Banks Should Hedge Rate Risk Before Calm Turns Costly

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Banks cannot treat interest rate risk as a crisis-only problem Derivatives can soften rate shocks, but they also create new liquidity and governance risks Supervision should tighten when rate stress rises and ease when conditions calm

A 450-basis-point increase in euro-area policy rates and a 525-basis-point hike in the United States turned a routine treasury task of interest rate risk hedging into a matter of bank viability. Those moves followed years when rates moved slowly and hovered close to zero. The pace was as important as the level. Securities declined in value, depositors earned higher rates elsewhere and concealed duration mismatches emerged all at once. The lesson is not that every bank requires similar levels of derivatives oversight in every market; that would turn what is an extraordinary response to a systemic emergency into an eternal administrative burden. Rather, it is that supervision must match risk. Calm periods necessitate a straightforward, consistent risk position picture. Fast rate moves demand incremental and intense monitoring. Hence, supervising interest rate risk hedging through a threshold-based approach tied to rate levels, speed, funding stress and balance-sheet sensitivity and allowing that threshold to ease once those dynamics subside, would be an appropriate management tool.

Why Interest Rate Risk Hedging Became a Crisis Tool

The inflationary shock of 2022 was a change in the price of waiting. Inflation in the euro area was 10.6% in October 2022. Inflation in the US was 9.1% in June. Central banks responded at a pace that many bank models had not represented as a real risk. A bond with a fixed rate does not need to go into default to do damage. It just needs to pay less than a new bond. As a rough estimate, a bond portfolio with a modified duration of five years can lose roughly 5% if yields increase by one percentage point. A billion-dollar position can therefore fall in value by nearly $50 million. The precise loss depends on flows and convexity, but the general trend is straightforward. Selling the bonds solidifies the resulting loss. Retaining them may keep the book value in the books, but it leaves the bank open to funds flowing out, to collateral demands and to the market believing the worst. It is therefore for that reason that a rapid rate rise makes balance sheet adjustment so difficult precisely when speed counts the most.

