Sovereignty Through Indispensability: Europe’s Realistic Path in the Global Chip Race

Published

1 The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

2 Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

The purpose of this article is to show that Europe's semiconductor strategy ought to evolve away from self-sufficiency towards sovereignty through indispensability. Between the Covid-19 shortages, burgeoning AI consumption, and intensifying geopolitical competition, all the United States, China and the EU now perceive semiconductors as a kind of critical infrastructure, rather than a normal industrial commodity, and the entire value chain of chip production and use is far too complicated, niche and capital-intensive for total control over its domestic economy to ever become a realistic policy target. The American effort demonstrates that enormous state investment is insufficient to break the dependency on the part of Asian memory manufacturers, Taiwanese manufacturers of the final chips, Japanese inputs and EU lithography equipment. The Asian model suggests that strategic leverage does not have to flow from entire value chain ownership, whereas China's whole value chain push highlights the limitations of state capital investment, when critical machinery, design equipment and manufacturing expertise is still externally dependent. In this environment, Europe's most viable option is to shore up its current critical chokepoints: ASML, its precision optics know-how, the necessary research equipment and facilities, power electronics, automotive semiconductors and specific parts of the intellectual property associated with semiconductors. Instead of focusing solely on total domestic production share, the EU policy needs to measure itself against its indispensability and the interdependence and co-investment it shares with its trusted allies. Chip sovereignty for the EU will rely far less on domestic production for every part of its value chain and more on its immunity to external economic exclusion from any of the key global chip-makers.

1. Introduction - Europe’s Semiconductor Sovereignty Cannot Mean Self-Sufficiency

After 2020, the semiconductor sector moved from the background infrastructure of the digital economy to the centre of geopolitical competition. The dual blows of pandemic shortages and ballooning demand for artificial intelligence (AI) revealed the West's weakness when outsourcing chip production to Asia. In reaction, the U.S. and EU enacted industrial policy, seeking to regain domestic chip value chain capacity. The common wisdom in Brussels and Washington was that technological sovereignty equated with self-sufficiency- countries must be capable in everything from R&D and design through advanced fabrication to assembly.[1] Europe's technological sovereignty had historically stemmed not from one large integrated system, but from a complex web of interlocking institutions and companies. The giants of microelectronics in the 1960s, such as Philips and Siemens, set the tone and European and European-based firms such as ASML and Arm remain central to several high-value links in the semiconductor chain. Although Europe offshored commodity chip production from the 1990s to 2000s, it maintains a critical share in key areas and R&D and has not allowed the entire ecosystem to leave its borders.[2]

Research infrastructure has played a vital role in European capabilities. The Institute for Microelectronics and Nanoelectronics Applications (IMEC) in Belgium, for example, has served as the core of Collaborative R&D bringing together academic researchers, start-ups and industry leaders to develop new manufacturing techniques and chip designs, Fraunhofer Society in Germany and the CEA-Leti in France, for example, had developed cutting-edge research on semiconductor materials science and chip integration, focusing on areas such as power electronics and photonics.[3] Driven by EU research framework programs such as Horizon Europe, these networks managed to push forward innovation despite their domestic production falling behind. In 2025, for instance, IMEC launched a pan-European initiative focused on sub-2nm process nodes that draws on experts from more than twelve countries and has attracted investment from world leaders such as TSMC and Intel, underscoring its importance as a collaboration hub.[4] Public-private partnerships further underpinned this approach; the European Processor Initiative (EPI) endeavors to develop energy-efficient processors suitable for supercomputing and the automotive sector;[5] the alliance combines European expertise, industrial capacity and end-user domains in order to bring advanced results. Their focus is on areas such as high-end packaging, silicon photonics and AI accelerators. Europe's capacity in chip production is not about scale but a well-integrated system involving knowledge, skill and cooperation across borders.

