From Liberalization to Governed Coexistence: China, Subsidies, and the Reordering of the World Trade System

Published

1 The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

2 Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

This article contends that the current trade crisis should not be read as the end of globalization, but as the end of a long period of institutional evasion in the rules-based trading order. The fundamental challenge is no longer the reintroduction of tariffs or a bilateral US-China trade conflict, but a structural transition in which China has moved from cost-driven manufacturing to technologically sophisticated, strategically critical sectors where subsidy, scale, finance, standards and export capacity have systemic effects. The article explores how China's industrial rise has unsettled Western economies, especially as the focus of the competition has moved into strategic sectors such as electric vehicles, solar technology, steel, semiconductors, critical minerals and technical standards. The article also shows how the US and the EU have undermined their own liberal-trade position through subsidy competition, tariff escalation, foreign-investment screening and industrial policy activism. The disorder cannot be remedied through unilateral Western pressure or Chinese claims to free-trade treatment while continuing to direct excessive subsidies toward mature, globally competitive sectors. A constructive resolution of this crisis demands reciprocal realisms: China must rein in subsidies, provide greater transparency and rebalance growth toward domestic demand and the US and the EU must embrace China as a long-term enforcer of the rule-book. The paper concludes that the worst-case scenario of divisive fragmentation can be avoided if governments define a coherent framework of governed coexistence premised on WTO-consistent disciplines, subsidy transparency, plurilateral agreements, reinforced dispute procedures and sector-specific restraint.

1. Introduction - The Trade Order After the Tariff Shock

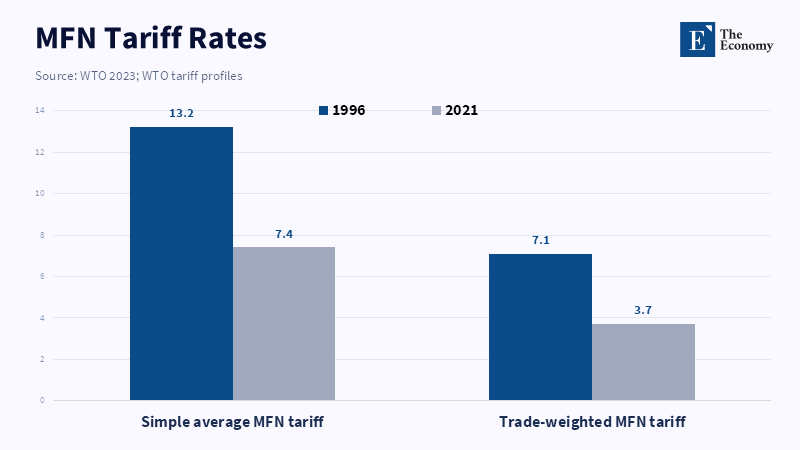

The easiest way to misrepresent the present trade order is to characterize it as the death of free trade. This diagnosis is appealing since the observable evidence seems to lend weight to it. The WTO reports that, since the mid-1990s, measures within the multilateral trading system have been instrumental in a protracted decline in mean tariffs, with simple average MFN tariffs applied by WTO members falling from 13.2 percent in 1996 to 7.4 percent in 2021 and trade-weighted MFN average tariffs falling from 7.1 percent to 3.7 percent.[1] Much of that liberalization took place in the ten years following the conclusion of the Uruguay Round Agreement and the establishment of the WTO, when WTO members halved the percentage of applied MFN tariffs that had been applied by WTO members in the decade following the Uruguay Round and Marrakesh Agreement. Against this background, the escalation of tariffs, subsidy conflicts, anti-dumping actions, export restrictions and investment screening appears ominous.[2] However, a more nuanced analysis suggests that it is not that trade liberalization has ceased, but rather that the institutional arrangement which allowed the late twentieth-century trading order to prosper has unraveled under the pressure of security politics, subsidy competition and the ascension of China as an institutionalized industrial state.

That level of breakdown is no longer just anecdotal. The WTO's recent trade-monitoring report cites the value of global goods imports affected by new tariffs and other import-restrictive measures expanding more than fourfold between mid-October 2024 and mid-October 2025, compared to the past twelve months, the highest coverage in more than fifteen years of monitoring.[3] Global Trade Alert echoes this, indicating that the overall share of trade interventions by G20 countries during 2025 was catching up with 2023 and 2024, with tariff moves reappearing as a serious barrier, along with the subsidy activism of a broader period.[4] But it is not only the number that counts. The nature of the intervention has evolved. Today's trade conflict is less about traditional border controls and more about the blend of tariffs, state industrial support, export restrictions, standards, procurement rules and restrictions on foreign investment, often justified through the language of security and strategic autonomy.

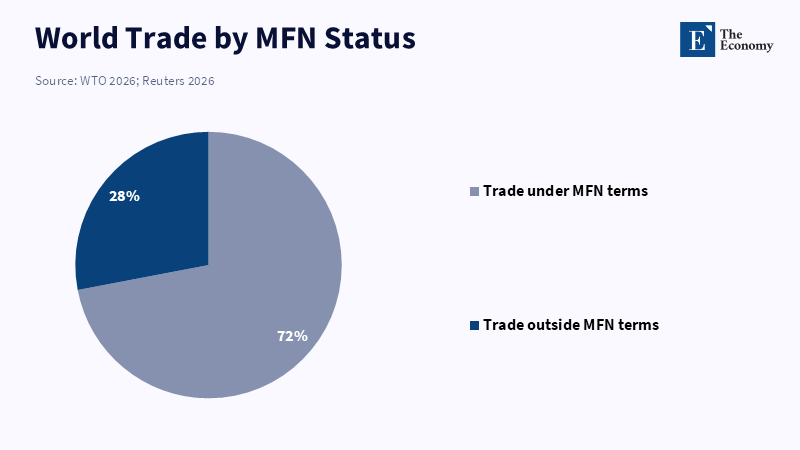

At the same time, the trading system has not yet given way to autarky. The WTO's March 2026 projections suggest that world merchandise trade volume grew by 4.6 percent in 2025, well above the October 2025 prediction, because AI-related demand and trade diversion countered some of the tariff ramifications.[5] That resilience is genuine, but it should not be romanticized. The same WTO report expressed that trade policy uncertainty remains historically high and only 72 percent of world trade is now conducted on MFN terms because of the policy upheavals of 2025.[6] Neither is the legal core of the system intact: the WTO Appellate Body still cannot hear appeals because its vacant seats have not been filled since late 2019, demanding that willing members use the provisional MPIA method rather than the universal dispute-settlement system the WTO was designed to make available.[7] The system still moves goods, but it no longer reliably organizes expectations.

