Iran’s Postwar Settlement: Sanctions Relief, Private-Sector Reopening, and the Political Economy of Regime Survival

Published

1 The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

2 Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

This article argues that the real U.S.-Iran postwar negotiating issue is not whether a ceasefire holds formally but rather who ultimately controls economic reopening in its aftermath. Whereas common scenario analysis treats Gulf security, nuclear verification, sanctions relief, and access through Hormuz as separate strategic variables, they ultimately matter most within the context of Iran's political economy. Whereas some sanctions relief might over time delegitimize the regime by restoring links between private business and Western and Gulf economies, bypassing Chinese channels for oil revenue, and circumscribing the rent-seeking power of sanctions-evading enterprises, the real outcome of a face-saving accord on nuclear terms will be the continuation of the ruling government's coercive powers as long as money flows through state-controlled banks, security enterprises and unofficial exchange systems and the deal is presented as a show of endurance. The article explores three scenarios of postwar deal-making: a protracted Trump win that involves commercially meaningful, if fiscally limited, sanctions relief; a regime win involving economic reopening in which funds are distributed on a controlled basis and with compensation to elites; and an unlikely, although costly, stalemate on verification, Hormuz, and sequencing. Its chief policy recommendation is to treat sanctions relief as a mechanism to shift agency away from Iran's security state toward legitimate private commerce, rather than simply a pause in violence.

1. Introduction - The Political Economy of Iran’s Postwar Settlement

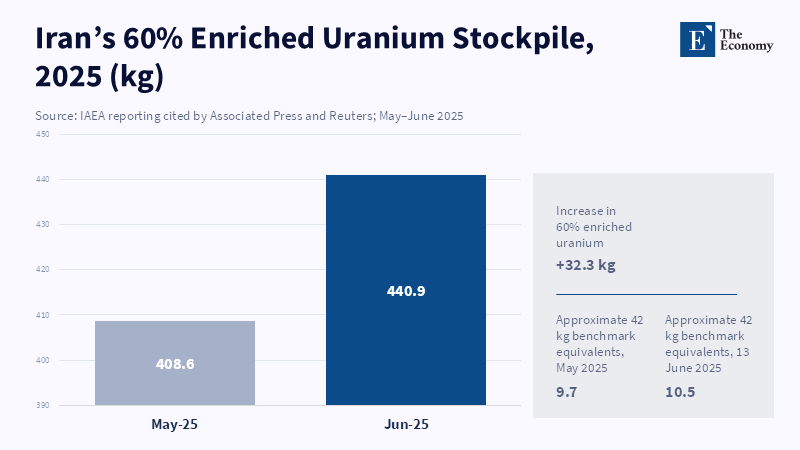

A recent scenario-planning study by the Carnegie Endowment for International Peace correctly argues that the Gulf Cooperation Council remains exposed to the security and economic consequences of the U.S. - Iran conflict.[1] Yet this framing understates the more decisive issue: the political economy of peace inside Iran. Whether Washington and Tehran formalize April's tentative ceasefire is beside the point. Whether the terms of the deal shift the benefits of re-negotiating it among the ruling factions is not. Even if direct military exchanges have paused, the unresolved questions of uranium stockpiles, sanctions relief, frozen assets, and the Strait of Hormuz remain the true architecture of the settlement.[2] Furthermore, attacks on Iran's nuclear sites have seriously compromised nuclear safety and security and raised concerns over a potential radiological release;[3] before the outbreak of hostilities, the latest estimate of total enriched uranium stock by the IAEA was 9,874.9 kg (with 440.9 kg enriched to 60 percent), an issue directly connected to the nuclear question of negotiation.[4] Thus, the issues are not diplomatic technicalities, but are key mechanisms which both parties utilize to assert their desired balance.

