EU China Dependency Is No Longer Cheap Trade

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Cheap trade became leverage China dominates key EU supply chains Europe needs de-risking, not isolation

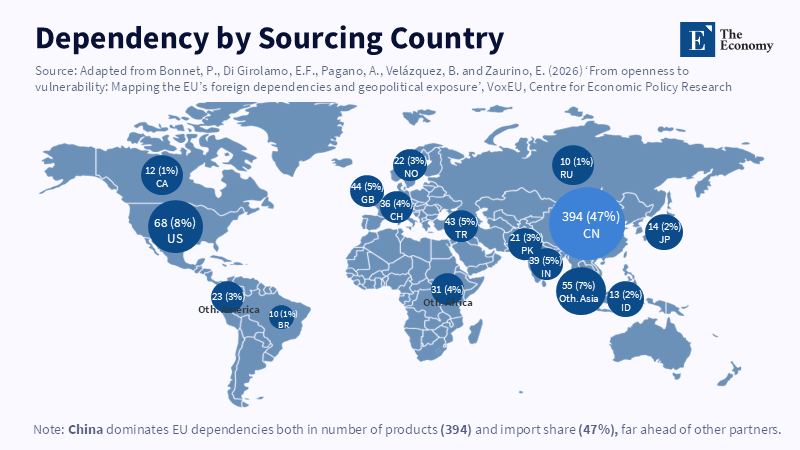

The warning is no longer buried in a policy paper. In 2025, the EU sold into China around 199.5 billion worth of goods and imported around 559.5 billion worth of them. That left the trade deficit of roughly 360 billion. It also made China the EU's largest source of goods imports. That is not simply an enormous trade deficit. That is a blueprint for power. EU dependency on China now passes through factory inputs, solar panels, batteries, rare earths, electric cars, and the myriad parts that lubricate modern industry. Low prices, a boon to consumers and firms, have also conditioned Europe to treat cheap supply as if it were secure supply. That error is now unacceptably expensive. When one state can influence prices, cause delays, flood markets, or impose punishments on fellow members, openness is no longer just an economic virtue but a security peril.

EU-China Dependency Has Changed the Meaning of Openness

For years, Europe treated trade with China as a practical bargain. China would be competitive in production; Europeans would buy cheap imports. Firms will access the inputs; consumers- the decent goods; greener transition- faster- come on stream. That deal made sense when the key issue was cost. It looks more shaky when the key issue is control. EU's reliance on China isn't typical of trade. Free trade mitigates risk by spreading it over many suppliers. A strategic reliance concentrates risk within a single political order and provides that firms and consumers, in the case of a crisis, 'trust' that order.

The fundamental policy question is not whether Europe should wall itself off. It should not. A rich and open bloc cannot base prosperity on fear. The question is whether openness can survive without insurance. But comparative advantage fares well when markets are contestable, when contracts are durable, and when shocks are largely commercial. Comparative advantage fares less well when a dominant supplier has state direction, excess capacity, and a track record of using access for political ends. Europe's mistake was not trading with China but replacing strategy with trade.

The US has taken a harsher route. It has imposed high tariffs, ending with direct barriers, to break with the Chinese supply chains. This may encourage domestic production, but also at the cost of higher prices. A clear illustration of the blunt cost of the US decision to ramp up tariffs can be gained by looking into recent tariff estimates performed in the US: as tariffs ramp up, households end up paying for the toll in higher prices and producers in more costly inputs. While Europe is right not to pilot such a policy in full, doing nothing is not cheaper: it simply postpones the toll from today's cost to tomorrow's crisis.

The Alarm Came When Cheap Supply Became Leverage

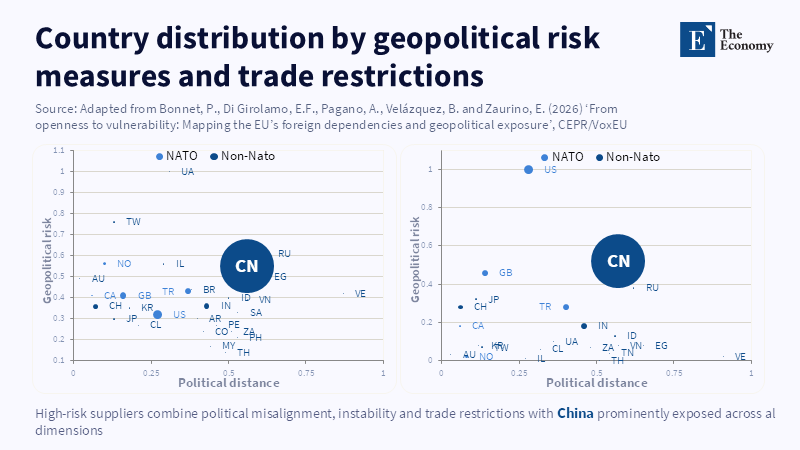

Europe's alarm was not delivered by a single event. China did not turn into the workshop of the world in one instant; its ascent had been produced over the course of decades on the basis of its scale, finance, industrial policy, local learning, and huge home market. The shock was seeing this power wielded in ways that markets can simply not correct. The lesson from Lithuania was harsh. Following a dispute over Taiwan's representation, Beijing sought to intimidate Lithuanian exports with directives and taxes and sent a warning to EU products with Lithuanian component parts. This shows that a small member state can be bullied through the supply chains of much larger firms.

