India’s Boardroom Moment: Why the India Investment Pivot Now Needs Policy, Not Slogans

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Japan and Korea are turning to India China is losing some appeal India must turn investment into production

One number now redraws Asia's industrial map: ¥10 trillion (about US$63 billion). That's Japan's new commitment for private investment in India over the next ten years. This is not aid. It is not a slogan from the summit. It is not an empty phrase uttered in a battle cry. It is a cold, hard fact from the boardroom: the India investment pivot has moved from diplomatic rhetoric to capital plans, factory blueprints, bank structuring, supply-chain risk management strategies. This is a milestone because it isn't just friendship. It is three hard truths: China has become a tougher low-cost growth platform for foreign business; India remains a growing economy capable of supporting immense, long-term capital investment; the Quad is compelling Tokyo, Seoul, Delhi and Washington to develop a common strategic framework. The immediate task for India is straightforward: stop viewing foreign investment as a badge of pride and develop a system capable of handling it effectively.

The India investment pivot is now a boardroom reality

The advanced version of the policy assessment is that business is moving faster than politics. Business sustained the Indian investment pivot while politics were weak and now politics is rushing to catch up. India's relations with the US were strained in 2025 because of tariffs, energy imports from Russia and Washington's delicate diplomatic dance with Pakistan and China, which did not, despite risks that this situation could slow the India strategy. Firms were responding to a pragmatic imperative to find a home for ten years of future Asian growth rather than to diplomatic atmospherics. Japan subsequently ramped up its private-investment ambitions to 10 trillion, building on an existing 5 trillion objective, which was reportedly met in three years. The key nuance is that the India investment pivot is not a technique of soft power; it's a decision of capital allocation.

The numbers, however, already hint at a bigger change than the exhausted "China plus one" cliché. In 2025, Japanese businesses poured in a record 8.8 billion dollars to Indian firms, including MUFG investing close to 4.4 billion dollars in a stake in Shriram Finance, the most significant investment in the Indian financial sector to date. For the second year in a row in 2024, Japanese foreign direct investment in India, in total, had already overshadowed its rival in China, as data from JETRO has been citing, as reported by FT. It does not imply a total sweep of China, which remains a vast, cost-effective production center, but the trend makes itself clear: Japan is steadily heading for a country where it can procure not only new innovation, skilled workers and time, but also strategic security.

South Korean companies are taking a parallel route. The country ranks as the 13th largest foreign investor in India, with a cumulative equity investment of $6.81 billion from 2000 April to 2005 June 2025. Hyundai's $ 3.3 billion flotation was India's largest IPO and LG Electronics India's valuation was higher than the parent company's listed name in Seoul. Hyundai announced a fresh investment of $ 5 billion in India till 2030 aimed at increasing output, bringing out new models and establishing India as a global export platform. The trend of companies like Samsung, LG and Hyundai investing in India is not because of an easy route but because China's openness is getting restricted and the domestic market is mature, while India sells both as a strong consumer market and a promising destination for fast growth. The India investment pivot is no longer a Japanese phenomenon but is a rising trend in North East Asia.

China's Setback is not India's Automatic Gain

The seductively simple story is that India is thriving as China loses some of its old pull. China is not simply declining; it is also working hard on the upgrading strategy. Precisely because of this effort, it is now becoming increasingly difficult for foreign investors and companies to use China as a way to reduce costs, as an infrastructure to tap into, or as a market to tap into. In 2024, average annual wages in China's urban non-private manufacturing sector reached 107,987 yuan, up from 157,964 yuan. Cost is not the only reason firms are rethinking China, but China is no longer the low-wage platform it once was

Consumer demand is the second pressure point. The other major factor serving as a pressure point is consumer demand: China's domestic market, although still enormous, does not give foreign firms the same demand assurance they had before. According to the World Bank, China's growth rate will be 4.9% in 2025 and 4.4% in 2026, while consumer spending power is predicted to stay soft due to a soft labor market and lower property prices. An urban depositor survey shows that more than 60% of respondents in Q2 and Q3 of 2025 favor saving over consumption or investment. For firms that thrive on a growing middle-class consumer base, this count is important. While a factory can go through a decade of weak domestic consumption with a strong export market, a consumer brand, lender, or automobile maker cannot run a firm for that length of time on such unsure household confidence.

