"Inflation Risks Are Mounting" Rate-Cut Expectations Fade Under the Warsh Fed as Bond Markets Already Price In Tightening

Authored On

Modified

Fed Officials Converge Around Hawkish Consensus: "Price Stability Comes First" Expectations for Policy Easing Under the Warsh Fed Lose Momentum Bond Markets Move Ahead of Policy Rates as Major-Economy Long-Term Yields Trace an Upward Curve

Officials at the U.S. Federal Reserve have delivered a succession of hawkish remarks. Expectations for interest-rate cuts that had emerged with the inauguration of new Fed Chair Kevin Warsh are rapidly losing force amid concerns over a renewed flare-up in inflation. Investors are already moving to price out the possibility of monetary easing, while bond markets are lifting long-term Treasury yields by preemptively reflecting inflation risks ahead of any adjustment in policy rates.

Hawkish Messages From Fed Officials

On May 28, local time, Fed Vice Chair Philip Jefferson said at the Bank of Japan-IMES Conference in Tokyo that the U.S. economy has maintained solid growth despite the recent surge in energy prices. He explained that as expanded investment in artificial intelligence creates a new growth engine, the Fed is closely monitoring “second-round effects” on inflation expectations and wages rather than focusing solely on energy prices themselves. Jefferson added that while the scale and duration of the war-driven energy shock make it difficult to determine the rate path with certainty, the Fed can remain focused on achieving its 2% inflation target given the resilience of the labor market.

That same day, Minneapolis Federal Reserve Bank President Neel Kashkari expressed a similar view in an interview with CNBC. “U.S. inflation has remained above the Fed’s 2% target for more than five years, but the labor market is still solid,” he said, adding that “price stability remains the top priority.” He also warned that if elevated inflation persists for an extended period, households’ and businesses’ inflation expectations could rise, entrenching price pressures. Fed Governor Christopher Waller, long regarded as one of the central bank’s leading doves, also said in a recent speech in Frankfurt, Germany, that he “would not rule out the possibility of rate hikes if inflation does not ease soon.”

Fed Governor Lisa Cook also said the previous day at an AI policy forum hosted by the Stanford Institute for Economic Policy Research that “the risks around inflation clearly remain elevated” and that the Fed is “prepared to raise rates if disinflation does not emerge in a timely manner.” One factor cited as amplifying inflation risks is AI investment approaching $1.5 trillion. If the AI investment boom pushes up prices for semiconductors, advanced equipment and related inputs, inflationary momentum could accelerate further, she said. Cook noted that “holding rates steady for the time being is appropriate because inflation is expected to slow in the coming months,” but warned that if inflation remains above the Fed’s 2% target for five years, price increases could become embedded in both prices and wages.

Low Probability of Rate Cuts in the Near Term

With the Fed’s internal hawkish tilt becoming increasingly pronounced, market attention is turning to the June Federal Open Market Committee meeting, the first to be chaired by Warsh. He was personally nominated by U.S. President Donald Trump, who has persistently pressed the Fed to cut rates. Warsh himself had criticized the monetary policy stance under Jerome Powell even before taking office and had previously argued for the need to lower rates. That history helped foster expectations that the Fed could adopt a more accommodative policy stance under his leadership.

However, the recent sharp deterioration in inflation indicators has effectively rendered those expectations meaningless. After the U.S. personal consumption expenditures price index rose 3.8% year on year last month, marking its highest level in nearly three years, views that additional tightening could soon be implemented began to gain traction. According to CME FedWatch, investors are pricing in a 98.9% probability that rates will remain unchanged at the June FOMC meeting. Even looking toward year-end, the probability of rate cuts is near zero, with market expectations concentrated on either a hold at 47.4% or an additional hike at 52.1%.

Analysts also broadly assess that Warsh is not the “rate-cut advocate” markets had expected. Their view is that his objective is to reduce the Fed’s role itself, rather than to ease monetary policy. Warsh has argued that the Fed excessively expanded its role in stabilizing markets and supporting the economy after the global financial crisis and the COVID-19 pandemic, and that it should focus on its core mandate of price stability rather than financial-market support. Under current conditions, with inflation risks intensifying, the likelihood that a Warsh-led Fed will deliver an accommodative monetary policy is low. Warsh recently said that shrinking the balance sheet through quantitative tightening could raise long-term rates and create room to lower short-term policy rates. That is better understood as a shift in the form of tightening rather than a genuine rate cut.

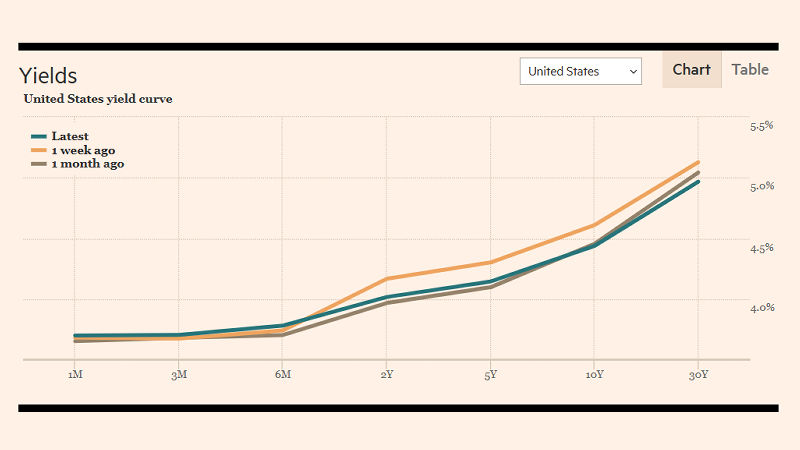

Clear Tightening Signals From Bond Markets

Bond markets are also showing a clear rise in long-term yields. The U.S. 10-year Treasury yield recently climbed to around 4.5%, its highest level in roughly a year, while the 30-year yield briefly surpassed 5%. In contrast to the past, when Fed policy rates determined the broad direction of financial markets, bond markets are now moving first to price in risk factors. One financial industry official said, “In the past, markets followed when the Fed moved rates, but now markets are moving long-term yields first and effectively setting a benchmark,” adding that “if this trend continues, an era may arrive in which market rates matter more than policy rates.”

This trend is not confined to the United States. In Japan, selling pressure in super-long government bonds has continued, sending 30-year and 40-year yields to record highs, while long-term gilt yields in the United Kingdom have also remained elevated. In Japan, expectations that the Bank of Japan could reduce government bond purchases have fueled the rise in long-term yields, while in the United Kingdom, concerns over widening fiscal deficits have added upward pressure. As in the United States, market risk factors are being priced in before central banks set their policy direction.

The upward pressure on market rates is also exerting a meaningful influence on monetary policy across countries. The BOJ continues to signal the possibility of additional rate hikes, while the Bank of England has begun to adopt a more hawkish stance after moving through a rate-cut cycle. Emerging economies are also adjusting monetary policy amid dollar strength and capital outflow pressure triggered by rising long-term yields. Indonesia, Southeast Asia’s largest economy, raised its policy rate by 0.5 percentage point to 5.25% on May 20, marking its first shift in policy stance in two years, while the Philippines lifted its policy rate by 0.25 percentage point last month.

- Previous Following the UK and Switzerland, France Extends Public Insurance Coverage to Wegovy and Mounjaro, Marking a Paradigm Shift From ‘Personal Responsibility’ to ‘Treatable Disease’

- Next "From Fines to M&A Roadblocks" EU Raises Regulatory Barriers Against Chinese Companies While Loosening Restrictions on Intra-European M&A

Similar Post