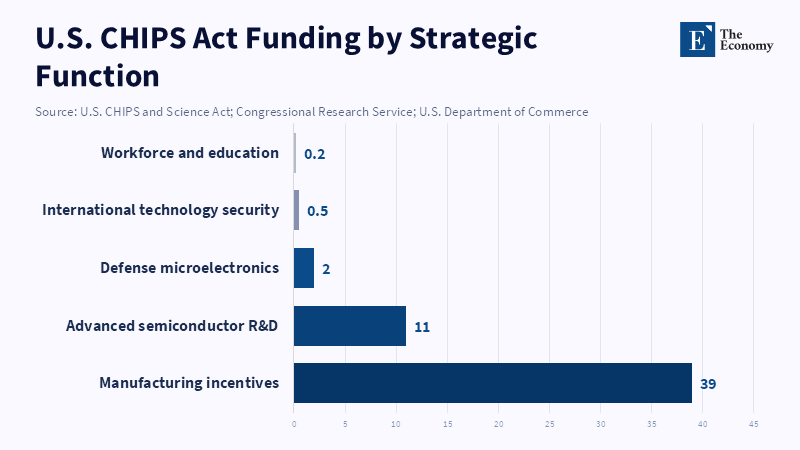

This paper will demonstrate that the discourse of self-sufficiency is not only insufficient but dangerous for Europe, because Europe lacks a consolidated national authority and a fully integrated ecosystem, pure self-sufficiency in chip production is unaffordable and inefficient. An "Indispensability" strategy should be deployed, in which Industrial Policy is used to enhance those strengths the EU already possesses and consequently integrate them within the global value chain and thus attain technological sovereignty. This argument can be illustrated through recent industrial-policy outcomes; the U.S. CHIPS and Science Act invested $52.7 billion to enhance domestic production capacity and R&D, to strengthen the U.S. Semiconductor value chain.[6] Even so, U.S. Still heavily relies on South Korea, Taiwan and Japan to supply most chips such as DRAM and NAND flash;[7] The 2023 EU Chips Act, despite mobilising roughly €43bn, still struggles to overcome Europe's deficits in leading firms, scale and coordinated financing[8] and there is neither a U.S. Approach (increasing R&D and capacity), nor a Chinese model (state-driven approach to self-sufficiency), to take as the blueprint. The EU should leverage its existing advantages, such as a leading position in high-end lithography (through ASML) and chip design (through Arm), in order to develop diplomatic and economic leverage.[9] A coordination framework at the EU level needs to be established to protect such core competitiveness by increasing interdependence with friendly actors, such as bringing Taiwanese and South Korean semiconductor firms including TSMC, Samsung and SK Hynix, into deeper production partnerships in Europe to enlarge capacity, thereby ensuring a supply security that does not come with political dependence.

The following sections compare the US, Asian Model (Taiwan and South Korea) and Chinese semiconductor models in order to draw out the strategic choices available to the EU. The U.S. Model is ambitiously planned and well-funded, but the whole chain cannot be reproduced; the Asian Model has specialization but is dependent on other foreign elements for upstream technologies; the Chinese Model has relied on enormous capital accumulation and aimed to build every link in the chain, but has struggled to reach cutting-edge technology. The article advances a fourth model: European indispensability, under which the EU does not attempt to do everything but secures sovereignty by becoming irreplaceable in selected high-value segments of the global semiconductor chain. The analysis uses recent evidence on capacity shares, investment commitments and market concentration to compare the limits of full-chain strategies with the advantages of strategic specialization. The policy implication is that the EU should abandon the logic of autarchy and embark on the strategic insertion into those parts of the chain, where interdependence is feasible.

2. The U.S. Model - Full-Chain Ambition Without Full-Chain Control

The United States responded to supply disruptions with an ambitious reshoring campaign, announced 2017-2020 and with the passage of the CHIPS and Science Act in 2022, which promised $52.7 billion in subsidies to lure domestic fabs and invest in R&D and workforce.[10] Companies such as Intel, Samsung and TSMC are expected to pour billions into constructing U.S. Fabs; recent project announcements have involved dozens of chip-related commitments across multiple states,[11] though not all announced investments are guaranteed to be completed on schedule aimed at achieving ultimate self-sufficiency and fully encompassing the value chain from R&D to assembly.

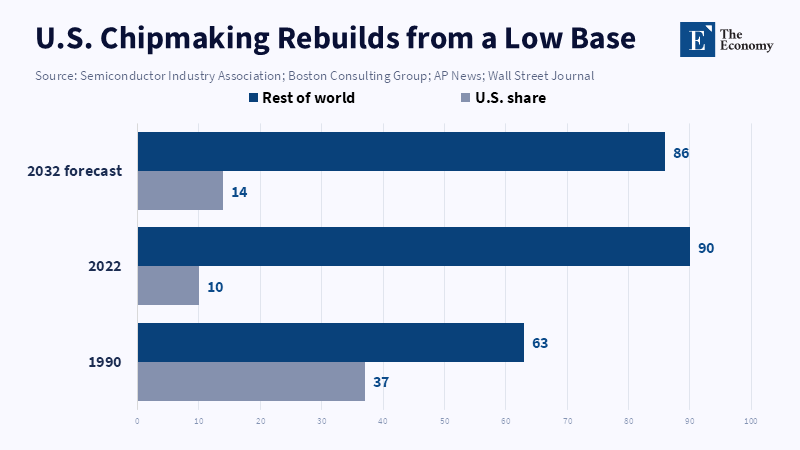

Despite this vast injection of capital, it is unclear what the ultimate impact will be: In 2026, the U.S. Share in global semiconductor manufacturing capacity will increase from 10-13% to only 14% in 2032 and it is still going to be far behind the rest.[12] It is in chip design that U.S. Companies hold most of the key elements, whereas manufacturing relies largely on overseas markets.[13] Thus, the U.S. cannot secure full control of the value chain.[14]

