Monetary Policy Spillovers Are a Balance-Sheet Problem, Not a Border Problem

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

US monetary policy does not hit the world evenly Its effects depend on inequality, financial openness, debt, and credit access Small central banks need balance-sheet strategies, not copycat rate moves

The target rate of the Federal Reserve increased from 0.25-0.50 percent in March 2022 to 5.25-5.50 percent in July 2023. In the space of just over fifteen months, the cost of dollar money was raised by more than five percentage points. That change did not land on a homogeneous world. It landed on floating exchange rates, on fixed pegs, on dollar credit, on weak banks and bond markets, on small firms and on wealthy households and cashless households, on countries with already little room to maneuver with fiscal policy. The monetary policy tightening spillover is often conceived of as a wave that breaks over borders. But that image doesn't fit. Better is the idea of a shock that ripples through balance sheets. It's a shock that hits hardest where debt is short-dated and finance is narrow, and currencies are mismatched. Less hard where markets are wide, buffers large, and trust in the central bank is credibly high. The policy challenge isn't whether megadomains of the economy are sending out spillovers; they do. The challenge is to whom do they spill and who is helpless?

Monetary Policy Spillovers Start at Home

The first error is to assume that a policy rate hits everyone the same way. The same decision in the same currency area can have disparate credit effects. The ECB increased its rate by 450 basis points from July 2022 to September 2023 and then reversed that by 200 basis points from June 2024 to June 2025. Still, the easing did not "trickle" through the economy. Demand for mortgage credit picked up when interest rates fell, but corporate credit remained subdued relative to historic tendencies. Manufacturing, which often requires working capital and has high fixed costs, remained more sensitive to credit than many service industries. Larger and less risky firms had an easier time accessing credit than smaller and more risky firms. It is for this reason that monetary policy spillovers resound: the central bank sets the "price" of money, but the market allocates access.

This is important since the euro area is not an aggregation of a set of disjointed economies. It is a single-currency area with one central bank and one interest rate. If monetary transmission is still uneven there, it will be naïve to expect smooth monetary transmission globally from the US. The euro example shows heterogeneity is nothing new but rather the norm in modern finance. Mortgage contracts, banks and local saving behavior are all quite different. Firms use bank lending, bonds, or self-generated cash to widely varying extents. A rate cut may be an important boost to a household with its first mortgage, yet induce a modest effect on a small, if promising, new enterprise. A rate hike might restrain demand in one region, affect cash flow in another. Logic only returns more firmly when the shock crosses the border.

The broad policy lesson is this: monetary spillovers filtered through institutions before they reach the people. Credit registries, bank capital, loan maturity, mortgage design and insolvency rules all determine the magnitude. So do fiscal buffers and macroprudential regulations. A country with long fixed-rate mortgages, sound banks and a credible inflation target can endure more exchange-rate shocks without triggering a credit panic. A country with short-term debt, weaker banks and more foreign-currency borrowing will have less cushion: it may have to raise domestic interest rates even when economic growth is sluggish, to defend the internal equilibrium and access to foreign capital. That is not failure by governors, only the fee for confronting a global shock with a fragile domestic economy.

The Dollar Turns Local Weakness Into Global Pressure

The dollar offers US policy unprecedented reach. The stock of dollar-denominated credit to non-US residents outside the US stood at $14 trillion at the end of end-Q3 2025. Slightly over half was in debt securities rather than bank credit. Dollar-denominated credit to emerging and developing countries amounted to slightly over $4 trillion. These figures are significant because they provide evidence that monetary policy spill-overs are no longer confined to trade or exchange rates; they are transmitted through balance sheets denominated in dollars but repaid with income earned in currencies other than the dollar. When dollar rates rise, the impact is not hypothetical; the effect manifests in debt-service requirements, refinancing risks, reserve losses and stagnation of private investment. For companies operating on narrow margins, the impact can be felt a long time before any dip can be observed in sales.

And this is also why the same US move can look very different in two countries with similar headline inflation numbers. In a country with low dollar debt, deep, liquid domestic bond markets and anchored expectations, the dose of dollar appreciation can be painful but not crushing. In a country where firms issue dollar-denominated liabilities and sell in local currency, that dose of dollar appreciation can turn into a solvency shock. The exchange rate depreciates, the dollar denomination of debt burdens spirals up: banks become risk-averse and the monetary authority is caught in a trap. Cutting rates could support output but aggravate capital outflows. Hiking could defend the exchange rate but deepen the recession. That is the real face of spillovers. The damage is not spreading by its geographic distance from Washington but by its degree of exposure.

Debt data make it hard to deny. Developing countries paid an additional $741 billion in principal and interest on external debt than they received in new debt flows – the largest such deficit in at least 50 years. In 2024 alone, they paid a record $415 billion in interest. Bond markets reopened for some borrowers but often at around 10 percent – close to twice pre-2020 levels. These numbers are not only the story of bad fiscal discipline. They are also about a global system in which the largest of central banks can change the cost of borrowing for countries that did not create the original shock. The result is a quiet transfer of policy burden from core economies to weaker international balance sheets.

