The Limits of Pillar Two: Heterogeneous Responses to the Global Minimum Tax Across Countries and Firms

Published

1 The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

2 Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

The aim of the global minimum tax was to establish a floor on international tax competition by eroding the advantages of shifting profits and of zero-tax states. But the unfolding practice of Pillar Two reveals that identical statutory rules do not lead to identical results. We claim that the success of the global minimum tax has less to do with equal statutory rates and more to do with varying responses of firms and states. In particular, cross-country differences in tax system design, enforcement capacity, industrial structure, and dependence on mobile multinational capital mean that the same change in tax rates produces very different consequences for revenues, investment, and welfare. These discrepancies are not marginal - they are central to understanding the true challenges of coordinated tax reform, particularly in light of the U.S. reducing its engagement.

The argument proceeds in three steps. First, we explore how diverse jurisdictions react in very different ways in terms of their tax bases and how firms anchored in the domestic economy respond differently from highly mobile, intangible-heavy multinationals. Second, we show, using recent evidence, how the global minimum tax impacts not just the observed income, but also the cost of capital, investment incentives, and welfare, leading to significant differentials between larger and smaller economies. Third, we claim that tax competition should not be seen in terms of tax rates any longer, given how geopolitical risk, legal security, governance quality, and access to markets have become determinants for where capital is invested. The primary takeaway is that sustainable tax coordination needs not a common minimum but differentiated implementation through domestic institutions, robust enforcement, and an enriched analysis of those non-tax conditions that drive international capital mobility.

1. Introduction - The Global Minimum Tax Beyond Rate Harmonisation

For decades, countries sought to contain excessive profit-shifting and tax competition by imposing a global minimum corporate tax rate. Under the OECD's Pillar Two framework, already adopted by 140+ jurisdictions, large multinationals should pay at least 15% tax on profits in each jurisdiction they operate.[1] The tax treaty would thus place a "floor" under the race to the bottom: companies would lose their ability to park income in zero-tax jurisdictions and governments would rake in billions in new tax revenues. Most estimates predict that a 15% floor would yield around $155-192 billion in annual additional revenue (6-8% of global corporate income tax revenues) when fully implemented.[2] However, the treaty hit a wall of practical resistance from U.S. Policymakers; as President Trump declared in early 2025, the Pillar Two agreement "shall be considered of no force or effect within the United States", exempting U.S.-parented multinationals from the new rules.[3] The significance of this withdrawal cannot be overstated given that U.S. Companies contribute disproportionately to global profit flows; roughly $1 trillion in profits (about 35% of profits reported offshore) was shifted to tax havens in 2022, according to one study.[4] Absent U.S. Compliance, this loophole will continue to be exploited by U.S. Firms even as other nations adhere to the minimum rate.

Conventional discourse about the ability of a harmonized 15% rate to resolve profit-shifting, therefore, paints an incomplete picture. After all, identical changes to statutory tax rates may produce very different effects at the firm level and certainly at the country level, as Patel, Bilicka and Seegert so adeptly illustrate: it is the "non-uniform impacts" of identical tax changes that lie at the heart of global tax competition.[5] Heterogeneity in tax code design, in administrative capacity and in market structures ensures that some nations profit much more (or lose more efficiency) than others. U.S. Abstention is merely the most glaring example of this fact: given that the United States own 10% minimum tax (GILTI) is already lower than the OECD floor, U.S. Multinationals will benefit from a tax floor that other nations have had to meet or raise, but which has little direct impact on their own behavior. Effectively, U.S. Income remains heavily subsidized by havens while the rest of the world faces more restricted opportunities.[6]