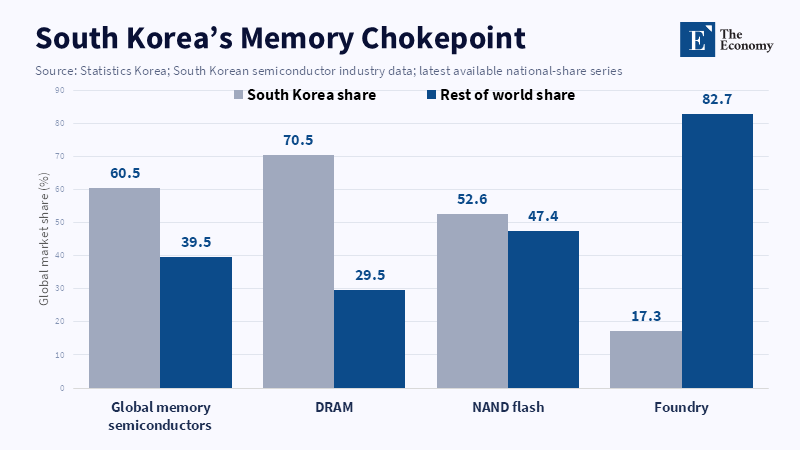

Secondly, the U.S. also has a key gap in DRAM and NAND flash memory; 73% and 51% of global capacity in those areas are occupied by South Korean chipmakers (Samsung and SK Hynix, respectively), with the U.S. having negligibly low capacity and importing the vast majority.[15] Since the U.S. lacks the domestic capacity in such memory products, it remains dependent on the East Asian Allies to fill those gaps; in fact, it is estimated that only 4% of memory chip capacity is to be found in the U.S. Despite a new commitment, it is still not enough to make up the deficit. The value chain of the U.S. is still inextricably intertwined with East Asia, irrespective of investments made.

Thirdly, the dependence on logic chip manufacturing has also not been completely severed. Despite the U.S. Capacity increase in leading-edge logic, it still relies on foreign suppliers for inputs, such as materials and equipment.[16] The EU firm ASML is indispensable for logic chip lithography[17] machines and much of the input material is imported from Japan. The chip design companies in the U.S., although they provide the blueprints, outsource the manufacturing part to fabless U.S. Chips; therefore, logic chip production between the U.S. and Asia remains mutually dependent. ASML alone has received more than $4.1 billion in R&D investments from U.S., EU and Asian chip manufacturers such as Samsung and Intel; a strong testimony to the dependency and interdependence between players of the semiconductor value chain.

Second-order consequences exacerbate the seemingly straightforward discourse about U.S. self-sufficiency. The America First discourse on semiconductors could lead to alienation between U.S. partners and undermine the integrity of EU and Japanese security interests. The way U.S. industrial policy might set incentives to favor domestic users and production sites can cause problems to allies in terms of access and coordination. Thus, threatening strategic allies with a potential two-tier access system. Thus, capacity alone cannot guarantee security and the risks to partners might rise.

Quantitatively, after massive investment commitments, the U.S. Will still rank fifth in global semiconductor manufacturing capacity by 2032 behind China, Taiwan, South Korea and Japan; Advanced logic chip (under 10nm) production will only reach 28% domestically-far from a leading position. In a word, the U.S. will be able to produce more domestically, but cannot replace foreign production or completely fulfill the global demand.[18] Even so, capacity expansion might not be the end of the story: a security focus of "America First" policies may indeed pose great challenges to the unity and trust among allies. Given that U.S. and Asian partners are deeply integrated, it is unlikely the EU can follow exactly the U.S. Path; there should be a different option for the EU.

