The EU Carbon Border Tax Cannot Stay a Green Tariff

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

The EU carbon border tax works like a green trade barrier for many non-EU firms It may help EU producers now, but that edge will not last Without technology transfer, it risks becoming protectionism, not fair climate policy

In April 2026, the EU Commission released the first official price for CBAM certificates, which was 75.36/tonne. According to the OECD, in 2023, around 16 percent of global greenhouse gas emissions faced an effective carbon rate above 30 euros per tonne, while about 11 percent faced a rate above 60 euros per tonne. This gap in carbon pricing has been a key driver behind the EU’s carbon border tax discussions. The policy is a climate correction on paper, but a trade barrier on the ground to many non-EU businesses as the real business opportunity for Europe: the policy prices not only carbon, but the gap in clean power, production technology, emissions accounting and compliance capacity as well, so the second stage of the policy is of crucial importance. Whether the EU carbon border tax turns out to be an act of green protectionism or an instrument for industrial upgrades, a better framework for shared standards and technology transfers remains to be seen.

The Reason Why the EU Carbon Border Tax Looks Like an Import Tariff to Foreign Firms

The arguments for the EU carbon border tax are quite clear: if EU firms pay the rising carbon price while those outside the EU do not, production might shift elsewhere, emissions could leak out, and dirtier producers would have an unfair price advantage over greener firms in Europe. To prevent such a scenario, the policy has been implemented, which will cover a range of goods, including cement, iron and steel, aluminum, fertilizers, electricity and hydrogen. According to the European Parliament, the EU's carbon pricing through its emissions trading system is designed to encourage industrial decarbonization and prevent companies from relocating production abroad in response to carbon costs. According to the OECD, the EU’s Carbon Border Adjustment Mechanism (CBAM) targets highly carbon-intensive sectors to ensure imported goods face the same carbon costs as EU-produced goods, aiming to prevent carbon leakage rather than serve as a protectionist measure. The OECD notes that the items covered by the CBAM accounted for just 0.31 percent of global greenhouse gas emissions in 2022, and it is projected to generate around €14.7 billion annually at a carbon price of €80 per tonne, provided trade flows remain unchanged. This would be achieved by reorienting EU sourcing toward more climate-friendly suppliers.

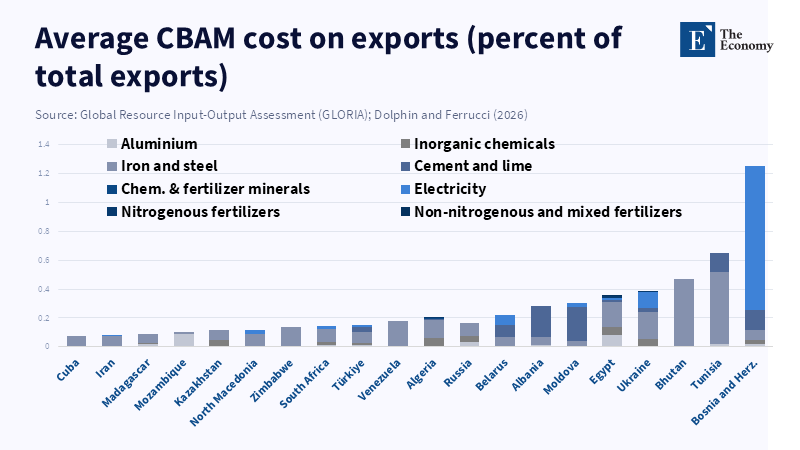

However, reality does not always match projections. While direct impacts of the EU carbon border tax on EU trade are modest according to IMF projections, country and product-level effects can be considerable. On average, the mechanism increases EU import prices and countries' export costs to the EU by 0.1% and 0.04%, respectively. Nevertheless, specific countries face up to 1.2% price increases, and specific goods-iron, steel, aluminum, and electricity-show more evident effects at the product level. Therefore, foreign companies often experience the EU carbon border tax as an unfair hurdle, in the form of lost contracts, lower profit margins, and new reporting requirements, rather than just climate adjustment.