The second concern was around critical materials and rare earths. These are no luxury items. They are the components of electric cars, wind turbines, chips, military systems, industrial motors, and grid equipment. The trouble came when China unleashed restrictions on a handful of heavy rare earths and associated magnets in 2025; it became impossible for automotive producers in Europe and across the world to buy permanent magnets. Some companies reduced or even halted activity. Prices outside China soared. The lesson is clear. A dependence is not dangerous when there is no supply. It is dangerous when the fear of delay influences the choices well before any formal trade blockade begins.

Hence, the importance of silent coercion. A government does not always have to threaten to induce compliance; on occasions, it can cause compliance because firms have assessed that a certain policy decision poses the danger of endangering some permits, components, or market access, and have mobilized to prevent that outcome. This is how the integration and dependency between the EU and China can become part of the domestic politics in Europe without the need for a public order to be taken or commanded by Beijing. The pressure is very indirect and is provided by procurement offices, exporters, vehicle assemblers, electricity users, ports, and jobs. Europe begins to impose sanctions on its own choices, not by its agreement with China, but simply because of the fear of the cost of non-compliance.

This will be criticized by arguing that this makes any trade flow a threat. It is too easy an answer. It is not imports that are hurting. What is hurting is highly concentrated imports in sectors that cannot wait. Missing out on a toy is annoying. Missing semiconductors, rare earth magnets, can hold up cars, drones, radar systems, robotics, and wind power. Missing solar panels can drive up energy costs. Missing chemicals can halt a factory 10,000km away from the original supplier. Strategic trade politics then has to look at a narrow question: what foods can Europe replace during a crisis, and which foods can hold Europe back from action?

EU-China Dependency Now Runs Through the Green Transition

The most delicate element of this thesis is that China has, in a number of aspects, reduced the costs of certain green transitions. Solar power is the most conspicuous example. China accounts for more than 80% in the world in each of the various steps involved in the main stages of solar panel manufacturing. In 2024, 98% of extra-EU import trends in solar panels came from China. This has accelerated Europe's deployment of clean energy more economically. It also introduced a different typology of energy risk. While Europe navigated several decades away from its reliance on fossil fuels, it should not trade that for another clean-tech variant potentially susceptible to other kinds of risk.

The same squeeze has hit batteries, EVs, and minerals. Lithium demand jumped nearly 30 percent in 2024. Demand for nickel, cobalt, graphite, and rare earths also increased. The clean economy is material-intensive. It requires mines, refineries, processors, magnets, cells, inverters, software, and ports. But refining is also becoming increasingly concentrated. For almost all key energy minerals, the 3 top refining nations gained share on average from 2020 to 2024, and most of that increase came from a single dominant supplier. This dominant supplier is China for both graphite and rare earths.

But this does not mean that Europe should slow down on climate measures. It means that climate policy should stop tokenizing supply chains. A cheap solar panel is not cheap if it kills the last existing domestic producer, drives reliance back up to near 100 percent, and leaves the system exposed to a potential future licensing shock. A cheap EV is not simply a car, but a message about batteries, the code, data, subsidies, and the fate of Europe's auto heritage. Hence, the significance of the EU's countervailing duty on Chinese battery electric vehicles. They are not an overall policy. They are a symbol that Europe has ultimately joined the dots between climate, industry, and strategic autonomy.

Another case of unfairness. If Chinese output is subsidized through WTO rules or simply through the state bureaucracy, some show to be propped up by massive state support, cheap credit, land policies, cheap energy prices and directed demand, then European firms are not just losing because they are not efficient. They are losing because they are not playing by the rules. Open trade can absorb vigorous competition; it cannot sustain a downward subsidy rivalry that is protected by the fiction that all prices are market prices. State-subsidized excess supplies may seem to make a large number of consumers happy at first, but as rivals depart the scene, the consumer finds himself less well served. He's experiencing monopoly market power.