3. The Asia Model - Specialized Indispensability Within a Fragmented Value Chain

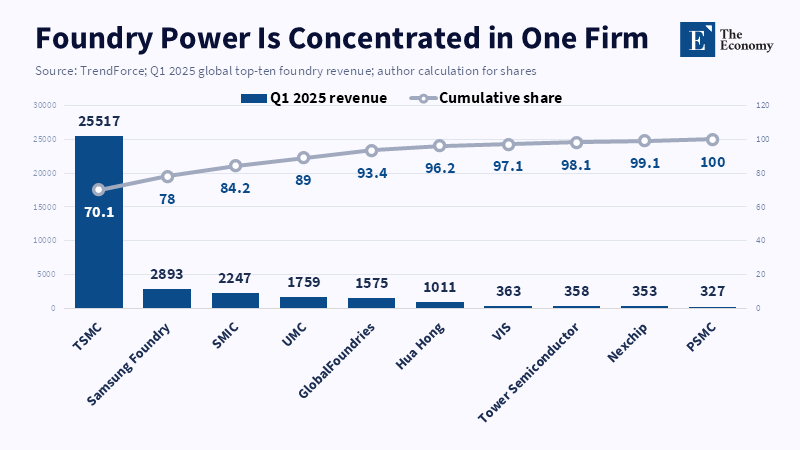

The Asian semiconductor model differs sharply from the U.S. approach;Taiwan and South Korea have become the powerhouse of global semiconductor manufacturing capacity and yield. In 2025, Taiwanese foundry TSMC dominated the foundry market with 70% global market share, whereas Samsung from South Korea had roughly 7%.[19] South Korea's memory giants Samsung and SK Hynix dominate global DRAM and NAND flash production[20] with 73% and 51% capacity share, respectively. Taiwan and Korea do not attempt to recreate upstream technologies; no Taiwanese foundry attempts to invent its own lithography machines and South Korean memory manufacturers have to rely on U.S. chip design and foreign design software. Both of them have to import essential machinery such as ASML's EUV lithography machine and Tokyo Electron's etchers and inputs from Japan like advanced chemical materials.[21] With EU firm ASML having an exclusive monopoly on the EUV lithography machine production, it gives the EU significant market leverage and economic value; no country can compete without it.[22]

ASML and TSMC are often referred to as a 'chokepoint' in the value chain: "without the lithography machine provided by the Netherlands-based firm ASML, it is impossible for TSMC to produce leading-edge semiconductors". South Korea's memory factories rely on Japanese equipment. China relies on foreign designs and technologies such as ARM processor architecture and EDA software from the U.S.; Third countries rely on the East Asian Countries for manufactured final goods: smartphones, servers, graphics processors and car parts, etc. Neither side completely holds sway over the other, because East Asian countries don't seek to match the U.S. and European technological advantage; they have concentrated on certain niche areas of the semiconductor value chain, thus giving them immense leverage despite relying on upstream producers for necessary components and equipment. East Asia demonstrated success with their "compromise" approach: selling itself as an indispensable supplier on some crucial part of the chain, with original technologies owned by third parties.[23] Hence, countries such as the U.S. and the EU are dependent on their East Asian counterpart.

However, in such a context, neither the U.S. nor the EU should replicate the entire East Asian value chain. China and the U.S. have focused their investments only on certain parts of the chain and they are not successful everywhere; thus, the East Asian Model reveals that specialization leads to success in specific areas and economic factors should dominate over political factors when considering industrial strategy. China and the U.S. have focused on manufacturing and design, respectively. It does not need to imitate that kind of specialized framework, because there are gaps that can be exploited.

4. The China Model - Whole-Chain Mobilization with Diminishing Strategic Returns

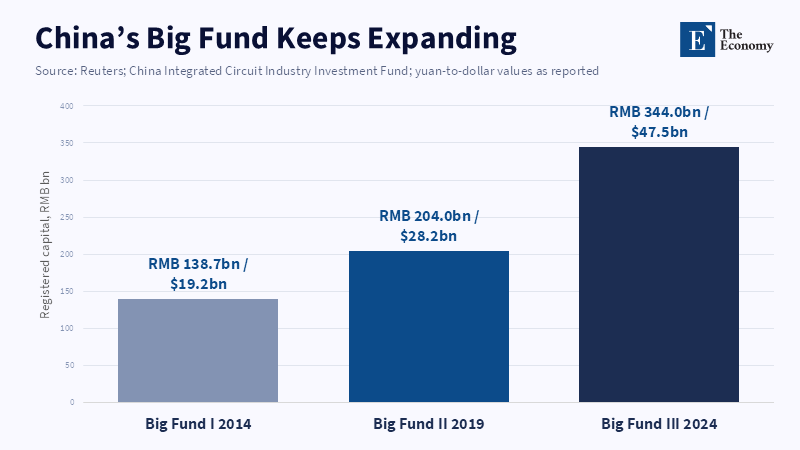

The Chinese vision of Technological Sovereignty through semiconductors appears to be the most aggressive. The government is pouring hundreds of billions of dollars into this sector via national funds such as the 'Big Fund' since 2014.[24] The aim is to have complete dominance of the entire value chain from design, manufacturing, to assembly of the chips.[25] Companies like SMIC, YMTC and CXMT are the pioneers.

