Europe’s Energy Trilemma and the Case for Integration

Published

1 The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

2 Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

This paper reinterprets Europe's energy trilemma as an issue of political scale instead of security, affordability, and sustainability trade-offs. Russia's war in Ukraine, the destabilization of the Middle East and the ambiguous US commitment to energy security reveal the failures of nationally fragmented energy approaches. The central claim is that system integration should be regarded not as a technical fix for energy policy but as the institutional mechanism for Europe to turn geographic diversity into strategic depth. Using a comparative analysis of Europe's unfolding integration agenda and China's continental-scale allocation model as well as Japan's and South Korea's import-heavy hedging approaches, the paper argues that energy security has become a challenge for the energy sector's capacity to manage generation, transmission, storage, sourcing, and market design over a vast geographic scale. While China's national grid integration has succeeded in channeling resource-rich regions toward industrial consumption and Japan and South Korea illustrate the limits of reserves, supplier diversification and alternative fuels when systemic flexibility is absent due to both geographic conditions and fragmented institutions, Europe enjoys unique conditions that allow it to develop a continental system while East Asia is faced with different challenges and approaches. This paper asks whether Europe's existing framework will result in resilience, should it regard integration as industrial policy, security policy and climate policy in parallel.

1. Introduction - Geopolitical Risk and the Return of the Energy Trilemma

The energy trilemma has returned not as a policy puzzle but as a test of scale. Security, affordability, and sustainability were long thought of as competing policy goals that could be traded off against each other using diversification of supply, technologies and markets. That approach is now too limited. The war in Ukraine, Middle Eastern political and economic instability and the increasingly uncertain role of the United States as a guarantor of global energy security show that energy systems are not simply technical networks.[1] They are political-economy systems, by which dependence, bargaining power and coordination between institutions translate into price risks, the supply insecurity and the resilience of industrial sectors. Europe's crisis following 2022 illustrated the problem sharply. The challenge was not simply the expense of imported gas or higher utility bills for consumers and businesses. The real difficulty was that their geographically disparate national energy systems were not equipped to cope with the geostrategic disruption of continental proportions. An energy system with little cross-border integration, limited supply options and nationally bound decision-making is less resilient to shocks than one that pools capacity to generate, transmit, store, procure and market energy across national borders. This paper argues that energy system integration is not a reform[2] for an optional addition. It is the institutional foundation on which Europe can reconcile the demands of the trilemma and simultaneously pursue affordable and sustainable energy policies.[3]

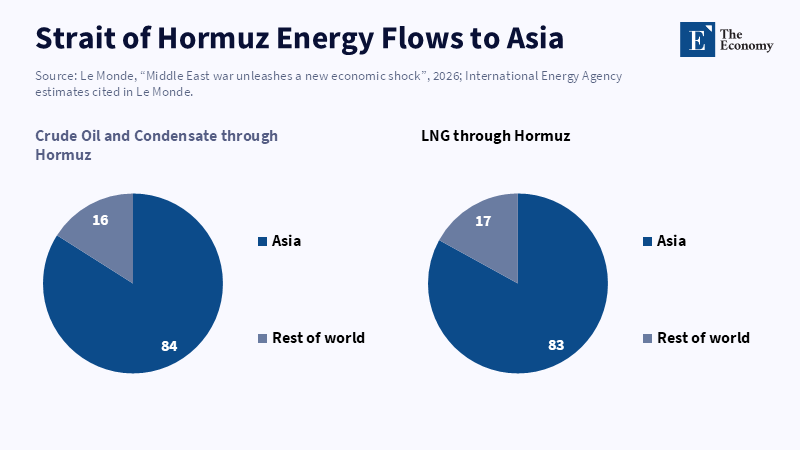

The same geopolitical forces operate in East Asia but on a less favorable institutional basis. Japan and South Korea have sophisticated industrial bases, advanced infrastructure and considerable financial capacity but they are dependent on fossil fuel imports and are vulnerable to threats to maritime trade routes. The impact of recent conflict in the Middle East, as highlighted by the disruption of oil supplies passing through the Strait of Hormuz and by sharp upward revisions of oil prices, is further underscored by these exposures. Brent crude is trading around the low-hundred-dollars range, rather than the considerably lower level it traded before the recent crisis.[4] Their response is, therefore, a defensive one, relying on diversification of supply sources, building strategic reserves, adopting new fossil fuel use practices (such as burning coal), and pursuing bilateral energy diplomacy with exporting countries. However, these measures do not replicate the underlying structural advantage that can be enjoyed through access to a wide range of supply and demand regions at the pan-continental level.