Europe Needs De-Risking Without Panic

The EU has begun to take steps. The Critical Raw Materials Act targets the production, processing, recycling, and diversification of strategic raw materials by 2030. At no more than 65% of its annual consumption should a EU strategic raw material come from a third country. The Net-Zero Industry Act seeks to have half to two-thirds of the industrial capacity in strategic clean technologies in the member states meet roughly 40% of the annually deployed demand by 2030. The Anti-Coercion Instrument gives the bloc a tool to react, as a bloc, when a third country attempts to coerce the decision-making of the Union or the single member states by trade and investment.

These steps are needed, but not sufficient. Europe is still lagging because its approach is based on markets, consensus, and rules. China's way can be much faster because it combines state finance, industrial plans, and power. The solution does not lie in copying China. It lies in rectifying the illusion on the time scale of industrial strength. A mine takes years to develop. A refinery can take years to set up. What about a new magnet plant? It needs skills, licenses, power, and customers. When Europe then hits the next crisis, it will find that emergency policy once again cannot fill the gaps left by yesterday's lack of industrial capacity.

A more intelligent policy would be selective and dull from the start. It would register not only imports but also tier-two and tier-three suppliers. It would impose diversification requirements on stuff crucial to production, but not everything that is traded. It would use the purchasing power of the state to generate European and allied demand in segments where security is central. It would even buy up a few minerals itself; however, it would know that synthetic stockpiles cannot be a substitute for domestic production. It would incentivize recycling, substitution, and material-efficient design. And it would require firms to reveal single-country exposures in critical supply chains, because undisclosed reliance is a nightmare for rational security planning.

Cost is by far the biggest objection. Diversification will push some prices up. Home-produced clean-tech could cost more than sourcing from China. Certain firms will object that rules create inflexibility. These fears are not illusory. But they are not final. The essence of insurance is that it costs before the fire. Europe should not slap tariffs on everything or subsidize all the uncompetitive companies. It should pay for resilience where the consequences of failure impose costs that firms ignore. The market price of a magnet does not include the cost of one’s factory grinding to a halt, of a delay in a defense project, let alone vetoing a foreign-policy move.

Europe must also make a political pact with its citizens. Leaders cannot defend a resilience premium as a free lunch. It will impose costs in the here and now. It may cost jobs and raise costs in some areas. Yet a resilient Europe should also mean better jobs, more secure supplies, greater negotiating leverage and a clean transition that no single supplier can conveniently hijack. This is about freedom of action, not autarky. A resilient, secure Europe must also be a Europe that can hold the line when it has to.

The opening figure should disturb policymakers because it reveals scale, not fate. A 360 billion Chinese goods deficit does not indicate the end of the story for Europe. Instead, it indicates that Europe has set up a system where cheap supply has gone ahead of strategic thinking. The next move is not a tariff wall; it is a dependency test for any industry that intersects with energy, defense, health, information networks, water systems, transport networks, and core manufacturing. Where Chinese supply is cost-effective and practicable, trade can flourish. Where Chinese supply is dominant and coercive destructive, Europe is going to have to broaden its choices, expand its production, and insulate its risks. Comparative advantage is useful for a snapshot.. Security takes time to accrue. Europe has learned this lesson belatedly. It should not have to learn it twice.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bonnet, P., Di Girolamo, E.F., Pagano, A., Velázquez, B. and Zaurino, E. (2026) ‘From openness to vulnerability: Mapping the EU’s foreign dependencies and geopolitical exposure’, VoxEU, Centre for Economic Policy Research, 23 May.

Clausing, K. and Lovely, M.E. (2025) ‘Trump’s tariffs on Canada, Mexico, and China would cost the typical US household over $1,200 a year’, Peterson Institute for International Economics, 3 February.

European Commission (2024) ‘EU Commission imposes countervailing duties on imports of battery electric vehicles (BEVs) from China’, Access2Markets, 12 December.

European Commission (2025) ‘European Critical Raw Materials Act’, European Commission.

European Commission (2025) ‘Net-Zero Industry Act’, European Commission.

European Commission (2025) ‘Protecting against coercion’, Directorate-General for Trade and Economic Security.

Eurostat (2025) ‘International trade in products related to green energy’, Statistics Explained.

Eurostat (2026) ‘Trade in goods with China in 2025’, Eurostat News, 10 April.

Gehrke, T. (2026) ‘How China’s silent coercion has Europe sanctioning itself’, European Council on Foreign Relations, 21 May.

International Energy Agency (2022) Solar PV Global Supply Chains. Paris: International Energy Agency.

International Energy Agency (2025) Global Critical Minerals Outlook 2025. Paris: International Energy Agency.

Israel, K.-F. (2025) ‘Europe’s strategic dependence on China: The next energy crisis?’, GIS Reports, 10 December.

Page, F. (2026) ‘EU aims to upend China dependency with new supply chain quotas’, Kharon, 20 May.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.