Because of these and other complex interactions, this paper argues that the true significance of a global minimum tax extends beyond the immediate gains or losses from its immediate revenue effects and depends critically on dynamic structural factors. Over and above such effects, the tax reform is influencing corporate financing and investment decisions in complex ways. The success of the initiative also hinges on simultaneous shifts in institutional factors and geoeconomics, including the new regime of industrial policy with targeted subsidies and changes in political risk that drive corporate behavior. These second-order effects will be most crucial by 2026; increasing importance of intangible profit streams (and therefore the capacity to shift income), coupled with growing geopolitical instability and the associated shift of activity away from perceived less secure havens, suggests these dynamics are at play more than ever.[7] It is time to move beyond the simplistic mantra that setting a 15% floor was sufficient on its own, particularly when powerful actors have opt-outs. This paper builds upon those second-order effects and argues that understanding precisely how individual countries and firms react to such reform is crucial. Ultimately, the paper shows that tax competition is less of a race to a single global bottom and more of a multifaceted struggle for market access, national allegiance and political and economic security.

The essence of our argument is that uniform tax rates will yield imperfect results without acknowledging heterogeneity. Policymakers should refrain from assuming that global coordination is equivalent to harmonizing outcomes. Rather, they must address why reactions vary, who gains and who loses within each country and how these shifting dynamics spread. The following pages unpack this argument in greater detail: Chapter 2 documents country and firm-level reactions, Chapter 3 provides microeconomic models to illustrate these mechanisms and Chapter 4 shows why other factors (such as political risk) are equally decisive. Each section is grounded in robust empirical evidence from 2023 to 2026 and highlights causal mechanisms. Finally, the conclusion synthesizes our results into policy recommendations for achieving an effective global tax framework by modifying incentives and institutions beyond simple rate alignment.

2. Differential Responses to a Common Tax Floor

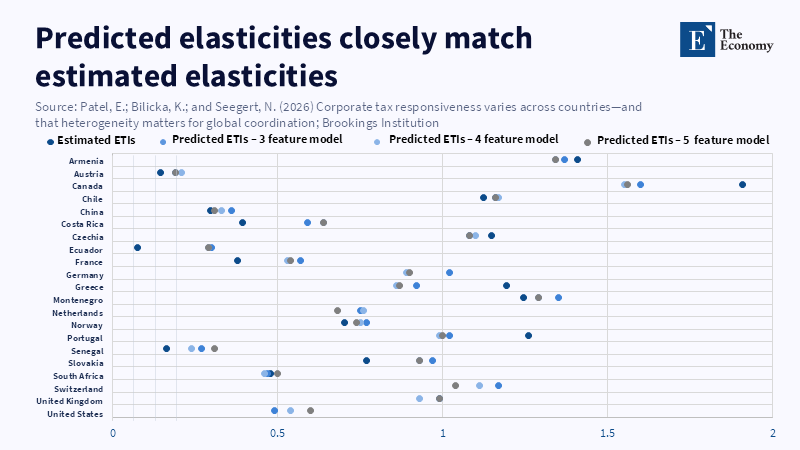

Not all countries or all firms react identically when given the same tax rate. Studies have estimated corporate tax elasticities – defined as the percentage change in tax base resulting from a 1% change in the tax rate – over a considerable range. The Brookings analysis estimated a range from almost zero to nearly two for its 16 surveyed countries.[8] It's a big range. For one country, a 1% increase in corporate tax rates might cause its tax base to shrink by almost 2%; for another, it's negligible. Why the discrepancy? To a considerable extent, it depends on the features and enforcement of each country's tax system.[9]

For instance, with lenient loss offset rules and a generous array of carve-outs, it's easy for firms to claim lower taxable income at higher tax rates. With firms allowed to carry losses backward and forward and establish a variety of special-purpose entities, multinationals have the freedom to shift profits wherever tax rates encourage them to. High tax elasticities naturally result. A nation with strict anti-avoidance measures, minimal tax loss benefits and diligent transfer pricing checks will experience much less profit shifting. The fixed cost is too high if they even try to reroute income and they pay the rate change relatively passively. Roughly half of the differences in response across countries can be accounted for by tax policy features.[10] The other half consists of economic structure: are firms dominated by export-oriented multinationals, or is it primarily a domestic market?