China has not managed to produce the desired cutting-edge result; Chinese foundries have seen success at older nodes, however, their structure is blocked from being commercially scaled to the leading edge as access to EUV lithography is still blocked,[26] which requires EUV machines that China has not been able to secure after the ban was enforced in 2019 due to U.S. Pressure. Hence, Chinese logic manufacturing remains reliant on old DUV technology, increasing the cost and slowing down production volume. Although China is seeking to break the dependence on foreign processors through the promotion of RISC-V, it is still way behind Western architectures such as ARM at present.[27]

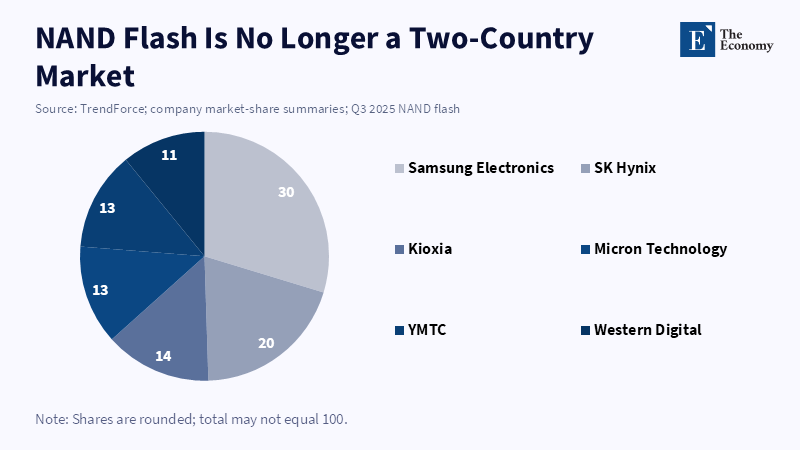

As for memory chips, China has made considerable progress but is not catching up quickly; YMTC has secured a significant share in NAND. However, China still lags the best of South Korean, U.S. and Japanese companies in many high-end memory segments, where factors like yield, access to equipment and customer qualification are crucial;[28] however, it's still lagging behind its Western competitors on crucial aspects. It is likely that Chinese capacity expansion will continue to affect global memory markets; however, certain kinds of memories, such as server DRAM, are still purchased from outside the country.

The ambition to achieve self-sufficiency is a politically driven project, but it leads to geoeconomic risks. The Chinese aim for independence, coupled with U.S. sanctions, has led to escalating pressure and restricted access to chip technology.[29] Furthermore, the geopolitical repercussions also extend to third countries as China attempts to gain control over certain vital components through raw material dominance. Meanwhile, there is the risk of a massive dump of chips below the market value due to the expansion of capacity, hence jeopardizing stable markets with overproduction.[30] The lessons are that state-led development is no magic bullet; decades of continued investment and innovation are a prerequisite. China's endeavor still hasn't reached its goals yet. The U.S and China Models are not sustainable choices to make; thus, Europe needs to find another path to enhance its semiconductor power.

5. The EU’s New Model - Sovereignty Through Indispensability, Not Self-Sufficiency

Europe’s Situation is distinctive and its semiconductor strategy must reflect that institutional reality. In contrast to the nation-state approach of either the U.S. Or China, as well as the efficiency-oriented export-driven strategy of smaller EU partners, the EU, as a collection of diverse economies with varying industrial strengths and policy aims, cannot pursue singular national ambitions and gambles in industrial policy or related technologies in the manner that the U.S. Or China do. One Member State cannot remold all of Europe’s chip supply and as one EU nation cannot pursue a single, unilateral ambition across Europe, nor can it easily attain it. Critically, over the next three to four years (2023-2026) and as the geopolitical environment evolves and technologies that were previously a technical area are now at the epicenter of a global technology race, a fully autonomous self-sufficiency model is unlikely to be the winning strategy; and could, dangerously, render Europe the eventual loser trapped between two greater rivals.