Conversely, China benefits not just from large investments in renewable power but from its capacity to match the supply of generation, transmission, storage and consumption across a vast and unified national space.[5] By this means, it can deploy wind and solar resources in its less-populous interior with ultra-high-voltage lines linked to its populous industrial heartland along the coasts, transfer surpluses of generation from provinces to demand centers throughout the national grid, and install capacity in those areas where wind and solar resources are most plentiful rather than close to where consumption is highest. It does not follow, therefore, that China’s approach can be directly replicated in Europe. As a nation-state, Europe cannot achieve the same level of centralized, and ultimately nationally constrained, management as China. However, Europe has an institutional advantage over Japan and South Korea; namely, the potential for supra-national institution-building to unify disparate national energy capacities into a coordinated pan-continental system. This paper contends, therefore, that the strategic choice before Europe is not between maintaining national sovereignty and integrating energy systems, but between two alternatives: either continuing its present dependence on external supply and price risks and using emergency hedging tactics or choosing managed interdependence within a pan-European energy system capable of bearing joint risks and apportioning the costs of decarbonization. It begins by exploring the Brookings argument for integration over a la carte energy security. It then contrasts the allocation system characteristic of China with the risk hedging models used by Japan and Korea, before concluding with recommendations for policy.

2. What has been suggested by the Brookings: Integration over À La Carte Energy Security

The post-2022 period in Europe, marked by considerable turmoil, has led many observers to a consensus on a singular, overarching proposal: integration of energy systems. According to a recent Brookings analysis (and its synopsis in EurekAlert), cross-border electrical and gas grid integration "holds the key to Europe's energy trilemma."[6] What this translates to in practice is that the once largely isolated national grids are being brought together into a broader continental network, not unlike what China has accomplished nationally. The core argument is that system integration delivers triple benefits-it ensures energy security by creating backup import options, reduces costs by tapping into the most competitive generation pool and advances sustainability through more effective utilization of renewables.

However, in the absence of integration, Europe functions on a piecemeal "à la carte" basis where individual members optimize their specific energy market, resulting in a different energy mix and cost of energy across countries.[7] Countries with huge potential of renewable energy sources (such as Spain and Greece) may not always be in a position to export excess to neighboring countries such as Poland or the Balkan states, which are heavily reliant on coal and imported gas. Cross-border transmission limits mean the countries are frequently unable to respond to fluctuations in demand and supply. As one European politician said, "market integration is happening à la carte: few countries want to share cheap electricity, so we see negative prices in one country and triple-digit prices in another". This ad hoc approach is neither mutually beneficial nor cost-effective. While one country is sitting on a surplus of renewable energy, another is struggling to keep itself supplied with energy.

This disjointed approach is incredibly costly: as indicated by Brookings' research, an integrated European energy network would currently save €39 billion a year, rising to €50 billion by 2030, in terms of lower curtailment levels, more coherent market pricing and increased investment efficiency.[8] However, these figures are actually historical in nature; the energy crisis of 2022 proved that countries with more extensive interconnections to neighboring states were able to import power during the period of shortages, sparing consumers and industry from the worst effects of the shortages. In summary, by consolidating the ownership of generation and transmission infrastructure, consumers would have had access to Europe's cheapest sources of energy, stabilizing supply/demand relationships and enabling greater resistance to potential future crises.

