“U.S. Economic Optimism Fades” Growth Loses Momentum, Prices Stay Sticky, and Stagflation Fears Turn Real

Authored On

Modified

Growth forecasts revised downward in successive rounds, signaling weakening economic fundamentals Tariff effects fade as investment and consumption cool, accelerating the downturn Surging oil prices and mounting price pressures heighten stagflation risk

The U.S. economy is entering an unmistakable downcycle. The confirmation of fourth-quarter growth at 0.5%, following two consecutive downward revisions, reflects a rapid deterioration in the country’s economic fundamentals. With both consumption and investment losing traction at the same time, the adverse effects of tariff policy and the transition toward a capital-driven growth structure are amplifying downward pressure on the economy. Compounded by a sharp spike in oil prices, the U.S. economy is moving swiftly into a multifaceted crisis marked by the overlap of stagnation and rising inflation.

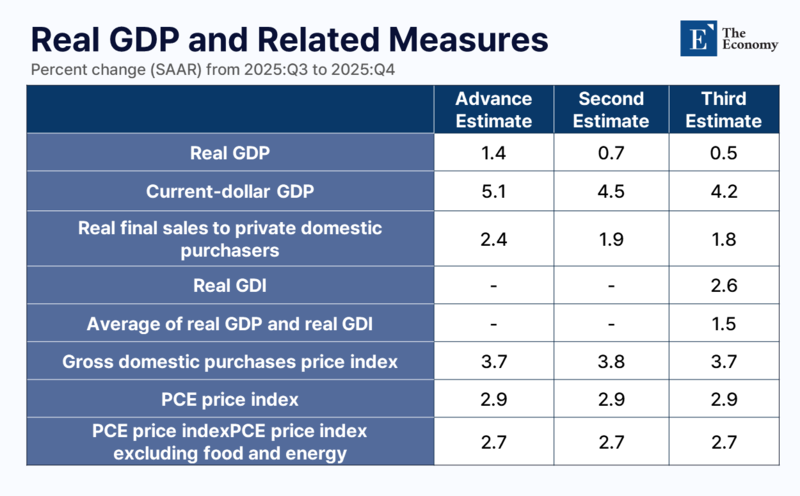

U.S. Final Q4 Growth Confirmed at 0.5%, Marking Sharp Drop From Q3

According to the U.S. Commerce Department on April 9 local time, final fourth-quarter GDP rose at a seasonally adjusted annualized rate of 0.5% from the previous quarter. That was 0.2 percentage point below the preliminary estimate of 0.7% released last month and also fell short of the 0.7% consensus forecast compiled by Dow Jones. It marked the weakest performance since the first quarter of 2025 and represented a sharp decline from 3.8% in the second quarter of last year and 4.4% in the third quarter. The U.S. government releases GDP in three stages—advance, preliminary, and final estimates—with the final reading incorporating economic activity indicators omitted from the preliminary calculation.

The downward revision to growth reflected declines in corporate intellectual property investment and inventory investment. With weakness in business investment, a leading indicator of the economic cycle, now confirmed, concerns over the erosion of growth momentum are intensifying. Consumption, which accounts for more than two-thirds of the U.S. economy, also slowed. The growth rate in consumer spending was revised down from 2.0% to 1.9%. Real final sales to private domestic purchasers, the combined measure of consumer spending and total private fixed investment closely watched by policymakers, rose only 1.8%. That was revised down from 1.9% and marked a clear slowdown from 2.9% in the third quarter.

U.S. real GDP growth for last year on a year-over-year basis also came in at 2.1%, unchanged from expectations. The interpretation is that tariff measures imposed in the first half of last year prompted companies and households to front-load purchases, while imports climbed to a record high, widening the trade deficit and ultimately slowing fourth-quarter growth. The core personal consumption expenditures price index for February, the inflation gauge most closely watched by the Federal Reserve, rose 3.0% from a year earlier, in line with market expectations and slightly slower than the previous month’s 3.1%. Personal spending in February, a key engine of the U.S. economy, also increased just 0.5% from the previous month, undershooting the 0.6% forecast.

