Why the Cross-Border Payments Market Rewards Trust Over Tokens

Authored on

Modified

Cross-border payments are still inefficient, but trust matters most XRP saw the problem early, but did not win the market As payments and capital markets merge, rankings help identify credible leaders

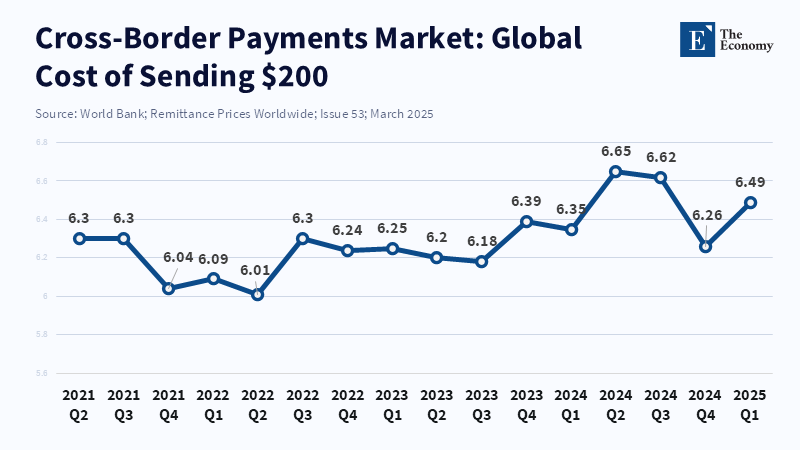

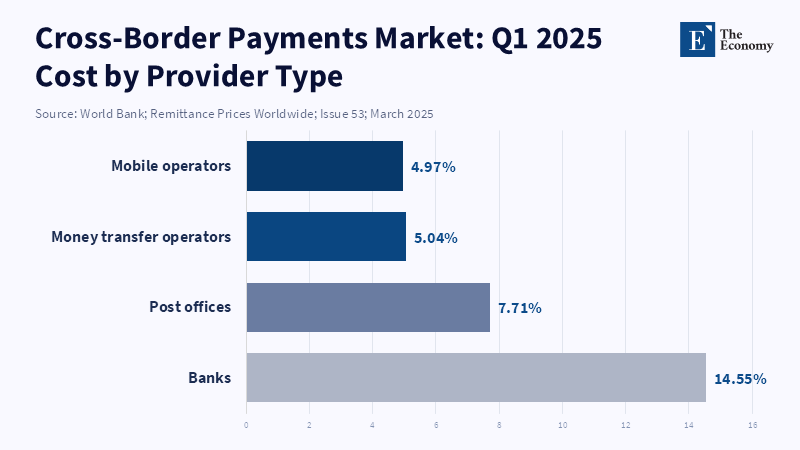

The cross-border payments ecosystem is still sufficiently broken to welcome reformers and still sufficiently important to reveal most of them. In the first quarter of 2025, the average cost of remitting US$200 from the G20 countries to others was 6.79%. Certainly, well over the long-term,declared global goals. And the Financial Stability Board has indicated that the G20's 2027 schedule cannot be expected to produce adequate world gains for end users. While stablecoins surpassed the $1.5tn cross-border payments figure, the IMF pointed out that in 2024, the total cross-border traditional and crypto payments neared $ 1,000 billion, yet stablecoins were only a slice of that. That is the real takeaway. Lack of demand was never the issue. The issue was that the ecosystem deteriorated into a war over trust, rules, balance sheet strength and reach, not speed of code. That is why years of effort and patience to rescue XRP have so far gained headlines but not market mastery. That's also why the next stage and the capital markets are potentially as relevant as payments.