Firms also differ by their global positioning. Certain multinationals consider their home country an essential business hub and a consumer base and may accept higher tax payments than they would otherwise in order to maintain their primary operations there. A national champion company, which already enjoys a substantial market position within its home country, is a case in point. It derives considerable brand name goodwill and maintains a network of local supply chain partners and political ties, which can implicitly entrench its commitment to the home market. Leaving this market could entail loss of consumer goodwill and governmental scrutiny. In fact, the majority of these kinds of firms use a strategy of paying some home tax but holding market presence, rather than eliminating it entirely through relocation. More broadly, cross-country evidence suggests that lower tax avoidance is associated with closer government relations, better regulation quality, and less complex bureaucracy.[11] Presumably, a similar logic holds true for other countries as well. Governments reward firms for domestic economic contributions, essentially subsidizing some level of local tax payment as the price for social license. Other firms, say the digital platform company, which has few local tangible fixed assets, will have the incentives to move all of its profit into a low-tax affiliate and will already invest in "avoidance assets" (lawyers, shell companies, IP-flows, etc.) for exactly this purpose.

The economic consequence for the nation as a whole is evident. Countries whose firms face substantial switching costs will find that the nation as a whole does not lose a lot of its tax base when rates are raised. However, countries whose firms operate in a more footloose manner and already operate complex profit-shifting structures will see a sharp contraction in the taxable base. Another aspect of the story relates to enforcement incentives. Even in a full-blown tax haven, tax avoidance can lead to counter-enforcement actions, as authorities have an incentive to investigate fully tax-free firms. So companies often may find it beneficial to pay a small amount of local tax in the haven as an informal bribe for legal stability rather than insist on zero taxation. So they may not treat purely statutory tax rates as the only part of the equation, but also enforcement economies. Firms may find it worthwhile to incur non-zero taxation and forgo an extensive inquiry into their operations.

In short, companies approach tax questions with a multi-attribute choice model-a balancing of tax against other factors like market access and governmental relations. The heterogeneity of this approach is evident in the last Pillar Two negotiations. For instance, U.S. Firms finally won an exemption on top-up taxes[12] (or "top-ups"), which companies from a variety of other countries, like South Korea, had also tried to secure. Firms like Samsung and LG had argued they deserved similar relief, claiming a U.S. Top-up tax (at a high rate, due to large U.S. Investment tax credits) would hurt their international competitiveness. By agreeing on an exemption for firms already taxed domestically, the compromise deal preserved relative competitiveness while discouraging purely nominal entities with no substantial physical presence that had managed to stay just under domestic tax floors (like companies incorporated in Bermuda and domiciled elsewhere). The deals effectively compensated for differences in domestic profit-shifting incentives; the US tech giants will now pay additional top-up tax on profit shifted from the US, but Korean multinationals that operate physical plants in the US already get generous credits and will also not pay top-ups when profits are returned to the U.S., since their country imposes similar measures on outward-bound profit. Ultimately, the world tax regime incentivized firms that combine substantial physical investment across borders at the expense of nominal "shell" corporations that had few ties to real economic activity.

These differing dynamics across countries yield starkly different outcomes. A country like Mexico with a highly mobile set of U.S.-linked firms would likely see only a minor revenue gain in raising corporate rates, since the companies will readily shift their profits abroad. Ireland, by contrast, whose companies include large U.S. Multinational firms receiving substantial investment credits, would be likely to see a large change in their tax base when rates rise because they would want to return these profits to the U.S. (in effect, be topped up back to the required rate by a domestic tax on foreign income). A country with many domestically owned companies that don't have complex foreign offshore structures, like China or India, would likely see nearly all revenue raised at the same rate change, but would capture this primarily on domestically earned income. The reality of revenue data backs up this assertion. We've seen previous examples where equivalent statutory changes led to boom and bust cycles in national revenue. Identical statutory tax changes therefore, will not produce the same revenue and efficiency results; any comprehensive plan to implement global tax agreements and capture revenue must acknowledge this difference.[13]