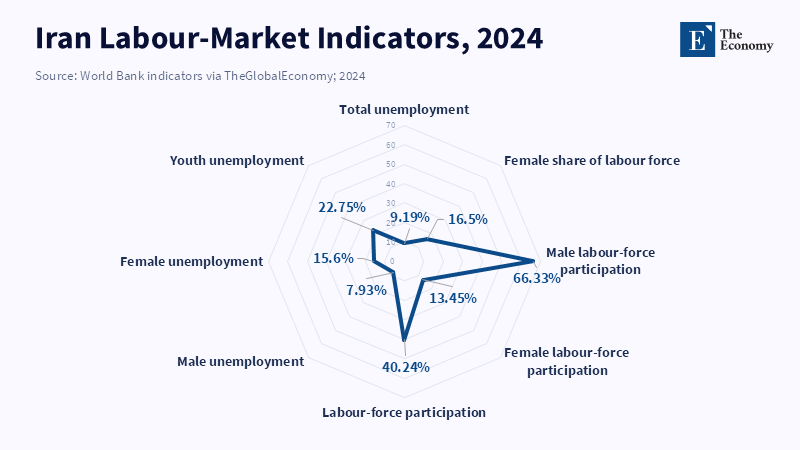

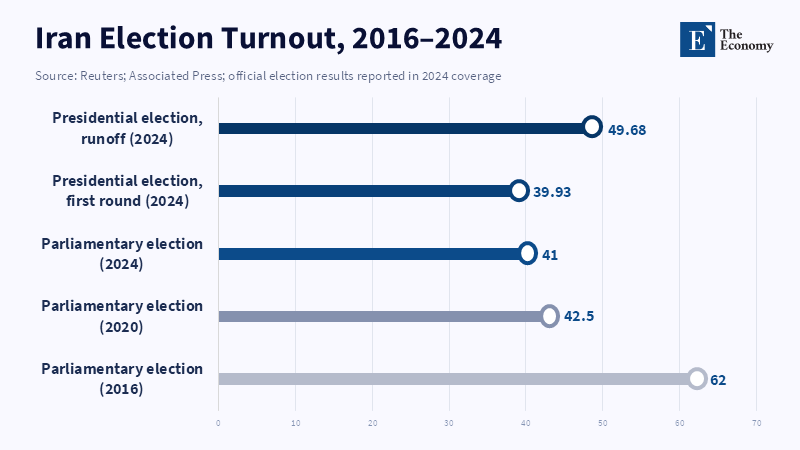

Iran, the subject of current negotiations, has returned not to the nadir nor to the recovering stage of economic policy and management, but to a middle stage, brittle resilience. Although according to World Bank real GDP has risen by 3.8 per cent in 2022-23 and by 5.1 per cent in the first half of 2023-24 thanks to the surge of oil exports and services,[5] GDP per capita has increased by just 2 per cent a year, with significant variations, according to Mahmoudi (2021), suggesting that overall economic growth may obscure deeper problems, including an undercapitalized banking system, illiquidity, unreliable private sector financing and a loss of highly skilled workers, which have remained obstacles to sustainable growth.[6] The official unemployment rate in Iran in March 2024 reached 9.19 percent of the total labor force . In the March 2024 parliamentary elections, voter turnout collapsed to its lowest level since 1979, around 41 percent and similar historic lows marked the first round of the June 2024 presidential election. By February 2025, Reuters documented at least 216 protests regarding wages, prices and delayed payments; large-scale civil unrest has been seen in many cities again at the end of 2025 and early 2026.[7] Therefore, the stability of the regime is not solely dependent on external factors, but also on the domestic political economy.