Reframing the cross-border payments market as a capital markets story

The problem with the classic reading of the cross-border payments story is that it is viewed purely as a tech problem. Whereas, there is a better way of viewing it as a market structure problem. BIS now portrays the cross-border payments market as a market with weak links between systems, two-sided network effects and governance frictions that private actors cannot solve alone. And this is important because capital markets are not willing to pay up solely for a simple engine. They are willing to pay for systems that can win on both sides of the network, receive and transmit compliance tests, operate cross-border, integrate into treasury processes and be comprehensible to regulators, auditors and boards. Once the framing change happens, the debate changes. It is no longer about how fast a token settles on paper. It is about which model can become trusted infrastructure across banks, brokers, custodians, payment firms and corporate treasury teams, without elevating new legal risks. Simply put, the cross-border payments market is not just a fintech narrative. It is literally a course on who will get to build the rails for worldwide liquidity.

And that framing matters now, because the market is no longer awaiting one clean break from the past. It is being reconstructed, incorporating various upgrades. A report by the Reserve Bank of Australia notes the increasing presence of domestic fast payment systems and the growing efforts to link them across borders, though it offers no hard data on the number of countries or cross-border gateways involved. The ECB reports there is evidence that connecting them could lift trade by around 4%. While transferring the current Venmo user experience to cross-border payments appears to be now available, Swift is simultaneously upgrading its aging infrastructure and creating a shared ledger for tokenized deposits. Stablecoins are actually providing valuable value in some corridors. Banks are experimenting with programmable cash, tokenized deposits and novel layers of coordination. The outcome is not a simple capitulation of the old system to one crypto backbone, but a dense infrastructure platform in which incumbents, challengers and hybrids are all competing for the same prize: trusted reach across systems. That is why the story, on the supply side, ultimately blinks straight into capital markets. Whoever configures cross-border value transfer will determine the pace of liquidity, the movement of collateral, the execution of FX, the switching of settlement risk and finally, where financial power resides.

The reasons why the best cross-border payments market did not actually give XRP the crown

Always the simplest premise, XRP 's basic argument was that,economically, travel and settlement were lengthy and pricey, because money passed through extensive bank chains and required cash laddered in advance; a bridge asset should free stranded capital and shorten clearance. That argument retains potency and can account for the traction achieved by Ripple, which has established upside-down penetration in over ninety markets, achieved more than 60 licenses worldwide and claims its payments layer has processed $70bn in volume. Otherwise, the cross-border payments proposition didn't morph into market saturation because purchasers paid for factors beyond speed: they didn't simply pay for payment rail, choosing instead who they could place reliance upon for compliance, performance, legal finality, accounting, corridor coverage and governance.

That difference matters. Swift still connects more than 11,500 institutions in more than 200 countries and territories and more than 4 billion accounts today and claims that 90% of payments on its network are delivered into beneficiary banks within an hour, with 99% settled within a day. Those numbers do not make the system perfect, but they demonstrate that reach, dependability and institutional mass are just as important as pure design. Even Ripple's own 2025 strategy page demonstrates the direction the market has taken. The company assimilated RLUSD into Ripple Payments and began to push stablecoin, enabling cross-border payments much closer to the core of its offering. That's not necessarily a repudiation of XRP. But it does highlight that enterprise (read: buying) clients increasingly want instruments that may be more appropriate within regulated margins. Combine the FSB's 2025 warning that the regulatory regimes for stablecoins and crypto remain uneven and rife with opportunities for gaming,and it's suddenly clear. A bA bridge asset can be used to great effect and still fall out of favor if clients decide that self-governing money is the longer-term safer bet.

How is this change going to affect the competition among markets

Once payments are regarded as capital market plumbing, the competitive map shifts. Winners won’t necessarily be those with the fastest routes from point A to B, but those who wield the tools that turn liquidity into a resource for treasuries, securities, FX and collateral workflows. Swift’s shared ledger vision for 2026 opens the way for mapping out. The goal isn’t just enabling retail payments better; it’s tokenized deposits with multiple settlement options underpinned by architectures able to support FX payment,versus payment and security,related cash movements—and that’s where cross-border payments overlap with capital market design. The reward isn’t just revenue from payments: it’s a powerful slice of the operating system of world finance.

