Why Senior Living Rankings Will Define the Village Model of Care

Authored on

Modified

Care is moving from isolated homes to organized care villages Trust and visibility now shape senior care competition Rankings help buyers spot credible providers fast

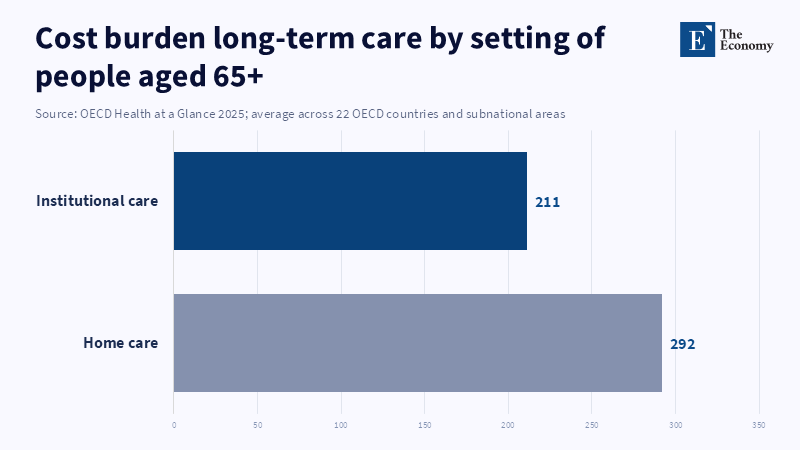

The aging story is no longer only a demographic story; it is also a market story, and senior living rankings are part of it. In the EU, in early 2025, the old age dependency ratio was 34.5 percent, meaning a little more than three people of working age for every one aged 65 or over. Across the OECD, the average level of long-term care workers per 100 seniors 65 + stabilized at five over the last decade (2013–2023), despite rising demand. The OECD report public expenditure on long-term care in Greece is approximately 0.1 percent of GDP, the lowest in Europe, at a time when the economics of dispersed care became ever less justifiable. As the OECD describes, individuals with severe care needs could face total long-term care costs of anywhere from a little over one to almost seven times the country’s median national income levels, thus raising not only affordability issues but also eligibility for institutions. Their infrastructure will be in demand and not just beds, but supported, credible, and protected systems of care, accommodation, and social life too. But senior living rankings are only part of that infrastructure.

From Housing Logic to Care Density

In theory, the most effective framework within which to envision a village model is not as the big sister/Golden state/ more refined version of the nursing home, or as a lifestyle, market potential in the chronically well decade; it is as a set of carefully crafted, high,statusservices, optimized for high population densities and modular enough that they are easier to imitate. Since an average older citizen lives in a few hundred square feet household, clinical and practical services are less likely to be scheduled or comanaged, co-opted, overseen, or woven; relatives are less likely to be available to pool resources; medical professionals and their supporting teams are more likely to be loitering; screening intervention is more likely to mean vigilance awakening and thus be unfulfilled; and, of course, there's a lot more on looking diminutive in the appropriate direction. In such a situation, the calculated unit cost of care is undefined. It would also be a huge delay, skipping awakening cues, skeletal expertise, and exhausted personnel. On the contrary, a village is a constellation of residents, employees, shared services, safety schemes, and social activities at one operating facility. This novel shape is less prescriptive, more efficient, more proactive, and less solitary.

That's all fine and dandy, but true optimism about aging and demand, aging is the current overlay of labor constraints and fiscal constraints. OECD trajectories show long-term care spending rising from an estimated 1.52% to 2.81% of GDP, in 2023 and 2050 respectively (base case); but the assumptions underlying the short-term and long-term dynamics of growth in labor rates suggest the possibility of reducing that rate of growth by as much as 13.5%, with a high productivity scenario that would incorporate assistive technology and integrated care. The OECD's new red book on aging paints an optimistic view of seniors, noting that successful interventions for healthy aging can diminish future health and long-term care utilization, but adds that we cannot yet say whether all existing retirement communities and dementia centers are "high-yield providers of care." It suggests the markets are headed for formats able to sort services at scale (by waiving the limits on competition in the private market)without compromising the ability to cocoon individuals in high,tech, high,close comfort settings. Nonetheless, supply still remains sparse in the vast majority of nations; adult day care utilization accounts for less than 1% of the population over 65 in most countries, despite the recommendation that it can be a cost-effective intervention. The opportunity is not for more bed capacity, but for integrated, effective care environments, mapped out between the isolated aging-in-place model and the high-utilization model of the nursing home.