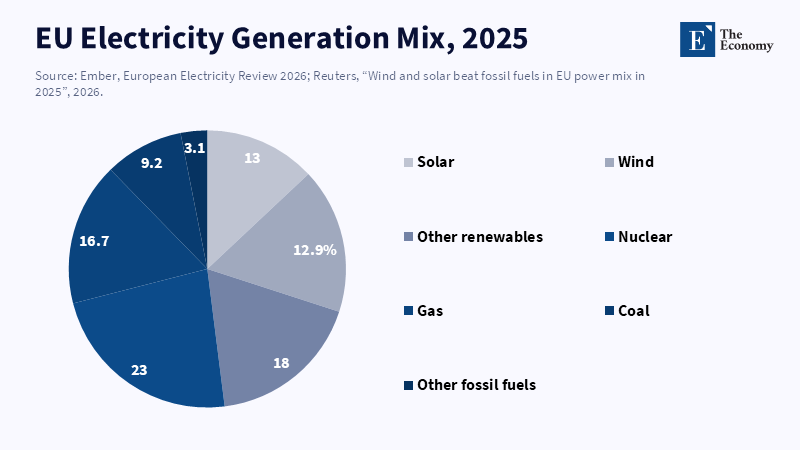

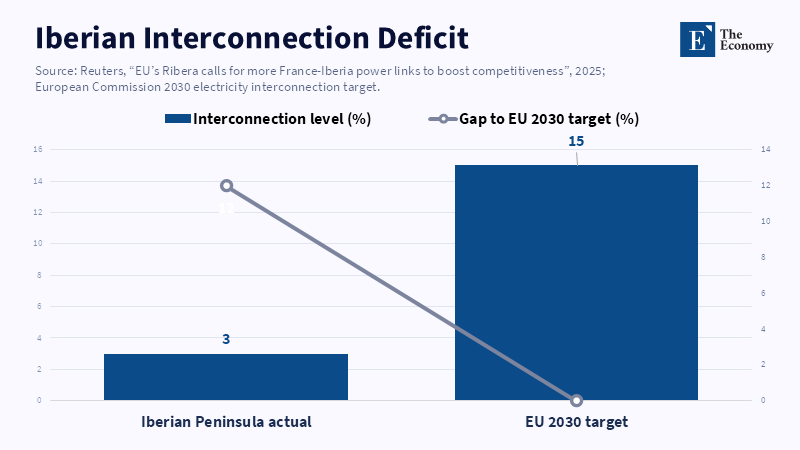

More specifically, the EU and its partners will look to several concrete steps to foster the integration process. First is the integration of the electricity markets. The EU has set a clear target of 10% interconnection by 2020 and 15% interconnection by 2030 to the electrical grid of every member state.[9] This will require new high-capacity interconnection lines, such as the interconnections between Iberia and France or the Baltic states and Poland.[10] Ursula von der Leyen has articulated eight "energy highway" projects that would serve as a linchpin for Europe's energy transition.[11] These include expanding interconnections in the Baltics and Balkans, across the Pyrenees and transforming the North Sea into a continental offshore renewable energy hub. This way, it would be possible to distribute solar energy generated in the south of Europe and offshore wind energy from the North Sea across the continent, thereby pooling geographical resources to generate more affordable renewable power.

