[Fed Watch] Stagflation Emerges as the Cost of Sustaining U.S. Hegemony, Rate-Cut Expectations Fade

Authored On

Modified

Stagflation Fears Rise Amid Persistent High Oil Prices Prolongation Implies High Inflation and Economic Slowdown Monetary Policy at an Impasse, Rate Cuts Effectively Off the Table

The Iran war is destabilizing the equilibrium of the U.S. macroeconomic environment. As the conflict drags on, mounting pressure on energy supply chains is simultaneously fueling inflationary resurgence and upward pressure on interest rates. Financial markets, likewise, are increasingly pricing in the risk of stagflation—a combination of economic stagnation and rising prices—amid concerns over asset price corrections and prolonged monetary tightening. This trajectory underscores how the costs of maintaining U.S. global hegemony are being transmitted across both the real economy and financial markets.

Inflation and Rate Pressures Intensify if Iran War Prolongs

On the 6th (local time), according to The Wall Street Journal (WSJ) and the Financial Times (FT), JPMorgan Chase CEO Jamie Dimon warned in his 48-page annual shareholder letter that the Iran war could trigger rising inflation and a downturn in financial markets in the United States. Dimon stated, “There is a risk that shocks to oil and commodity prices will persist over the coming months,” adding, “This could lead to sustained inflation and ultimately result in higher interest rates.”

He likened inflation to a “skunk at the party,” warning that geopolitical conflicts, including the war with Iran, could drive up energy prices, thereby undermining expectations for Federal Reserve (Fed) rate cuts and potentially forcing further rate hikes. Dimon emphasized, “The greatest risk that could materialize in 2026 is a gradual rise in inflation,” noting that “this factor alone could lead to higher interest rates and falling asset prices.”

Dimon also unveiled an “economic security enhancement” strategy involving an investment of $1.5 trillion to reinforce strategic industries in order to safeguard U.S. economic and military hegemony. At the core of this initiative is the “Security and Resiliency Initiative,” launched in October of last year. JPMorgan plans to allocate a total of $1.5 trillion over the next decade to intensively support sectors directly tied to U.S. economic security. Market participants interpret this as a strategic effort to bolster U.S. self-sufficiency amid the restructuring of global supply chains, effectively constructing an “economic fortress” capable of withstanding external shocks.

Dimon further referenced historical episodes from the 1970s and 1980s, when sharp increases in oil prices precipitated severe recessions, while assessing that the current U.S. economy is less vulnerable to such shocks than in the past. Nevertheless, he delivered a stark warning, stating, “Success is not a birthright,” underscoring both geopolitical risks and internal economic fragilities facing the United States.

Rising Probability of War-Induced Stagflation

In practice, concerns over stagflation are gaining traction in the United States as the Iran war prolongs. Surging prices for oil, natural gas, and other energy sources are simultaneously driving up production costs—fueling inflation—while eroding consumer purchasing power, thereby intensifying downward pressure on economic growth. Although Federal Reserve Chair Jerome Powell dismissed such concerns, stating, “I prefer to reserve the term ‘stagflation’ for the conditions of that era (the 1970s),” markets have already begun signaling warnings of an impending downturn.

Experts caution that the scale of the current shock is historically unprecedented. Fatih Birol, Executive Director of the International Energy Agency (IEA), remarked that the present crisis is comparable to a combination of the two oil shocks of the 1970s and the gas supply disruption following Russia’s invasion of Ukraine in 2022. Prolonged disruption in the Strait of Hormuz could extend beyond oil and gas to destabilize supply chains for petrochemical products such as fertilizers, helium, and sulfur. Such energy supply shocks are rapidly transmitted into consumer prices. Rising oil and commodity prices erode corporate profitability for firms that process raw materials or import goods for resale. As profitability deteriorates, companies pass on higher costs to consumers, creating a feedback loop that accelerates inflation.

Even under optimistic scenarios, economists expect the U.S. economy to struggle to avoid inflationary pressures. It is widely accepted in economic literature that a sustained $10 increase in oil prices per barrel raises inflation by approximately 0.3 to 0.4 percentage points. Nobel laureate Joseph Stiglitz of Columbia University similarly warned, “Prices are rising first due to tariffs and now due to war, while growth is slowing,” emphasizing that the U.S. economy faces a tangible risk of stagflation.

