Why the Healthcare Staffing Crisis Is Reordering the Market for Trust

Authored on

Modified

Capacity now depends on execution, not just beds or equipment The healthcare staffing crisis is reshaping procurement, trust, and competition Rankings help identify which partners can actually deliver under pressure

This is not a tale of vacant beds and missing persons; it is a story of the meaning of capacity today. Previously, capacity was a matter of physical resources. It was beds, it was ventilators, it was square feet, it was machinery. During the pandemic, that logic was useful when systems needed to think up surge beds and stockpile emergency supplies. Yet, most of the more difficult lessons came much later. Staffing is not truly capacity if it cannot be safely staffed. No scan can exist if delays in transportation, documentation, and discharge slow its flow. The WHO has projected a global lack of 11 million health workers by 2030. It has also been reported that the world's 2025 nursing workforce will include 5.8 million fewer nurses than needed, as 2023 has already shown 2023. Meanwhile, aging demand continues to rise, with 1 in 6 people worldwide expected to be 60+ years by 2030 and 2.1 billion by 2050. The crisis in staffing is therefore not merely a restriction in the markets of labor, but is enlarging the scope of care itself.

That distinction might be significant because the market still too often talks as if demand just pours into the system, but it doesn't. There is a fragile chain from demand, the patient,and supply, care delivered: labor, flow sheets, handoffs, software, billing, management attention, reimbursements. By 2026, that chain will have become the real bottleneck. Hospitals have learned how to manage surge capacity in the wake of COVID. What's becoming clearer now is that that's actually a scarce resource when the stakes are highest. We're no longer talking about capacity, computers that support a certain level of activity. We have to be able to convert demand into safe, staffed, billable, effective care without the whole thing collapsing around the caregivers.

How the Healthcare Staffing Crisis Changed the Meaning of Capacity

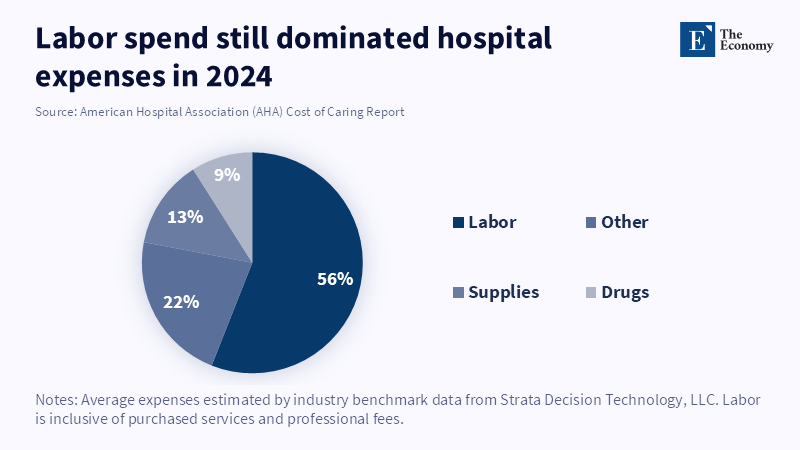

Healthcare labor shortages have long been characterized as primarily a labor force policy problem. That is no longer tenable. The healthcare staffing crisis is a market structure problem because it penetrates the entire healthcare service stack in the battle for organizational market share: how organizations compete, how buyers gauge vendors, and where value surfaces in healthcare. Labor as an organizational constraint in healthcare means jobs, skills, and speed in every corporate decision, throughput, retention, workflow, and stability to be operationally competent. Boards treasure operational conversion more than naked growth, purchasing teams vendors who help them fight at the margins more than jargon, and investors look for signals that you can run hospitals through hell. This is why, now, capacity has become a false sense of comfort. Hospitals may have the resources they used to have, the buildings, the equipment, the licensed space, but the ability to utilize those resources depends on the availability of staffing, efficiency of workflow, and sustainability of operations. The American Hospital Association reported in the

Labor was also 56% of hospitals' expenditures in 2024, or roughly 890 billion dollars, and the avowed new positions for enrolled nurses increased by an inflation,adjusted 26.6% in the 4 years prior. 129 gone by, and the campaign wages for enrolled nurses gained by inflation, adjusted 26.6% more than high-end footwear in the 4 years prior. There is no problem overlooked. It is the fundamental cost profile of the house. When labor becomes the highest cost and the scarcest input, health becomes a "service" business.

