Masstige Appliance Branding Is the Only Real Escape from the Middle

Authored on

Modified

Samsung and Japanese appliance makers are trapped between Chinese low-cost scale and European heritage luxury Masstige branding gives them a realistic middle path To work, the premium must be proven through design, service, durability, and useful smart features

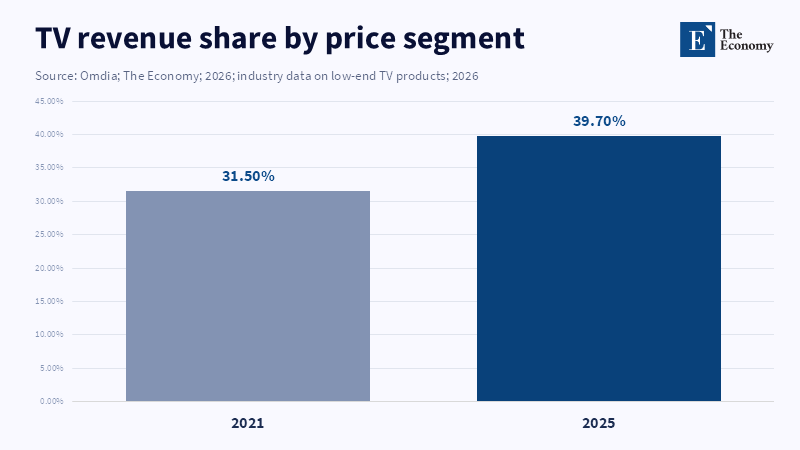

The single most significant number in the appliance wars is not Samsung's AI spend nor even the maturity of Gaggenau's brand credibility, but the 39.7% TV revenue that late 2025 came from sub-$500 products up from 31.5% in 2021. That transition is what happened to the old middle of consumer electronics. It was not patiently refined. It was hollowed out from below. Chinese companies brought better-than-good-enough, faster, cheaper and at an industrial scale. Samsung and even the inheritors of the old Japanese appliance masters simply cannot buy their way out of this corner they have put themselves in, by pretending this floor does not exist. Nor can they stroll back into Europe's luxury zone, an area built over several decades and in some cases centuries on the foundations of matter-of-fact, transparent trust. The only credible way forward is: masstige appliance branding. Good enough and certainly safe enough to produce a sensation of progress and function but cheap enough to sell en masse and self-controlled enough that they do not overshadow the prestige.

Masstige appliance branding needs reasons, not just prices

The new MDPI research into masstige buying provides an important context, since it treats masstige not simply as a Marketing "game" and "price" substitute. The message is clear: consumers buy approachable luxuries for reasons that they can defend and not simply because they are "cheaper" than high-luxury goods. The MDPI study, based on masstige jewelry consumers in Türkiye, matters because it shows that buyers need reasons they can defend, not only a lower price than true luxury. To investigate the relationships between "values, motivations and reasons" in such purchases is a lesson for appliances, which are high-involvement buys with consumers living with the buy for years. Appliances buyers are not looking for features- they are looking for something more profound: a story that makes the higher price worth paying.

That's the rationale supporting the Samsung & Japanese paradox. Masstige branding of electronics isn't smuggling luxury in, it's communicating a short-hand promise-the brand "says the customer can expect a valid explanation for the price they are paying." The customer is willing to pay above the Chinese "rough" benchmark if the brand offers a concrete benefit that the customer values. This benefit is commonly a combination of good design, energy efficiency, longer warranty, superior build quality, integrated design with the consumer's home and less obvious display of status. The MDPI paper admitted that not all benefits support the brand's stand in the same way. For one person's purchase, it may be the final sales price. For another, this same value proposition may erode the prestige of a brand for that person. A descending brand that wants to begin to serve the masses has to be overly cautious lest the low price ruins the masstige image and the high price repels the masses.

This is a factor that is so often missed in appliance strategy. Companies feel like premiumization is a journey to overnight luxury, when the reality is a fine dance. While there needs to be something tangible in the product that is a premium step-up from the mass market, it can't be too far removed and aspirational. They can't sell only on their current across-the-board channels, but they can't be seen to be flogging stock off either. It comes down to technology, which needs to be buyable and make life easier, rather than buyable and make life more complicated. It is this fine art that sees many premiumization efforts fall flat.