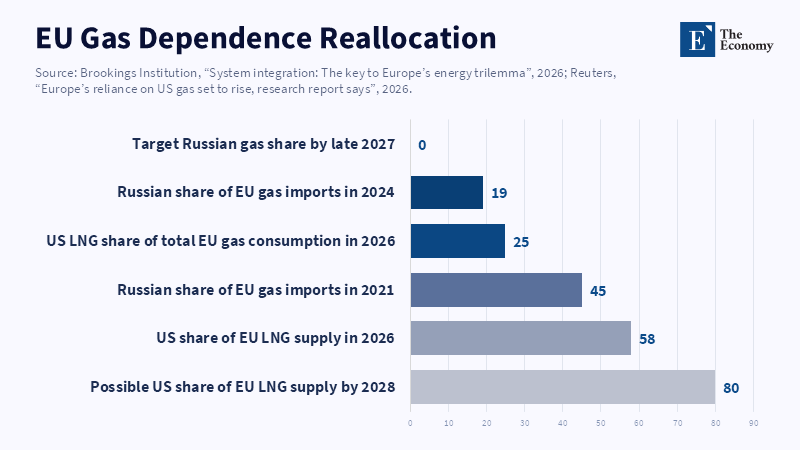

Second, the EU has long tried to integrate its natural gas markets by liberalizing trade and creating virtual trading points such as the TTF in the Netherlands. Since the Russian invasion of Ukraine in 2022, priorities have shifted towards reducing dependency on a singular source. Russian imports have decreased from 45% of total gas imports in 2021 to 19% in 2024[12] and are pledged to be phased out by 2027.[13] There has been much infrastructure to support this transition, such as the Poland-Lithuania gas interconnector opened in 2022, which integrated the Baltic states into the wider EU network and reversed pipeline flows to supply Moldova with energy. The EU also, for the first time, used a collective purchase scheme (AggregateEU)[14] where suppliers were allocated to buyers to account for almost a third of the demand.[15] Such collective demand pooling essentially acts as a single nation-state, aggregating demand to attain better prices, similar to the Chinese nationalized system.

In addition, funds are to be found for integration: the costs of HVDC lines, hydrogen pipeline and LNG terminals are running into hundreds of billions of euros[16]. Apart from the capital, integration also requires long-term planning, standardization and agreement on regulations and public support, all of which are difficult in a fragmented political setting. Resistance to the building of large-scale infrastructure projects is also to be expected at the local level due to land and environmental concerns.

The political challenges are similarly daunting as integration can only be achieved if individual states are willing to lose some degree of sovereignty, in particular if they had previously been used to protecting their national champions and domestic generators. They might be wary of cheap imports, which will threaten national production and cause job losses. Italy, for example, was initially reluctant to send excess wind from its south to its north due to grid constraints and regional disparities. Equally, an all-EU hydrogen grid is mostly hopeful and the ambitious north-south corridors have to wait given the political obstacles to agreement on cost sharing, technical standards and market access.[17]

However, even Brookings acknowledges that "the costs of inaction will be even greater",[18] as countries that do not seek to integrate within an overarching energy policy are exposed to shocks, while participation allows risk sharing and enhances resilience against supply shocks. While the recent crises of 2022-2026 proved the limits of myopic solutions, leaving individual nations exposed to the negative effects of global market volatility, a collective response would allow for economies of scale and risk sharing. Finally, the energy integration argument is not one about economics, but about the kind of European energy future Europe seeks: one that is based on interdependence, resilience and joint prosperity, or one of fragmentation and insecurity.

The implication is clear: for Brookings, Europe should not allow such a fragmented approach; it should invest in large networks and joint purchases, rather than duplicate investments and hoard supplies. Such a "European energy highway" can extend even to neighboring states, such as Norway and Ukraine. Norway is the EU's "battery" for hydropower, while Switzerland agreed on full integration to the EU's grid; these initiatives show growing recognition that interconnectedness leads to lower cost and more energy security. This comparison leads naturally to China and Japan/Korea, contrasting the Chinese system with the bilateral hedging strategy adopted by Japan and Korea.