And this is exactly why the conventional story is far too narrow. It is not a question of whether the US, China, or Europe is "protectionist" in an abstract sense. The real question – and the one that explains why these three actors now act so differently, from so very different vantage points and with very different consequences for the rest of the world – is rather this: why do China, the US and Europe now all deploy trade and industrial policy in pursuit of global strategic sectors, but under such radically different conditions of influence, with certain effects "spilling over" unevenly across the world? And why has this conflict become so pronounced ever since the shift whereby China has morphed into a scale rival in electric cars, batteries, solar equipment, semiconductors, wind tech, critical minerals, logistics in e-commerce and increasingly in the technical standards that future markets hinge upon? Once an emerging economy’s industrial ascent moves from low-technology, price-based competition to high-technology, ecosystem competition, what had once seemed (to advanced economies) "normal trade" increasingly came to represent a challenge to their own industrial, then to labor and finally to strategic sovereignty.

The central argument is even more ambitious. The current disorder is not just induced by Western hypocrisy, although such hypocrisy is real, nor is it induced solely by the activism of the Chinese state, although this activism is, of course, unavoidable. It is induced by a transition that the world trading order has not yet completed. The United States and Europe internalized that China is simply too big, too technologically advanced and too institutionalized to be treated as just another coming manufacturing power. China, on its part, has had to realize that the catch-up industrialization that created its manufacturing preeminence is politically combustible when adopted by globally dominant firms in already consolidated sectors. The main question is therefore transitional: a rising power is exhibiting the behaviors of a latecomer, while the incumbent powers are responding by abandoning many of the liberal precepts they used to believe in.

Developments in 2025–2026 added even greater urgency to that reframing. While the second Trump term instituted a record-setting pace of tariff hikes, according to the Yale Budget Lab its effective tariff rate averaged 17.5 percent in January 2026 among the major industrial economies (the highest since the early 1930s)-Washington and Beijing both indicated that indefinite tariff escalation is damaging:[8] after their May 2026 summit, the two sides showed signs of a limited tariff rollback on agricultural products and of establishing a process for rapid identification of non-strategic goods for tariff relief, even while maintaining strategic restrictions on others. The point is not that free trade has entered a new golden age. Each great power is being forced to relearn, in the balance of power, that a general tariff war is economically costly and blunt and that narrow de-escalation is mutually beneficial. This recognition has already created a path to move beyond today’s stalemate in some way. But the worst-case outcome of a stalemate can only be avoided if today’s painful deal is expanded into a public bargain. China must slow its excess subsidies to strategic sectors, while the United States and Europe build the framework within which China's role as a rule-shaper, rather than a pariah, is accepted.

2. China’s Shift from Low-Cost Manufacturing to Strategic Industrial Power

None of the Western irritation with China over trade emerged because Chinese exporters were adept, driven, or numerous. For decades, advanced economies put up with - and in many ISIC sectors gained from - China as a low-cost producer of manufactured products. The world political economy shifted when China shifted from being a low-cost producer of labor-intensive, low-technology goods, to providing a host of general-purpose technologies for which scale, state finance and state coordination can change world competitiveness. OECD data tells us that, during the 2005-2023 period, the five most subsidized industrial sectors vis-à-vis firm revenues were: solar cells and modules, semiconductors, aluminum, shipbuilding and steel.[9] None of those are fringe sectors. They are systems industries with heavy spillovers into energy, transportation, defense, machinery and digital infrastructure.

Chinese firms in those sectors received subsidy support, relative to their revenues, that over the period was between four and eight times the subsidy support that firms in the rest of the world received,[10] at the same time, while below-market borrowings increased from USD 22 billion in 2020 to in excess of USD 46 billion in 2023.[11] The central issue is not simply import competition, but import competition supported by a financial architecture that temporarily depresses capital costs for Chinese firms in sectors where scale and learning can rapidly foreclose rivals.

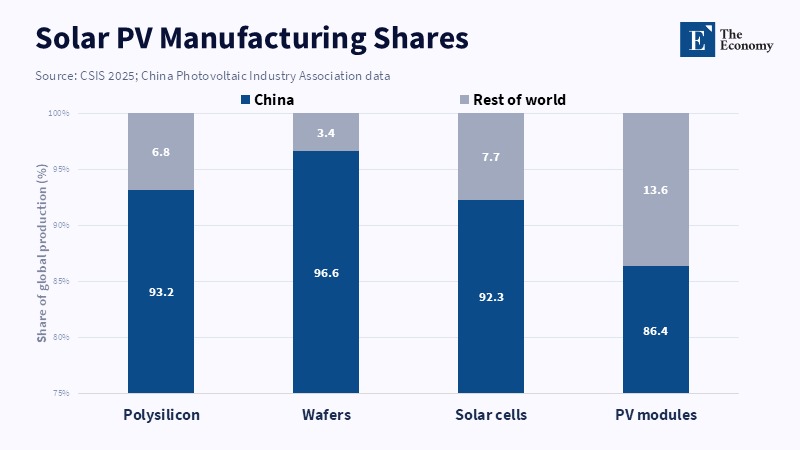

This becomes evident when one takes sectoral dominance into account. China's dominance in solar manufacturing is now pronounced. CSIS, citing China Photovoltaic Industry Association data, notes that in 2024, China is responsible for 93.2%, 96.6%, 92.3%, 86.4% of global production of polysilicon, wafers, solar cells and PV modules, respectively.[12] REN21 also reports that China is responsible for approximately 80% of the installed capacity of the PV value chain and that it produces almost 630 GW of modules in 2024,[13] which nearly doubles its annual domestic deployment, dominated by periods of excess supply. This is significant as it illustrates the mechanism by which domestic subsidy, cheap finance, economies of scale and weak firm exit interact. At this level of industry concentration, complaints from other countries are no longer just about "unfair trade" in the narrow legal sense. But about the spatial concentration of industrial ecosystems, the tenuousness of entry barriers and the political salience of being able to maintain domestic capacities in allied economies.