Senior Living Rankings as Market Infrastructure

Third comparison (herein, competition of time and money) arises when care is no longer the unique and wonderful all-in-one family purchase. No single family buying into an independent house call actually buys square footage, they buy the assurance (backed by program reputation) that the place has "enough" staff, that there won't be room swap shift changes and admin logrolling, that residents will have the high, experience they are looking for, that the place will respond well in the future when services change. But the majority of family purchasers who walk in the door arrive in the category dimensioned by research as "truly pressed for time and uninformed", which is vividly illustrated by the 2025 A Place for Mom survey of 1104 family caregivers, in 2025, 67% of the families visited for a senior care decision took 60 days or fewer and 88% made the claim that, with the research they wanted and needed to do, previous experience in family or friend circles made no difference in the amount of time needed or help wanted. We call this kind of shopper a classic trust gap; the customer is time, pressed and needs help finding what they are looking for with a rare and difficult to benchmark variety of mom and pop solutions and the customer understands exponentially more about rates, staffing, resident density, resident mix, retention, turn and escalation than any facility brochure or tour ever will. Senior living rankings are hugely relevant for this exact customer base because they cut into search costs and can reach an agreement on a shared lexicon for evaluating very highly varied products.

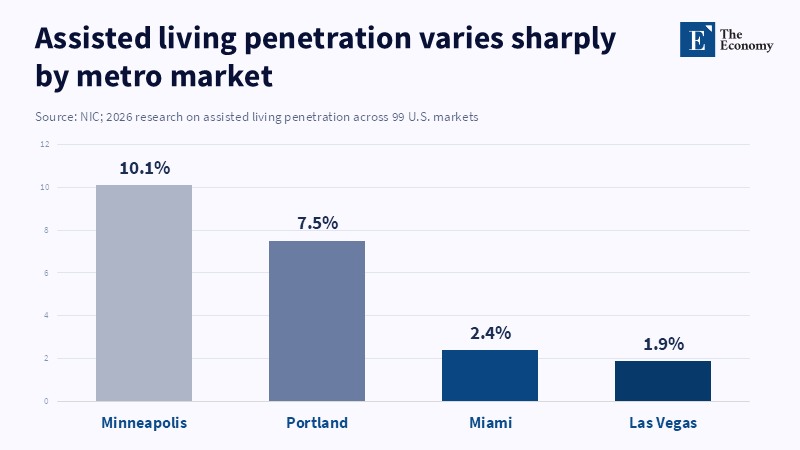

The more subtle point here is that demand is not caused by age or income. The NIC reports that there is a wide variation among the US metros, by city and in bed availability between regions and urban clusters in the density of consumers and in the success of community participation by market segment. Portland, Philadelphia, Kansas City and Seattle have some of the highest overall senior home community penetration levels, versus very low levels in Los Angeles, Riverside, New York and Las Vegas. The difference? The table stakes necessary for successful market entry include broad market readiness, consumer education, staffing plans, policy readiness and product confidence. This offers an important cue. When it comes to care markets, demand gets there, but with consumer confidence, provenance and source, it is much more mobile and accessible. The best providers don't set the market—they create it. They make the village model understandable, familiar and attainable, long before panicky purchasing turns into a true crisis.

Competition is shifting from real estate to momentum and reputation

And that is why it looks like the market is not only deeper and more accessible, but it is also plumper with capital. The NC reports that by the end of 2015, senior housing occupancy was 89.1%, up 2.2 percentage points in the year, even as construction continues to slow. The report also predicts that over the next five years, the 80 + population segment that accounts for the greatest share of senior housing operators will expand 28%. To date, capital has seen the beginning of the ideal circumstance where by the start of 2026, the NC has called the industry a $450 billion to $600 billion operation where private forprofit owners, operators, even nonprofits, maybe own as much as 86% of today's facilities, a level that will tempt some to buy up numerous players at once. That is the architecture of an industry speeding away from local firms toward national and international efficiency. But in the meantime, it speeds in as well, the death tolls in the form of damage control. More than ever before, because smart operators have been better able to prune ineffective operations and better label what is "long-lasting" and "respectable" in its face, where there are $10 million in flagrant failures and the smallest dent of public opinion erosion.