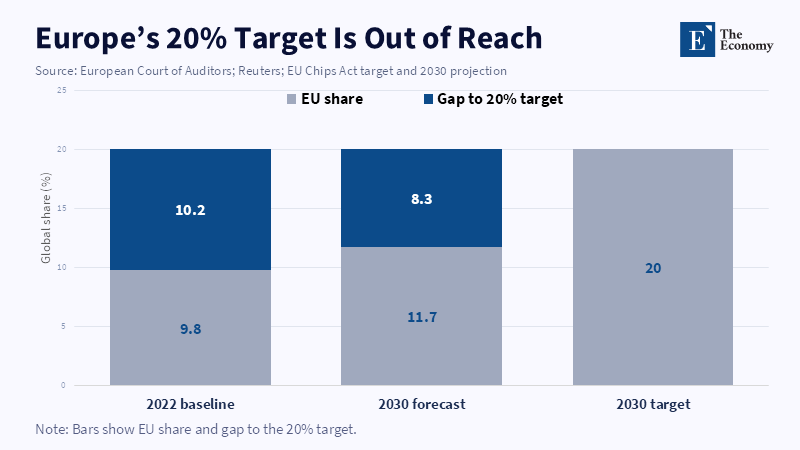

The EU strategy thus far, codified by the 2023 Chips Act, is by and large similar to that of the U.S. – aiming for a 20% share of the global semiconductor market by 2030.[31] Even by the Commission's own figures, Europe will not even achieve over 11% share by 2030 under current plans.[32] To hit 20% would take approx €250bn – more than currently available – and would only bring partial independence at an eye-watering price.[33] Whether it is a monopolistic element, such as ASML's exclusive equipment technology, or Taiwan's crucial role in fabricating chips, the simple creation of a handful of additional factories does not equate to the acquisition of Europe's chip sovereignty.

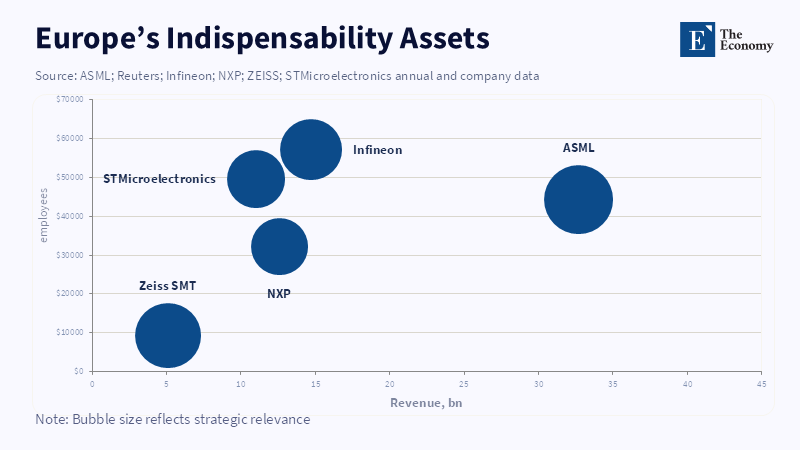

Instead, a strategy of indispensability, a distinct European concept that will be elaborated, offers a more attainable proposition. Europe is the possessor of unique capabilities and so the continent's task should be to transform those specific strengths into mutually dependent value creation, establishing Europe's claim as an indispensable partner in the global supply chain, not as an autonomous, self-sufficient producer across all segments of the semiconductor value chain.[34] Instead of re-creating all segments of the semiconductor value chain from scratch, Europe should focus on enhancing and solidifying existing competitive advantages. That would translate into, as an example, the Dutch company ASML, which is one of the critical technologies relied on by every world leader in chip production – without ASML's most advanced lithography systems, leading-edge chip production would face severe constraints[35] – and ARM, a UK company, the instruction set architecture for most smartphones on the planet gives the broader European technology landscape a critical place in semiconductor IP, although it is critical to put this into context, regarding ownership, and geography.[36] Such niche market dominance can become the focus of Europe's funds and research support, building up a few highly competitive EU companies as world leaders in areas where they have a strategic advantage, supported by research partners like imec in Belgium and Fraunhofer in Germany.

A focus on indispensability is inherently a strategy that leverages Europe's strengths: the continent dominates the fields of precision optics and machinery (the German company Zeiss is the second largest supplier of lithography optics after ASML), is home to excellent academic electronics networks and, even though their market segment largely comprises less cutting-edge technologies, houses the leading manufacturers of semiconductors in Europe: Infineon, STMicro and NXP.[37] Instead of spreading its resources too thinly, Europe should develop symbiotic relationships with Asia and America, which would make them dependent on Europe’s contribution to their own chip supply at least as much as the EU relies on their supply. In practical terms, this brief strategy calls for leveraging European technologies in order to create mutual dependence such that America and Asia's interest in gaining access to Europe’s production capacity, whether to the latest lithography machines designed by ASML or the precision optics manufactured by Zeiss, is just as high as the partners' interest in maintaining Europe's access to their chip supply, thereby making the future market for European production essential for global chip capacity.

This strategy has important implications for policy. First, 20% EU market share should no longer be the key policy target; instead, it should be replaced by a few critically essential technologies, which are to be dominated by a handful of elite European manufacturers. Chip Act 2.0 should reward these targeted companies, as suggested by many experts; second, Europe should adopt a more forward stance on inviting investment from Asia; facilitating integration between the EU's funds and those investments by key Asian partners (such as TSMC, Samsung and SK Hynix), evidenced by the planned chip manufacturing plant in Germany that will be operated jointly with European manufacturers Bosch, Infineon and NXP.[38] This should be underpinned by streamlined permitting, integrated incentive mechanisms and a consistent policy framework in order to support these new collaborations, secure an EU supply and move away from a model that merely exports finished goods and instead establish more profound industrial partnerships. At its heart, this strategy mirrors that adopted by the Asian countries of allowing Asian manufacturing facilities in areas of strategic necessity and in this case, this will involve the EU inviting Asian investment for certain stages in the European supply chain rather than manufacturing offshore.