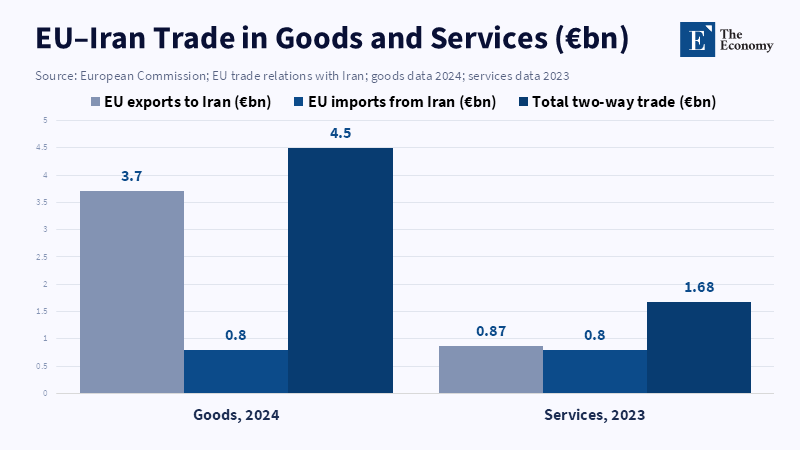

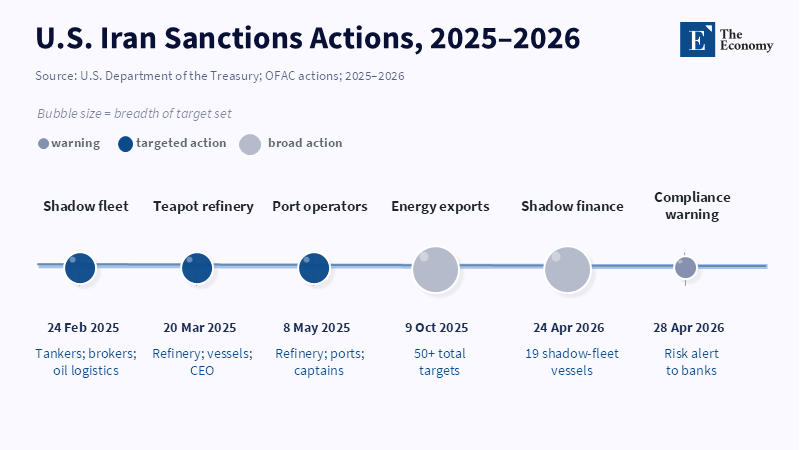

The fragility is important precisely because sanctions, contrary to what they are intended for, created concentration instead of autarchy. From U.S. EIA data nearly 90 percent of Iran's crude oil and condensate exports in 2023 were to China,[8] whereas U.S. EIA analysis of 2025 Chinese imports shows that many shipments that left ports under the label Malaysia were in fact Iranian oil rerouted through China, which the U.S. Treasury Dept has already designated as a primary source of funding for the Iranian regime and its military forces, following a pattern where most sanctioned oil was exported to Chinese "teapot" refineries.[9] According to the EU, total goods trade with Iran in 2024 stood at 4.5 billion, which signifies a very low baseline due to persistent sanctions.[10] Thus, this equilibrium is not a sustainable post-Western path but merely an indicator of how sanctions have concentrated Iran's commerce in a restricted, low visibility path which offers more potential for state control.[11]

This asymmetry has a central implication. A deal that provides minimum direct fiscal gains but a wide opening of legitimate trade, shipping, banking, insurance and private investment in Iran may prove more damaging to the current system over time than a loudly proclaimed diplomatic crisis. Conversely, even with a written restriction on nuclear capabilities, funds routed through state banks, opaque exchange houses and security-related trading entities will reinforce the ruling coalition. In the medium term, the key indicator is not how far Donald Trump capitulated, symbolically, but the rate of reintegration of Iran's private sector into the Western and Gulf markets in relation to the ruling elite's re-assertion of its monopoly on these commercial channels. The question for the future lies in how this dynamic will unfold and it is contingent on factors including the survival rate of the new regime until the end of Trump's term, how quickly Iran's private sector re-engages in established commercial ties and how China and Russia manage to keep or cede influence under the new arrangement according to the specific terms of the deal.

2. Trump’s Win: Sanctions Relief Without Regime Compensation

Under the first outcome, the final deal will deliver Iran none of the substantive reconstruction funds and nothing of the sort of authority over Hormuz transit or substantial domestic political reform in exchange for a release of sanctions or even a minimal opening of frozen funds. It is not a zero-sum, but is certainly close enough to the premise to matter where it will result in lifting commercial, not state cash benefits for Iran. The evidence thus far suggests a limited bargain, rather than normalization, where Iran is only requesting the release of sanctions, external capital and a certain degree of nuclear recognition, and the United States is unwilling to pay a financial price and to maintain that enrichment capacity remains politically intact.[12] If an agreement under these conditions does occur, it will take the form of progressive sanctions relief without replenishment of the state budget.[13]

For the ruling elite in Iran, this will be the worst possible outcome because the country’s reconstruction would be decentralized rather than managed centrally by the current leadership. Iran's domestic and social economies are much more complex than those of simple petro-dependent states and are not easily governed by solely oil revenues.[15] According to World Bank analysis, Iran's non-oil economy-driven primarily by its services and industry sectors-is more diversified than in any other regional state despite sanctions limitations on technology and investment and while official reports state that Iran’s production is likely to be much higher following sanctions relief, the economy cannot rebound overnight and would be dependent on obtaining revived shipping insurance, payment networks and reconnecting with international markets.[15] China's imports of Iranian oil will continue to rise proportionally with sanctions relief, though at a pace dictated by available international buyers and not the leadership in Iran, which will have many other avenues open to them, including a more open European and US commercial sphere and the removal of the price gouging of sanctions-tied intermediaries in Iran. The argument that security forces are the only ones capable of ensuring steady and fluid flows of goods into Iran will crumble as private traders and industries will be allowed legitimate channels for import and services, thus opening possibilities for independent social capital. The Iran that will emerge will therefore not be as beholden to security forces and the political elite as it has been and although this could bring about changes that could include a new, more liberal political system, the ruling elite will have less say in dictating it and will ultimately become less indispensable.

This would be a blow to Iran's shadow economy which at the present time, according to Treasury Department documents, constitutes an intermediary nexus in which shell companies and foreign exchange offices manage cash on behalf of the National Oil Company, IRGC and other security agencies and sanctioned banks.[16] This shadow economy functions as rent paid out to those best able to negotiate with ambiguities of coercion, ambiguity and sanctions evasion. Consequently, removing the discount attached to sanctions will not lead to the enrichment of the Iranian state and ruling elite but will ultimately destabilize the economy, diminishing the usefulness of informal and black market banking and payment systems, decreasing China's purchase discounts and ending the rationale of security forces for overseeing trade.[17] This also goes for Iran's currency of choice. While Iranian negotiators have long stated their preference for their funds being restored along with EU trade and not for being forced to barter, conduct business in yuan and utilize sanctioned illicit finance networks. The growth in non-dollar alternatives is clearly a function of Iran's sanctions-induced isolation and not some inherent geoeconomic realignment on Iran's part.[18]