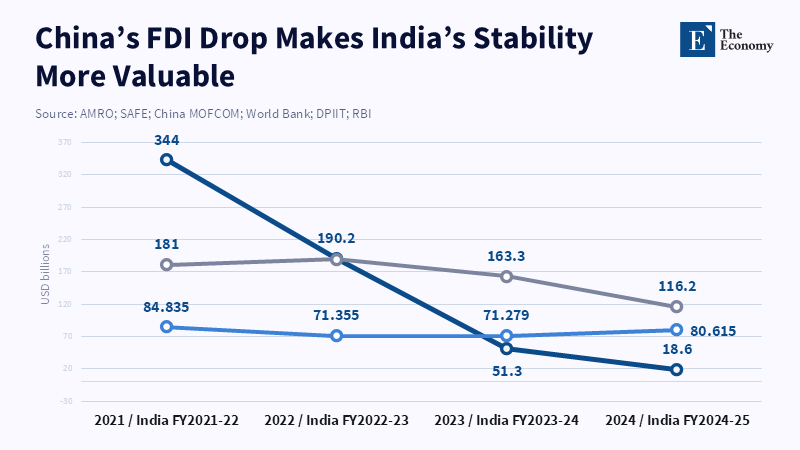

At the same time, India should not see this as an automatic win. Despite net FDI inflows into China falling from a high of 344 billion dollars in 2021 to 18.6 billion dollars in 2024, according to the balance-of-payments, AMRO also stated that usage of FDI in China was still 116.2 billion dollars in 2024 and interestingly, the utilization of FDI in high technology industries recorded an average annual growth rate of 15 percent in China from 2019 to 2023. Simply put, China is losing some old foreign capital and gaining new capital in high-end production processes. This is the reason India's investment pivot should really be seen more as a duel of execution with a focus on long-term commitment, as a duel in "performance" and not in "attention". Give India cheap labor and it will not succeed; provide India with speed, trust, talents and scale and India will get commitments for good.

Policy Must Turn the India Investment Pivot into Production

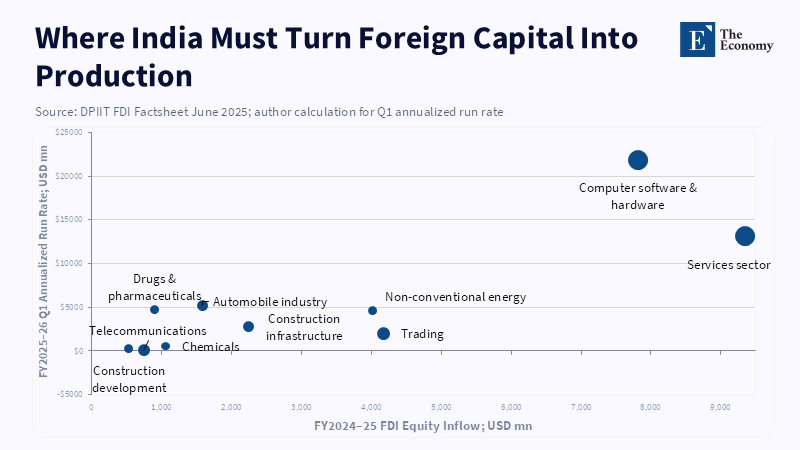

India's strength is not only in its large population but also in its mix of growth, capital markets, inter-state competition and youthful workforce. Despite external headwinds, the IMF expects India's growth rate to be 6.5 percent in FY2024/25 and 6.6 percent in FY2025/26. India has received gross FDI worth US$1.1 trillion from April 2000 to June 2025, with US$80.62 billion in FY2024/25 and another US$26.61 billion in the first quarter of FY2025/26, which is a 17 percent growth from FY2024/25. While these numbers speak for themselves in terms of investor interest, they are not the sole reasons for the setting up and sustainability of factories, the expansion of supply chains and the transfer of technology. This is where policy intervention is the need of the hour.

The first rule is to stop selling India as a cheap second best to China. India itself is an altogether different platform where China's strength was its complex supplier networks, its efficient ports and logistics, knowledgeable factory managers and responsive local governments. It is in this area that India's comparative advantage will have to come from a federation that balances such policies at the Center with good state-level implementations. The new Japanese investment facilitation center is a good step to build on as it will address the business pain points of state-specific regulations, legal uncertainty and the tax uncertainty. India will need to follow this up with joint investment offices at key states, time-bound customs clearance for approved investment, training of labor to real plant technology needs and time-bound dispute settlement. The India investment pivot will occur not in the room of the press conferences but in the store room of land records, electricity, ports, tax assessments and shop floor proficiency.

The second is to bring forward finance within industrial policy. Foreign banks and insurers are not bystanders; through lending and niche expertise, they can cut capital costs, support suppliers and promote long-term infrastructure provision. The steps of MUFG and Mizuho reflect an ambition for more than export customers in India; they show a desire to participate in its financial growth. This can support Indian entrepreneurs if regulators foster a competitive environment and do not treat foreign capital as either a risk or a solution. Korean listings serve as a sobering warning from the other side of the coin; local capital markets can own fund Indian subsidiaries. Host jurisdictions must demand better disclosures and corporate governance and demand that new investment is put back into the group at home. Policy should actively promote listings that add to the depth of India's market and be cautious of those that are simply a means of divesting foreign parent companies.

The Quad can Support the India Investment Pivot but it cannot Replace Reform

The reinvigoration of the Quad's agenda re-creates the external environment that was politicizing the India investment pivot. In May 2026, Quad foreign ministers from India, the United States, Japan and Australia met in New Delhi, with supply chains, critical minerals and Indo-Pacific security high on the agenda. Later, Reuters captured details of how Rubio's trip is aimed at repairing damaged India-U.S. Relations and will focus on discussions on energy, trade, defense and the Indo-Pacific. The strategic rationale is unmistakable: the US needs India as an Asian counterweight to China and the Iran crisis has inflicted greater burdens on energy routes and India's crude oil supplies. Close to Washington and incurring risks from China, Japan has a stronger incentive in holding India in the Quad's economic-security matrix.