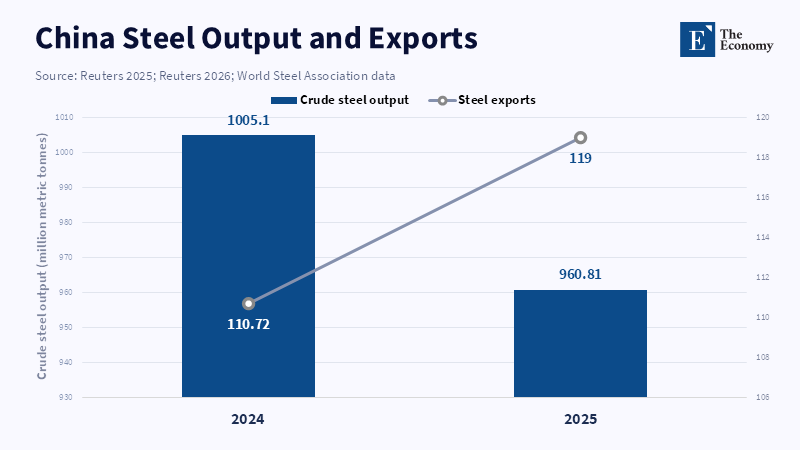

This same dynamic now applies to a wide range of other products and industries, indeed, well beyond solar. For steel, the OECD estimates that global excess capacity could reach 721 million MT by 2027;[14] Chinese steel subsidisation rates are estimated to be ten times those of OECD countries;[15] China's steel exports have more than doubled since 2020, setting a new record of 118 million MT in 2024;[16] and planned capacity additions between 2025 and 2027 total 165 million MT, predominantly in Asia, with China and India the key contributors. China, in particular, has been a major source of cross-border investment related to new capacity. But we are not operating in a normal competitive cycle, in which more efficient firms displace less efficient ones; the current environment is policy-aligned where subsidization and state guidance can support production for the long term, beyond where it would normally go and where the cost of adjustment is exported to foreign producers, who then respond to this challenge by imposing safeguards.

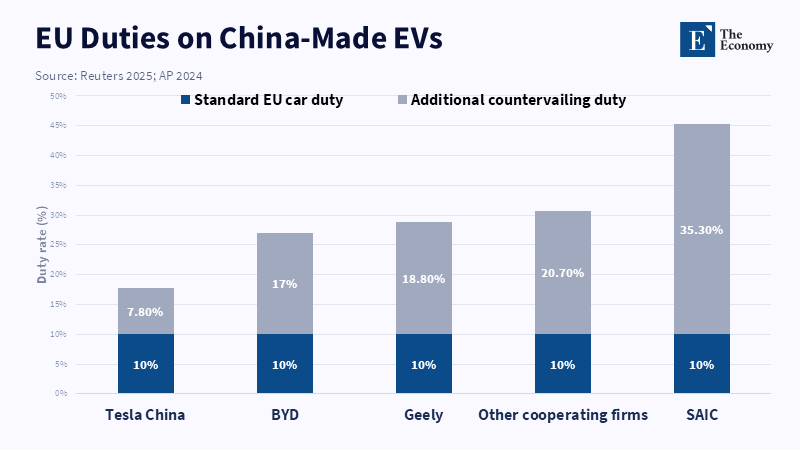

Electric vehicles pushed this friction into the political mainstream because they made something that had already occurred in less consumer-facing sectors more visible: what the EU complained about in the anti-subsidy case, the market share of Chinese EVs sold in the EU increased to 8 percent-up from less than 1 percent-and was expected to increase at a rapid clip for the foreseeable future,[17] as Brussels imposed definitive countervailing duties in October 2024, ranging up to 35.3 percent for some producers.[18] Reuters reported in early 2026 that Chinese automakers had already doubled their share of the European market to 6 percent in 2025,[19] despite these measures and as of April 2026, Chinese brands still enjoyed triple-digit registration growth in the main European countries.[20] European concern, then, is not only the cheaper imports but whether climate policies, consumer subsidies and the transition away from combustion engines will generate the market for a new strategic reliance on Chinese-produced green technology.

It would nonetheless be analytically careless to explain China's competitiveness solely through subsidies. One of the most compelling counterarguments-and one that deserves to be taken seriously-is that in fact the Chinese firms are often inherently more efficient: being larger-scale businesses, more integrated, less burdened by overhead and innovating in far larger markets than anywhere else in the world. Rhodium Group's 2026 study of EV cost competition makes this argument just as well: that state support in China is relevant, but only explains part of the cost differential between BYD and Tesla in China,[21] as the robust economics of its scale, vertical integration and lower operating costs do the most work. If policy thinking focused dogmatically on subsidy stories, Western policy anxiety would be unwarranted because Chinese success is artificial. Policy should therefore focus on actual productive advantages that supplement state support, opaque finance and standard-setting aspirations to magnify market distortion and intensify strategic anxiety.

That synthesis of real ability and state support is also palpable in China’s strategy for overseas expansion. Chinese mining businesses have stepped up their foreign acquisitions:[22] according to Reuters and other sources, citing S&P Global and Mergermarket data, there has been a dramatic rise in major foreign deals in mining (seven in 2025 compared with four in 2024); and according to the Griffith Asia Institute, Chinese investing into overseas mining during 2025 hit a record of USD 22.1 billion.[23] This expansion is especially controversial because it involves resource control that affects batteries, electronics, renewable-power installations and defense-related technology; all the more so since China's strategic motivation once business acquisitions, standards-building and subsidized manufacturing are understood as part of the same strategic whole. Western policy-makers perceive the Chinese overseas expansion not as the natural extension of comparative advantage, but as a project to sustain ecosystem dominance.

