Samsung’s Premium Appliance Bet Has Japan’s Old Problem

Authored on

Modified

Samsung’s premium appliance strategy faces the same trap that weakened Japan’s electronics giants AI features may lift the product, but they cannot create luxury heritage overnight The real premium test is trust, service, repair depth, and long-term brand authority

Samsung can report KRW 333.6 trillion in annual revenue and KRW 43.6 trillion in operating profit, yet still carries a clear warning sign in its consumer hardware base, as its TV and home appliance businesses lost nearly KRW 200 billion last year. This is the whole story. A premium appliance brand is not a graceful escape from price war; it is an entirely different game, governed by different memories, sales channels and rules of trust. Samsung’s attempt to climb upward onto the game’s other side comes as Chinese rivals cause prices to fall. It is a sound course of action. But even rational decisions don't win when they come too late. The Japanese already showed the pattern. They had the engineering, the consumer understanding and the monozukuri language. Yet Japanese logos did not become coveted by the connoisseurs of high-end appliances. Today, Samsung must face that same wall without the myth of the Japanese craft system behind it.

Premium appliance branding will not nullify the low-cost shock

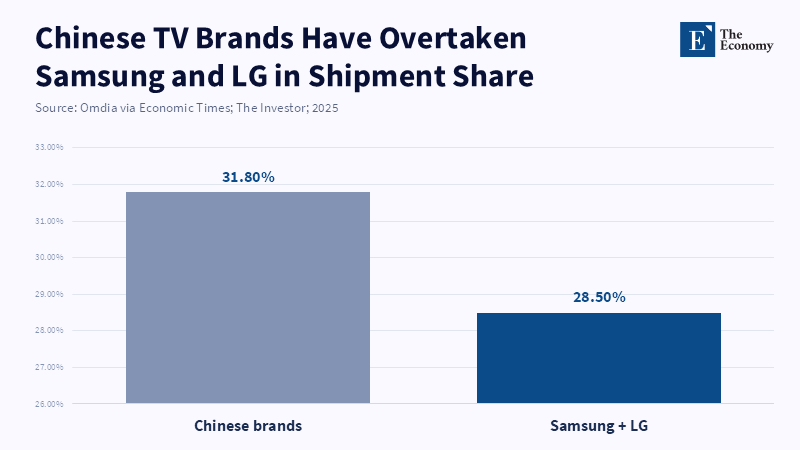

The first thing to correct is the notion that China’s appliance rise is merely a price war. TCL, Hisense, Midea, Haier and Xiaomi continually sell cheaper products. The real problem is that those brands now give people the same feeling, feature pace and improvements at a crisp, sleek modern pace. In TV, Chinese brands accounted for 31.8% of global TV shipments in Q3 2025, surpassing the 28.5% booked by the two core Korean players. Growth in the sub-$500 model also shows how strong the low-end pressure has become. That is critical because a mass market produces scale, data, retail and strength. Retailers are looking to raise prices at the top. Component suppliers watch who arrives at their factories. When those eyes and appetites turn away, then premium branding starts to look like a defensive retreat rather than a growth strategy. Even if a firm could increase prices on the tip, it would lose its mojo if the base and core consumers departed in droves. This isn't just a retreat from a given country, then. It is a warning about how the whole hierarchy may look.

Samsung's course is clear. It wants live-upgrading platforms such as Bespoke AI, SmartThings , home-connected kitchen, fridge cameras, voice controls and learning wash cycles, to move its appliances into a higher-value category. The engineering works. But the premium appliance brand doesn't (yet). Those same Chinese firms capable of driving prices down can just as readily add mass displays, apps, sensors, cameras and precise digital brainpower when asked. The ever more highly-mediated home display on a built-in fridge will be keenly viewed for a dozen product cycles. After that, it is banal. Software ages faster than cover components like steel, hinges and compressors. A premium icon would not be able to bank on a feature that a competing, poorer brand can imitate in less than two years. The focus must be on whether an affluent buyer would still be more inclined to pay more even after the distinction is narrowed. That is where Samsung looks like it is coming apart.