Third, far greater coordination of the chip investment and related policies at the EU level is needed. As explained by the Center for Future Generations, it is the EU-level coordination on export controls and screening of investment that provides crucial security;[39] it is not enough for individual states to each take action independently, with a fragmented approach inevitably weakened. This is to say nothing about the responses Europe should offer in case other countries (such as China) implement export restrictions. This unified position must at the very least guarantee Europe the ability to leverage its relatively open market conditions to bargain from its position in terms of controlling the export of its crucial technology, thus creating incentives for foreign nations to engage constructively with the EU, a principle at the heart of the existing Chips Act.

Fourth, the production of further factories shouldn't necessarily form the center of the European strategy even if it will continue to be an important factor in areas where European strengths lie – such as the logical operations and silicon carbide production areas exemplified by the investment of Intel and TSMC in Germany. Although the recent series of delays and cancellations in certain European projects of semiconductor manufacturing indicate that only when new fabs are economically necessary, selectively driven and integrated into a larger system of suppliers and customers are they worthwhile.[40] Autonomy will need to take the form of integrated resilience; Europe will have to rely on its expertise in equipment, design and possibly certain advanced manufacturing stages to create strategic dependencies such that the denial of access to its technologies and production capacity would impose substantial costs on the other countries themselves. Instead of building vast swathes of new greenfield factories, Europe should invest in and expand its research networks and develop a handful of niche leaders in a range of key areas, thereby enabling the design of the world's future chips with the EU in the forefront of that endeavor.

Finally, 'indispensability' has a clear implication for investment. Europe can no longer rely on a strategy of 'sovereignty through expenditure';[41] as global chip production currently only constitutes about 15% of world production, in less sophisticated technologies than would be involved and as investment gaps are likely to grow further between 2023 and 2026, one can no longer assume that buying critical mass through mere increases in capacity is possible. Europe's chip security strategy must be centered on creating critical dependencies and making itself indispensable to its global partners[42] and in turn developing enough leverage over others' chip supplies that Europe can ensure its own chip access. Europe has considerable strategic advantages via ASML, Zeiss and associated research-industrial networks-an advantage that will only be meaningful if protected, scaled and integrated at the EU level.[43] This type of approach secures negotiation instead of exclusion. It relies on making its production indispensable, thereby providing for a nation's chip security in an essential industry. The challenge is formidable: fail to adapt such a strategy during 2023-2026 and Europe risks becoming ever more vulnerable as demand for chip-dependent products skyrockets, whilst its capacity to meet those needs independent of outside support or leveraging critical dependencies remains inadequate.

6. Conclusion - Europe’s Chip Power Depends on Being Irreplaceable

The problem of Europe is not simply about a shortage of semiconductors. On a more fundamental level, Europe has attempted to imagine sovereignty within the same standard as the other major power in the world: total output. U.S. can invest astronomical sums in producing virtually every element of an almost-closed ecosystem and yet remain reliant on the import of Asian memories, Taiwanese foundries, Japanese components and European lithography; China can pour enormous state resources into every stage of the global supply chain and yet remain bound by equipment availability, design tools, advanced manufacturing techniques and knowledge. The challenge of semiconductor sovereignty cannot simply be to copy every step in the process at home.

A more realistic route for the EU is sovereignty through indispensability. Europe has already secured some unique, non-substitutable strategic resources - lithography, high end optics, research facilities, power semiconductors, automotive chip manufacturing and some forms of semiconductor IP. The policy goal must be not to divert money towards a numerical production figure, but to further strengthen Europe's chokepoints and align them at the EU level and more generally and place Asian and allied investments within a larger European resilience context. Europe's revised Chips Act must promote indispensable strategy, rather than symbolic autarky. Europe's security does not lie in its own production, but in a situation where each of the main semiconductor powers must continue to keep Europe within its supply chain.

References

[1] Bruegel (2025) Revamping Europe’s Chips Strategy: Indispensability, Not Self-Sufficiency. Bruegel.

[2] European Commission (2022) A Chips Act for Europe. European Commission.

[3] imec (2025) Annual Report and Semiconductor Research Programmes. imec.

[4] imec (2026) NanoIC Pilot Line for Sub-2nm Semiconductor Research. imec.

[5] European Processor Initiative (2024) European Processor Initiative: Energy-Efficient Processors for HPC, Automotive and AI Applications. EPI / EuroHPC JU.

[6] United States Congress (2022) CHIPS and Science Act. Public Law 117–167.