China has also begun to shift more openly from manufacturing to creating the rules for the new technologies. The 2026 Automotive Standardization Work Plan, in addition to the previous National Standardization Development Outline, contains a noticeable push to drive standards in areas such as autonomous driving, batteries, electric vehicle safety, the industrial internet and other new-generation technologies.[24] For a superpower en route to full industrial dominance, this seems a reasonable course, but it takes on a distinctly political tone when used in conjunction with subsidy intensity and export levels. Standards are never solely about the technical issue at hand but also have important implications for replacement markets, maintenance networks, software compatibility and downstream value capture locations. As China transitions from price competition to standards dominance, Western concerns rise because the game can now be played with the instruments of future institutional lock-in rather than current trade flows.

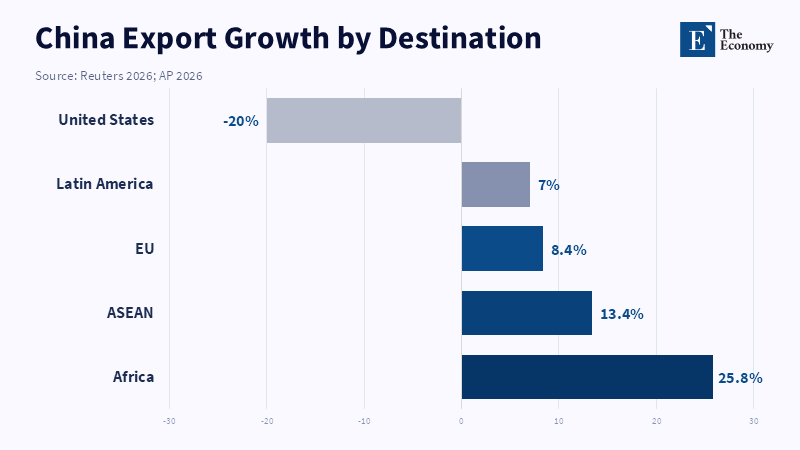

Lastly, China's macro situation complicates all that. Reuters reports that China's merchandise trade surplus ended 2025 at an all-time high of nearly US$1.2 trillion,[25] with exports to ASEAN, Africa and the EU more than compensating for the 20 percent drop in exports to the United States. The IMF's message to Beijing in December 2025 was equally unambiguous: a country of China's size cannot continue China's export-led adjustment without triggering defensive reactions from abroad.[26] That is precisely the issue at stake in current tensions. What the Western economies object to most about China is not Chinese industrial policy per se. It is the country's pioneering use of high-powered state support by a former latecomer, where domestic demand is still too narrow to cope with the country's productive expansion. Under such circumstances, exporting countries no longer see it as a contribution to global prosperity. They see it as an externalization of China's internal disequilibrium.

3. Why China Must Move from Catch-Up Industrial Policy to System-Level Restraint

But a sustainable deal cannot be secured by merely asking the US and Europe to unilaterally restore liberal discipline because a deeper issue is at stake. The system faces a structure of incentives confronting all large powers, where some gains conferred by the blunt trade-off will be usurped by the returns attributable to strategic retaliation. Consider two options: the first is evident and the second is aspirational. The obvious option in the short run is the pathway of subsidy escalation, unilateral tariffs, export controls, screening of investments and domestic-content favoritism-all justified in the language of resilience or security but collectively destructive of the trading order. The second is a process of negotiation, simultaneously to bring down tariffs and subsidy distortions, something that would revive indefinitely the logic that delineated the postwar era of liberalized trade. The latter is politically difficult in the short term, as it involves addressing the underlying problem rather than postponing it and implementing it is challenging in the long term, as it requires reciprocal restraint, transparency and an apparent acknowledgment that the problem cannot be addressed by a single actor.

The problem is that the West has already compromised its own case for simply defending free trade. Research by the OECD involving 20 countries, as explored through industrial strategies, finds that grants and tax expenditures increased from 1.34 percent of GDP in 2019 to 1.55 percent in 2023,[27] the lion's share being devoted to fixed capital investment, the energy transition and relief from the costs of energy. US semiconductor policy is even more illuminating. According to a December 2025 report by the GAO, by July 2025, the Department of Commerce had committed 19 companies to support for 40 semiconductor projects to the tune of USD 30.9 billion in direct funds and a further USD 5.5 billion in loans,[28] with the original CHIPS framework legislated also featuring components of "upside sharing" positioning the taxpayer to benefit from potential windfalls. By late 2025, Reuters reported an active debate in Washington about acquiring direct equity positions in CHIPS beneficiaries and, by August 2025, Intel had changed its CHIPS contract to reserve for the American state a 9.9 percent shareholding.[29] Whatever the policy justification about the policy case, this is far from normal market neutrality.

That matters because it alters the magnitude and the strategy space. The language of market neutrality no longer describes reality; neither does the idea of the state as a neutral referee. What is much closer to reality is the proposition that all key nations are engaging in industrial policy, but with that industrial policy shaped by different institutional constraints. Research from the OECD and IMF indicates that under prudent circumstances, industrial policy can be effective at raising output in targeted sectors but by limited degrees, often heterogeneously and with meaningful spillovers. The IMF 2025 report finds a very similar outcome, with limited gains from industry-specific subsidies and coverage of broader interventions can often bring down overall productivity, as resources are guided away from more efficient areas.[30] The same chapter also presciently observes that the large industrial race is likely to induce consequential retaliation by trading partners and that the best achievable outcome globally would be a coordinated advantage over subsidy escalation. In essence, a game in which every major economy chooses subsidization, regardless of common minimum disciplines, is not a pragmatic adaptation but growing negative-sum competition.

And that, of course, is the reason this conflict cannot be resolved in Washington, Brussels, Berlin, or Paris. China has to decide whether or not it wishes to be a sustainable system-supporting power or a persistent market destabilizer. The distinction is one of practicality, not polemical rhetoric. A responsible system-supporting power does not abandon its national interests but recognizes that leadership in the system entails an obligation of restraint, disclosure and reciprocation. For example, China has demonstrated a limited appreciation for the strategic benefits of market opening. It agreed in May of 2026 to initiate tariff negotiations with the United States on agricultural products and to move toward identifying non-strategic commodities for tariff reduction. This followed a move also in 2025-2026 to grant zero-tariff access to imports from the 53 African countries with which it maintains diplomatic relations. Both reflect an awareness that market opening can be a strategic asset. But it is tactically selective, being employed wherever it facilitates the achievement of export goals, Global South diplomacy, or bargaining position, but not yet in the context of an overarching framework governing subsidy discipline and reciprocal access in market negotiations with the advanced economies.