3. Modelling the Effects of Global Minimum Taxation

Both theory and recent data help interpret these nuanced reactions. A useful way to think about it is as an investment of real resources: according to Bilicka et al. (2025), the first aspect is a lump sum cost of entering into profit-shifting-- say 1.5% of the MNEs' true tax base, plus a marginal cost. The lump-sum cost varies between MNEs; they argue it might be very low for finance or technology MNEs, which have already invested a lot in transfer-pricing expertise, while for manufacturing MNEs the cost might be considerably higher. So, at very low costs full shift will be optimal and at higher costs, less or none at all, will be optimal. Standard regressions capture only the "intensive margin" ( firms reporting positive income), thus failing to account for "extensive margin" moves of fully leaving the market. Bilicka et al. Reconcile the two approaches by comparing the estimates of one elasticity ( micro one) computed for firms reporting positive income (ca 1.3) to the macro estimates of the aggregate tax base (around 2.4). The difference means that partial analyses may fail to capture the real level of response to changes in tax rates.[14]

Indeed, these investments in profit shifting have consequences on real activity: by effectively lowering their future tax payments, they subsidize investment for an MNE. The CEPR model concludes that if the statutory rate increases from 15% to 16%, capital investment will be reduced by only 0.8% for high-shifting MNEs, as they had been paying low rates anyway and so investing more, relative to lower-shifting MNEs. Their fall in capital investment will thus be smaller than the 1.8% estimated for the low-shifting MNEs. As these investments in profit shifting are curtailed, the MNEs will face a higher cost of capital and hence invest less, reducing the growth of new investments. This is the crucial tradeoff of the global minimum tax: revenue is generated by the abolition of a profit-shifting related tax-reduction subsidy, but at the cost of potentially lower investment growth.[15]

Similarly, modeling confirms that Pillar Two results in trade-offs. If high-tax countries were to lower their statutory rates under Pillar Two without a floor, MNEs would be incentivized to shift their profits back home, investing more in their domestic market; however, the government would receive less tax revenue per unit of income. If, in contrast, haven rates were raised by a global rule, MNEs would reduce profit shifting, thus overall raising the cost of capital for MNEs; investment growth would slow down. Simulations from the CEPR model reflect this tradeoff: introducing a 15% rate floor will significantly reduce profit shifting and thus "wasteful investments" and lead to a gain in global welfare at moderate levels of GMT; however, if the floor is raised too much, the gain in welfare might fall to zero and then negative, as the minimum becomes too distortive. It appears to be a sweet spot around low-teens of percent-terms for the minimum tax rate; higher than that and welfare declines because the tax cost gets too high for all MNEs; lower than that and firms can still invest significantly in profit-shifting schemes.[16]

OECD calculations reinforce this picture; the estimates are positive: "on a reasonable range of assumptions, it could increase the world’s corporate tax receipts by an amount that is 6.5-8.1% of current receipts." The revenue effect depends on institutional designs (countries vs. Top-up) and the actual impact is likely less than the theoretical optimum. With the implementation of the IIR in 2024 (and safe harbors, domestic top-ups, etc) and the Side-by-Side Agreement in Jan 2026, the practical impact of the GMT should be somewhat softened compared to the initial design assumed by the OECD/IMF calculation; for example, if a country already taxes profits at a minimum of 15% domestically (like the US), top-up tax won't be applied by foreign governments. For that reason, real revenue gains may be lower than initially predicted.[17]

Asymmetry between countries of varying size and existing tax rates also appears to be another key takeaway of models. One paper shows that the GMT narrows real tax differentials and seems beneficial for large capital- importing countries, while the revenue effect for small capital-exporting countries is unclear. In the short-term and assuming rates are fixed domestically, a small capital-exporting country would experience a revenue gain at low costs of profit shifting and losses in case of high, due to global top-ups. The impact in the long term is affected by countries adjusting their own tax rates. Countries may enter a game where the minimum rate is a new constraint. According to that paper, moderate rates might improve both a big and a small country's welfare (and revenue), while higher rates may harm the smaller country.[18]