The best evidence that differences in quality exist is in their competitive outcomes. A 2024 NORC study shows that current moves into senior housing increase, on average, by a week, a week's additional life expectancy in the observed sample, relative to a matched group of seniors who remained in the community. Communities in the highest quartile added an average of 70 days of life expectancy, and the difference between the lowest quartile and the highest quartile was a week. When a gap in quality performance is one week or more in life expectancy, rankings in the popular press do not simply subsist as a collection of names listed on a webpage. The rankings become a lens through which you can peer into your own universe and see how far you are from such an established standard. Buyers want rankings because they want to distinguish one product from another. Investors want rankings because they want to know which companies have the ability to be scaled successfully. In senior living's new chapter, 'that high-ranking silver,topped facility can be the one that produces miracles, Nobel,winsideam," and those results will be evidenced by visible indicators that are reliably reported everywhere.

What Good Senior Living Rankings Need to Do Next

It is not difficult to criticize the things you dislike in rankings. They "may oversimplify", fail to reflect a highly complex culture, fail to tell a story and foster herd mentality towards operators that are no longer impressionable. Sure, there are ways to do this. Perhaps a weak rankings system in a weak industry may only turn into little more than a shiny mirror that dotes on the traffic. But the worst solution ("not comparable at all") is totally wrong. Yes, weak benchmarks and rankings systems in OPACS, lines of ads and themed magazines will make current operators stronger, but they will not help consumers, no matter how much more cheerful and toothless their marketing words might be. Poor rankings are a problem, but not having a rankings system might be worse.

Hence, a new and improved successor to today's senior living rankings should be composed along the lines of infrastructure rather than opinion. It should use tough criteria based on measures of the seven dimensions that most clearly show how the village model delivers: staffing levels, scope of amenities and services, expertise specialization, coordination of services and staff, satisfaction levels of residents, quality assurance/measures and price positioning. It should keep a lid on distinctions between assisted living, retirement housing, dementia care communities and integrated senior care environments so that the categories stay in view. It should differentiate operators that develop pioneering clinical services and early and social interventions from those who only offer comfort. It should allow consumers to know that the operator is covering the promise on the ground. This kind of ranking in both unsought and third-party formats will only serve to organize consensus.

Its importance extends beyond senior living to the grander scheme of the built environment. As 'the aging world' settles in, not only will more businesses build around mixed systems for care and the elderly, they will forge the hybrid pitch of in-home medical and social activities, centered around housing and healthcare delivery,toward prevention and monitoring that transcends industries. Even some segments of the luxury aging market may need a mixed set of services, while the middle market will need them too, not to mention the needy, fragile, frail and totally busy retirees. Ultimately, all of these proposals will have similarly limited sectors, trustworthy ranking tools, limited ability to look into the future and forecast quality and the desire to translate management reputation into a dollar amount for services and proven output. This is the role and ultimate goal of rankers in senior living: close the gap between imperfect information and confident consumer choice, so that families can, earlier in life, make a purchase; so that providers can breed differentiation based on execution; and so that investors can direct resources to the organizations that can reliably produce all necessities of care on predictable large scale.

The opening statistic should therefore be regarded as both a signal for action and a provocation to action. A future in which there are fewer workers to care for older people and even higher long-term care expenses may not be going away on its own and it may no longer be possible to look away but inward and celebrate the fact that people are trapped inside their own homes. As the aging population increases, this fact alone should become reason enough to support care formats that cluster on-demand services and safeguard independence where appropriate and that keep transparency about services. One response to that fact is senior living. It privileges the systematization of formal care, from a dispersed assignment into a bureaucratized system. But senior living rankings are the network partner that makes that system obtainable in a competitive market. Now, in the decade of excess, unpredictability and forsaken confidence, they are no longer a minor journalistic exercise but one of the key standards shaping where appropriate portfolios will be ordered and consumed.

References

A Place for Mom (2025) Senior Care Search Trends: Navigating Options in the U.S. New York, NY: A Place for Mom.

Blavet, T., Lorenzoni, L. and Rapp, T. (2026) Future Long-Term Care Expenditure Trajectories across OECD Countries. OECD Health Working Papers No. 194. Paris: OECD Publishing.

European Commission, Eurostat (2026) ‘Population structure and ageing’, Statistics Explained, 2 February. Luxembourg: European Commission.

National Investment Center for Seniors Housing & Care (2026a) ‘Occupancy Rate for Senior Living Communities Increased in 2025 as Construction Stalled’, 15 January. Annapolis, MD: NIC.

National Investment Center for Seniors Housing & Care (2026b) ‘Research: Assisted Living Market Penetration Depends on More Than Local Demographics or Economics’, 17 February. Annapolis, MD: NIC.

NORC at the University of Chicago (2024) An Analysis of Longevity Among Senior Housing Residents. Chicago, IL: NORC at the University of Chicago.

OECD (2025) Health at a Glance 2025: OECD Indicators. Paris: OECD Publishing.

Similar Post