Tariff Effects Fade as the Economy Enters a Downturn Phase

Until the beginning of this year, concerns over a U.S. recession had remained limited. Contrary to earlier expectations, the U.S. economy had continued to post resilient growth. Defying recession fears, U.S. growth in the third quarter of last year reached 4.3%, the highest in two years and well above the market’s prior forecast of 3.2%. There were questions over the reliability of the data due to the impact of the federal government shutdown, but November consumer inflation also came in at 2.7%, below the 3.1% forecast. Added to that, sharply rising expectations for economic growth and the performance of the stock market left little doubt that the economy was in expansion.

The economic indicators released this time, however, uniformly point to the U.S. economy having entered a clear contraction phase. Experts broadly agree that as the short-term stimulus effects of the Donald Trump administration’s tariff policy began to weaken after a certain point, the real economy moved abruptly into a correction phase. In the early stage of the policy rollout, tariffs supported growth through domestic demand stimulation and expectations of supply-chain reorganization. As time passed, however, the adverse effects of higher costs and shrinking trade began to materialize in earnest.

Goldman Sachs, in fact, estimates that Trump’s tariff policy has already added more than 70 basis points to core inflation. Excluding that tariff effect, underlying inflation would appear far more contained. Core consumer price inflation is estimated at roughly 1.75%, while core PCE is put at around 2.25%, suggesting that the tariff policy itself is generating significant inflationary pressure.

Oil Shock Adds to Economic Strain

Signs of a U.S. downturn can also be found in the extreme income polarization of a K-shaped economy. According to Moody’s Analytics, households in the top 10% of the income distribution accounted for 49.2% of consumer spending as of the second quarter of last year. Put differently, the remaining 90% accounted for only 50% of consumption, highlighting severe income disparity. Data from the Federal Reserve Bank of New York show that 4.8% of total household debt was delinquent as of the end of December last year. U.S. credit-card delinquency rates also stood at 12%, the highest level since the 2008 financial crisis.

The reason the economy has become fractured by such extreme polarization is that the U.S. growth model is shifting toward one in which capital contribution is expanding relative to labor input. Before the emergence of generative artificial intelligence, and even before the COVID-19 pandemic, corporate profits—or GDP as the aggregate of value added—and labor input, measured by nonfarm employment, moved with similar slopes, showing a structure in which value creation and labor contribution were closely linked. Since then, however, with the post-pandemic reopening and the onset of the AI era, labor input has merely recovered its previous trend, while corporate profits have risen on a completely different trajectory. That widening gap reflects the growing contribution of capital rather than labor. Unless labor income rises alongside it, the consumption base can only continue to weaken. As a result, consumer retrenchment is likely to deepen over the medium to long term, raising the possibility that the sustainability of economic growth will be undermined.

Against that backdrop, external geopolitical shocks are pushing the U.S. economy deeper into fears of stagflation. At the end of last month, Moody’s Analytics raised the probability of a recession within the next 12 months to 48.6%. That is well above the historical average of around 20%. Mark Zandi, chief economist at Moody’s, said, “The risk of recession is uncomfortably high and rising,” adding, “It is now becoming a real threat.”

Other Wall Street institutions have also raised their recession probabilities across the board. Goldman Sachs lifted its estimate to 30%, while Wilmington Trust raised its forecast to 45%. EY-Parthenon projected a 40% probability and warned that “if the Middle East war becomes prolonged or intensifies, that probability could rise sharply.” BCA Research also raised the likelihood of a U.S. recession over the next 12 months from 30% to 40%. BCA Research said deteriorating labor-market conditions, slowing retail sales, and inflation risk stemming from higher oil prices were increasing recession odds, adding, “The U.S. economy was not in a fully strong state even before the oil shock hit, and if the oil shock persists, that alone could drag the economy into recession in the second half of this year.”

Nobel Prize-winning economist Paul Krugman also warned that a sustained oil shock could produce severe economic consequences. He said, “If oil supply from the Gulf region continues to decline in the short term, the impact on the U.S. economy could be severe.” Krugman has previously cautioned that conflict in the Middle East could become the final blow that pushes the U.S. economy over the edge. Those assessments reflect expectations that as oil prices and inflation rise in tandem amid Iranian geopolitical risks with no clear exit, downward pressure on the economy will intensify as interest-rate cuts are delayed. In fact, excluding extraordinary episodes such as the pandemic, surging oil prices preceded nearly every recession phase since the Great Depression.

Similar Post