Under this outcome, Iranian reliance on both China and Russia will start to ebb as Iran will once again have options, not total dependence. Iran currently offers China leverage as it has few other alternatives with which to buy its crude oil, though it is important to note that although Russia has offered bargain prices for Iranian crude as well as structured transactions using off-shore intermediary accounts to deal circumvent Iran's illicit banking networks, its ability to strong-arm certain buyers, like China's independent "teapot" refiners is limited and rather than a boom, Chinese oil imports actually fell to 11.1mbpd in 2024, down 1.8% from 2023's record high of 11.3mbpd.[19] Russia's position is certainly less stable; its economic partnership with Iran with provisions for expansion in oil, intra-bank payment systems and national currency settlements is much smaller than China's and less well established and based on less sound principles.[20] The removal of dependence on sanctions cannot be considered a purely negative outcome for Iran, nor will it necessarily transform Iran into a Western-allied country overnight but it will end the ability for Moscow and Beijing to count on sanctions and illicit networks to maintain dominance over Iran.

It is essential to note here that this shift will primarily be internal and domestic rather than stemming from foreign diplomacy. Stability of the post-war system, particularly after Ali Khamenei's passing, is contingent on the election process of the Assembly of Experts which Khamenei shaped significantly by filtering out reformists and moderates, thus likely ensuring that a conservative leadership, likely focused on security, will ultimately gain control. Although the state might not necessarily collapse (states with coercive control can and do weather legitimacy crises for years), stability will no longer depend solely on coercion and the state's tight grip on resource distribution. As business activity begins to increase along private lines, foreign investment picks up, trade and internet services expand and more generally, the shadow economy begins to disappear in favor of a legitimate commercial sector, state control will begin to erode as it can no longer count on the need for its internal machinations to ensure the supply of goods and the flow of money.[21] Low election turnouts, continuing protests and increasing economic disenfranchisement prove that the ruling elite's main challenge today is not about quelling protest or controlling opinion so much as being unable to actually administer the country for the needs and desires of its population who now see being locked down through sanctions as increasingly costly, not necessary.[22] Ultimately, Trump may not be able to trumpet his victory at the dawn of some public capitulation, but by unlocking the commercial sector of the Iranian state, he may be able to weaken it in an even more significant manner.

The ramifications of this first outcome are thus clear for policymakers in the US, European and Persian Gulf states: To incentivize changes, the lifting of sanctions to bring about legitimate private enterprise should concentrate on verifiable shipping routes, financial sector opportunities, clear legal frameworks and trade finance and insurance rather than large budget allotments or weak supervision over reconstruction funds. At the same time, sanctions must remain on the security forces’ black market intermediary activities to avoid legitimation of the black market's role in pricing Iran’s crude. The Gulf States, particularly those who fear and/or have been victims of maritime and physical threats from Iran, will ultimately want to work towards de-escalation on the maritime sphere and to attempt to incorporate increased Iranian private trade within legitimate global networks and not keep Iran’s commercial economy within its isolated, corrupt black market spheres as it has been for decades. Small-scale "Trump wins" with regard to media visibility can ultimately translate into substantially longer-term gains for the security establishment in the West and its regional partners.

3. Iran’s Current Government’s Win: Face-Saving Concessions and Controlled Reopening

The second outcome described above, while not a "civilizational" win for Iran in any meaningful sense of the term, is indeed a win for the current regime leadership. In this alternative reality scenario, Iran is not awarded a blanket sanctions rollback. Instead, it receives politically useful face-saving measures, such as the appearance of having access to several billion dollars of frozen money, more ambiguity about the sequencing of the sanctions relief, some uncertainty over Iran's future enrichment capacity, or even a "package" benefit that could be internally spun as an acknowledgment of Iran's perseverance through the sanctions, not as a concession given in exchange for nuclear disarmament. This is not merely a theoretical possibility, but one that caused great concern for U.S. allies as well as experienced American negotiators. Even according to April 2026 reports from Reuters regarding Iran's demands for compensation for the war, claims of reparations and the release of its external funds, coupled with the pursuit of nuclear enrichment rights, Western diplomats had already warned that a rapid agreement with a framework deal carried the risk of separating superficial headline terms from carefully constructed sequential sanctions rollback and verification measures.[23] Even without U.S. Assent, the logic of the second scenario remains clear: once the deal is sealed with concessions that can be credibly presented to the Iranian public as reciprocal rather than abject, the internal perception of nuclear disarmament takes on an entirely different dimension.[24] All that would remain would be to determine who gets to articulate the success of the deal, disperse the cash it brings and dictate the terms of its execution.