That sets up another sort of competition. Rather than selling their one product, banks, exchanges, storage providers, stablecoin publishers, transaction roadways and cash card networks are selling the belief that their pile will stay available, light and rules,abiding during the market splits into more paths, more asset symbols and more 24/7 requirements. The IMF's recent examination of stablecoins assists in this regard. It indicates that stablecoin cross-border flows are growing quickly, but still constitute only a small part of the broader market, while the dollar still benefits from profound trust, strong network effects and the size of US financial markets. The takeaway isn't necessarily that crypto does not matter. It's that adoption most often depends on authoritativeness, not freshness. In finance, finance still runs to the institutions that diminish control risk and function smoothly with current reservoirs of funds. That's the reason tokenized deposits, regulated stablecoins, connected fast payment systems and modernized bank rails are all piquing significant total attention simultaneously.

Why have so many rankings become the infrastructure of this market

This is also the moment when rankings, benchmarking and comparative market intelligence cease to be media add-ons and start to behave like infrastructure. The market for cross-border payments is getting too frenzied, too technical and too prestige-sensitive for buyers to judge by brand testimonials alone. A bank selecting a new payment partner, a treasurer trying to choose a liquidity model, an investor evaluating infrastructure companies, or a corporate contemplating entry into a new corridor are none of them simply buying software; they are all making a judgment on counterparty quality. In that environment, rankings have more value because they reduce search costs, convert diffuse information into convenient shorthand and clarify which firms are setting up a real source of strength. In fragmented industries, curated credibility is no mere frippery. It helps coordinate choices.

You can argue all of those points but you can't argue that all rankings are bad—and the solution is not to ignore some markets' need for a lens. In contrast to a weak ranking, a good ranking can enable an analysis that compares what buyers need to know. In cross-border payments, if you want a ranking to help measure output against input, you could compare corridor coverage, settlement certainty, licensing depth, transparency, client composition, access to liquidity, percentage of time the system is up, breadth of connectivity, balance sheet strength and actual volume beyond pilot theatre. Such a ranking, driven analysis is not only more relevant, but it also grounds the market by—gasp—making firms deliver instead of talk. It endows them with a need to stay real and takes away the nefarious appeal of excess hype. You see the very same truth in advisory, legal, medical and wealth, where it's just getting harder and harder to ignore the role of rankings.

The cross-border payments market is thus entering a phase more advanced than many crypto stories had speculated. The Gaps are no longer between old finance and new technology. They are between the infrastructures that are capable of gaining institutional trust and those that aren’t. XRP helped frame the problem before others and brought the discussion closer to the future, but the world that it sought to transform did not settle on a single bridge asset. It settled on governance, reach, compliance and fit. This transition is already remaking capital markets by reframing how liquidity units are distributed, how settlement value is sourced and where reputational capital is built. In a new world, the firms that succeed most will do more than move money around; they will make themselves credible, comparable and visible within a busy global system. And that is why rankings are no longer marginal to the subsequent narrative. In this market, they are becoming part of how the market determines who is worthy of capital, trust and Enterprise.

References

Adrian, T. et al. (2025) Understanding Stablecoins. Departmental Paper No. 25/09. Washington, DC: International Monetary Fund.

Claessens, S. and Rice, T. (2026) Cross-border payment technologies: innovations and challenges. BIS Papers, No. 167. Basel: Bank for International Settlements.

Ferrari Minesso, M., Lebastard, L. and Triay Bagur, O. (2026) ‘Unlocking trade potential: the benefits of improving cross-border payments’, Economic Bulletin, Issue 2. Frankfurt am Main: European Central Bank.

Financial Stability Board (2025) G20 Roadmap for Cross-border Payments: Consolidated progress report for 2025. Basel: Financial Stability Board.

Team Ripple (2025) ‘Ripple Integrates RLUSD into Ripple Payments Driving Enterprise Demand and Utility’. San Francisco: Ripple, 2 April.

Swift (2026) ‘Swift’s blockchain-based shared ledger progresses to MVP implementation’. 30 March. La Hulpe: Swift.

World Bank (2025) Remittance Prices Worldwide: Issue 53, March 2025. Washington, DC: World Bank.

Similar Post