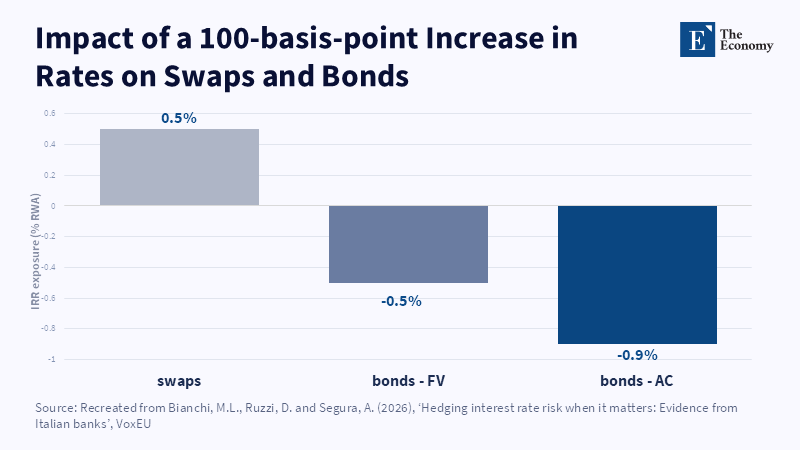

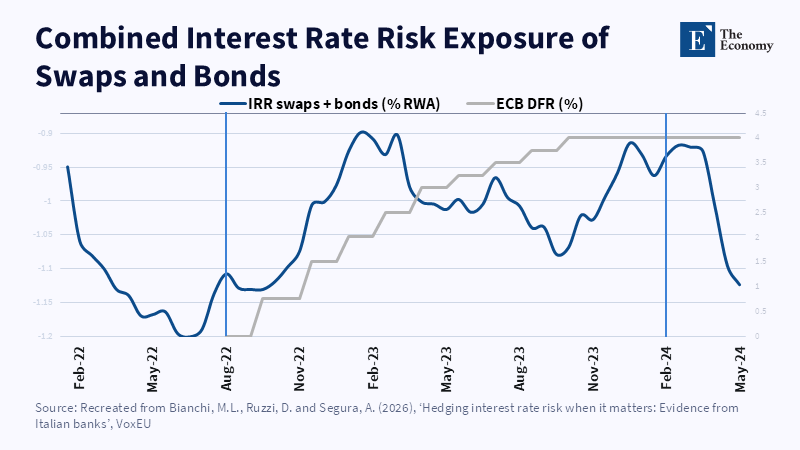

Derivatives provide the speedier route. They allow an interest rate swap to modify the rate profile on an existing asset without having to sell off that asset itself. This can be less costly than liquidating a large bond portfolio in a declining market. Indeed, the Italian evidence shows that when Italian banks tightened their policy between 2021 and 2024, bond losses following a notional 100-basis-point hike in interest rates were roughly 1.4 percent of risk-weighted assets, with gains following swaps averaging roughly 0.5 percent. In practice, derivatives offset roughly one-third of the bond losses. Moreover, just as duration hedging intensity increased by roughly 6 percent in the aftermath of a tightening cycle, so can derivatives. Evidence that these financial derivatives can reduce interest rate risk does not mean they would do so under all circumstances. It simply means that given a jump in the term structure that finally makes that risk too costly and transparent for banks to ignore, they resort to derivatives.

The US experience warned of the costs of reliance on the banking assumption. The study of US banks that commanded more than 80 percent of all assets found that interest rate swaps played only a small part in offsetting risk in the aggregate asset positions. One calculation put this at around 6 percent. Silicon Valley Bank was an extreme case but not alone in sounding alarm bells. It withdrew interest rate hedges and moved its focus toward short-term earnings as rates climbed. On the liabilities side, it used a narrow band of uninsured deposits. Confidence was lost – more than $40 billion was withdrawn in a single day; another hundred billion was expected to follow. Its downfall was not caused by one bad bond or one failed hedge. It was the result of duration risk piling into weak governance, volatile funding and late-coming supervision. Policymakers need to learn from their experience. A report on derivatives in isolation was ineffective. One on an integrated perspective on assets, liabilities, deposits, liquidity and hedges could have been.

Derivatives Are Fast, but They Are Not Free

The size of derivatives markets can make any call for lighter regulation appear reckless. In June 2024, the Bank for International Settlements reported a notional stock of interest-rate derivative contracts close to $579 trillion. That is a huge sum, but the notion value isn't money at risk: it's the reference sum used for payment calculations. The market value of those trades is much lower-and fluctuates with changes in rates, netting, collateral and maturity. Between 2024 and 2025, the notional value of interest rate derivatives was nearly zero while their gross market value declined for a third consecutive reporting period. As the pace of rate tightening had abated, the value of the outstanding contracts fluctuated less. In 2025, notional sums grew again amid greater policy and trade uncertainty. Such changes just bolster the case for conditional regulation. A huge notional sum in itself is no indicator of risk. Supervisors must learn where contracts fluctuate in value, need collateral, or stand against tangible risk positions.

Derivatives introduce a variety of other risks which are not apparent from a dull bond-focused perspective. While a hedge can result in an increase in economic value, it can simultaneously result in a cash outflow via margin calls. One contract can help against a parallel shift of rates, but fails when different points of the yield curve move differently. A swap can also match the stated maturity of the asset but not the duration. This is especially visible in mortgage-backed securities, where the repayment behavior of borrowers changes with such rate moves. Counterparty, basis and rollover risks, as well as rules on hedge accounting, can all erode the effectiveness of the hedge. Often, complex products cause pricing and governance issues. A prudent institution, therefore, often prefers a plain vanilla swap or cap because layered products are too difficult to be explained by most directors. The goal of hedging interest rate exposure, after all, is not to make finance managers' reported earnings more stable, but to eliminate the possibility of a rate move turning into a capital or liquidity crunch.

Direct asset sales are still useful, but during a period of stress, they often are slow and expensive. A study of portfolios of US securities revealed that when banks suffered securities losses, they trimmed purchases and reduced the duration of the new purchases they made. They did not appear to sell outright the securities they had bought at a loss, did not grow formal accounting hedges very much and were constrained in their ability to act by fixed costs, existing systems and the complex nature of callable bonds. Another study showed that the banks that made the biggest securities losses pulled back more from business lending. The effect was more pronounced if, as tended to be the case, the securities position was not fully hedged. That is a public cost. The bank that forgoes a hedge may secure the current period's income, but a future rate shock may then depress credit to otherwise healthy companies. Derivatives may cushion that spillover, but requiring every bank, in every period, to keep a large hedge is not costless: premiums, collateral, staff, models, legal work and accounting are not cheap. Policymakers need to factor in both effects.