The second scenario represents the ideal outcome for the current regime because it offers what is likely the most important commodity to any post-war autocratic state after military and political trauma: an independent sphere of control over the country's reconstruction. The detailed analyses of Iran's present-day payment mechanisms by the Treasury Department reveal much about why this is the case.[25] Even now, Iran's annual tens of billions of dollars in commerce transactions are not conducted on an open market; instead, they are handled through complex shadow-banking networks, using currency exchanges, front corporations, shell companies, blacklisted entities, state-run oil exporters and even front entities linked to security institutions. If a sanctions agreement offers only minor sanctions relief without fundamentally altering these institutions, it will not emancipate Iran from its sanctioned existence; rather, it will simply recapitalize it. Money will flow through networks favored by the regime, permits for commercial activity will be issued based on political connections, contracts will be given to allies and money will be drip-fed to ensure business activity is contingent on compliance with state directives. Instead of facilitating Iran's transition away from its current system, the country's economic recovery will become another mechanism of authoritarian integration and control under the regime.[26] The need for Iran to salvage face after agreeing to give up its nuclear leverage will likely make this second scenario even more plausible: in the absence of significant face-saving concessions related to the nuclear program's symbolism, the material concessions and monetary flows will become ever more central and with the regime's allies firmly in control of material distribution, social dependence on the state will only be amplified.

In this second scenario, the private sector is not necessarily excluded; its recovery is instead conditional. This is significant since, as the preceding analysis suggests through World Bank studies and confirmed by recent Reuters reporting on Iran's blackouts, which points to the careful nature of the regime's state management of access, the regime is both seeking to avoid undermining its legitimacy and to mitigate technological vulnerabilities.[27] It is therefore less likely to usher in an open market that risks enabling a free flow of information, external connections and independent capital formation; rather, it will opt for a segmented system of regulated access, allowing only politically privileged firms to resume trade and postponing access for other businesses to markets and supplies. From a technical perspective, the trade and investment picture will improve and this will be welcomed by the United States; however, the process of recovery will be so slow and so uneven that it is unlikely to result in any meaningful change in the political equilibrium. The post-war economy will open partially and strategically, with the state ensuring that only favored parties receive legitimate signals of foreign trade and commerce, not all signals.

China and Russia will be key players in this second scenario, not due to any affection for Iran, but rather because continuing to block a free flow of commerce will maintain their political leverage. Beijing will continue to be Iran's primary oil customer so long as real, political, or ideological constraints on Western buyers persist.[28] China's teapot refineries and shadow banking networks are already critical to Iran's revenue stream and the asymmetrical nature of the 2021 Sino-Iranian agreement means that influence is likely to follow, even if China's promised investments are somewhat delayed.[29] Russia's role will be smaller but still relevant, given the 2025 accord, which pledges increased military cooperation, independent payment systems and settlement in local currencies.[30] If the tempo of U.S. Normalization is dictated by Tehran, the offers made by Russia and China-not necessarily optimal, but offering guaranteed, regulated political stability-will become highly attractive under continued sanctions, leading to a post-war Iran that appears outwardly more open, yet more intimately tied to the very forces that generated its crisis.

This second scenario will bring both positive and negative implications to the region. Despite the high human toll of the war, it is likely that the Islamic Republic's governmental structure remains intact. While access to the International Atomic Energy Agency will continue to be of paramount importance because a face-saving deal is less likely to ensure rigorous verification of Iran's enrichment activities, continued Iranian stonewalling is likely to mean continued restricted access.[31] Gulf states may benefit from a period of relative security, but they will not experience a reordering of regional dynamics. In fact, the fundamental problem remains: a regime with legitimacy has been temporarily reaffirmed by military survival rather than tested by a genuine reform and may feel inclined to exercise a veto over its own reintegration into the global order. The ultimate foreign policy mistake here would not be to be cheated on a specific clause in the deal, but to misunderstand diplomatic completion as true structural change, or worse, to grant Iran access to tangible funds with little oversight, which would empower the coalition that produced the country's crisis to cement its hold on power under the guise of post-war normalization.[32]

4. No Proper Truce: Hormuz Stalemate, Verification Gaps, and Strategic Drift

The third possibility is the indefinite stalemate: either the stalemate has no significant re-initiation of exchanges, but it has merely replaced any genuine cessation with a perfunctory armistice; or more likely still, not simply ended kinetic operations but all mechanisms for nuclear verification, shipping, sanctions and compensation. Least palatable for any one side, least likely outcome to the world, the stalemate cannot be dismissed: the issues are the ones most immutably rooted in sovereignty and the struggle for survival. The ceasefire, as of 8 April according to Reuters, is holding, while the exchange of proposals has never ceased.[33] But Reuters also notes, "Trump's apparent dissatisfaction with Iran's proposals," "Tehran's demand for an end to the US policy," "the proposals to delay nuclear questions earlier in the process, and the shifting from an ambitious comprehensive accord to an interim memorandum." The agreement, if such, can fail not out of unwillingness to compromise, but out of the simple fact that the unresolved items are precisely the ones most intertwined with regime security and deterrence; specifically, enriched uranium disposal and stockpile size, external security assurances, and postwar finances.[34]