Resilience Is Built Before the Shock Arrives

There is one common rebuttal to this argument. It says that spillover talk is just an excuse for weak domestic policy. That rebuttal contains a caution but misses the point of the larger story. Poor fiscal policy, lax credit regulation and weak central bank policy credibility do make countries more vulnerable. But vulnerability is not destiny. Recent experience from emerging markets suggests that when countries adopt better policy regimes, spillover vulnerability can give way to greater resilience. Improved inflation targeting, sounder fiscal rules and greater macroprudential regulation have enabled many countries to face risk-off "shocks" with less output loss and less inflationary overshoot than in earlier episodes. Good policy does not eliminate the effects of monetary policy spillovers. It alters their character. It can convert a destabilizing "sudden stop" into a hard adjustment but not a crisis.

The difference is big enough to matter. In recent IMF analysis, better policies and institutions translated into about 0.5 percentage point higher growth and 0.6 percentage point lower inflation during typical risk-off episodes after the global financial crisis compared to earlier episodes. Model simulations underlined that a good framework can help a country with significant currency depreciation to lose less output. The moral of the story is not that emerging markets are now safe, but that strengthened institutional quality has been a new shock absorber. Countries that develop credibility before the crisis can maneuver over potential trade-offs. Countries that wait until the market receives the blow often will find that all their instruments have become more costly. Every delay increases the real accumulation of external shocks, which have strong and lasting effects on their economies in the end.

This calls for a can-do agenda. Finally, central banks in small and mid-sized economies should not copy the Fed or even the ECB but instead specialize in mapping out the pipes through which the Fed and the ECB are likely to affect them. This map should specify big foreign-currency debt holders by sector, the proportion of their debt with short-term maturities, banks’ open position in foreign currency, import dependence, census-identified mortgage reset dates and the proportion of firms that depend on rolling credits. Which banks will run out of lending first if others pull back? This is not about forecasting all Washington's or Frankfurt’s moves, but about knowing which domestic pipes will burst should the global pressure increase and only then can spillovers be managed. This is, of course, elementary risk work, rather than forward-looking stylized models.

But too much relies on the policy rate. Foreign-exchange intervention can buy time but not credibility. Macroprudential buffers can slow credit booms before they turn into dollar debt traps. Instruments to manage capital flows can be useful in niche situations, but they cannot fix broken banks. Fiscal policy can shield investment against a credit crunch when the central bank must remain tight. Debt managers can extend maturities before the market disappears. Supervisors can constrain currency mismatches before they become costly. The point is that these measures are not extraordinary. That is why they are effective: they turn policy from an emergency response into balance-sheet architecture. In an unpredictable world, this 'architecture' of monetary sovereignty is also a cost-effective one, as it can be designed and back- tested.

Monetary Policy Spillovers Need a New Policy Compact

Large central banks lack the capacity to conduct policy for the rest of the world. The Fed has a domestic mandate; the ECB, a euro-area mandate. This argument is valid and it cannot be brushed aside. But it does not settle the argument. Domestic mandates need not also imply strategic myopia. Scope for a policy shift in a core country currency area by itself moves the scale of global credit, exchange rate and debt-service effects into the spillover calculus. Spillovers shape trade, financial stability, migration pressures, commodity markets and ultimately the core countries-and they should shape it too. A limited mandate can coexist with a broad horizon. But the analysis of global effects is neither pity nor public service. It is self-protection. Foreign transmission should therefore be recognized as a fixed boundary condition.

The better answer is a new policy compact. Large reserve-currency central banks should issue more transparent spill-over analysis when interest rate changes are sharp, or balance sheet tools are being used. Smaller ones should stop viewing exchange rate pressure as a temporary market sentiment and start viewing it as a test of local credit arrangements. International institutions should make foreign currency debt, credit maturity and borrower level exposures cornerstones of their oversight, not secondary items. Development banks should assist countries in closing off mismatches and setting up local currency markets in the run-up to the next tightening cycle. This is not a plea for one global interest rate. It is a plea for honest accounting of which party takes what risk with moves in dominant currencies. The burden is shared, but it is not shared equally. The broadest issuers of reserve currencies have the broadest obligation to explain.

The final worry is that worrying too much about spillovers may undermine the efforts to fight inflation. The opposite is more plausible. Spillover awareness can enhance stability by lowering the likelihood of irrational reactions. The central bank, which is well aware that its measure of foreign-currency debt is woefully inadequate, can tighten more carefully. The finance ministry that knows its refinancing wall is less likely to impose a sudden austerity shock. The regulator that discerns relative credit thickness risks is less likely to wait until small firms are driven from the economy. Spillovers in monetary policy are most damaging, after all, only if their existence is denied until markets impose a painful adjustment. They are less damaging, after all, if they are recognized, described and factored into policies before the adjustment is public knowledge. The aim, after all, is not to make monetary policy easier. It is to make transmission more assured with fewer mistakes.