Interest Rate Risk Hedging Needs a Regime Switch

Normal times are not without risk, but they do reduce the economics of the hedge. When rates rise within a relatively narrow band, banks can gradually change new lending, pass through deposit pricing and buy assets. The retail deposit base can also be a 'built-in' hedge. During the ECB tightening cycle, policy rates increased by 450bp. As of October 2023, new time deposit rates had increased by 372bp, while new overnight deposit rates increased by only 50bp. The slow pass-through kept bank margins protected for a while. It also meant some banks did not have to purchase large derivative positions. To that extent, a large retail deposit base can anticipate a part of a rate shock. However, this protection hinges on customer behavior. Depositors might accept low returns this time before moving quickly next time. Online banking amplifies that shift. A large, ongoing deposit franchise remains an economic hedge only if deposit volumes and interest rates do not change.

This is where a static supervisory rule runs into difficulty. Non-stop reporting at crisis levels would analyze small retail banks with bank-like short-term assets as if they were large banks with long bonds, wholesale funding and rate-sensitive depositors. It would also drown supervisors in data that is rarely useful for making decisions. The superior model would have three speeds. First, there would be an evergreen baseline. Banks would be required to keep supervisors up-to-date on key duration-gap figures, swap ratios, collateral terms, counterparty concentration and the exposure-to-standard-rate shocks. Second, there would be even closer review if risk indicators rose, such as a large change in policy rate, a growing duration gap, large losses when tested against an economic value, rising deposit betas, deposit drains and increasing margin needs. Third, there would be intense surveillance during a live-rate shock, where weekly or daily data would be reviewed as needed on the most sensitive firms. The supervisory burden would never be eliminated. It would just become a question of how slowly supervision proceeds and how fast it can respond.

A trigger-based model, on the other hand, can incorporate existing rules. European standards, for example, test the impact of abrupt changes in interest rates on the economic value of equity and net interest income. A decrease of more than 2.5% of a bank's Tier 1 capital in a year's net interest income is viewed as a material decline that may trigger supervisory concern. Such a threshold should not be used in isolation, but it certainly provides supervisors a reasonable benchmark. The bank could remain in baseline review as interest rate moves are moderate, deposit flows are normal and stress losses are easily covered by capital. When two or more signals exceed predefined thresholds, the bank could move into enhanced supervision. When funding pressures and market losses coincide, it could be placed under intensive review. This framework would direct limited supervisory resources toward those banks for which derivatives provide transmission or mitigation of a shock, while making escalation less reliant on the judgment of a single examiner.

The strongest criticism is that risk often accumulates in quiet periods. Years of low rates lead banks to buy longer assets and to presume a generation of cheap, loyal deposits. Conditional supervision cannot be seasonal slack. Baseline data must still be collected and even in quiet markets, stress tests should simulate large moves. The only thing that should be non-seasonal is the frequency and depth of transaction-level scrutiny, not the need to monitor where the position is. Another criticism is that banks should hedge before a shock, not after. That is also accurate, but supervisors should not impose a pre-hedge ratio on every institution. The correct pre-commitment is a board-approved strategy. It should specify which kinds of risks will be hedged, through what devices, what events will prompt a change and how much more collateral liquidity should be kept handy. The regimes should be uniform. Trading volume can be conditional.

A Conditional Rule for the Next Rate Shock

A sound policy would decouple the risk map from the hedge itself. The central banks and bank supervisors first need to quantify (for fixed-rate assets, non-maturity deposits, wholesale funding, off-balance-sheet deals, collateral calls and the likely behavior of customers) the total exposure. After that, they can assess whether the derivatives were a better or a worse means of distribution or elimination of that risk. A swap that would eliminate interest rate risk but entail a large short-term liability is not a perfect hedge. Neither is a deposit model that makes generous revenue estimates in the expectation that customers will stay passive even when rivals put up their rates. The review should also evaluate similar institutions with comparable funding and asset profiles. Evidence from Italy shows that weaker capital and more wholesale funding cause a bank to hedge more with derivatives. That is intuitively right, but it also implies an excess of demand when other banks do the same during a crisis. Supervisors need to monitor concentrations of dealers and clearing houses if a dozen or more banks transfer their positions at one time. The policy question is not whether derivatives are good or bad. It is whether the industry has the capacity to sustain this level of hedge.

The next phase of quiet will test whether the lesson has taken hold. Unrealized losses at US banks had fallen to $413.2 billion by the first quarter of 2025, down 20% from a year previously, but they had not disappeared. Lower inflation and rate cuts can ease visible pressures without correcting weak models and poor governance or unstable funding profiles. The risk is an ersatz choice between permanent crisis controls and neglect. Interest rate risk hedging is not needed. It needs a rule that tightens before losses form a run and loosens when the evidence can support it. Banks should keep clean exposure data, simple approved instruments and sufficient liquidity to sustain their hedges. Supervisors should escalate when rate speed, duration and funding fragility climb together. The 450-basis-point shock was no reason to pound on every derivative the same way, for eternity. It was evidence that supervision must be prepared to change gears before the market does.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Acharya, V., Carletti, E., Restoy, F. and Vives, X. (2024) Banking Turmoil and Regulatory Reform. The Future of Banking 6. London: CEPR Press.