The African case is particularly illuminating. In opening markets, China's zero-tariff policy on imports helps unlock access and provides Beijing with a conspicuous diplomatic benefit[31] when the US is rolling back its renewed tariff pressure. Yet as Reuters and AP coverage indicate, the conditions of trade are still grossly asymmetric. China's exports to Africa are still many times what it imports back and Africa still faces nontariff restrictions and deficiencies in infrastructure that hinder it from enjoying the full benefits of formal tariff preferences. The point is not that China's African policy is opportunistic. It is that tariff openness does not generate a well-balanced trading regime when productive capacities, logistics, capital constraints and leverage are so fundamentally asymmetric. It is equally applicable to both the context of Europe and the US. If China really desires access to high-income markets for its most evolved manufactured items, it simply cannot claim the benefits of foreign market access and forgo the concerns about market disruption in such markets while evoking free trade, even as it supports persistent subsidy support to mature sectors and subsidizes and below-market finance that its trading partners increasingly regard as no longer compatible with available contributions and reciprocity.

What would system-supporting Chinese conduct imply? It would start with credible subsidy discipline, where Chinese firms are competitive today, even in global markets. This does not imply complete abandonment of industrial policy, which the World Bank’s 2026 reassessment of industrial policy - due in 2026 - is clearly too pragmatic to endorse. It recognizes that governments are not required to abandon targeted instruments that correct market failures, but also that broad tariffs and crude subsidies are still not to be trusted and that industrial policy should not permanently displace macro stability, infrastructure, skill development and good domestic institutions: in the strongest version, the World Bank argues that industrial policy should buy time for adjustment (and while it should not be used to deny needed adjustment to the viability of inefficient firms); ideally it should not be structurally sticky. A similar message applies to China: support in sectors during the catch-up phase was justifiable; sustained support to the strongest firms in the solar, battery, EV, steel and linked supply-chain sectors now provides broader costs to the rest of the trading system with less developmental justification than earlier.

A negotiated exit from the current disorder will therefore need to be a two-way process. The US and Europe will have to bear in mind that China will not be excluded from key strategic fields of the future, where developing the associated technical disciplines requires effort. At the same time, it should also not be expected, as if China were still merely a latecomer, that the country will need to compete with earlier late-industrializing powers such as Japan and Germany on the same historical terms. Bruegel's 2026 model offers some useful pointers here by noting that it is largely unrealistic to assume that Washington and/or Beijing will suddenly revert to the older liberal multilateralism of the late twentieth century. The emphasis should be on an EU-led platform of middle powers campaigning for stronger disciplines on subsidies, new plurilateral options and an overhaul of dispute-settlement, even if some of these initially have to go through certain arrangements in partly outside the WTO framework. Admittedly, it is a pragmatic, not an ideal way of going forward, but an essential one, not an illusion that one side will adversarially suppress the other side and prosper from imbalances, but rules capable of making coexistence less distortionary.

4. The Cost of Persistence: More Tariffs, More Screening, More Fragmentation

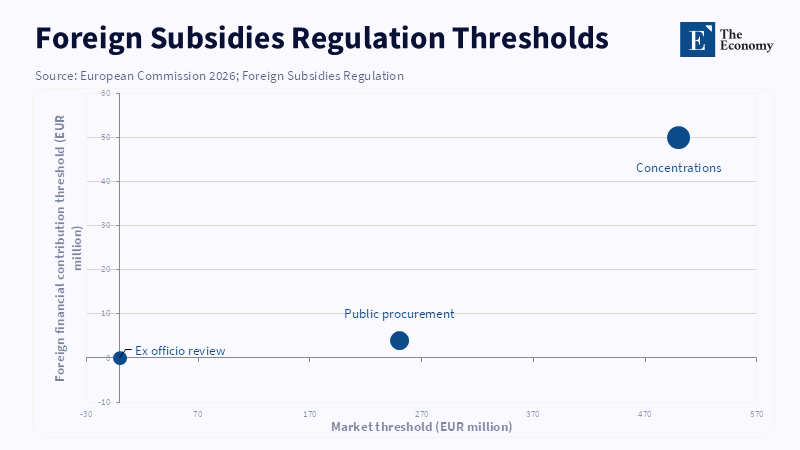

If China sustains this weak combination of local demand, large external surpluses and high-density support for global competitive sectors, the risk is not just a fresh local equilibration, but instead an "upstream proliferation" of defensive constrainment abroad. The earliest signals were already there: the EU Rules governing Foreign Subsidies, effective since 1 July 2023, with mandatory notification thresholds since 1 October 2023, authorizing the European Commission to investigate mergers between companies that received large financial contributions from non-EU countries. This "tool" has already swiftly become an element of the EU's 'China policy'. Its scope covers all targets generating a minimum of EUR 500 million in EU turnover, characterized as having received more than EUR 50 million in associated international financial inputs during the last three years.[32] This "rule-based solution" can be interpreted as an institutional response to a political problem: that subsidized international firms may, via "capital-market" activities and acquisitions, rather than solely via 'exports', tap into state-derived comparative advantages within the Single Market.

The recent cases illustrate how quickly trade conflicts can turn into investment conflicts. In May 2026, the European Commission opened an in-depth FSR investigation into JD.com's effort to buy Ceconomy,[33] believing that state support by the Chinese government in the form of financing, tax privileges, or grants may have supported a bid that risks undermining the internal market. Moreover, in 2024 and 2025, the Commission also used the Foreign Subsidies Regulation in cases involving Chinese-linked security equipment and wind-energy procurement for wind energy technology. The pattern of suspicion is arguably more significant than the outcome of any particular case. Europe is transitioning from ad hoc anxiety about surges in inflows to a broader assumption that distortions caused by subsidies can be carried forward through ownership configurations, service provider networks and public procurement. Once in that territory, the fight does not remain simply a border fight over tariffs. It becomes a broader war over who can own, supply, finance, or standardize strategic markets within Europe.

