U.S. Mortgage Rates Fall Below 6% for First Time in Three Years, Marking Psychological Inflection Point Amid Rising Home Prices

Authored On

Modified

Average 30-Year Fixed Mortgage Rate Drops to 5.98%, First Sub-6% Reading in Three Years Mortgage Rates Remain Elevated Even as Home Prices Climb Break Below Key Psychological Threshold Fuels Hopes of Housing Market Rebound

The average rate on a 30-year fixed mortgage in the United States has fallen below 6%, reaching its lowest level in roughly three years. As inflationary pressures ease and the Federal Reserve maintains a rate-cutting stance, mortgage rates have continued a gradual downward trajectory. The moderation in borrowing costs is expected to exert recalibration pressure across the broader structure of U.S. housing expenses.

Mounting Housing Cost Burden Dampens Mobility

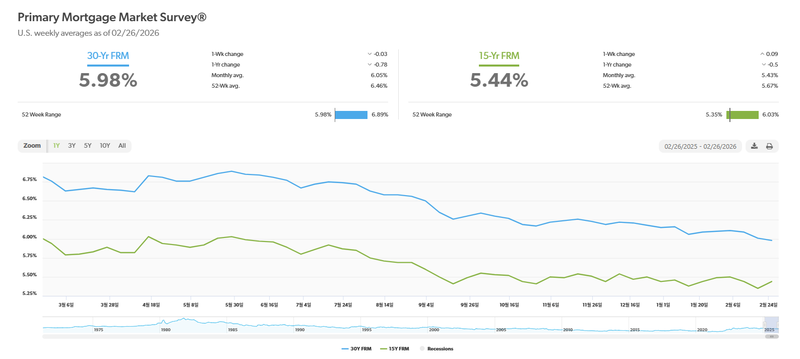

On the 26th local time, Freddie Mac, the U.S. government-sponsored mortgage enterprise, reported in its Primary Mortgage Market Survey (PMMS) that the average rate on a 30-year fixed mortgage declined to 5.98%. This marks a 0.03 percentage point drop from the previous week’s 6.01% and a 0.78 percentage point decrease from 6.76% a year earlier. It is the first time since September 2022 that the 30-year rate has fallen below the 6% threshold. Compared with the same period a year ago, the rate has retreated by 78 basis points.

U.S. mortgage rates had surged above 7% at one point in January last year, sending warning signals across the housing market. Elevated borrowing costs have since materially slowed market activity. Homeowners who secured properties under lower-rate mortgages have been reluctant to trade up amid higher rates, while prospective buyers have deferred purchase decisions in the face of sharply increased financing costs, entrenching a contraction in transactions. This phenomenon is widely referred to as the “golden handcuffs” or “locked-in effect,” reflecting the reluctance of homeowners to forfeit favorable existing rates, thereby constraining housing mobility.

According to a recent survey by real estate brokerage Redfin, U.S. home purchase agreements have continued to trend downward overall. As of January, contract activity declined in all but five of the 50 most populous metropolitan areas. Oakland, California, recorded the steepest drop, with contract volume falling approximately 21.6% year over year.

The time required to secure a sales contract has also lengthened. The median duration to contract signing for a typical home reached 66 days, about one week longer than a year earlier and the longest since early 2019. Housing inventory currently stands at a 5.5-month supply, the highest level in seven years. Months of supply measure the time required to exhaust existing listings at the current pace of sales; a higher figure indicates a shift toward buyer leverage.

First-Time Homebuyers Now Enter Market at Age 40

Affordability pressures remain acute. Since 2019, U.S. home prices have risen more than 50%, while ownership-related costs—including electricity bills, homeowners insurance premiums, and property taxes—have also climbed, intensifying the financial burden. Ongoing uncertainty surrounding employment stability has prompted many households to postpone large-scale expenditures.

The broad rise in housing costs has delayed the timing of first-time home purchases. According to the National Association of Realtors (NAR) in its latest Profile of Home Buyers and Sellers covering July 2024 through July 2025, the median age of first-time homebuyers has reached 40 for the first time on record. When the survey began in 1981, the average age of first-time buyers stood at 29 and remained at or below 33 for decades. The figure rose to 36 in 2022 and 38 in 2023, ultimately reaching 40 last year. The data underscore how surging home prices combined with higher interest rates have materially raised barriers to entry for younger households.

The median age of all homebuyers climbed to 59, also a record high. Compared with 47 in 2019, just before the COVID-19 pandemic, this represents a 12-year increase over six years. The share of first-time buyers has contracted sharply as well. Last year, they accounted for just 21% of total transactions, down from 50% in 2010. Delayed entry into homeownership risks widening wealth disparities. Residential property values have historically appreciated at an average annual rate of roughly 5%, and NAR estimates that purchasing a home 10 years earlier can generate approximately $150,000 in additional economic gains compared with delayed entry.

Improved Purchasing Power as Mortgage Rates Ease, Potential Release of Pent-Up Demand

Conditions have begun to shift as mortgage rates have trended lower in recent months. According to the Associated Press, the 30-year fixed mortgage rate has declined for three consecutive weeks. Mortgage rates typically track the yield on the 10-year U.S. Treasury note, which lenders use as a benchmark in pricing home loans. As of 12 p.m. on the 26th local time, the 10-year Treasury yield stood at 4.02%, down 0.05 percentage point from the previous week.

The easing reflects moderating inflation and heightened economic uncertainty. After President Donald Trump signaled a large-scale purchase initiative for mortgage-backed securities (MBS), bond yields stabilized, with spillover effects on mortgage rates. MBS are securities backed by pools of home loans, and movements in this market directly influence borrowing costs for end buyers. Increased demand for MBS compresses yields, which in turn translates into lower mortgage rates. In addition, the Federal Reserve’s three rate cuts in the second half of last year have supported long-term yield stability. Market participants increasingly believe the monetary tightening cycle has peaked, ushering mortgage rates into a gradual adjustment phase.

Financial institutions and real estate market participants view the break below 6% as a symbolic inflection point. In recent years, the 6% level has functioned as a psychological ceiling constraining buyer sentiment. With rates now in the 5% range, analysts suggest that some sidelined demand could re-enter the market. Bill Banfield, Chief Business Officer at major U.S. mortgage lender Rocket, stated that borrowers have come to accept that a return to ultra-low rates in the 3% range is unlikely, adding that the 5% to 6% corridor is increasingly perceived as the new baseline. A rate beginning with a “5” could encourage dormant demand to convert into actual transactions.

Lower rates directly enhance household purchasing capacity. According to online real estate platform Zillow, as of January this year, under a roughly 6% rate environment, a median-income U.S. household could afford a home priced at $331,483, the highest purchasing power level since 2022. Even a 0.5 percentage point decline in rates can translate into several hundred dollars in monthly payment differences, generating a tangible affordability impact. Should rate stabilization persist, refinancing demand from borrowers who purchased homes during the high-rate period is also expected to expand.

However, forecasts suggest limited room for further substantial declines. The Mortgage Bankers Association projects an average mortgage rate of 6.1% this year, while Fannie Mae anticipates a level around 6%. Bhavesh Patel, head of consumer channels at Chase Home Lending, JPMorgan Chase’s mortgage division, noted that given current conditions, rates are unlikely to deviate significantly from the upper-5% to low-6% range. The Federal Reserve, at its latest meeting, held its benchmark rate steady and reiterated that additional cuts would hinge on clearer evidence of sustained inflation moderation.

Similar Post