3. China vs. Japan/Korea: Continental Allocation versus Import Hedging

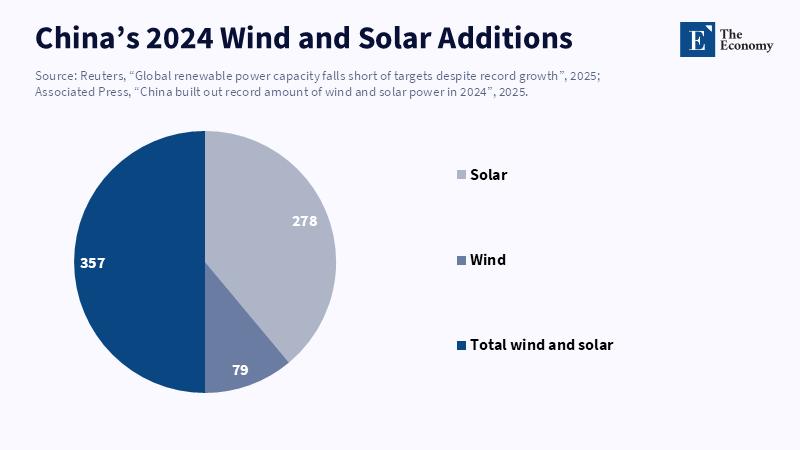

The massive size and unique political system allow China to build an unmatched energy and renewable energy integration system. In the past few years, they have been developing a continent-spanning UHV grid system, which is able to move power from resource-rich areas to urban centers more efficiently. Currently, China's UHV system has a capacity of 340 GW from renewable sources in the northwest of the country to its coastal cities, providing approximately 23% of peak load.[19] The system is expected to expand to 420 GW in 2030, capable of hosting up to 900 GW of renewables.[20] For instance, a 17.2 billion yuan ($2.4 bn) project is in the works to move power from an Inner Mongolia wind farm to northern Beijing and the State Grid spent a record $93 billion in 2025 alone on developing their "super highway" of electricity;[21] in 2025 alone, they are putting down 650 billion yuan on expanding the network.

Essentially, China has developed a single national power grid instead of operating through the former provincial and local networks, which had to operate with local supply and demand dynamics only. Technically challenging as it is, this move has eliminated significant inefficiencies like the curtailment of renewable sources that appeared when certain areas had surplus capacity and could not push this capacity to other areas that needed energy and could not be supplied, thus demanding the importation of fossil fuel. As the WEF has recently put it, China is pushing for breaking down "inter- provincial barriers" and fostering a "unified national market" through electricity trading.[22] Market mechanisms like long-term, spot and ancillary service markets enable the movement of power generated by the solar farms of Xinjiang to Shanghai with the same legal and economic feasibility as if it were generated locally.

The political imperative for such a scheme is huge; power consumption centers and power generation sources are far from each other (a vast amount of China's wind farms and solar farms are in deserts in the northwest of China, while most of China's population and industries are in the East). The only logical solution for this kind of spatial gap is the revolution of power grids. China established massive GW- scale wind and solar farms where the natural resources are available and moved the power to the eastern grids through UHV power lines (which are highly efficient for moving power over long distances), complemented by flexibility measures that the country implements by developing both flexible thermal power and storage facilities. This helps China meet its ambitious goals for green power generation.

This level of integration has significant economic advantages; the rate of curtailment of wind and solar energy has been cut and the cost of energy generation has decreased significantly.[23] It has been estimated that by using the UHV corridor networks, 330Mt CO2 has been cut in five years while coal consumption has been reduced by 330Mt,according to a Chinese newspaper. Southern China also uses massive hydropower and solar projects that are complemented with North-South transmission lines, placing generation where resources are abundant rather than demand.

Even beyond the national borders, China advocates the concept of a "Global Energy Interconnection" with which it is proposing to share power with its neighbors, like Central Asian nations in the case of their solar and wind resources and Southeast Asian countries with their respective wind resources.[24] Diplomacy, large-scale infrastructure projects such as the BRI energy initiatives and UHV interconnections with Russia and Mongolia help to enhance the extent of this integration scheme. China is managing its power system increasingly as a continental allocation platform by linking energy-rich provinces and coastal industrial demand through state-guided grid investment and interprovincial electricity trade, as well as UHV transmission.

Japan and South Korea are at the other end of the structural spectrum. They are developed industrial economies with first-rate physical infrastructure but have no big hinterland endowed with natural resources, no continent-sized national grid like China's. They are not vulnerable for technological reasons; they are vulnerable for reasons of geography, import reliance, and insufficient integration of regional energy systems. While they can pursue supply diversification, building stocks, and longer-term supply contracts, such measures serve as hedges against turbulence, not as an alternative to a mechanism that is able to redistribute the regional or national supply of energy.