Therefore, as well as clinical impact, burnout, turnover, and organizational burden are relevant to the business of medicine. Hospitals have some capacity for handling vacant positions. They have less capacity when experienced clinicians remain on staff, while lazy time for interruptions in each transaction: fighting payors for authorization, redocumenting through incomplete software, or trying to make sense of backward workflow, all of which render them less productive. These efficiencies are not reflected by decreasing staff, patient ratios, but influence capacity on each day. Therefore, the crisis of the healthcare workforce isn't just the market supply, but how much organizational capacity can be derived from a shrunken workforce.

Execution Under Constraint Is the New Competitive Test

Accepted that reality, however, and the competition framework rapidly becomes a different one. Winners are no longer those who are adding head count, making the most expansive efficiency claims, or even helmed by the coolest CEO or, most of all,star management team. Rather, winners are those who enable provider organizations to retain staff, to cut coordination costs, and to convert a bigger share of their tightly constrained operating base than anyone else. This not only includes staffing technology companies, but scheduling and documentation solutions, patient access solutions, revenue cycle management vendors, Workforce management solutions, and, if enabled, process adoptors, as well. The healthcare staffing measure has broadened the scope of competition because the market values whoever makes the patient touchpoint journey cheaper and easier.

This helps explain why provider operations have drawn so much innovation capital. A 2025 Silicon Valley Bank healthtech report states: providers' operations on their own represented 44% of healthtech investment dollars by 2025, while AI-driven therapeutics for documentation, scheduling, billing, etc. had not yet crossed the 25% threshold. At the same time, a 2025 McKinsey survey showed 85% of health system leaders were experimenting with or deploying generative AI capabilities, 64% of them measuring ROI, which was already positive in some cases or about to be. This doesn 't mean every claim around AI is worth the fiber it is printed on. It means the industry has gotten pragmatic fast: investment is flowing into technology that promises to free up clinician time, reduce operational waste, and improve execution in the context of labor shortages. This isn't a technology fad; it is a healthcare workforce crisis.

2025 year, end review by Rock Health points in that direction. U.S. digital health investment in 2025 grew, but disparities surged, and fewer firms claimed more of that revenue. Funding rounds more than tripled in size, mega deals took a larger share of what was available, and 54% of all funding was dedicated to AI, enabling organizations. In the face of witnessing demand from buyers and investors for proof, funds for digital health are not allocated evenly across all potential solutions; rather, they are eyeing the companies most likely to scale towards health infrastructure. In the world of health infrastructure, this increasingly translates to the ability to keep labor, scarce systems operational.

Procurement Is Moving From Price Shopping to Proof Shopping

This trend is happening in plain sight. Before a less pressured market, hospital buyers would have been comparing vendors on price, feature set, or average clinician comfort with a brand. Now, in the pressured market we have, those are simply not enough. Buyers will want to see results: evidence of fill rates, ramp-up time, clinician adoption rates, fit to existing flow, implementation cost, effect on clinician retention rates, lead time, system assimilation, and whether promised savings prove out in a field test of those front-line users, the clinicians and admins who will be living with this every day. The healthcare staffing squeeze has forced greater skepticism in buying, because the cost of making a bad choice is hugely magnified. Just as having a bad staffing partner is more than just performance issues, it's burning out or destabilizing whole service lines, an inadequate workflow tool can have the same effect.

And this is all the more certain when you consider the fact that the supply side is torn. The update to the healthcare staffing market issued by Capstone Partners in February 2026 describes a market in which shortages persist in ways to keep demand high, M&A activity increased in 2025, and the market remained highly fractured with many smaller private companies as well as a dwindling pool of public businesses. This is just the type of setting where uncovering is difficult, and alternative choices tend to side towards the easiest profiler. In this kind of field, large brands possess the advantage that services are in front of a multitude of small providers, both locally and functionally in a care site, but the small providers are increasingly difficult to compare and verify. The healthcare staffing pain point offers increased incentives to use a sure choice device since the price of error in using trial and error for buying increases.