Evidence suggests that the extent of profit shifting has been systematically underestimated. The CEPR argues that estimates, such as nearly $1 trillion in profits shifted to tax havens in 2019, may not accurately reflect the situation. This could imply that actual revenue forecasts based on existing analyses are pessimistic and MNEs' behavior is more flexible than assumed.[19]

In general, the evidence confirms that it's not just the minimum rate that determines the effect of Pillar Two, but all surrounding institutional factors that reshape the arena for tax competition. Smaller countries, countries with higher existing tax rates or stronger tax enforcement will fare differently from others. The responses of MNEs (shift profit home vs. Change investment patterns, vs. Seek loopholes) are key to assessing the outcomes and require specific policy responses. Many countries rely on QDMTTs as opposed to the foreign top-up taxes assumed in the standard OECD models (at least to retain revenue locally), though this may still result in tax planning opportunities (like previous evidence shows with U.S. Carving outs). Evaluating Pillar Two’s effects requires more than identifying a minimum rate; its real impact lies in how that minimum price will affect the cost of capital, investment decisions and tax revenue for governments.[20]

4. Beyond the Tax Haven: Institutional and Geopolitical Determinants of Capital Allocation

Lastly and arguably most significantly, the desirability of a low tax jurisdiction goes far beyond its headline rate. The past weeks have shown this starkly. A conflict in the Middle East - one that saw its targets in Dubai include hotels and financial centers - caused an exodus of money and businesses from the Gulfhavens. Capital that used to chase Dubai’s zero tax rate is now flowing toward stability and tax breaks. Switzerland’s canton of Zug, for example, is a recipient of much of this money. It levies slightly higher taxes (approx. 11-12% effective rate) than Dubai, but investors prefer its 500-year-old neutrality and the security provided by its legal framework. High-net-worth individuals from the West had been using Dubai to shelter money; now, reports say, they are shifting funds to Switzerland "to reduce geopolitical risks."[21] The Swiss canton saw the number of companies it hosts increase from a few thousand in the 1970s to over 40,000 now, based not just on tax rates alone but on investors' trust in the state.[22]

Asian capital, meanwhile, is being diverted toward Hong Kong. However, amid increasing turmoil across the Gulf, affluent Asian individuals have been shifting liquidity toward Hong Kong in what can best be described as the acquisition of a safe haven.[23] And this is occurring not because of fiscal policy advantages but on the grounds of transparency, liquidity and reconnecting to China. In normal times, companies invest in places such as Hong Kong or Singapore not just because the tax burden is low but also because of its rule-of-law, its infrastructure and its ease of doing business. No country is completely risk-free. The instability evident in Dubai in the recent days, hotel bombings and airport strikes are brutal reminders to companies that the lower the taxes are, the higher the geopolitical risk may be.

This demonstrates that capital's elasticity for tax differences is finite. Businesses and individuals make overall cost-benefit assessments. Money goes to a slightly higher tax rate in Switzerland because it is safe and the state is reliable. Money may go to Singapore for carbon capture rather than any number of other locations with lower taxes, because the country has good courts and the workforce is highly educated. The logic of tax competition alone is incomplete. There needs to be an appreciation that poor governance, at any given level of taxation, renders the tax benefits insignificant.[24] More concretely, tax benefits may need to be combined with the offer of security and stability, or countries that continue to cut their rates all the way to zero may find their tax policies falling flat - as these past weeks have confirmed.