The Japan-model monozukuri lesson should give Samsung pause for thought

Japan is really the example to fear here, not the exception. For generations, Japanese consumer electronics came to stand for precision, durability and trust. Monozukuri provided the corporeal metaphors of discipline and precision. "This is not assembled, it is crafted" was the Japanese message of superiority. Then, new lifestyles named Japandi suggested a softer aura of calm, warm nature and muted taste. If just one Asian company was ever poised for entry to the top pocket, it would have been the Japanese. Yet the premium kitchen-appliance list continues to be packed with the likes of Sub-Zero, Wolf, Miele, Gaggenau, Variotherm, Fisher & Paykel and SMEG. Corporate Japanese and Korean large appliances still don't really have a time. They are not ubiquitous enough to be functionally invisible. That is the key point.

So what happened? Plainly, "the general" was not the same as "the luxurious." Japanese companies made great margins and held a recognizably adept user image, but lost ground when flat screens, digital supply systems and Asian owners appeared, scaling their product image down. Sharp was the first to lose its vertical display gaming lead to Samsung in 2006. Today, their analogy is the Chinese display companies displacing their Japanese and Korean forebears. The Japanese end-user story shows that, even at their dignity, once the sales power evaporates, a near-iconic name can keep respect but end up meaning nothing. Furthermore, the craft language alone cannot then reconquer distribution channels. Creating a high-end building retail domain requires presence in showrooms, architectural plans, installers' routines and the repair team. Japan had a deeper crafts history than that of Samsung, even one that was not visibly invoked. Yet Samsung never made it there. It would not be wise to assume that a software upgrade would be able to do what Japanese monozukuri could not. This is the gap between admiration and speculation. Or between an ordinary consumer's love and their use of what builders pick.

The premium appliance branding can only be built into the wall, not the screen

The premium appliance market isn't bought as if a phone were a phone. It is often bought in a package, a refurbishment, a luxury apartment block, hotel suite or a nearby second home. The purchasing sequence is thus lengthier and more conservative. Developers want safe choices. Designers want fit and finish. Affluent homeowners expect undisturbed quiet, long-lived service points, accessible products and an appliance brand that won't seem preposterous next to stone, wood and custom cabinetry and tailored work. Energy standards, repair regulations and future product passports will further accentuate the attraction of that service. So it is that European premium brands enjoy a deep script advantage that defies imitation. Those brands sell not merely an appliance, but an element of the traditional space concept. When built in, the appliance becomes part of the kitchen wall, counter and installation queue.

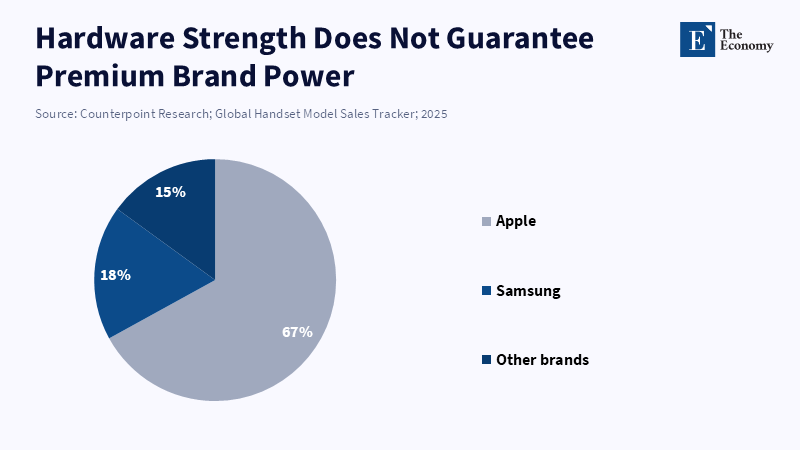

And so it is that Samsung's slightly serendipitous strength in broad-based commodified appliances may turn into its doom in high-end branding. Sure, Samsung is an expert at global product launches, extensive proximity retail, the recipe for modular machines and the attraction of visible technology. But high-net-worth buyers have only a sometimes-unexpected need for the technology to be obvious. Unlike low-net-worth buyers, they want effortless performance in the interior and hidden noise. They want quiet, calm and long-outdated durable use, with robust spare parts, the reassuring time with its brand and the assurance that it will age happily. The smartphone market offers the same warning. Superior parts, comfort and service don't guarantee a dominant share of the premium phone market. But they will soften the luxury attachment. They will no longer apply to luxury appliances in the long run. Or in the example of the automatic volume control, to premium appliances in the short one, too. Thus, what the seller of the absolutely luxurious should expect from the home ecosystem is certainty that the appliance will not be a star, but a long-lasting participant. Samsung should not expect to be able to, by definition, make their premium appliance style depend on just a better screen, when they seem happy enough to do well in mid-range screens.

