The proposed measures, based on the international rules of TBTF, should cover: bank-level measurement of FX risk; whether the hedge is tested for rollover, collateral risks, etc.; a credible plan for currency transfer in stress; and parent capital adequate to support or dispose of foreign subsidiaries without public assistance. The goal should be to leave global banks self-sufficient in stress or even panic, not to be rescued by taxpayers.

International evidence backing the increased attention to these issues is also available. Despite its size, the FX market is increasingly complex and evidence indicates that macro-stress episodes generate higher funding costs, lower liquidity and financial spillovers to bond and equity markets. As an increasing number of derivatives are used by non-bank financial intermediaries and dealer networks and payment systems aggregate into systemic stress points, a global bank is like a single node in an elaborate network of potential crisis propagation channels. Funding risk for foreign currencies, therefore, should not be kept only on the treasury dashboard but embedded in the strategy, the business model, growth decisions and subsidiaries' structure long before a crisis hits.

For banks' boards and senior managers, this implies that a business line with high foreign earnings but using short-dated dollar swaps or dubious intra-group loans to fund itself is imposing a public risk that should be incorporated in internal pricing even before the government has to act. If an overseas subsidiary cannot be financed in a time of crisis without endangering the parent, its growth is not cheap but based on the premise of open markets. For supervisors, the lesson is practical: tests should be multi-currency runs, blocked transfers, failed rollover FX swaps and failed settlements. The key issue is not whether a bank has cash, but whether that cash is available in the required currency.

The debate has now become a Swiss ideological divide. One camp says the new TBTF rules are vital for taxpayers, another that they are damaging to UBS and the Swiss financial system as a whole. The reality is somewhere in the middle: a well-capitalized bank unable to compete effectively is not a stable system, a globally competitive bank in need of state support during a foreign currency panic is not truly private. A common sense middle way is targeted TBTF reform, which requires higher capital at the parent where foreign operations generate liabilities, foreign currency specific liquidity requirements, liquid and tradable risk management, operational crisis plans and cross-border drills. These will not prevent every single bank failure, but they would go a long way towards avoiding a taxpayer-financed bailout caused by foreign currency funding risk. It should not be forgotten that the daily FX trade of $9.6 trillion can disappear in a heartbeat, leaving even a large bank exposed at the exact moment confidence disappears. TBTF reform needs to provide that the parent bank, not the public balance sheet, is the first port of call during a dollar crisis, by including it in capital, liquidity and governance requirements before a weekend panic. A truly robust reform does not look good in quiet times, but can still operate during a dollar crisis.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Basel Committee on Banking Supervision (2023) Report on the 2023 Banking Turmoil. Basel: Bank for International Settlements.

Bank for International Settlements (2025) Triennial Central Bank Survey: OTC Foreign Exchange Turnover in April 2025. Basel: Bank for International Settlements.

Committee on the Global Financial System (2026) Foreign Currency Funding Risk and Cross-Border Liquidity. CGFS Papers No. 71. Basel: Bank for International Settlements.

Curcuru, S.E. and Martin, A. (2026) ‘Foreign currency funding risk and global financial stability’, VoxEU, Centre for Economic Policy Research, 17 May.

Federal Council (2026) Too-Big-to-Fail Regulations: Federal Council Adopts Dispatch and Capital Adequacy Ordinance. Bern: Swiss Confederation.

Federal Department of Finance (2026) Too Big To Fail. Bern: Swiss Confederation.

FINMA (2023) Lessons Learned from the CS Crisis: FINMA Report. Bern: Swiss Financial Market Supervisory Authority.

Financial Stability Board (2024) Depositor Behaviour and Interest Rate and Liquidity Risks in the Financial System: Lessons from the March 2023 Banking Turmoil. Basel: Financial Stability Board.

Fitch Ratings (2026) Timing, Impact of Swiss TBTF Proposals on UBS Still Uncertain. New York: Fitch Ratings.

UBS Group AG (2026) UBS Statement on Regulatory Capital Announcements Made by the Swiss Government. Zurich: UBS.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.