In some sense, these are forms of "aggregating natural gas supply" like the EU's aggregate purchase plan, but given the smaller size of the markets and limited bargaining power, the impact is less favorable; for example, if Hormuz were to be closed, neither Japan nor Korea has pipeline connections that reach it and it would take years for any alternative pipelines to come on line. While both can revert to coal-fired plants, use reserves and imports, such measures offer only short-term solutions and are unsustainable during a prolonged energy crisis. While the US, in partnership with the two countries, is planning trilateral stockpiling frameworks for oil and gas, the countries maintain limited interconnection schemes in the form of joint strategic stockpiling and do not yet have pooled energy supplies or a continent-wide grid as in the EU and China.

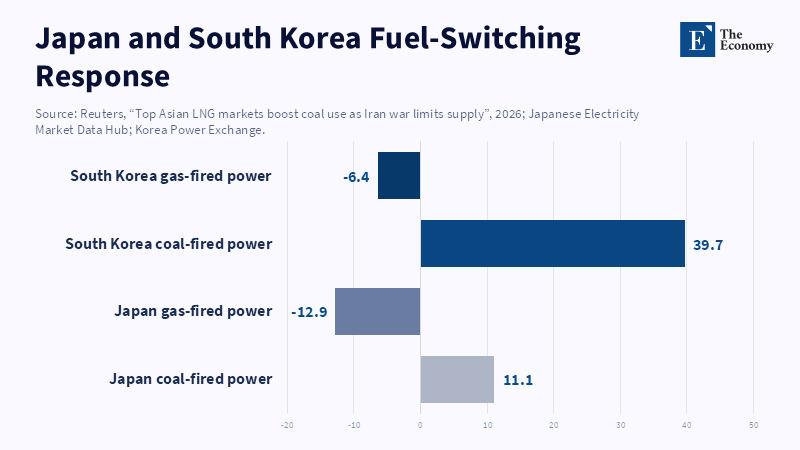

This stark contrast shows that China can direct State Grid and its utility companies to build UHV lines connecting anywhere in its grid, but Japan and Korea cannot do that to their own homelands. During the 2026 Hormuz disruption, they drew from stockpiles (by March 2026, Japan had already sold 80M barrels) and struggled to secure spot cargoes from anywhere they could. Energy security for both countries during the crisis came in the form of more fossil fuel burning: Japan's coal generation rose 11.1% and gas fell 12.9% and Korea's coal consumption increased by 39.7%. These measures were temporary quick mitigations and not long-term solutions.

The United States became Japan's largest crude oil and naphtha exporter and Korea's top petrochemical supplier by late spring 2026. Both nations are exploring trilateral stockpiling strategies with the United States. Stockpiles are ultimately a limited resource. Only the market and China can provide a continued supply and China is systematically integrating through its UHV lines, developing its markets without worrying about foreign shutdowns and short-term price surges on the spot market. China has achieved a stage of building an integrated continental energy market and leveraging the infrastructure through market dynamics. However, Japan and Korea, in contrast, lack this infrastructure and only "hedge against volatility" through hedging instruments. Is it China's integrated model, by expanding the already existent EU grid and market to cover continent-wide transactions, or the Japan and Korea model of limited, bilateral hedging? Europe seems to be in a unique position to take advantage of the existing EU union rather than fail. It will take a lot of political will, however.

4. Japan/Korea: Advanced Infrastructure within a Small-Geography Constraint

Japan and South Korea provide classic examples of the pitfalls of "hedge" strategies. Although these are highly developed democracies with cutting-edge technologies for grid and storage systems, their geographical constraints force them into a position of extreme reliance on imported fuels. As CSIS has observed, Japan imports over 85 percent of its total energy needs and 94 percent of its total crude oil from the Middle East.[25] This has persisted for decades, even with diversification; over 90 percent of its oil imports still come from the Gulf region[26] (chiefly Saudi Arabia and the UAE). South Korea presents a similar picture; its oil imports are dominated by the Middle East[27] (roughly 70 percent), with small portions coming from the same regions and only very little (7-11 percent) from the United States. This creates a very significant vulnerability to chokepoints.[28]