Adalid, R., Lampe, M. and Scopel, S. (2024) ‘Monetary dynamics during the tightening cycle’, ECB Economic Bulletin, Issue 8/2023.

Ahnert, T., Bertsch, C., Leonello, A. and Marquez, R. (2025) ‘Bank fragility and risk management’, CEPR Discussion Paper No. 19523. London: Centre for Economic Policy Research.

Alhusaini, M. (2022) ‘Hedging the interest rate hiking cycle’, Enterprising Investor, CFA Institute, 10 May.

Bank for International Settlements (2024) OTC Derivatives Statistics at End-June 2024. Basel: Bank for International Settlements.

Bank for International Settlements (2025) OTC Derivatives Statistics at End-June 2025. Basel: Bank for International Settlements.

Bianchi, M.L., Ruzzi, D. and Segura, A. (2026a) ‘Banks’ dynamic interest rate risk hedging’, CEPR Discussion Paper No. 21588. London: Centre for Economic Policy Research.

Bianchi, M.L., Ruzzi, D. and Segura, A. (2026b) ‘Hedging interest rate risk when it matters: Evidence from Italian banks’, VoxEU, 29 June.

Board of Governors of the Federal Reserve System (2023) Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank. Washington, DC: Board of Governors of the Federal Reserve System.

Board of Governors of the Federal Reserve System (2024) Monetary Policy Report, July 2024. Washington, DC: Board of Governors of the Federal Reserve System.

Drechsler, I., Savov, A. and Schnabl, P. (2021) ‘Banking on deposits: Maturity transformation without interest rate risk’, Journal of Finance, 76(3), pp. 1091–1143.

European Banking Authority (2022) Guidelines on the Management of Interest Rate Risk and Credit Spread Risk Arising from Non-Trading Book Activities. EBA/GL/2022/14. Paris: European Banking Authority.

Federal Deposit Insurance Corporation (2025) Quarterly Banking Profile: First Quarter 2025, 19(2). Washington, DC: Federal Deposit Insurance Corporation.

Fuster, A., Paligorova, T. and Vickery, J.I. (2024) ‘Underwater: Strategic trading and risk management in bank securities portfolios’, CEPR Discussion Paper No. 21036. London: Centre for Economic Policy Research.

Greenwald, D.L., Krainer, J. and Paul, P. (2024) ‘Monetary transmission through bank securities portfolios’, NBER Working Paper No. 32449. Cambridge, MA: National Bureau of Economic Research.

Guerrini, G. and Rice, J. (2025) ‘Interest rate and deposit run risk: New evidence from euro area banks in the 2022–2023 tightening cycle’, VoxEU, 22 August.

Hoffmann, P., Langfield, S., Pierobon, F. and Vuillemey, G. (2019) ‘Who bears interest rate risk?’, Review of Financial Studies, 32(8), pp. 2921–2954.

Jiang, E.X., Matvos, G., Piskorski, T. and Seru, A. (2023) ‘Limited hedging and gambling for resurrection by US banks during the 2022 monetary tightening?’, SSRN Working Paper.

Jiang, E.X., Matvos, G., Piskorski, T. and Seru, A. (2023) ‘Monetary tightening and US bank fragility in 2023: Mark-to-market losses and uninsured depositor runs?’, NBER Working Paper No. 31048. Cambridge, MA: National Bureau of Economic Research.

Lane, P.R. (2024) ‘Disinflation in the euro area’, speech delivered at the Hutchins Center on Fiscal and Monetary Policy, Washington, DC, 8 February.

Lu, X. and Wu, L. (2026) ‘Banking on inattention: When deposits hedge or amplify interest rate risk’, VoxEU, 16 February.

McPhail, L., Schnabl, P. and Tuckman, B. (2023) ‘Do banks hedge using interest rate swaps?’, NBER Working Paper No. 31166. Cambridge, MA: National Bureau of Economic Research.

Nelson, W.R. (2024) ‘Deposit and interest rate risk: Some simple but surprising results’, Bank Policy Institute Research Note, 29 January.

US Bureau of Labor Statistics (2022) ‘Consumer prices up 9.1 percent over the year ended June 2022, largest increase in 40 years’, The Economics Daily, 18 July.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.