Digital Bank Runs and the New Prestige Hierarchy of Private Banking

Authored on

Modified

Digital bank runs make confidence a liquidity issue In private banking, reputation now moves money Rankings help buyers judge trust and resilience

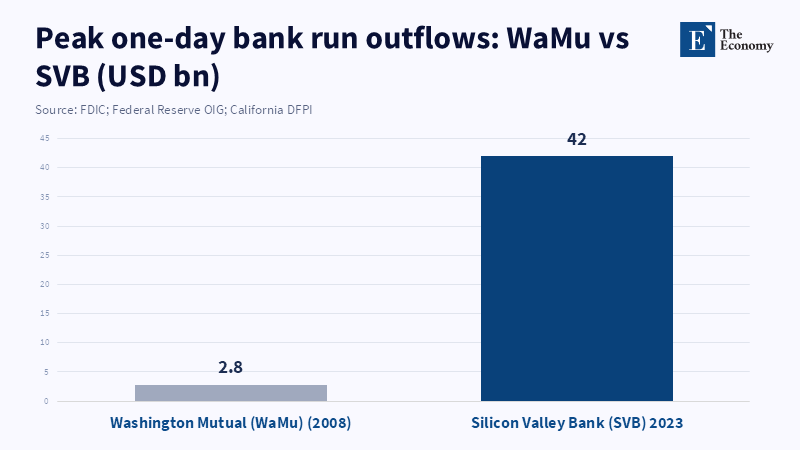

Silicon Valley Bank just got a reality check. $42 billion of deposits were withdrawn at the bank in a single day. Another $100 billion was up for grabs that morning. This should have been the end of the old story that bank confidence is a slow variable. In a digital market, confidence now rests in the moment. Mobile banking, group chats, X, WhatsApp, entrepreneurs' networks, and private circles can turn worry into action before CEOs can finish a press call. But history proves that fragile banks implode at a core level, the balance sheet rather than on rumor alone, eliminating institutions that were already healthy to begin with. But for private banking's billionaire depositors and the corporate OEMs and private banks that serve them, the age of digital bank runs is changing what it takes to be competitive. In private banking, liquidity is no longer a treasurer's problem. It is one of image, speed, reputation, and a bank's ability to read and respond to public signals faster than clients cannot "wait and see." That's why the digital bank run should be the most exciting thing about the market shift. Success will not be simply in high spreads or continuous product lines. It will be in who can stay credible even as money moves out faster than reassurance can be made.

Digital Bank Runs Have Changed the Product Offering for Wealth Clients

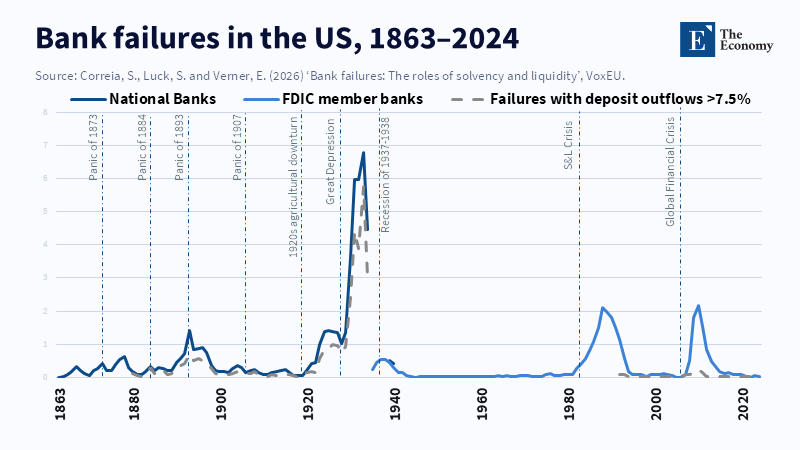

The key fact from the last banking panic is often reported through the wrong lens. Certainly, poor fundamental threats remain chief. Silicon Valley Bank was committed to uninsured deposits and had significant vulnerability to interest rate exposure. First Republic was a top-tier brand with a high net worth deposit base, and also a model that was not resilient, as those clients pulled out nearly all at once. History remains that even a few banks with unsound balance sheets tend to die, with deposit runs merely accelerating the end. Still, the market structure has, in fact, changed: because digital bank runs take place at a greater speed, they lower the time between doubt and withdrawal from days to seconds. We believe this settles depositors' expectations about what they are buying when they purchase a bank. They are not only buying a yield, a service, a name; they are also buying the ability to respond, that is, cash flow resilience, customer base strength, and narrative strength, in order to get a message out that "no, I am not liquid" before a deposit drain turns into an institution run.

This is very relevant to high-net-worth banking because the economics are also different in that space. Wealthy investors have higher concentrations of uninsured deposits, more easily mobilized relationships, and can compare and contrast independent entities by a broader set of indicators, both tangible and intangible. Even the First Republic post mortem is instructive. When the bank spent more time in the new service arms of large clients, private banking, wealth management, trust, brokerage, and used that franchise to leverage an outsized amount of uninsured deposits, that could have been the model in quiet markets. But in fragile markets. The same high-earning book that raises income and adds franchise value will also increase the speed of withdrawals in large client accounts with dense nets, when those customers expect withdrawal questions in the future but not the past. In that environment, the deposit franchise becomes more than a source of funding;it becomes a tool for customer experience. For family offices and relationship managers, that means banking relationships no longer have to be chosen: service levels and level of prestige are no longer relevant, their volumes are stable, because that is a proxy for operational stability and systematic risk.