Masstige appliance branding. Samsung's masstige strategy is a tightrope

Samsung's appliance business now finds itself on the precipice. One foot is planted next to large-volume low-cost producers in Haier, Midea, Hisense, TCL and Xiaomi, the other next to heritage European brands Miele, Bosch, Siemens and Gaggenau, which have an advantage not merely based on the quality of their product but in the cultural gravitas secured over centuries, if not millennia, by their heritage. Gaggenau was set up in the 17th century by Margrave Ludwig Wilhelm von Baden's ironworks and Miele, since 1899, has been owned and run by the same family. These facts do not necessarily mean every single item is superior, but they do make their offering more credible when making the premium pitch. Samsung has the mass production muscle and global distribution reach, along with a reputation as a tech innovator; connected, screen-heavy appliances loaded with sensors, AI chips, cameras and SmartThings. But while all that technology is attractive, this alone does not build deep-seated trust and put an oven, dishwasher, or built-in refrigerator at the center of your home for the next 15 years.

The more plausible future for Samsung is not the domain of all-encompassing luxury. It is in the domain of a masstige appliance branding of "smart home at a mass" scale. Samsung’s Bespoke AI strategy can only be taken seriously if it solves real problems faced by individuals and not as a novelty for those who want to buy still more technology. A refrigerator that delivers significant reductions in waste; a washing machine that treats fabric more gently while also saving water and time; a servicing scheme that relieves any fear of repairs and breakdowns—all of these justify a premium price, while a screen on the washing machine does not. The danger is feature inflation: while Chinese players can replicate external appearances almost instantaneously, incumbent European brands regard features as irrelevant gimmickry. Samsung's real point of differentiation has to be how its technology, service and styling come together to produce an experience so much better than mass market that consumers can reach it without the heavy investment implied by leadership in the old world of luxury.

The recent exit from China is a sobering reminder. If competitors local to sale are prepared to price brands off the shelf, then it may be time for global mass brands to think hard about what battles are actually worth fighting. Exiting categories that aren't working by outsourcing low-margin brands or getting out of businesses altogether can be smart moves that free up resources to focus on a mid-premium, mid-value offer. But if you do that while maintaining an archaic cost base and merely rebranding an existing, generic product line with the new, premium brand name, then you're simply failing. Masstige appliance brands require operational transformation to support a consistent message through factories, service, software and even retail finance and more.

Japanese quality has to become proof, not nostalgia

Japanese appliance makers face a similar, though more serious challenge. For many years, companies like Panasonic, Sharp, Toshiba and Sony managed to conjure up an image of quality that registered in the minds of most markets around the world. But the branding magic has faded, with manufacturing, display technology and home electronics shifting to China's lower-cost base. Panasonic's strategy documents offer a rarely honest picture of its plight: it wants to cling, as far as possible, to brand loyalty and Japanese chips while cutting costs fast enough to stay ahead of China and Korea. Like many companies trying to rescue the middle ground without cheapening the product (even if it cannot afford it), this reads as the language of attempting to eke out a niche as the company pushes for forward-looking, collaborative parts sourcing, commonalization and supply chain efficiency.

The problem is that "Japanese quality" can no longer be sold as a vague national badge of honor. Masstige appliance branding must turn that aura into hard facts. A Japanese washing machine can't just advertise "reliability"—there must be a set of hard facts on longer service life, water-and energy-saving, program flexibility, availability of spare parts, noise control, et al. A Japanese air conditioner can't just be "advanced"—there needs to be a definite set of benefits for a higher price than a Chinese counterpart that evolves quickly, but a lower price than a European built-in premium system. The same goes for flat screen televisions and kitchen appliances. If Japanese brands go only for nostalgia, they would alienate the young market. If they go only for low cost, they would compromise margin. The middle ground has to be reclaimed as a focused, purposeful identity, not defended as an inheritance.

Most importantly, Japanese and Korean players also need to understand that China is no longer just a low-end competitor. Chinese brands are catching up on everything from price and inferior design to smart features, strong supply chains, rapid product rollouts and enough quality to knock the packaging and positioning edge away from ingrained premium brands. The solution is not to sneer at these brands but to define the value proposition exactly—allow customers to quantify the difference in utilization, service, resale value—otherwise, "premium" becomes a tax on loyalty.