This wider perspective has clear implications for the tax policy debate worldwide. For one, it confirms that an effective global minimum tax is not going to be a "race to the bottom of the law" where countries that simply abide by minimum tax rules have an edge and can compete on their own rules; it needs to be combined with at least minimal amounts of rule of law and market access. For another, it reveals an opportunity that goes beyond tax competition: states can increase cooperation on information sharing, corruption and dispute settlement. By simply allowing jurisdictions that do not meet certain standards on the quality of their governance to have higher automatic effective taxes, the global war against tax avoidance is implicitly served. Nevertheless, the experience of 2023 has demonstrated one certainty: tax havens cannot simply ride on their low tax rates anymore, their allure hinges on an increasingly wide array of other factors. Governments with unstable political systems are losing capital even without modifying corporate tax rates.

In essence, the consideration of GMT or other tax treaties should never be an isolated affair. War-induced shifts demand the integration of geopolitical risk into the analysis of tax policy. Policymakers should be told that merely offering a low tax rate without the institutional credibility to ensure its efficacy is essentially offering nothing at all. For example, any developing country seeking MNE investment by offering low taxes should at least ensure that there are proper legal assurances to avoid the expropriation of assets and red tape that can effectively cancel out the tax advantages. Simultaneously, states that have embraced the GMT can secure sustained inflows if they uphold high standards of transparency, showing that the tax revenues generated come alongside the rule of law. In short, the message from the world post-2023 is that pure tax competition is not enough; there are dimensions of international mobility that are only just starting to be explored – in particular, safety and good governance.

5. Conclusion - From Rate Coordination to Structural Tax Governance

The foregoing analysis demonstrates that a global minimum tax cannot be the cure-all or the narrowly technical fix. Mandating a 15 percent floor would help to curb egregious profit shifting and add billions to tens of billions to most governments’ tax revenues.[25] Unless carefully implemented, however, it would create a skewed playing field. Countries whose tax bases are more sensitive would face a significant adjustment and efficiency loss; others would barely feel a change. Corporations, meanwhile, would re-optimize along multiple margins – financial vs. Real, domestic vs. Foreign. Some will repatriate profit, others will restructure; some will pay more tax, others will exploit carve-outs. Most importantly, the quality of the domestic environment - from corporate governance to political stability – would determine all decisions.

From these points, two policy recommendations follow from this analysis. Firstly, international coordination must move beyond a nominal rate-setting exercise to a strengthening of enforcement and closing of tax loopholes. Governments should implement robust supporting measures, such as Qualified Domestic Minimum Taxes and strong Controlled Foreign Corporation Rules, to ensure that the benefit of GMT reaches the intended tax bases.[26] Secondly, each country should devise its own complementary measures given its own responsiveness. Governments whose corporate tax bases are relatively sensitive could raise their tax rates gradually or through other measures that deepen tax bases with anti-avoidance rules; governments with inelastic tax bases can raise taxes more quickly. Thirdly, global coordination should not neglect the other factors influencing location decisions: rule of law, transparency and stability. Governments and international bodies should develop complementary international agreements with rule-of-law-based dispute resolution mechanisms and cooperation mechanisms regarding information exchange, alongside a global minimum tax.

In other words, joining a global minimum tax would be the first step only. To achieve the stated goals, it must complement a comprehensive effort to reconstruct corporate taxation in a globalizing world. This requires assessing the country-specific responsiveness of tax bases, balancing revenue considerations with growth incentives and reinforcing tax legislation with sound governance structures. Without such an approach, the world would still face the situation where countries pursue loopholes through a complex web of tax treaties, the exact same fragmented situation that GMT aimed to combat. By adopting a systemic framework of tax incentives, governments and international institutions will ensure that corporations align their business decisions with societal goals. In conclusion, cooperation and diversity need to be managed together; cooperation through a global minimum tax would restrict each country's unilateral pursuit of lower tax burdens, whereas an assessment of each country's specificity would allow policy to be implemented with tangible economic benefits.