The EU Carbon Border Tax is Essentially a Readiness Test

This is where the core issue of the ongoing debate about the EU carbon border tax lies. According to the OECD, the EU Carbon Border Adjustment Mechanism is a groundbreaking effort to address carbon leakage by making sure imported and EU-produced goods face similar carbon pricing. As a result, this policy has been seen not just as climate policy or protectionism, but also as both a tool for managing carbon emissions and testing readiness. In practice, the initial winners have not always been the greenest companies overall, but those best equipped to track emissions data, purchase clean energy, and improve their production processes. and documenting compliance. The early evidence indicates that CBAM is influencing neighboring countries to implement more carbon pricing, indicating that the measure could spread pressure for policy reforms to other regions; however, it also highlights that low-income economies will need additional assistance, lest the pressure become more about exclusion than climate mitigation. Without it, the EU carbon border tax simply formalizes the current technological gap and makes those outside the EU pay for it.

This topic is particularly relevant for educational journals since readiness is built through learning, from vocational and engineering institutions and business schools, to customs academies and corporate training programs. Once the EU carbon border tax becomes a more permanent feature of global trade, the tracking of embedded carbon, the electrification of industries, the use of low-carbon technologies in metallurgy and the overall understanding of carbon markets will move from niche expertise to a necessity. Educational institutions must therefore consider the implications of this for their curricula as a significant policy and industrial issue, not just abstract sustainability rhetoric. Companies and governments must also move away from the idea that regulations alone will drive decarbonization; it requires trained employees to monitor embedded carbon, optimize processes, and meet complex reporting requirements at the border. Those businesses and workers who can learn and adapt quickly will thrive.

Short-Term Gains with Long-Term Exposure

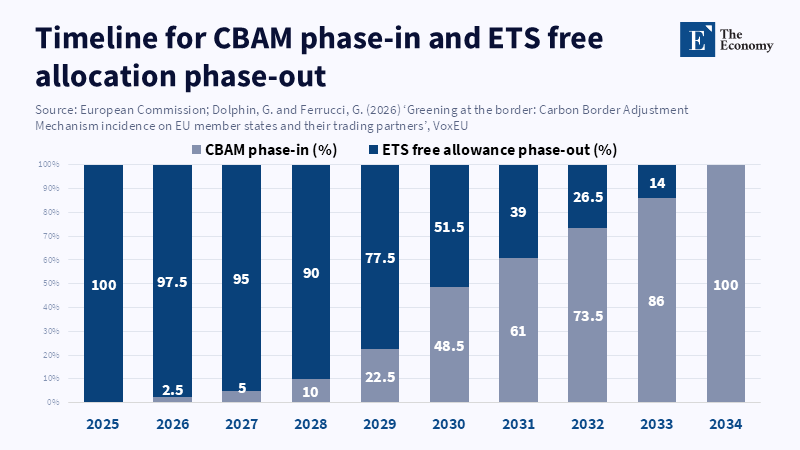

In the short run, some European businesses will benefit from the EU carbon border tax. This is an essential, though sometimes unpalatable, truth for defenders of the policy: the goal of the measure is to reduce the cost advantage of producers without carbon costs to a smaller gap relative to those within the EU, hence some trade diversion is inherent. An example given is in the steel industry, where imports are projected to decline by 24% by 2034 due to the EU carbon border tax. In fact, import charges on steel shipped to the EU were estimated to rise significantly for highly carbon-intensive products over the next decade. Therefore, it is understandable that foreign businesses may perceive the EU carbon border tax as an import tariff. It will hit the dirty and slow-to-adapt the hardest.

However, this short-term advantage cannot last on its own. It is the stimulus for foreign businesses to upgrade, either through investments in clean power, less emissions-intensive manufacturing, or improvements to their compliance systems, and to gain their way back into the European market. Even OECD projections predict that the introduction of CBAM will increase EU import prices by at most 0.6%, except for basic, fabricated metal, electrical, and automotive industries that will see higher prices. The European Commission has admitted that the CBAM does not completely eliminate the carbon leakage risk associated with EU exports, and that leakage may even shift to more integrated or deeper-level parts of value chains, meaning the risk of Europe falling into the trap of over-reliance on the CBAM as a protectionist tool still exists.

The EU Carbon Border Tax Must Become an Investment in Learning, Not an Escalation of Protectionism

The most appropriate and sustainable long-term solution is for the EU carbon border tax to be transformed from an instrument of penalty to a platform for development. Europe should continue implementing it, but also offer comprehensive support and capacity building to developing countries and LDCs that have lower access to resources to achieve the green transition. Through partnerships such as joint ventures, supplier training, and long-term commercial agreements with EU businesses, European firms will benefit not from exclusivity but from the global expansion of cleaner industries. This approach would make the policy fairer and mitigate the risk of retaliatory trade measures, eventually avoiding an endless loop of escalating protectionist barriers. The core argument is that Europe must shift its support from minor technical assistance to real capability-building programs.