[7] TrendForce (2025) DRAM and NAND Flash Market Share Reports. TrendForce.

[8] European Parliament and Council of the European Union (2023) Regulation (EU) 2023/1781 Establishing a Framework of Measures for Strengthening Europe’s Semiconductor Ecosystem. Official Journal of the European Union.

[9] ASML (2025) Annual Report 2025. ASML Holding N.V.

[10] U.S. Department of Commerce (2023) CHIPS for America: A Strategy for the CHIPS for America Fund. U.S. Department of Commerce.

[11] Semiconductor Industry Association (2025) CHIPS Act Manufacturing Projects and Private Investment Tracker. Semiconductor Industry Association.

[12] Semiconductor Industry Association and Boston Consulting Group (2024) Emerging Resilience in the Semiconductor Supply Chain. SIA / BCG.

[13] Boston Consulting Group and Semiconductor Industry Association (2021) Strengthening the Global Semiconductor Supply Chain in an Uncertain Era. BCG / SIA.

[14] Semiconductor Industry Association and Boston Consulting Group (2024) Emerging Resilience in the Semiconductor Supply Chain. SIA / BCG.

[15] Semiconductor Industry Association (2024) 2024 State of the U.S. Semiconductor Industry. Semiconductor Industry Association.

[16] Center for Strategic and International Studies (2024) Mapping the Semiconductor Supply Chain: Allied Materials and Equipment Dependencies. CSIS.

[17] ASML (2025) EUV Lithography Systems and High-NA EUV Technology. ASML Holding N.V.

[18] Semiconductor Industry Association and Boston Consulting Group (2024) Emerging Resilience in the Semiconductor Supply Chain. SIA / BCG.

[19] TrendForce (2025) Global Top 10 Foundries Revenue Ranking, Q1 2025. TrendForce.

[20] TrendForce (2025) Memory Market Share and Revenue Analysis: DRAM, NAND and HBM. TrendForce.

[21] SEMI (2024) World Fab Forecast. SEMI.

[22] ASML (2025) Annual Report 2025. ASML Holding N.V.

[23] Miller, C. (2022) Chip War: The Fight for the World’s Most Critical Technology. Scribner.

[24] Reuters (2024) China Sets Up Third Fund with $47.5 Billion to Boost Semiconductor Sector. Reuters.

[25] OECD (2023) Semiconductors and the Global Value Chain: Risks, Dependencies and Policy Responses. OECD.

[26] TechInsights (2023) Huawei Mate 60 Pro Teardown and Kirin 9000S Analysis. TechInsights.

[27] RISC-V International (2024) RISC-V Adoption and Ecosystem Report. RISC-V International.

[28] TrendForce (2025) China’s Memory Industry and Global NAND Market Share. TrendForce.

[29] U.S. Bureau of Industry and Security (2022) Commerce Implements New Export Controls on Advanced Computing and Semiconductor Manufacturing Items to the People’s Republic of China. U.S. Department of Commerce.

[30] Rhodium Group (2024) Overcapacity at the Gate: China’s Semiconductor Expansion and Global Market Risk. Rhodium Group.

[31] European Commission (2023) European Chips Act: Strengthening Europe’s Semiconductor Ecosystem. European Commission.

[32] European Court of Auditors (2025) The EU’s Industrial Strategy for Microchips: Ambitious, but Facing Major Implementation Risks. European Court of Auditors.

[33] European Semiconductor Industry Association (2025) Recommendations for a Chips Act 2.0. European Semiconductor Industry Association.

[34] Bruegel (2025) Revamping Europe’s Chips Strategy: Indispensability, Not Self-Sufficiency. Bruegel.

[35] ASML (2025) Annual Report 2025. ASML Holding N.V.

[36] Arm Holdings (2025) Annual Report and Form 20-F. Arm Holdings plc.

[37] ZEISS Group (2025) Annual Report 2024/25. Carl Zeiss AG.

[38] European Commission (2024) Commission Approves German State Aid Measure to Support European Semiconductor Manufacturing Company Facility in Dresden. European Commission.

[39] Center for Future Generations (2025) Strengthening EU Coordination on Semiconductor Export Controls and Investment Screening. Center for Future Generations.

[40] Reuters (2024) Wolfspeed Shelves Plans to Build Chip Factory in Germany. Reuters.

[41] European Court of Auditors (2025) The EU’s Industrial Strategy for Microchips: Ambitious, but Facing Major Implementation Risks. European Court of Auditors.

[42] Bruegel (2025) Revamping Europe’s Chips Strategy: Indispensability, Not Self-Sufficiency. Bruegel.

[43] Bruegel (2025) Revamping Europe’s Chips Strategy: Indispensability, Not Self-Sufficiency. Bruegel.