To sum up, resistance to Pillar Two by the United States is driven by self-interest, but this reflects a general phenomenon that the global community will need to balance individual country self-interest through well-designed and resilient cooperation, given the difficulty of getting all actors to act for the common good. The United States’ efforts demonstrate that setting an equal statutory rate, however important, is far from sufficient. The challenge is really about redefining incentives for multinational firms so that profits accrue from profitable operations rather than accounting maneuvers to move income to preferred jurisdictions. This demands careful integration of global rules and national tax policies that encourage local value creation. To avoid undesirable side effects and truly achieve the objective of the global minimum tax, a broader effort is imperative; policymakers and negotiators need to embrace a more holistic approach to reforming the global tax regime.

References

[1] OECD (2026) Global Minimum Tax. OECD Publishing, Paris.

[2] Hugger, F., González Cabral, A.C., Bucci, M., Gesualdo, M. and O’Reilly, P. (2024) ‘The Global Minimum Tax and the taxation of MNE profit’, OECD Taxation Working Papers, No. 68. OECD Publishing, Paris.

[3] The White House (2025) ‘The Organization for Economic Co-operation and Development (OECD) Global Tax Deal (Global Tax Deal)’. Presidential Memorandum, 20 January. Washington, DC.

[4] Alstadsæter, A., Godar, S., Nicolaides, P. and Zucman, G. (2024) Global Tax Evasion Report 2024. EU Tax Observatory, Paris.

[5] Patel, E., Bilicka, K. and Seegert, N. (2026) ‘Corporate tax responsiveness varies across countries—and that heterogeneity matters for global coordination’. Brookings Institution, 2 April. Washington, DC.

[6] The White House (2025) ‘The Organization for Economic Co-operation and Development (OECD) Global Tax Deal (Global Tax Deal)’. Presidential Memorandum, 20 January. Washington, DC; Reuters (2025) ‘Trump effectively pulls US out of global corporate tax deal’, 21 January; U.S. Department of the Treasury (2026) ‘Treasury Secures Agreement to Exempt U.S.-Headquartered Companies from Biden Global Tax Plan’, 5 January. Washington, DC.

[7] Hugger, F., González Cabral, A.C., Bucci, M., Gesualdo, M. and O’Reilly, P. (2024) ‘The Global Minimum Tax and the taxation of MNE profit’, OECD Taxation Working Papers, No. 68. OECD Publishing, Paris; OECD (2024) OECD Secretary-General Tax Report to G20 Finance Ministers and Central Bank Governors (G20 Brazil, February 2024). OECD Publishing, Paris.

[8] Patel, E., Bilicka, K. and Seegert, N. (2026) ‘Corporate tax responsiveness varies across countries—and that heterogeneity matters for global coordination’. Brookings Institution, 2 April. Washington, DC.

[9] Patel, E., Bilicka, K. and Seegert, N. (2026) ‘Corporate tax responsiveness varies across countries—and that heterogeneity matters for global coordination’. Brookings Institution, 2 April. Washington, DC.

[10] Patel, E., Bilicka, K. and Seegert, N. (2026) ‘Corporate tax responsiveness varies across countries—and that heterogeneity matters for global coordination’. Brookings Institution, 2 April. Washington, DC.

[11] Anggraini, P.G., Sholihin, M., Mangena, M., Wijayana, S. and Rakhman, F. (2025) ‘The determinants and consequences of tax avoidance: A psychological contract perspective’, Research in International Business and Finance, 79, 103077.

[12] U.S. Department of the Treasury (2026) ‘Treasury Secures Agreement to Exempt U.S.-Headquartered Companies from Biden Global Tax Plan’, 5 January. Washington, DC; OECD (2026) ‘International community agrees way forward on global minimum tax package’. OECD press release, 5 January, Paris; OECD (2026) ‘Global minimum tax: Understanding the Side-by-Side package’. OECD webinar, 13 January, Paris.

[13] Patel, E., Bilicka, K. and Seegert, N. (2026) ‘Corporate tax responsiveness varies across countries—and that heterogeneity matters for global coordination’. Brookings Institution, 2 April. Washington, DC.