However, the significance of the Quad should not be overplayed. Investors do not build factories only after the foreign ministers of four nations have met. They do it after input costs, legal risk, demand, suppliers and exit options turn attractive. The Quad could help in important areas like critical minerals, semiconductors, clean energy, cybersecurity and maritime resilience. India and Japan have already chosen semiconductors, critical minerals, pharmaceuticals, clean energy and ICT to be their priority sectors and there is a program to refine rare-earth elements in Andhra Pradesh, open RAN pilots and NTT setting up a one-million-square-foot data center. These are commendable steps, but they will be of real significance only if they are backed up by orders, credit lines, buy-back insurance, land and labor and commitments to buy. Directions set in speeches must find manifestation in accords.

The criticism remains legitimate-the nation has been there before. It still has a shortage of modern infrastructure, a long battle against an ineffective judicial system, an unconducive tax structure and structural inadequacies of the state capacity. Its labour pool is large but many workers still need job-ready industrial skills. Its suppliers are improving but the cannot yet match China's depth in many sectors. These are the real obstacles and they require doing more to raise the bar of policy. They need not have every company exiting China, but may opt for companies with experience, suppliers' bazaar, higher expenditure systems and export discipline. Japanese and Korean investors are a special gift because of their strategic mindset and rational expectations from the Indian system can help meet the state capacity challenge and lead to more improvement if we do not count them as criticism but consider them as a change driver.

The call to action, then, is clear but not easy. India must build an investment state, surrounding the India investment pivot, that simplifies projects, develops its human capital, defends its contractual commitments, connects foreign anchors with local suppliers and measures performance by the extent of its production, not headline numbers. Japan and Korea should stop seeing India as just a hedge and instead begin to see it as a co-production hub. The US must use the Quad to mitigate some of the risk and avoid forcing an alignment in India that could be unmanageable politically. The ¥10 trillion figure opened the story. The real test is whether that money becomes factories, finance, skills and resilient supply chains. whether that amount of money actually turns into factories, financing, skills and resilient supply chains. If it does, then India will not replace China. It will accomplish something even more extraordinary – become the second industrial center India has been yearning for.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

AMRO (2025) ‘China Still an Attractive FDI Destination’, ASEAN+3 Macroeconomic Research Office, 26 May.

Asian News International (2026) ‘India-Japan reaffirm strength of ties, agree to advance bilateral ties’, Daily Prabhat/Dailyhunt, 4 May.

Chaudhury, D.R. (2026) ‘Japan to create special cell to push FDI into India’, The Economic Times, 31 March.

Department for Promotion of Industry and Internal Trade (2025) FDI Factsheet: June 2025. New Delhi: Government of India.

India Today Business Desk (2026) ‘Japan bets big on India with $68 billion investment target, tech push’, India Today, 22 May.

International Monetary Fund (2025) ‘IMF Executive Board Concludes 2025 Article IV Consultation with India’, IMF Press Release, 24 November.

Ji, K. and Jiao, Y. (2025) ‘China Still An Attractive FDI Destination’, ASEAN+3 Macroeconomic Research Office, 26 May.

Kaushik, K., Keohane, D. and Dempsey, H. (2026) ‘Japanese investment in Indian finance hits record as business ties tighten’, Financial Times, 22 March.

Martina, M., Brunnstrom, D., Lewis, S. and Hunnicutt, T. (2026) ‘Rubio touts US energy on India trip meant to repair ties’, Reuters, 23 May.

Ministry of Commerce and Industry, Government of India (2025) ‘2025 Year End Review for Department for Promotion of Industry and Internal Trade’, Press Information Bureau, 10 December.

Ministry of External Affairs, Government of India (2025) ‘Fact Sheet: India-Japan Economic Security Cooperation’, 29 August.

Ministry of External Affairs, Government of India (2026) ‘Quad Foreign Ministers’ Meeting’, 22 May.

National Bureau of Statistics of China (2025) ‘Average Annual Wages of Persons Employed in Urban Units in 2024’, 17 May.

Nishizawa, T. (2026) ‘Business, not politics, drives Japan–India investment ties’, East Asia Forum, 22 May.

Petersmann, S. and Ahmad, S. (2026) ‘US top diplomat Marco Rubio in India to renew strained ties’, Deutsche Welle, 24 May.

Shekhar, A. (2025) ‘Korean IPOs in India reflect global confidence in India’s capital markets’, Invest India, 10 November.

Tandon, K. and Pant, M. (2025) ‘Hyundai Motor doubles down on India with $5 billion investment’, Reuters, 15 October.

World Bank (2025) China Economic Update: Advancing Reforms, Enhancing Prospects. Washington, DC: World Bank.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.