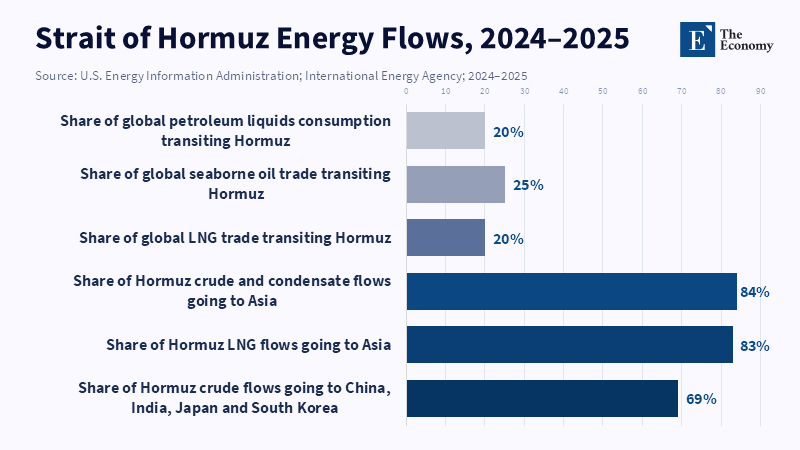

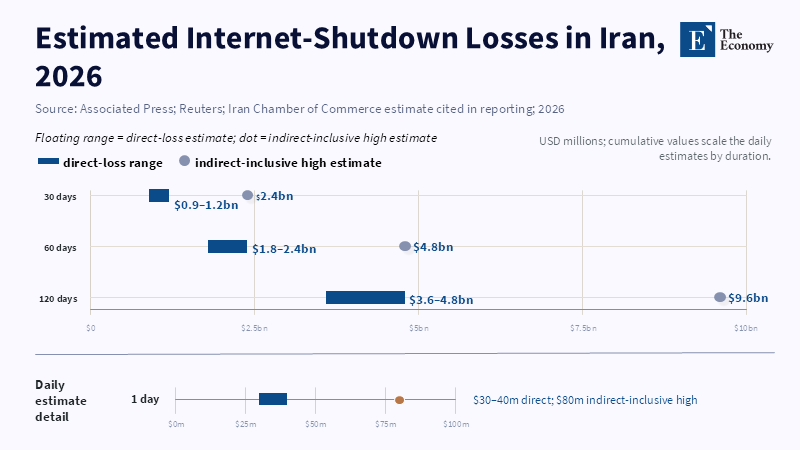

The economic consequences of such a deadlock are already being manifested.[35] The Strait of Hormuz is not merely a waterway: in 2024, roughly 20 million barrels per day of oil moved through it, equivalent to about one-fifth of global petroleum liquids consumption. This, along with the aforementioned increase in benchmarks, has maintained crude over $100 per barrel, as Pentagon estimates already put military spending at $25 billion by late April. The macroeconomic impacts have been most severe for Iran: the World Bank estimated that GDP growth in 2025/26 will be -2.7% as of April 2026, while gross fixed investment fell dramatically, exports declined sharply, the rial lost 44% year-on-year in early March, inflation was running at 62.2% in February, with food inflation at 99% during that month. Thirty-six percent of Iranians have dropped below the upper middle-income poverty threshold, calculated at $8.30/day, the World Bank projected.[36] Beyond macroeconomic factors, individuals are suffering: internet restrictions implemented at the start of the protests continue, albeit selectively lifted through phased access for business during the war, as local economic reports suggest daily losses between $30-40 million, up to $80 million with indirect costs.[37] An end to hostilities, lacking the resolution of these other issues, is effectively just a comprehensive tax on individual existence.

Stalemate therefore, offers no reprieve for the regime itself and no reduction in stakes; while the scarcity of oil continues to offer them leverage, and the clandestine nature of the deal permits the Chinese some negotiation with Iran, the pressure for reform domestically, inevitable if this situation continues, will only increase. This is problematic for China, which has strongly lobbied for the immediate reopening of Hormuz and has no interest in the prolonged risks to shipping and oil-price volatility inherent in the status quo. Treasury attempts to stem Iranian circumvention of sanctions have increased significantly, and as of February 2025, the administration has designated over 1,000 individuals, vessels and aircraft involved with Iran as part of a "maximum pressure" campaign.[38] While Russia provides diplomatic assistance and alternative financial channels, per the terms of a bilateral treaty, its actual economic influence over Iran is relatively negligible.[39] The Arab States of the Persian Gulf are unlikely to permit continued deadlock either: as of Carnegie's March 2026 analysis, all six GCC states are inherently tied to the war's security consequences, and thus possess obvious incentives to coordinate further among themselves.[40] Reuters has noted efforts to coordinate an international coalition to restore freedom of navigation. The push to agreement, therefore, comes not just from Washington and Tehran but also from energy markets, Arab commercial interests, and China's concern for shipping costs.