[14] Bilicka, K.A., Devereux, M.P. and Güçeri, İ. (2024) ‘Tax Policy, Investment and Profit Shifting’, NBER Working Paper, No. 33132. National Bureau of Economic Research, Cambridge, MA.

[15] Bilicka, K., Devereux, M.P. and Güçeri, İ. (2025) ‘Reforming international taxation: Balancing profit shifting and investment responses’, VoxEU/CEPR, 30 November. London.

[16] Bilicka, K., Devereux, M.P. and Güçeri, İ. (2025) ‘Reforming international taxation: Balancing profit shifting and investment responses’, VoxEU/CEPR, 30 November. London.

[17] Hugger, F., González Cabral, A.C., Bucci, M., Gesualdo, M. and O’Reilly, P. (2024) ‘The Global Minimum Tax and the taxation of MNE profit’, OECD Taxation Working Papers, No. 68. OECD Publishing, Paris; OECD (2024) OECD Secretary-General Tax Report to G20 Finance Ministers and Central Bank Governors (G20 Brazil, February 2024). OECD Publishing, Paris; OECD (2026) ‘International community agrees way forward on global minimum tax package’. OECD press release, 5 January, Paris.

[18] Chen, X. and Sun, R. (2025) ‘The Global Minimum Tax, Investment Incentives and Asymmetric Tax Competition’, MPRA Paper, No. 126538, revised version available as MPRA Paper No. 127330. University Library of Munich, Munich.

[19] Wier, L. and Zucman, G. (2022) Global profit shifting, 1975–2019. WIDER Working Paper, No. 2022/121. UNU-WIDER, Helsinki; Bilicka, K.A., Devereux, M.P. and Güçeri, İ. (2024) ‘Tax Policy, Investment and Profit Shifting’, NBER Working Paper, No. 33132. National Bureau of Economic Research, Cambridge, MA.

[20] OECD (2026) Global Minimum Tax. OECD Publishing, Paris; OECD (2024) OECD Secretary-General Tax Report to G20 Finance Ministers and Central Bank Governors (G20 Brazil, February 2024). OECD Publishing, Paris; Langenmayr, D. and Liu, L. (2022) ‘Home or Away? Profit Shifting with Territorial Taxation’, IMF Working Papers, 2022(177). International Monetary Fund, Washington, DC.

[21] Reuters (2026) ‘Swiss money managers expect Iran war to increase inflows from Gulf’, 13 March; Reuters (2026) ‘How Dubai’s safe-haven status is being put to the test’, 2 March.

[22] Allen, M. (2007) ‘Tax paradise leads Swiss company boom’, SWI swissinfo.ch, 18 July; Zug4You (2026) ‘More new companies than ever before’, 12 January. Zug.

[23] Gan, N. and Liu, A. (2026) ‘Hong Kong Leader Says Middle East Conflict to Spur Capital Flows’, Bloomberg, 17 March; Securities and Futures Commission (2025) ‘Hong Kong’s AUM grew 13% with 81% increase in fund inflows: SFC’s 2024 survey on asset and wealth management business’, 16 July. Hong Kong; Hong Kong Monetary Authority (2025) Hong Kong’s Wealth Management Market: Opportunities Ahead. Hong Kong.

[24] Anggraini, P.G., Sholihin, M., Mangena, M., Wijayana, S. and Rakhman, F. (2025) ‘The determinants and consequences of tax avoidance: A psychological contract perspective’, Research in International Business and Finance, 79, 103077.

[25] Hugger, F., González Cabral, A.C., Bucci, M., Gesualdo, M. and O’Reilly, P. (2024) ‘The Global Minimum Tax and the taxation of MNE profit’, OECD Taxation Working Papers, No. 68. OECD Publishing, Paris.

[26] OECD (2026) Global Minimum Tax. OECD Publishing, Paris; OECD (2024) OECD Secretary-General Tax Report to G20 Finance Ministers and Central Bank Governors (G20 Brazil, February 2024). OECD Publishing, Paris.