By then, costs are numerous and diverse. Anti-subsidy duties, anti-dumping investigations and foreign direct investment screening lead the charge. Next come localization mandates, sourcing preferences, informal incentives for domestic manufacturing and tighter data, standards and supply-chain transparency restrictions. The global economic consequence is of a world where headline trade is likely to persist –but where the costs of switching into and out of it seem likely to proliferate, appear to grow heavier, slower and more imbued with possibility. WTO Statistics reveal that this thickening process appears to be in progress. The aggregate value of trade impacted by new import barriers in a world economy deeper into the thickening process has increased enormously and even where members have, on balance, introduced more liberalizing policies (as they seem to have done), the manufacturing environment remains one of "heightened policy uncertainty." Similarly, the 2025 factbook compiled by Global Trade Alert reveals the same structure: tariff barriers are thicker, subsidies continue to be widespread and newer justifications in terms of national security underpin a growing proportion of these initiatives. Hence, the most ominous indicator of systemic depletion is not simply the erosion of trade, but rather its transformation from a relatively rule-governed activity into an inherently politically situated one.

In spite of the excess burden of retaliation, overall costs are even for the countries that act reflexively. Based on the Yale Budget Lab estimates, the new tariff arrangement in January 2026 as a whole implied an effective pre - substitution tariff rate of 17.5 percent, the highest since 1932. The NBER survey mentioned above finds pass-through rates of approximately 80 percent for tariffs in 2018-19 and 94 percent for tariffs to 2025, meaning that the burden of tariffs fell primarily on US importers. Yet another study, published by the New York Fed, echoed that: American firms and consumers paid 94 percent of tariffs in early 2025 and still paid 86 percent by November. The Congressional Budget Office has found that the 2025 tariff increases would lead to lower output and raise prices by an average of 0.4 percentage points in 2025 and 2026. Policy-wise, these results are conclusive. Retaliatory protection may meet the needs of the protected constituencies, but as an economic policy tool, it amounts almost exclusively to a tax on domestic producers and consumers.

Nor do these domestic costs deliver real strategic restraint. WTO trade data indicate that global trade maintained vigorous growth in 2025, as companies rerouted flows, brought shipments forward and in some cases shifted sourcing. In 2025, Asian economies comprised 71 percent of global merchandise trade volume growth, reorienting some supplies away from North America and toward South America and Africa. That tendency means inefficient tariff wars could produce domestic inflation and compliance costs without reliably forcing the targeted economy to contract toward desired sectors. For instance, China's trade figures exemplify that reality. As Reuters reports,partly due to increasingly aggressive American tariffs in particular, China bookended 2025 with a record USD 1.2 trillion trade excess by redirecting volumes to other markets. This should not be mistaken for strategic strength: That's why retaliation is self-defeating. Broad tariffs can reroute trade, but can't always address the underlying imbalance.

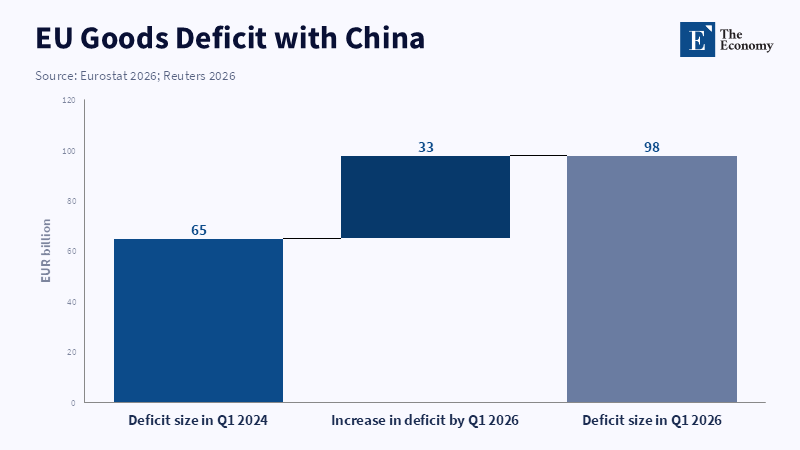

On a similar note, Europe has a risk of it happening to it. According to the latest Eurostat update, the EU's goods deficit with China has worsened from EUR 65 billion in the first quarter of 2024 to EUR 98 billion in the first quarter of 2026,[34] as imports increased and exports weakened. Meanwhile, the European Commission is now "concluding" that its trade and investment relationship with China is no longer sustainable and is even mulling withdrawal of measures, or the threat thereof, against Chinese chemicals, metals and clean-energy industries. For an economy with weak productivity growth and high energy prices, this is a reactive practice appropriate, but if carried out absent some agreement thereon, then it will only entrench Europe in a permanently more expensive, high-cost, de-risking business environment: more restrictions, more admin work, more pressure for public subsidies and more reliance on market-wide public capital.

The legal and institutional implications are, of course, equally crucial. With the appellate arbitration mechanism disabled, more disputes will be brought and fewer will be so conclusively determined that their authoritative legal rule, to be universally binding, will be identical. China has already relied on the WTO to confront fresh US tariffs. And the EU-China electric-vehicle conflict has only intensified the call for alternative negotiated solutions, such as undertakings at minimum prices. But without a working appellate mechanism and stronger subsidy disciplines, these fights are likely to migrate ever more from the realm of law toward that of power politics. Bruegel's pronouncement that the WTO is headed for a fate of irrelevance unless willing coalition members create new subsidy disciplines and plurilateral channels is certainly not exaggerated. Far from arriving at some neat new order, however, the emerging pattern will be one of layered fragmentation-some trade remaining, some market access gained, some disputes litigated and others relegated to bilateral clientelism and bargaining. It will be a world of more fights, more harm and more losses; however, without forward-looking GDP predictions immediately collapsing.