The greatest argument against this scenario is that absolutely no party will accept it; Trump would claim a failed bargain and no resolution to the proliferation problem. Iran, with severe economic and internal needs, can afford no prolonged lack of funds. China, desperate for reliable seaborne energy, cannot afford continued risks and volatility in the same vein; as can, the Arab States, for pragmatic economic reasons. Iran itself has also failed to secure a settlement on terms it can fully negotiate to establish a deal when it could, and while it cannot afford to accept a stalemate indefinitely, it cannot afford any resolution other than the one immediately implemented or its functional equivalent. The IAEA is now on record warning that credible verification requires renewed access to Iran's nuclear sites and stockpiles.[41] The result is a situation in which the legal and ethical foundations of non-proliferation are temporarily weakened by the technical difficulty of verification. The highest attainable deal then would seem to be an enforceable, albeit limited one: prompt reopening of shipping lanes, renewed IAEA access and rigidly enforced, retractable intermediate ceilings on enrichment levels, stockpile sizes and sanctions relief. Anything short may just legitimize the stalemate.[42]

5. Conclusion - The Real Test Is Who Controls Reopening

The standard test for assessing the postwar diplomacy-whether Trump achieved evident capitulation or whether Iran retained sufficient face for resilience-frames the issue wrongly. Sanctions relief cannot be a mere political reward, but rather a process to redistribute domestic political power and wealth in Iran. Narrow on the fiscal and broad on the commercially meaningful, sanctions relief can expand the arena for private commerce, decrease rents enjoyed by shadow banking and oil-on-discount dependencies and, in doing so, diminish incrementally state control over society and the external pressures of China and Russia.[43] Narrow on the commercially meaningful and broad on the fiscal, it can reinforce the coercive state much faster than it supports autonomous markets, strengthening the governing regime even after the military shock it has weathered. Without legitimate terms, all parties will likely find themselves saddled with an expensive, unpredictable stalemate in which the gaps between promises and performance, oil instability and domestic suffering compound. The policy question is, accordingly, remarkably straightforward: any accord should be framed to recover the nuclear component verifiably, allow for the return of legitimate private commerce and restrict state institutions with security links to controlling the gains from this new era.[44] An accord that falls short of appearances might succeed far more durably on this latter account than one that exceeds them.

References

[1] Leber, A. and Worby, S. (2026). ‘Three Scenarios for the Gulf States After the Iran War’. Carnegie Endowment for International Peace, 16 April.

[2] Liptak, K. (2026). ‘Deadlock on Strait of Hormuz and Iran’s nuclear stockpile led to impasse, officials say’. CNN, 12 April.

[3] Grossi, R. M. (2025). ‘IAEA Director General Grossi’s Statement to UNSC on Situation in Iran’. International Atomic Energy Agency, 20 June.

[4] International Atomic Energy Agency (2026). Verification and monitoring in the Islamic Republic of Iran in light of United Nations Security Council resolution 2231.

[5] World Bank (2024). Iran Economic Monitor: Sustaining Growth Amidst Global Uncertainty.

[6] Spruk, R. (2026). ‘Confrontation with the West and Long-Run Economic and Institutional Outcomes: Evidence from Iran’. arXiv:2602.03231.

[7] Amnesty International (2026). ‘Iran: Deaths and injuries rise amid authorities’ renewed cycle of protest bloodshed’. 8 January.

[8] U.S. Energy Information Administration (2024). Iran Country Analysis Brief.

[9] U.S. Department of the Treasury (2025). ‘Treasury Imposes Additional Sanctions on Iran’s Shadow Fleet as Part of Maximum Pressure Campaign’. 24 February.

[10] European Commission (2025). ‘EU trade relations with Iran’. Directorate-General for Trade.

[11] Mirramezani, M. and Samani, S. (2026). ‘Iran’s Exports Under Sanctions: The Myth of Maximum Pressure’. Stanford Iran 2040 Project.

[12] Reuters (2026). Reporting on U.S.-Iran negotiations, sanctions relief, frozen assets, enrichment demands and Hormuz negotiations, April–May.

[13] U.S. Department of the Treasury (2026). OFAC Iran sanctions actions and Hormuz-related sanctions guidance, May.

[14] World Bank (2024). Iran Economic Monitor: Sustaining Growth Amidst Global Uncertainty; U.S. Energy Information Administration (2024). Iran Country Analysis Brief.

[15] Raynor, B. (2022). ‘The shadow of sanctions: reputational risk, financial reintegration, and the political economy of sanctions relief’. International Relations, 28(3).

[16] U.S. Department of the Treasury (2026). ‘Economic Fury Targets Global Network Fueling Iran’s Oil Trade and Shadow Fleet’. 24 April.

[17] Mirramezani, M. and Samani, S. (2026). ‘Iran’s Exports Under Sanctions: The Myth of Maximum Pressure’. Stanford Iran 2040 Project; Pokorny, L. (2026). The Economics of Sanctions Evasion Through Proxy Networks: Iranian Proxy Groups as Economic Pressure Release Valves. Zenodo.

[18] Babaev, K. V. (2025). ‘Mutual payments between Russian and Chinese banks: a geoeconomic aspect’. Economy of Regions, 21(3), pp. 703–715.

[19] U.S. Energy Information Administration (2024). Iran Country Analysis Brief; U.S. Department of the Treasury (2025). ‘Treasury Increases Pressure on Firms Importing Iranian Oil’. 8 May.