An appliance branding policy test for many-branded masstige products

In the case study of the Harvard Business Review for Breyers, what is taking shape by which this occurs? Breyers Gelato Indulgences was priced considerably higher than everyday ice cream, but still was a few steps out of the super-premium gelato price point. This was a calculated move that capitalized on mass distribution to create an elevated feeling of a premium. For appliances, quite simply, a mass brand does not have to transform into a palace brand. It must find a pricing point and give a promise to make "trade-up safe". For appliances, this means the premium should be apparent on day seven and persist until year five and be abided by until year ten. If not, it's just packaging and not a core value.

What then for industrial policymakers, executives, and business schools? The case of Samsung and Japanese makers should be approached as an industrial policy puzzle and not just a branding one. This is the macro problem of how developed economies can maintain value in the middle if the bottom is driven by China and the top is protected through 'heritage'. The intellectual solution is not protection—tariffs buy a bit of time, they do not generate desire. Subsidies buy a bit of capacity, but they do not create trust. Industrial policy needs to service repair networks, energy efficiency, spare parts stock, software services and design expertise at home. Business schools need to teach managers to re-examine the compromise middle more frequently. It is not only low-end versus luxury-end. It is often more common to labor over selling someone to loosen their purse strings.

Masstige appliance branding has changed how firms must also consider success. Unit share as a measure works poorly if each incremental sale destroys the margin. Premium share works poorly if unit volumes are too small to sustain factories. What works is a justifiable premium at scale; what you are willing to pay for it, given that its status will be clear, not uncertain. This takes attention away from launch hype and applies it toward ownership. It also forces firms to invest in unspectacular premiums such as service visits, spare parts stock, firmware updates and sales-room education. Appliances are not finished once they ship from the factory; they are evaluated for how quietly they operate, how well they save energy, how well they work in the kitchen and how easily they can be fixed for years.

The opening data point shows that the old middle is being pulled lower. When close to two-fifths of sales of a large consumer electronics grouping are below a low price line, the market has spoken. Samsung and Japanese makers cannot succeed merely by pursuing the lowest price or by adopting the upper-crust language of old European luxury. They must codify the third route. Masstige appliance branding is the only pragmatic game plan as it recognizes their existing factories, customers and the premium they can continue to develop.

References

Beard, R. and Lubel, L. (2016) ‘Finding the Sweet Spot Between Mass Market and Premium’, Harvard Business Review, 19 October.

Gaggenau Hausgeräte GmbH (2026) Company Profile. Munich: Gaggenau Hausgeräte GmbH.

Miele & Cie. KG (2026) The Miele Company: Continuity for 125 Years. Gütersloh: Miele & Cie. KG.

Panasonic Corporation (2024) Progress in Medium- to Long-Term Strategy: Living Appliances and Solutions Company. Osaka: Panasonic Corporation.

Paul, J. (2015) ‘Masstige Marketing Redefined and Mapped: Introducing a Pyramid Model and MMS Measure’, Marketing Intelligence & Planning, 33(5), pp. 691–706.

Reuter, M. (2026) ‘“Pivoting Toward High Value and Premium Segments” — Samsung Electronics Reshapes Home Appliance Strategy, Can It Challenge Europe’s Established Brands?’, The Economy, 29 April.

Samsung Electronics Co., Ltd. (2024) ‘Samsung Reveals 2024 AI Home Appliances at “Welcome to BESPOKE AI” Event’, Samsung Global Newsroom, 3 April.

Truong, Y., McColl, R. and Kitchen, P.J. (2009) ‘New Luxury Brand Positioning and the Emergence of Masstige Brands’, Journal of Brand Management, 16, pp. 375–382.

Uluturk, A.S. and Asan, U. (2024a) ‘Examining the Moderating Role of Reasons in Masstige Luxury Buying Behavior’, Behavioral Sciences, 14(1), 67.

Uluturk, A.S. and Asan, U. (2024b) ‘Masstige Luxury Buying Behavior’, Encyclopedia, 7 February.

Similar Post