5. A Governed Settlement: China in the Leading Tier of Rule-Shaping Economies, with Disciplined Subsidies

A viable alternative is not Western capitulation to Chinese industrial policy and it is not Chinese abandonment of industrial policy altogether.[35] It is rather a negotiated accommodation to a changed distribution of power.[36] Ironically, this would require Washington and Brussels to accept that China is now ready to join the leading tier of industrial and regulatory powers; yet, at the same time, China would have to accept that policy tools that promoted a Chinese catch-up may then be politically illegitimate once applied by mature globally competitive firms by state or private actors once applied by an equally (or more) mature catch-up firms. Such a deal would not go back to the relatively liberal multilateral order that characterized the 1990s.[37] It would, nonetheless, produce a more litigation-prone yet more governable and predictable international order: one in which the strategic contest goes on, but while the intensity of subsidy, tariff escalation and standards conflict is contained by reciprocal rules and review procedures.[38]

History indicates that this middle course is the correct one.[39] Many readers will find their intuition confirmed that China is not alone in using the state to leap forward in industry: the US industrialized after a relatively high set of nineteenth-century tariffs, Germany's debates over whether to try to catch up were conducted within the context of the infant-industry doctrine (related to Friedrich List),and in the 1950s and 1960s the "miracle" nations of Japan and South Korea relied heavily on directed credit, public coherence and planned industrial policy and export-led industrial strategies.[40] But historical analogy is only conceivable if applied prudently. NBER work on late nineteenth-century America indicates that while high tariffs assumed a defensive stance toward more than doubling the pace of the economy, growth owed far more to population growth, capital accumulation and productivity gains after accounting for the effects of the tariffs and tariffs impeded capital formation in some cases, too.[41] South Korea's strategy of targeted development of the "heavy and chemical" industries, by contrast, did encourage targeted growth and active comparative advantage,[42] as is well known in recent quantitative work. The lesson to be learned from all of this is not that protectionism is necessarily always good or necessarily a stumbling block to growth. Rather, it is that industrial policy can be an effective policy instrument in catch-up industries, but only when particular macro-conditions are present: discipline, competitive pressure, an orientation to foreign markets and an endgame.[43]

That is the key difference today for China. Intermediary nations such as Japan and Korea were hit with hard budget constraints, fierce export discipline and the consistent test of foreign markets and opened gradually as their sectors became mature. The ADB work on East Asia stresses that export growth and industrial policy were a pair, not because tariffs made industries strong, but because firms were forced into competitive world markets and judged against the outside world. The 2026 World Bank reassessment comes close to the same conclusion in words more appropriate today: Industrial policy can be one part of a toolbox, but broad tariffs are crude and intervention cannot last forever. When support no longer solves coordination failures and begins to cement the established elite, it stops being developmental and turns distortive.[44] The argument applies to Chinese firms that are globally competitive in EVs, batteries, solar, steel, shipping and digital platforms to an extraordinary degree.

A credible deal therefore needs to be rooted in a Chinese concession to excessive subsidies, which should comprise: first, tighter disciplines for the provision of below-cost financing to incumbent large firms across globally-concentrated markets; second, mandatory, verifiable reporting of central and local subsidy programs; third, restrictions on export and acquisition support in sensitive sectors; fourth, more robust domestic antitrust policy to curb subsidy-induced price wars and excess capacity; fifth, macroeconomic rebalancing that increases household demand while reducing systemic reliance on external surpluses. China has already alluded to the conceptual logic of such a rebalancing. Reuters reported in late 2025 that EVs were not included in the 2026-30 five-year plan, suggesting at least a phased scaling back of the earlier subsidy-based approach once the sector matured. Taken to other mature industries seriously, such measures would not be an indication of weakness. They would be an indication of the policy evolution befitting a leading system player.

The other side of the coin is the reciprocal Western response. The United States and Europe must reject setting policy in terms of an either/or choice of unconditional openness or exclusion that permanently shuts China out of strategic value chains in a first-best world. Neither one exists. China is a state actor that is already writing the rules as its increasingly ambitious standards agenda makes clear and Beijing is too deeply integrated into world production and resource supply in key industries like manufacturing, critical materials and clean-energy technology to be excluded from analysis. The challenge on the ground is to give in selectively to surrenders of specific strategic sectors and instead accept China's seat at the rule-writing table so long as stronger disciplines on subsidies, standards interoperability and market opening are in place. Trade policy pragmatism, institutional coordination and a moderation of security language can help both to sustain meaningful cross-border exchange where the security argument is not strongly invoked and bolster the effectiveness of other coercive tools and carrots. That begins with rolling back broad and distortionary tariffs and replacing them with targeted, WTO-consistent trade remedy procedures, transitioning away from indefinite punitive duties by designing reviewable safeguard instruments and rewarding past reforms with explicit tariff reductions, especially in sectors where relative improvements are most notable.

Formally institutional, the best way that a common framework can be implemented does not have to be through enormous quid pro quos. It can be a multitude of regimes that work in different layers. Bruegel's plan to form an EU initiative between middle powers is constructive because it accepts the situation as it is without yielding to despair.[45] To be credible, a program of reforms should be, for instance, stronger limits on the scope of subsidy programs, particularly when granting below-market financing and supporting it through non-transparent local elements; more explicitly prioritizing industrial policy measures that relate to standards; incorporation of plurilateral deals in the WTO structure; and exploring short-term learnings to reinstate the WTO's appeals procedure beyond the interim MPIA. Discussing the terms of sectoral pacts, such as EVs, clean energy equipment, steel, semiconductors and critical minerals can be carried out in parallel, exposing proponents to requirements for permanency regarding transparency, enforceability and ceilings on investments and over-capacity expansion. Even if these actions will not eradicate interstate incitements, they should make them less virulent. Today's is already an enormous challenge.

The message for policymakers is pragmatic. US and EU tariff policy should be pinned to concretely quantifiable limits rather than rhetorically defined maximal positions. Administrators should bolster transparency rules for subsidies, coordinate criteria for investment reviews and nurture rapid-response procedures that separate real security issues from ordinary commercial competition. Trade officials should focus on architecture for established strategic fields, not try to prohibit industrial policy, in other words, to ban it in general, a remedy that neither political reality nor economic history can support. Chinese authorities should admit that external enmity cannot be managed solely through improved government economic relationships or an aggressive exporting model in the developing world. It can only be satisfied by effectively altering the composition of support existing at home and redeploying the economy to the needs of the household, referring to domestic users. Otherwise, each boost in the Korean economy hand lowers their household demand, which will be seen internationally not simply as efficiency, but as a subsidy to the socialization of change-like economic burden for China's relative adjustment on the rest.