Knowing this, Tokyo and Seoul have both tried to hedge by developing and maintaining massive energy reserves (roughly equivalent to 250 days of consumption) and have also entered into bilateral agreements with various partners to ensure secure energy supplies.[29] They also keep an eye on investment in nuclear power and renewables. Stockpiles offer a partial defense against acute supply interruptions, but neither the advanced grid technology nor vast reserves of fossil fuels constitutes a comprehensive answer to dependency on imports. Energy price volatility has an especially huge impact on these two economies due to their significant import dependency,and the ability to shift between sources of energy is relatively limited. Despite increased oil exports to Asia from the US in April 2026, this supply amounted to less than half of the total US exports and a mere fraction of Japan's and Korea's imports; for instance, only 7-9% of their oil imports are coming from the US currently and this trend is slow to change, even though US LNG exports are expected to increase significantly by 2029.[30]

The responses to the crisis stemming from the closure of the Hormuz Strait are telling: Japan and Korea switched to using vast amounts of coal power in response to the shortfall and in both countries, dormant plants were brought back to life (Korea used its own for industrial purposes and Japan decided on capacity market utilization)[31]. Environmental concerns in Japan and Korea drove their decisions to reduce coal power usage for generation, but the crisis put aside those concerns and coal became the one fuel that the crisis did not affect. It is clear that this approach is not only unsustainable environmentally speaking but also short-term and the existing emergency stockpiles did not make for a viable replacement for intra-regional (or even internal to each country) integration; while the transition towards clean energy is on, sustainable integration will be key, rather than continue with external hedging strategies.

Institutionally, ties between Japan and Korea on energy are still weak and slow moving; Several plans like joint LNG purchases and common stockpiles are discussed,[32] but even grid-meshing projects between Japan and Korea are being considered but are extremely costly and far from realization; Although business cooperation and knowledge sharing on renewable energy technologies (both countries are leaders in offshore wind and EV), a cross- border grid and market is nowhere to be found for sharing hydro or wind power; In contrast to China which shares these kinds of resources and effectively operates like one continent-wide utility, there are only market agreements between Japan and Korea, buying from abroad rather than sharing.

In conclusion, both Japan and Korea, despite being technologically advanced in grid and corporate structures, are constrained by their geographies to use hedging strategies, which make them heavily dependent on global markets and vulnerable to supply disruption from chokepoint countries and to extraordinarily high prices when resorting to alternatives, which makes this strategy costly and insecure for a protracted crisis like the present one. The crisis that coincided with the energy transition and the changing geopolitical scenario in the region clearly shows the limitations of such strategies compared to other areas of the world. Europe is in a favorable position: it can exploit its already existing EU union to integrate the entire continent, something that the two countries of East Asia would have had to build from scratch. The EU can create a continental power grid similar to China's and consolidate its purchase plans, hence overcoming the trilemma factors and achieving a sustainable, reliable and affordable energy system for its member states.

5. Conclusion - Europe’s Choice between Continental Integration and Strategic Hedging

The energy trilemma is no longer simply about balancing supply security, affordability, and climate objectives. It is a question of whether political institutions are capable of coordinating energy systems at a scale demanded by the challenge posed by geopolitical risk. Japan and South Korea both illustrate the limitations of hedging. Reserves, multiple supply contracts, and rapid fuel switching can blunt an energy shock; they can neither replicate the flexibility inherent in continent-scale networks nor provide a meaningful response to prolonged supply disruption. Conversely, China demonstrates a logic about strategic advantage in siting generation where resources are deepest and channeling electricity across a domestic market capable of absorbing local imbalances.

Europe's challenge is to decide whether to emulate one of these two approaches. Treating interconnectors, shared purchases, storage capacity, renewable resource locations and market regulations as shared, strategic resources can transform Europe's territorial diversity into a source of resilience. But failure to move beyond nationally fragmented national strategies may condemn Europe's advanced economies to the vulnerabilities inherent in geographically constrained importers. The policy message is inescapable: integration is not an ancillary support for energy policy but must form the heart of Europe's industrial, security and climate strategies.