For educators and administrators, this implies clear priorities. Business schools need to educate managers about cost pass-through mechanisms and supplier improvement strategies. Engineering faculties must integrate industrial decarbonization as a central commercial concern. Vocational schools must train technicians in electric arc furnaces, hydrogen readiness, waste heat recovery, and digital monitoring techniques. European universities should also collaborate with international institutions on joint programs, as competition will be global rather than fortress-like. This is not just about altruism; it is a smart industrial strategy based on educational approaches. According to the OECD, if only European workers are trained and foreign competitors are simply taxed through the EU carbon border mechanism, the policy could act largely as a protectionist measure. However, fostering skills and competencies may help encourage cleaner competition and reduce reliance on ongoing protectionist policies.

The first official price for CBAM certificates, 75.36, puts a definitive figure on the EU's climate commitment. The broader implication of the EU carbon border tax, however, is political and communicative: Europe is signaling that market access will be increasingly contingent on carbon mitigation capabilities. This may drive positive industrial reforms but also reinforce the image of Europe cloaking industrial protectionism under the guise of climate policy. The ultimate impact depends on subsequent actions in factories, schools, and policy spheres. If the EU uses CBAM as a transitional mechanism to allow for a ramp-up in global technology transfer and supplier learning, it can ultimately achieve clean competition. If the EU treats it as an end goal in itself, it may precipitate a spiral of short-term protection, increased trade friction, and subsequent calls for further defensive measures. The EU must now choose the more difficult route of enabling broader industrial transformation, rather than locking itself into a permanent defensive posture, to ensure the long-term climate and economic sustainability of the EU carbon border tax.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bahí, A., Fuchs, M. and Reverdy, C. (2026) Carbon pricing beyond borders: assessing climate policy spillovers from the EU carbon border adjustment mechanism. Bruegel Working Paper 05/2026.

Dechezleprêtre, A. and Haramboure, A. (2025) ‘EU Carbon Border Adjustment Mechanism: What is it, how does it work and what are the effects?’, OECD Blog, 21 March.

Dechezleprêtre, A., Haramboure, A., Kögel, C., Lalanne, G. and Yamano, N. (2025) ‘Carbon Border Adjustments: The potential effects of the EU CBAM along the supply chain’, OECD Science, Technology and Industry Working Papers, No. 2025/02. Paris: OECD Publishing.

Dolphin, G. and Ferrucci, G. (2025) ‘The EU’s CBAM: Implications for Member States and Trading Partners’, IMF Working Papers, 2025(125). Washington, DC: International Monetary Fund.

Dolphin, G. and Ferrucci, G. (2026) ‘Greening at the border: Carbon Border Adjustment Mechanism incidence on EU member states and their trading partners’, VoxEU, 2 April.

European Commission (2025) A European Steel and Metals Action Plan. COM(2025) 125 final. Brussels: European Commission.

European Commission, Directorate-General for Taxation and Customs Union (2024) CBAM and developing countries/LDCs. Brussels: European Commission.

European Commission, Directorate-General for Taxation and Customs Union (2025) ‘Commission strengthens the Carbon Border Adjustment Mechanism’, press release, 17 December.

European Commission, Directorate-General for Taxation and Customs Union (2026a) Carbon Border Adjustment Mechanism. Brussels: European Commission.

European Commission, Directorate-General for Taxation and Customs Union (2026b) Price of CBAM certificates. Brussels: European Commission.

European Parliament and Council of the European Union (2023) Regulation (EU) 2023/956 of 10 May 2023 establishing a carbon border adjustment mechanism. Official Journal of the European Union, L 130, 16 May, pp. 52–104.

Fuchs, M. and Reverdy, C. (2026) ‘The European Union is exporting carbon pricing through trade’, Bruegel First Glance, 1 April.

Hasanbeigi, A., Springer, C. and Chobthiangtham, P. (2025) The Impact of the EU CBAM on Global Steel Trade: Implications for U.S. Steel Tariffs. Global Efficiency Intelligence.

OECD (2025) What to expect from the EU Carbon Border Adjustment Mechanism? OECD Policy Brief. Paris: OECD Publishing.

Siy, A.L., Wang, A., Zheng, T. and Hu, X. (2023) ‘Research on the Impact of the EU’s Carbon Border Adjustment Mechanism: Based on the GTAP Model’, Sustainability, 15(6), 4761. doi:10.3390/su15064761.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.