The change will be involuntary. Disputes will occur along the lines of thresholds, standards of proof, developmental exemptions and definitions of legitimate security policy. Some policies that are now entrenched in practice were introduced in a state of emergency and will be difficult to roll back. Some ongoing negotiations, including parts of the US-China tariff mitigation process and the European Commission's foreign-subsidy investigations remains in a state of flux. But what is settled thus far is the governing logics. China can no longer be regarded as a permissible exception as a latecomer to industry, wielding all-out economic power. The days that the US and Europe could uphold a viable trading regime as they went about supporting a potentially transient rise of China no longer exist. It is now a choice of governed coexistence against an incremental fracturing. The former requires transfer of authority from each actor to the reigning order and the latter requires little immediate adjustment from any actor.

6. Conclusion - Governed Coexistence or Managed Fragmentation

The ongoing trade crisis does not mark the end of globalization, but rather the end of evasion. For three decades, the multilateral trading system has avoided the tougher question of how a rules-based order should adapt when a former latecomer becomes a technological, financial and industrial power capable of transforming strategic sectors. China has now made that question unavoidable. Today, its subsidization and scale advantages, export surpluses and standards ambitions have systemic effects that can no longer be regarded as mere catch-up policy. Yet, the response by the US and the EU has also exposed the boundaries of defending liberal trade by means of rising tariffs, subsidy races and unilateral controls.

A stable settlement therefore requires reciprocal realism. China needs to reverse the expansion of subsidization into the more efficient and more mature industries of the world economy, improve disclosure of subsidy programs and rebalance growth toward stronger domestic demand. The US and Europe should accept China as a permanent rule-shaping power and move away from broad tariff warfare in favor of more selective and reviewable WTO-consistent disciplines. The best way forward is not a return to the trade of 1995, given that it was not predefined by reciprocal subsidy resolve, but a guided coexistence defined by subsidy transparency, plurilateral agreement, refurbished dispute resolution procedures and sectorally limited time frames. Absent such an agreement, although trade will endure, trust, legal clarity and productive efficiency perspective will continue to erode.

References

[1] World Trade Organization (2023) World Tariff Profiles 2023. WTO.

[2,3] World Trade Organization (2025) Trade Monitoring Report: Mid-October 2024 to Mid-October 2025. WTO.

[4] Global Trade Alert (2025) Global Trade Alert Factbook 2025. St. Gallen Endowment for Prosperity Through Trade.

[5,6] World Trade Organization (2026) Global Trade Outlook and Statistics, March 2026. WTO.

[7] World Trade Organization (2024/2025) Dispute Settlement: Appellate Body and MPIA Documentation. WTO.

[8] Yale Budget Lab (2026) State of U.S. Tariffs: January 19, 2026. Yale University.

[9,10,11] OECD (2025) The State of Play of Industrial Subsidies as of 2023. OECD.

[12] Center for Strategic and International Studies (2025/2026) China’s Solar Industry and Global Supply-Chain Concentration. CSIS.

[13] REN21 (2025) Renewables Global Status Report. REN21.

[14,15] OECD (2025) OECD Steel Outlook 2025. OECD.

[16] OECD / World Steel Association (2025) Steel Market Developments and Global Excess Capacity. OECD / World Steel Association.

[17] European Commission (2024) Anti-Subsidy Investigation Concerning Battery Electric Vehicles from China. European Commission.

[18] European Commission (2024) Definitive Countervailing Duties on Imports of Battery Electric Vehicles from China. European Commission.

[19,20] Reuters (2026) Chinese Automakers Gain Share in Europe Despite EV Duties. Reuters.

[21] Rhodium Group (2026) Why Are Chinese EVs So Cheap? Rhodium Group.

[22] Reuters / S&P Global Market Intelligence (2026) Chinese Mining Acquisitions and Overseas Resource Strategy. Reuters / S&P Global.

[23] Griffith Asia Institute (2026) Chinese Investment in Overseas Mining, 2025. Griffith University.

[24] Standardization Administration of China / State Council of China (2021–2026) National Standardization Development Outline and Automotive Standardization Work Plan. Government of China.

[25] Reuters (2026) China Ends 2025 with Record Trade Surplus. Reuters.

[26] International Monetary Fund (2025) People’s Republic of China: Article IV Consultation / Staff Concluding Statement. IMF.

[27] OECD (2025) Quantifying Industrial Strategies across OECD and Partner Economies. OECD.

[28] US Government Accountability Office (2025) CHIPS for America: Semiconductor Incentives and Program Implementation. GAO.

[29] Reuters (2025) Intel Amends CHIPS Act Deal with U.S. Commerce Department. Reuters.

[30,44] International Monetary Fund (2025) Industrial Policy, Subsidies, and Spillovers. IMF.

[31] Reuters / Associated Press (2025/2026) China Expands Zero-Tariff Access for African Countries. Reuters / AP.

[32] European Commission (2026) The Foreign Subsidies Regulation in a Nutshell. European Commission.

[33] Reuters (2026) JD.com’s Ceconomy Deal Faces Full-Scale EU Subsidy Investigation. Reuters.

[34] Eurostat / Reuters (2026) EU-China Goods Trade Deficit and China-EU Trade Relations. Eurostat / Reuters.

[35,36,45] Bruegel (2026) A Plan to Revitalise the World Trade Organization. Bruegel.

[37,38] Reuters (2026) WTO Chief Calls for Trade Overhaul to Meet New World Order. Reuters.

[39,41] Irwin, Douglas A. (2000/2020) Historical Perspectives on U.S. Trade Policy and Industrialisation. NBER / Economic History Literature.

[40] Chang, Ha-Joon (2002) Kicking Away the Ladder: Development Strategy in Historical Perspective. Anthem Press.

[42] Amsden, Alice H. (1989) Asia’s Next Giant: South Korea and Late Industrialization. Oxford University Press.

[43] World Bank (2026) Leaning Heavily on Tariffs Blunts Developing Nations’ Industrial Push. World Bank.