[20] Shkvarya, L. V. (2022). ‘Russian-Iranian trade and economic relations at the present stage and directions of their development’. Innovative Economy, 9(4).

[21] Spruk, R. (2026). ‘Confrontation with the West and Long-Run Economic and Institutional Outcomes: Evidence from Iran’. arXiv:2602.03231; Raynor, B. (2022). ‘The shadow of sanctions’.

[22] Associated Press (2026). ‘Iran's monthslong internet shutdown is crushing businesses in an already battered economy’. 1 May; Amnesty International (2026). ‘Iran: Deaths and injuries rise amid authorities’ renewed cycle of protest bloodshed’.

[23] Liptak, K. (2026). ‘Deadlock on Strait of Hormuz and Iran’s nuclear stockpile led to impasse, officials say’. CNN, 12 April.

[24] Grossi, R. M. (2025). ‘IAEA Director General Grossi’s Statement to UNSC on Situation in Iran’; Leber, A. and Worby, S. (2026). ‘Three Scenarios for the Gulf States After the Iran War’.

[25] U.S. Department of the Treasury (2026). ‘Economic Fury Targets Global Network Fueling Iran’s Oil Trade and Shadow Fleet’. 24 April.

[26] Pokorny, L. (2026). The Economics of Sanctions Evasion Through Proxy Networks; Spruk, R. (2026). ‘Confrontation with the West and Long-Run Economic and Institutional Outcomes’.

[27] Aceto, G., Persico, V. and Pescapè, A. (2026). ‘Iran's January 2026 Internet Shutdown: Public Data, Censorship Methods, and Circumvention Techniques’. arXiv:2603.28753; Associated Press (2026). ‘Iran's monthslong internet shutdown is crushing businesses in an already battered economy’.

[28] U.S. Energy Information Administration (2024). Iran Country Analysis Brief; U.S. Department of the Treasury (2025). ‘Treasury Increases Pressure on Firms Importing Iranian Oil’. 8 May.

[29] U.S.-China Economic and Security Review Commission (n.d.). ‘China-Iran Relations: A Limited but Enduring Strategic Partnership’.

[30] Russia-Islamic World Strategic Vision Group (2025). ‘Russia and Iran Plan to Fully Integrate Payment Systems by End of 2025’; Babaev, K. V. (2025). ‘Mutual payments between Russian and Chinese banks’; Shkvarya, L. V. (2022). ‘Russian-Iranian trade and economic relations’.

[31] International Atomic Energy Agency (2026). Verification and monitoring in the Islamic Republic of Iran.

[32] U.S. Department of the Treasury (2026). ‘Economic Fury Targets Global Network Fueling Iran’s Oil Trade and Shadow Fleet’; Pokorny, L. (2026); Mirramezani, M. and Samani, S. (2026); Raynor, B. (2022).

[33] Reuters (2026). Reporting on U.S.-Iran ceasefire and negotiations, April–May.

[34] Liptak, K. (2026). ‘Deadlock on Strait of Hormuz and Iran’s nuclear stockpile led to impasse’; International Atomic Energy Agency (2026). Verification and monitoring in the Islamic Republic of Iran.

[35] United Nations Development Programme (2026). ‘Military Escalation in the Middle East: Economic and Social Implications for the Arab States Region Assessment’.

[36] World Bank (2026). Iran macroeconomic and conflict-impact outlook; United Nations Development Programme (2026). ‘Military Escalation in the Middle East: Impact Analyses’.

[37] Associated Press (2026). ‘Iran's monthslong internet shutdown is crushing businesses in an already battered economy’; Reuters (2026). ‘Iran eases internet curbs for businesses as blackout enters third month’.

[38] U.S. Department of the Treasury (2026). ‘Economic Fury Targets Global Network Fueling Iran’s Oil Trade and Shadow Fleet’. 24 April.

[39] Shkvarya, L. V. (2022). ‘Russian-Iranian trade and economic relations’; Russia-Islamic World Strategic Vision Group (2025). ‘Russia and Iran Plan to Fully Integrate Payment Systems by End of 2025’.

[40] Leber, A. and Worby, S. (2026). ‘Three Scenarios for the Gulf States After the Iran War’; United Nations Development Programme (2026). ‘Military Escalation in the Middle East: Economic and Social Implications for the Arab States Region Assessment’.

[41] International Atomic Energy Agency (2026). Verification and monitoring in the Islamic Republic of Iran.

[42] International Atomic Energy Agency (2026); Leber, A. and Worby, S. (2026); U.S. Department of the Treasury (2026); Raynor, B. (2022).

[43] Mirramezani, M. and Samani, S. (2026). ‘Iran’s Exports Under Sanctions’; U.S. Department of the Treasury (2026); U.S. Energy Information Administration (2024).

[44] Pokorny, L. (2026). The Economics of Sanctions Evasion Through Proxy Networks; U.S. Department of the Treasury (2026); Raynor, B. (2022); Spruk, R. (2026).