This is where rankings as signals stop looking like editorial gloss and start looking like market infrastructure. In a highly competitive, more opaque, more sensitive, pecking order environment, rankings stake out the "most likely to do well in a crisis" territory. They make search costs lower. They make reality on the ground instantlysqueezed into easy,to,kill categories. They deliver distinct, broad, brush, awareness at one end of the spectrum, one that can be used with actual, credible execution at the other end. For the hospitals and health systems that will be choosing or creating the market for their next workforce solution, the new rankings can be more selective with regard to the providers that qualify on the first tier of a sourcing effort. In a healthcare staffing environment that is struggling with a crisis, rankings are not intended to turn the world into a simpler place; they are designed to make the initial selection process easier.

Trust Under Constraint Is Becoming the Real Source of Advantage

The strongest case is clear. Rankings distort quality. They confer fame, not value. They promote bandwagoning. All is true. That is not an argument against rankings. It is an argument for better benchmarking. But the alternative in markets like this one is not competing sub-markets, it is a maze of indecipherable noise, inertia of shelf space, dull chunks of folk wisdom and closed-door decision rooms. All of which invests sales penetration with virtually the most heavily scaled powers in the game. And, I am well aware of how we have determined candidate market leaders. Better rankings do a more valuable thing. They can aggregate diffuse signals into comparative insights. They can provide buyers with a visual neighborhood map of who has been buying first in the game, hiring driven, single source predominantly content, center, leads across time from who is providing permanent, solid retention, implementation quality, concentration, resilience. They do not eliminate diligence; they render it transparent.

It's critical because credibility is no longer a branding overlay on the Operating Room, pharmacy, and outpatient lines of regional health systems, and that’s starting to look downright irrelevant. It’s become input. If you’re short on staff, short on cash, short on flow, a recognized partner who can deliver and doesn’t fall behind is going to be a huge advantage. So the playing field begins to lean toward those with demonstrated operational results, not the latest, most savvy platitudes. Likewise, we're beginning to favor those who can effectively communicate value: transparency and clear, tangible results in clinician workload easing, staffing and throughput boosting, and demand generation to discharge ratio improvement, which can all lead to increased spending and stronger alliances along with corporate governance. Ultimately, the next time a provider graces the cover of a leading industry publication, it may not be just because they have, through that company, created the most efficient institution. The health care staffing crunch is beginning to change the needs of providers, and the market rewards them.

The broader implication is that a day is coming when all kinds of tangible assets, the physical infrastructure of medicine, will continue to be available, but can no longer be the defining factor for capacity. The defining factor will be whether a given organization can actually deliver in the context of the constraints. Beds, providers, and physical infrastructure will still be critically important but can no longer be taken as a given. By 2026, the true capacity wedge will be the difference between those organizations that, when the workforce is constrained, are able to reliably deploy their tangible assets to deliver safe, high-quality care and those that are not. This explains the maelstrom for piratical procurement and capital schemes, operational machines, staff unions, and contemporary rankings. When capacity means delivery, your size will matter far less than your capacity to reliably deliver under stress.

References

American Hospital Association (2026) 2025 The Cost of Caring Report. Chicago, IL: American Hospital Association.

Capstone Partners (2026) Healthcare Staffing Market Update – February 2026. Boston, MA: Capstone Partners.

Goldstein, J.F., He, D., Kandilian, N., Lennox-Miller, A., Komatireddy, A. and Bousleiman, R. (2025) The Future of Healthtech 2025 Report: Key VC Investment Drivers. Santa Clara, CA: Silicon Valley Bank.

Martin, C.P., Lamb, J., Dahab, A., Jones, J. and Bhasker, S. (2025) ‘Generative AI in healthcare: Current trends and future outlook’, McKinsey & Company, 26 March.

World Health Organization (2024) Global Strategy on Human Resources for Health: Workforce 2030: Report by the Director-General. Geneva: World Health Organization.

World Health Organization (2025a) Ageing: Global Population. Geneva: World Health Organization.

World Health Organization (2025b) State of the World’s Nursing Report 2025. Geneva: World Health Organization.

Similar Post