“PCE and PPI Are Climbing, Yet…” Warsh’s Focus on Trimmed Mean Inflation Fuels Case for Rate Hold Amid Conflicting Signals

Authored On

Modified

Kevin Warsh, the newly appointed Chair of the Federal Reserve, highlights the importance of the trimmed mean inflation measure Relatively stable trimmed mean inflation contrasts with surging PCE and PPI readings Divergent inflation indicators strengthen Wall Street expectations for an extended rate pause

Kevin Warsh, the newly appointed Chair of the U.S. Federal Reserve (Fed), has argued that policymakers should place greater emphasis on alternative inflation measures rather than relying solely on traditional gauges. Specifically, he has shifted attention away from core Personal Consumption Expenditures (PCE), long regarded as the Fed’s primary benchmark for monetary policy decisions, and toward the “trimmed mean” inflation measure. Critics, however, contend that the methodology behind the indicator is excessively subjective. While the trimmed mean inflation index has remained relatively stable, major inflation gauges, including PCE, have shown a pronounced upward trajectory since the outbreak of the Iran conflict. As multiple inflation indicators deliver conflicting signals, Wall Street is increasingly coalescing around the view that the Fed is likely to keep interest rates unchanged for the foreseeable future while monitoring developments.

Focus on Underlying Inflation

According to a Wall Street Journal (WSJ) report published on May 31, Warsh stated during a recent Senate confirmation hearing that “underlying inflation matters more than one-off shocks stemming from geopolitical developments or fluctuations in beef prices.” He argued that traditional inflation measures are “rough estimates” that incorporate too many temporary price distortions and that greater attention should be paid to trimmed mean inflation indicators. While Fed officials already consider a range of supplementary inflation metrics, it is highly unusual for a Fed chair to publicly emphasize the significance of the trimmed mean measure.

The trimmed mean inflation index is calculated by excluding the items that experienced the largest price increases and the steepest price declines during a given period, then averaging the remaining categories. Under current market conditions, for example, it effectively removes sharp increases in import prices caused by tariffs and energy price spikes resulting from the Middle East conflict, focusing instead on longer-term inflation trends. The metric is designed to identify the trajectory of underlying inflation rather than short-term volatility. The Dallas Federal Reserve’s trimmed mean inflation gauge recently showed a 12-month increase of approximately 2.3%, close to the Fed’s 2% target.

Dovish policymakers within the Fed have cited the trimmed mean measure in pushing back against calls for tighter monetary policy. Speaking at a conference in Reykjavik, Iceland, on May 29, Fed Governor Michelle Bowman stated that “adjusting monetary policy in response to temporarily elevated energy inflation could result in unnecessary policy tightening and impose unwarranted burdens on economic activity and labor market conditions.” Her remarks reflected the view that indicators measuring underlying inflation remain relatively stable and that inflationary pressures driven by energy prices should not be overstated.

Clear Upward Trend in Traditional Inflation Indicators

Many traditional economists, however, remain skeptical of the trimmed mean approach. They argue that excluding certain components that contribute to inflation amounts to little more than “removing numbers one does not like.” Critics warn that once exceptions are introduced into the calculation process, it becomes increasingly unclear which inflation indicators markets should trust. Notably, most major U.S. inflation gauges outside the trimmed mean framework have traced a distinctly upward path since the outbreak of the Iran conflict.

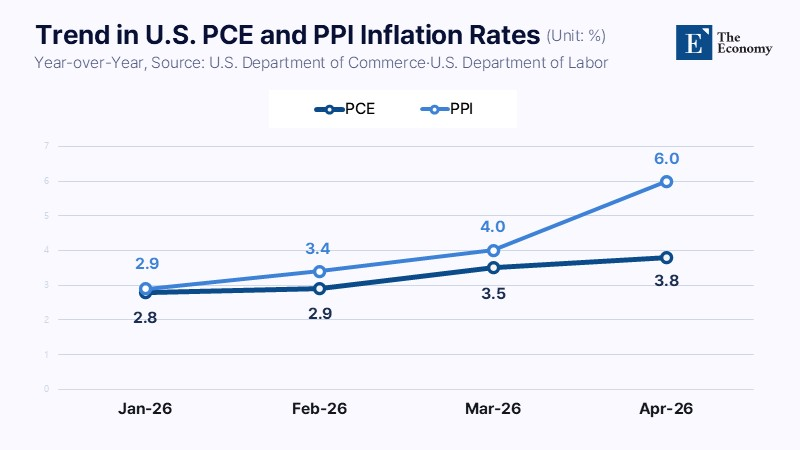

PCE offers a prime example. Designed to reflect changing consumption patterns more quickly than the Consumer Price Index (CPI), PCE employs more frequently adjusted weightings and has accelerated sharply since tensions erupted in the Middle East. According to data released by the U.S. Department of Commerce on May 28, the April PCE price index rose 3.8% year over year, marking the highest increase since May 2023, when it reached 4.0%. Core PCE, which excludes food and energy, climbed 3.3% from a year earlier, its strongest reading since October 2023.

Producer Price Index (PPI) data for the same month also showed a seasonally adjusted monthly increase of 1.4%. This represented the largest monthly gain since March 2022, when PPI rose 1.7%, and significantly exceeded the Dow Jones consensus estimate of 0.5%. The increase was driven primarily by surging energy prices linked to the Middle East conflict. Prices for final-demand goods advanced 2.0% month over month, with more than three-quarters of that increase attributed to higher energy costs. Gasoline prices surged 15.6% in a single month, while jet fuel and diesel prices also posted substantial gains. Prices for industrial chemical products likewise moved higher.

Limited Likelihood of Near-Term Monetary Policy Adjustments

Despite the conflicting signals emanating from various inflation indicators, markets generally believe that Warsh is unlikely to alter monetary policy in the near term. Analysts argue that his broader objective is not monetary easing but a reduction in the Federal Reserve’s overall role in financial markets. Warsh has repeatedly criticized the Fed for expanding its mandate excessively during the global financial crisis and the COVID-19 pandemic under the banner of market stabilization and economic support. He argues that emergency measures such as large-scale quantitative easing (QE) became entrenched as permanent policy tools, effectively transforming the Fed into a backstop for financial markets while weakening its core responsibility of maintaining price stability. Warsh has also been a prominent advocate for shrinking the Fed’s balance sheet, contending that repeated interventions to supply liquidity and support asset prices have fostered excessive dependence on the central bank among both governments and market participants.

Wall Street has increasingly embraced the outlook for an extended rate hold. In a recent report, JPMorgan stated that “policy continuity is likely to prevail in the short term even under a Warsh-led Federal Reserve.” Although energy prices have surged because of Middle East risks, the bank expects the Fed to maintain a wait-and-see stance and keep benchmark interest rates unchanged throughout the year. Michael Feroli, JPMorgan’s chief U.S. economist, noted that “core inflation remains relatively stable despite elevated oil prices, and the labor market has proven more resilient than expected,” adding that these conditions provide ample justification for the Fed to keep rates unchanged.

Major global banks including HSBC, BNP Paribas, and Standard Chartered have likewise projected no additional rate cuts this year. HSBC expects the Fed to leave rates unchanged, arguing that energy price increases linked to Middle East tensions could accelerate inflation. BNP Paribas has also assigned a low probability to further rate cuts, citing inflationary pressures stemming from tariffs and higher oil prices. Standard Chartered forecasts that the Fed will maintain current interest rate levels for an extended period, supported by a resilient labor market and persistent inflation in the services sector.

Similar Post