Compounding the situation, the financial fragility of U.S. consumers further constrains shock absorption capacity. According to a December survey by Bankrate, only 47% of Americans reported having emergency savings sufficient to cover an unexpected $1,000 expense. Meanwhile, 29% indicated that their credit card debt exceeds their emergency savings. Even borrowers with strong credit profiles face annual credit card interest rates approaching 20%. Consumer sentiment has also deteriorated sharply. The University of Michigan’s Consumer Sentiment Index fell to 51 in November of last year—near historical lows—before partially recovering, only to decline again to 55.5 in a preliminary March reading, marking the lowest level of the year.

Necessity of Maintaining a Tightening Stance

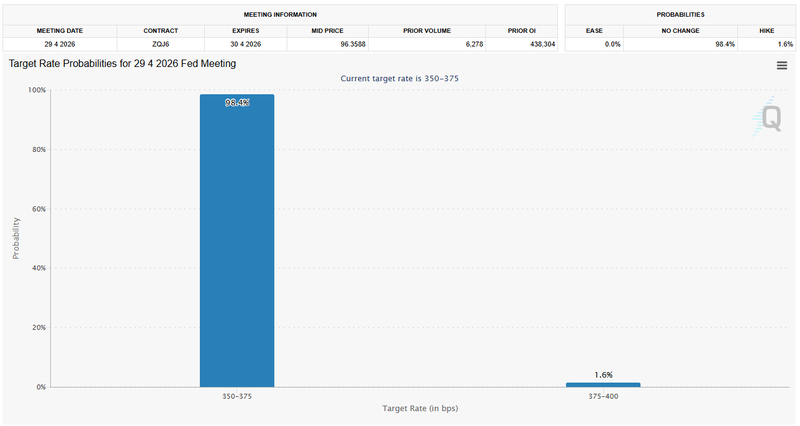

These macroeconomic shifts are rapidly constraining the Federal Reserve’s policy options. With surging energy prices fueling inflation, the scope for rate cuts has effectively vanished, while the likelihood of prolonged monetary tightening to contain price pressures is increasing. According to CME’s FedWatch, the probability that the Federal Open Market Committee (FOMC) will hold rates steady at the current range of 3.50% to 3.75% at its upcoming meeting on the 28th–29th stands at 98.4%. The probability of a 25 basis point hike is only 1.6%. As inflation concerns driven by rising oil prices intensify, market expectations for Fed rate cuts are rapidly eroding.

Federal Reserve officials have also recently characterized the inflation outlook as being in a “warning phase,” signaling the need to maintain a tightening stance. Chicago Fed President Austan Goolsbee and Cleveland Fed President Beth Hammack, appearing jointly on NPR’s economic podcast on the 6th, described inflation as being at an “orange” level when asked to assess the current economic conditions using a color scale—one notch below the highest “red” crisis level, yet above the “yellow” caution level.

Goolsbee stated, “There had been optimism that inflation would return to the 2% target, but it has recently worsened again,” adding that “the trajectory is moving from orange toward red.” He particularly noted that tariff-driven price increases have persisted longer than expected, while rising energy prices due to the Iran war are acting as an additional stagflationary shock. Hammack similarly assessed inflation as being at a “deeper orange” level, stating, “Inflation remains above target and has been stagnant for an extended period.” She added that while a weakening labor market could justify rate cuts, “if inflation persistently exceeds our 2% target, rate hikes may be necessary.”

Economists interpret these developments as the manifestation of the costs associated with maintaining U.S. global hegemony through the financial system. The expenses incurred in managing geopolitical conflicts and controlling energy supply chains are being transmitted in the form of higher interest rates and increased asset price volatility. The critical issue lies in the global diffusion of these costs. Elevated interest rates trigger capital outflows and financial instability in emerging markets, exacerbating the global economic slowdown. Simultaneously, rising living costs and declining real incomes amplify social tensions, potentially undermining the long-term legitimacy of hegemonic power itself.

Similar Post