What Samsung should do if premium appliance branding is to work

Samsung can by no means afford to make branding the project that attempts to teleport the headlining retailer-brand seen on the mid-market gadgets into the star-avid top-end. It has room for plenty of newly-Century collaborations, but it is getting booked to the point that the space for a history-loaded name is compromised. It is far more effective to craft in niches that do not matter to until they are fully formed and incumbent. Therefore, Samsung should focus on connected laundry and drying, smarter energy management and electric drive tools, diagnostics, that make life better for central-cities owners in compression, that supply an elegant sense of assuredness and that combine with subscriptions and service packages to offer a replacement every decade of lifetime without equating luxury with a European icon. That could yet secure premium margins. Still, it would be a Samsung-based premium, rather than a derivation of the European one.

Policy should not become a rescue plan for famous brands after low-cost competitors attack. That sort of measure wastes resources if it just extends brands rather than capabilities. More importantly, the deep engineering layer that underpins the appliance brand should be the main policy goal. Heating pumps, powerful vacuum motors, intelligent substitutes, smart-home standards, open systems and so forth. Nevertheless, retailers and house builders should simply be more careful. They should judge appliances by their costs of ownership, their repair depth, their energy levels and the cost of emerging with a compatible home, rather than simply by language on a 20% discount label. Actually, buying a premium appliance is not about getting the gadgets and new looks. It is about keeping faith in the brand after ten years of ownership. They know this instinctively, too.

Samsung's luxury appliance gamble will falter if luxury just becomes a higher sticker price on an overstuffed box. Samsung’s appliances are not weak; the premium market is not won with features alone. It is won with the power of trust, service depth, the command of design, the authority over distribution, and the silent assurance of how a device will still feel right to you a decade into a house that costs millions. Japan had a better artisanal tale than Samsung, and the country’s homegrown brands couldn't turn it into lasting dominance in high-end electronics. The stakes are higher now for Samsung, with pressure from China at the lower end and legacy luxury brands occupying premium space. Simply put, Samsung shouldn't buy into the fantasy of an inherited kind of luxury. Instead, it needs to create its own tightly focused, service-intensive niche at the premium edge. That niche will center on its expertise in energy-efficient technology, intelligent diagnostics, and the enduring, yet invisible, value of connected home ownership.

References

ChosunBiz (2026) ‘Chinese brands seize nearly 60% of Japan TV market as Sony shifts to TCL’, ChosunBiz, 20 February.

Counterpoint Research Team (2025) ‘Global premium smartphone share climbs to 25% in 2024 as premiumization continues’, Counterpoint Research, 16 February.

Gallagher, J. (2025) ‘The Throne Shakes Under China’s Cost-Effective TV Offensive: Samsung and LG’s “Premium Strategy” Put to the Test’, The Economy, 25 June.

Jin, H. (2026) ‘Samsung says to discontinue China sales of some consumer electronics products’, Reuters, 6 May.

MarkWide Research (2025) Europe White Goods Market: Size, Share, Trends, Analysis and Forecast 2026–2035. Pune: MarkWide Research.

Mordor Intelligence (2026) Europe Major Home Appliances Market: Size and Share Analysis. Hyderabad: Mordor Intelligence.

Nicholson, A.-M. (2025) ‘Chinese Budget RGB LED TV Rated “Beyond Expectations,” Samsung’s Two-Decade Reign Under Threat’, The Economy, 17 September.

Reuter, M. (2026) ‘“Pivoting Toward High Value and Premium Segments” — Samsung Electronics Reshapes Home Appliance Strategy, Can It Challenge Europe’s Established Brands?’, The Economy, 28 April.

Samsung Electronics (2026) ‘Samsung Electronics Announces Fourth Quarter and FY 2025 Results’, Samsung Global Newsroom, 29 January.

Toshiba Lifestyle Products and Services Corporation (2024) ‘Toshiba Lifestyle Announces Strategy to Strengthen its Market Presence in Asia Pacific and Reveals Innovative Product Launches in Vietnam’, Toshiba Lifestyle, 2 September.

Similar Post