When Deposits Move at Network Speed, Prestige Becomes Liquidity

The private banking reality is already being quietly reset. The regional bank pressures of 2023 found depositors instead flowing into the largest banks, even with the most generous compensation. This has nothing to do with price. It is signaling. In a volatile system of confidence, we find in wind tunnels, that big banks have a funding advantage based on the large predicted destination, the perceived backing from the sovereign, the often-provided analyst coverage, and the limitless television brand recognition. Big banks win in that scenario precisely because they are seen as safer, more predictable, willing to support, and capable of being supported. Smaller and midsize banks lose out because they have to substantiate themselves in a rush on the aspect of their performance that nobody else needs to, because the cash has already left. Therefore, the digital bank run continues to serve not just as a cause for M&A and regulation, but also as a psychological factor. Indeed, the flight to quality there causes what? A flight to reputation. The moment that trend is real, the market then begins to compensate capital for that franchise-specific importance before a crisis even unfolds.

The digital efficiency here gives us a better tune. For high-net-worth investors, the concern is no longer just the bank's published abatement, but the perspective of solidity. Now, it is also whether the institution can survive the examination. Traditionally, those factors included capital adequacy, asset quality, interest rate exposure, and uninsured deposit share. Modern indices draw on enhanced inputs, such as explicit scope of sense of ownership from wealth, and the scope of dependence on a handful of big depositor clients and sources for funding; how clearly management communicates; how aware the franchise makes itself to outside investors; whether early problem signals are detected; and how many steps there are between the profit statement and the extent of uninformed or unconnected information within the RM network. The Wizer 2023 survey for the Financial Stability Board has publicly cited that the speed of deposit flows, passively driven by the Internet, the social Internet's efficiency in propagating concerns such as uninformed bank runs has, in fact, increased exponentially. The prevalence of lies and speed-up driven by AI,enabled disinformation campaigns, raises the concern that today, trust is more difficult to transition into buying managers' wallets. In fact, they expect a bank and, especially, a trust management system, to be congruent and visible, and fit the seriousness of the public room to the credibility of the organization. The customer wants trust to be a platform of peace of mind, a charge to premium, a frame of comfort, and a glass of praise.

That's why rankings today actually matter more than they ever have before. In an environment immersed in specialists with wide access, network fatigue, and significant other biases, rankings define the standards of comparison. They reduce the search for connections between the bank and the obvious, and enable viewers to check the bottom line, bottom-up, with the many measures of systemic importance. They define stakes for deep diving and let market actors focus their hard, scientific attention where it is most useful. The most useful rankings will not measure size but instead will screen by source of funding, the source's openness, readiness from the creditor side, concentration levels, communication discipline, the maturity and use of digital services, the effectiveness of the range of wealth services, and the anticipated credibility of a proposition based on normal or crisis expectations. This is not irrelevant. It is simply efficient. The point of ranked comparison is not to eliminate a debate; it is to lead it to where the real conversation needs to be in order to find the next winner.

Others will contend that rankings oversimplify core measures of excellence and confer status by sheer force. That is how the old game is won, but it will not win going forward. Without comparison and contrast measures, markets are doomed to hide behind buzzwords or star CEO halos, which only help the loud but ineffective players. Rankings will not hide one-dimensional qualities; instead, they will suggest granularity in due diligence. They will tell investors, other big investors, and family clients where they may want to check their search logistics. They will indicate what institutions can deepen the target of their research into, and what institutions are simply coasting on a fact of history already established. Rankings will motivate banks to do the right job. Once in sight, banks will be able to focus on the aspects of the franchise that will persuade high-dollar clients and family offices during stressful times, including transparency, response times, safety measures, headcount, and trusted customer relationships. For the industry, Deloitte's new Digital Banking Benchmark makes it clear how universal rankings can go: the whole global banking industry appears ranked, able; now, the industry shows it is willing to measure that ranking. But the real step in the maturing of the new system is that managing public confidence expectations can become as systematic as managing balance sheets. The institutions that develop the skills of social listening, false rumor response, customer service,customer messaging, and real-time sentiment monitoring will not only execute successfully, but they will also dominate.

The winners will combine monitoring narratives as effectively as balance sheets. The true competitive insight is that the banks integrating their information and data functions with their financial functions will have an advantage. Examining what the world is saying about public data feeds is never a marketing campaign; it is a record of expenses saved in a liquidity shock. The ability to detect what information materializes, what people think of it, and how long we have to get an answer to customers is now just as important as the ability to accurately keep the books, so the profitability persists. The old world where weak banks are the ones with the most splendid parties is over. The winners will be those who can both demonstrate number resilience and be able to read and interpret the signals. In fact, the first banks that commit to social listening, false rumor response, customer-by-customer message standards, and real-time sentiment dashboards won't just win by being smart. They will win because they're safe.

References

Board of Governors of the Federal Reserve System, Office of Inspector General (2023) Material Loss Review of Silicon Valley Bank. Washington, DC: Board of Governors of the Federal Reserve System.

Correia, S., Luck, S. and Verner, E. (2026) ‘Bank failures: The roles of solvency and liquidity’, VoxEU, 16 April.

Department of Financial Protection and Innovation (2023) Review of DFPI’s Oversight and Regulation of Silicon Valley Bank. Sacramento, CA: California Department of Financial Protection and Innovation.

Federal Deposit Insurance Corporation, Office of Inspector General (2023) Material Loss Review of First Republic Bank. Washington, DC: Federal Deposit Insurance Corporation.

Financial Stability Board (2024) Depositor Behaviour and Interest Rate and Liquidity Risks in the Financial System: Lessons from the March 2023 Banking Turmoil. Basel: Financial Stability Board.

Gerdeman, D. (2023) ‘What does the failure of Silicon Valley Bank say about the state of finance?’, Working Knowledge, 14 March.

Ranking News Editor (2026) ‘Rankings as signals: How benchmarking shapes reputation and market perception’, The Ranking News, 16 March.

Similar Post