References

[1] International Energy Agency (2025) World Energy Outlook 2025, International Energy Agency.

[2] Gross, S. and Stelzenmüller, C. (2026) ‘System integration: The key to Europe’s energy trilemma’, Brookings Institution.

[3] European Commission (2023) Grids, the Missing Link: An EU Action Plan for Grids, European Commission.

[4] Reuters (2026) ‘Oil rises on fears of ship attacks and seizures as tensions persist’, Reuters.

[5] International Renewable Energy Agency (2025) Renewable Capacity Statistics 2025, IRENA.

[6] Gross, S. and Stelzenmüller, C. (2026) ‘System integration: The key to Europe’s energy trilemma’, Brookings Institution.

[7] ACER (2025) Market Monitoring Report 2024: Electricity Wholesale Markets, European Union Agency for the Cooperation of Energy Regulators.

[8] Gross, S. and Stelzenmüller, C. (2026) ‘System integration: The key to Europe’s energy trilemma’, Brookings Institution.

[9] European Commission (2023) ‘Electricity interconnection targets: 10% by 2020 and 15% by 2030’, European Commission.

[10] Reuters (2025) ‘EU’s Ribera calls for more France-Iberia power links to boost competitiveness’, Reuters.

[11] Gross, S. and Stelzenmüller, C. (2026) ‘System integration: The key to Europe’s energy trilemma’, Brookings Institution.

[12] European Commission (2025) ‘EU roadmap to end Russian energy imports’, European Commission.

[13] Reuters (2025) ‘EU Parliament approves phaseout of Russian gas imports’, Reuters.

[14] European Commission (2024) ‘AggregateEU: EU Energy Platform and joint gas purchasing mechanism’, European Commission.

[15] European Commission (2024) ‘AggregateEU demand aggregation and joint purchasing results’, European Commission.

[16] ENTSO-E (2024) Ten-Year Network Development Plan 2024, European Network of Transmission System Operators for Electricity.

[17] Neumann, F., Zeyen, E., Victoria, M. and Brown, T. (2022) ‘The potential role of a hydrogen network in Europe’, Joule.

[18] Gross, S. and Stelzenmüller, C. (2026) ‘System integration: The key to Europe’s energy trilemma’, Brookings Institution.

[19] China Daily (2026) ‘UHV corridors set to scale up nation’s power transmission capacity’, China Daily.

[20] China Daily (2026) ‘UHV corridors set to scale up nation’s power transmission capacity’, China Daily.

[21] Reuters (2026) ‘China’s power grid investments to surge to record $574 billion in 2026–2030’, Reuters.

[22] World Economic Forum (2025) ‘China’s unified national electricity market and renewable-energy transition’, World Economic Forum.

[23] Li, Z. and Wang, M. (2025) ‘Allocation of provincial renewable energy power quotas in China: A supply–demand balance perspective’, Energy, 338, 138819.

[24] Global Energy Interconnection Development and Cooperation Organization (2024) Global Energy Interconnection and Clean Energy Transition, GEIDCO.

[25] Center for Strategic and International Studies (2026) ‘What are the implications of the Iran conflict for Japan?’, CSIS.

[26] Reuters (2026) ‘Japan’s Middle East energy dependency — and how it mitigates shocks’, Reuters.

[27] Deutsche Welle (2026) ‘Strait of Hormuz: Iran war threatens Japan and South Korea energy security’, DW.

[28] U.S. Energy Information Administration (2025) ‘The Strait of Hormuz is the world’s most important oil transit chokepoint’, U.S. Energy Information Administration.

[29] International Energy Agency (2024) Oil Stocks of IEA Countries, International Energy Agency.

[30] Nakano, J. (2026) ‘How the Hormuz energy crisis is reshaping US, South Korea, and Japan energy cooperation’, The National Interest.

[31] Reuters (2026) ‘Top Asian LNG markets boost coal use as Iran war limits supply’, Reuters.

[32] The Diplomat (2026) ‘Japan and South Korea’s energy hedge’, The Diplomat.