The start was not just a US story. It was a stress test of the global financial system. A five-percentage point correction in the dollar payoff would reveal cracks in the global financial fabric, its kindred credit-geography and the world's credit architecture. Some breathe a little. Some broke. The differences varied little with geography, but right sheet, hard monetary policy trust, debt geography and effectiveness of regulation. Tomorrow's shock could emanate from the Fed, the ECB, China, energy markets or a sudden shift in risk appetite,or a swing in risk appetite. The source will not matter much. Importantly, it will not matter at all beyond channels and transmission. All economies should be prepared for this new financial world, so far uncharted. That, not financial market stability, is where monetary sovereignty must now begin and it must begin before the dust has settled, not after.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

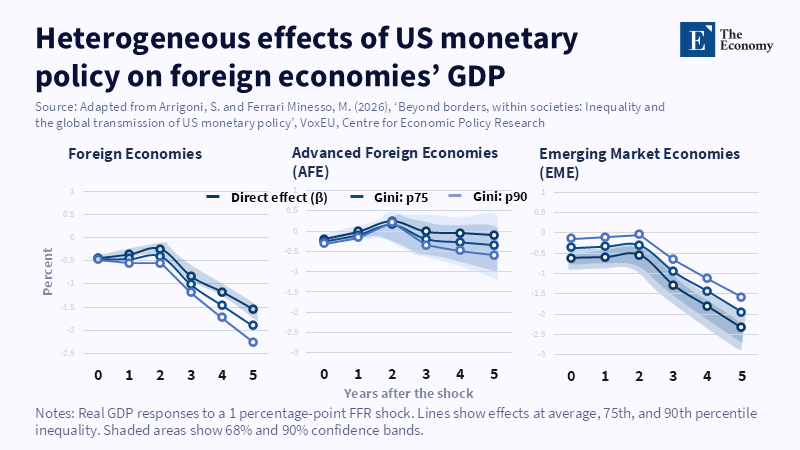

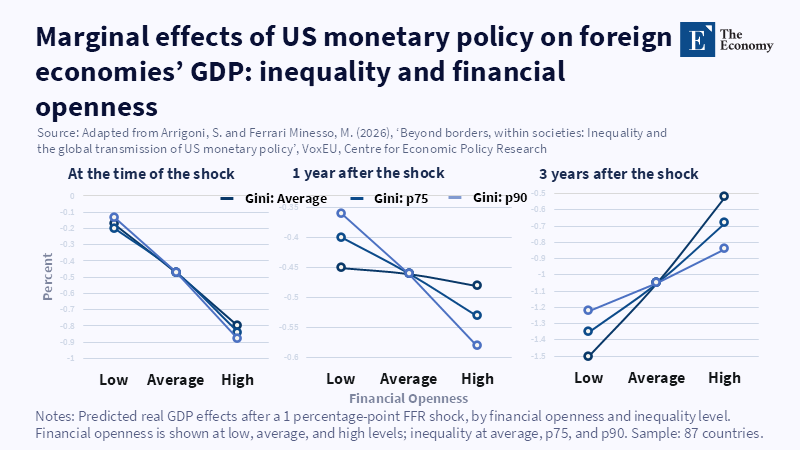

Arrigoni, S. and Ferrari Minesso, M. (2026) ‘Beyond borders, within societies: Inequality and the global transmission of US monetary policy’, VoxEU, Centre for Economic Policy Research, 23 May.

Bank for International Settlements (2026) ‘BIS global liquidity indicators at end-September 2025’, BIS Statistics, 29 January.

Board of Governors of the Federal Reserve System (2022) ‘Federal Reserve issues FOMC statement’, 16 March.

Board of Governors of the Federal Reserve System (2023) ‘Federal Reserve issues FOMC statement’, 26 July.

Bruno, V. and Shin, H.S. (2015) ‘Capital flows and the risk-taking channel of monetary policy’, Journal of Monetary Economics, 71, pp. 119–132.

International Monetary Fund (2025) ‘Emerging market resilience: Good luck or good policies?’, World Economic Outlook, October 2025, Chapter 2.

Lane, P.R. (2025) ‘The transmission of monetary policy: Financial conditions and credit dynamics’, welcome address at the 5th WE_ARE_IN Macroeconomics and Finance Conference, European Central Bank, Frankfurt am Main, 21 October.

Miranda-Agrippino, S. and Rey, H. (2020) ‘US monetary policy and the global financial cycle’, The Review of Economic Studies, 87(6), pp. 2754–2776.

World Bank (2025) International Debt Report 2025. Washington, DC: World Bank.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.