“Fee Cuts, Loan Curbs, and Delinquent Debt Pressure” Card Firms Losing Competitiveness Face Mounting Challenges in Defending Profitability

Authored On

Modified

Merchant fees ↓ Card loan delinquencies ↑ Corporate bond dependence remains in the 70% range All-out cost-cutting including voluntary retirement

As profits at credit card companies shrink, their contribution to group-level net income is weakening. With core business profitability eroded by merchant fee cuts, a surge in card loan delinquencies combined with tighter regulations is exerting simultaneous pressure on both profitability and asset quality. Additional pressure from “win-win finance” policies has fueled skepticism that, for card subsidiaries within financial holding groups, reintegration into banks may be the only viable path forward.

Last year, card firms’ net profit limited to $880 million

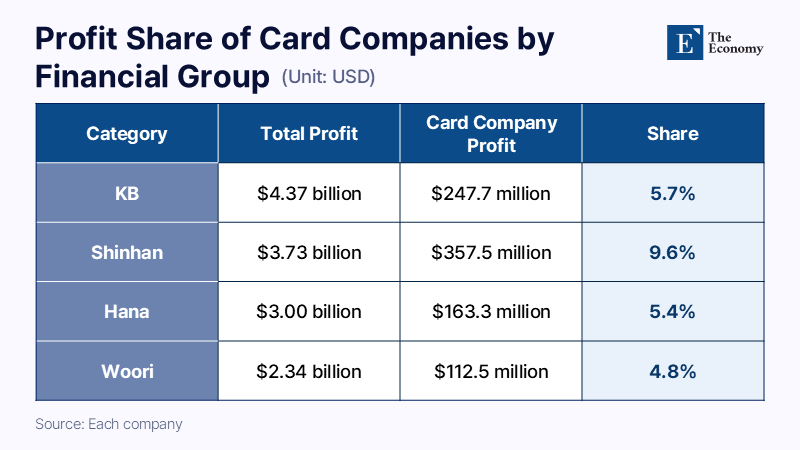

According to the financial industry on the 10th, the combined net income attributable to controlling shareholders of four card subsidiaries under the four major financial groups (KB, Shinhan, Hana, and Woori) totaled $880 million last year, down about 12.6% from $1.01 billion a year earlier. In contrast, the combined net income of the four financial groups rose 9.7% year-on-year to $13.45 billion from $12.27 billion. Performance was driven by non-card affiliates such as banks, insurance, and securities. As a result, the share of card companies in total group earnings declined sharply. Card firms accounted for 6.6% of total net income last year, down from 8.4% in 2023 and 8.2% in 2024.

Among bank-affiliated card companies, Shinhan Card—long the dominant player—saw its contribution to group net income fall from 12.9% in 2024 to 9.6% last year. KB Kookmin Card’s share dropped from 7.9% to 5.7%, while Hana Card declined from 5.9% to 5.4%, down 2.2 percentage points and 0.5 percentage points, respectively.

According to the Financial Supervisory Service, Shinhan Card’s net income for the first quarter of last year stood at $102 million, down 28.8% from $143 million a year earlier. For the first quarter of this year, forecasts suggest an additional 10–20% decline. Should this trend persist, net income could effectively be halved within two years. Other bank-affiliated card firms, including KB Kookmin Card and Hana Card, have also been navigating a challenging operating environment since last year.

A key factor has been the persistently unfavorable market environment driven by rising interest rates. According to the Korea Financial Investment Association, the yield on AA+ rated three-year specialized credit finance bonds stood at 4.01% as of the 8th, significantly higher than the 3.5–3.7% range a year earlier. After entering the 4% range on the 23rd of last month, yields have shown little sign of easing. With no deposit-taking function, card companies rely on bond issuance for roughly 70% of their funding. Rising bond yields translate directly into higher costs.

Credit card loan delinquency rates at commercial banks hit a 21-year high

Conditions in core operations remain challenging. The card industry has seen profitability in its credit sales segment deteriorate significantly due to cumulative reductions in merchant fee rates. Since 2012, financial authorities have recalibrated eligible costs every three years to lower the fee burden on small and micro merchants. The recalibration reflects funding costs, risk management costs, general administrative expenses, and marketing expenses. A further reduction implemented in February last year has continued to compress credit sales income.

Within the industry, there is growing recognition that a negative margin structure has effectively taken hold in core operations. While lending products such as card loans and cash advances have helped offset this, tightening government controls on household debt, stricter card loan regulations, and a shift toward high-credit borrowers have constrained further expansion. Last year, regulators reclassified card loans from “other loans” to “credit loans,” subjecting them to debt service ratio (DSR) rules. This limits loan amounts within borrowers’ annual income, reducing card loan capacity. Since July last year, the introduction of stress DSR—applying an additional 1.5% interest rate in loan assessments—has further tightened effective lending limits.

Amid these constraints, rising delinquency rates are placing simultaneous pressure on profitability and asset quality. According to the financial sector, the delinquency rate on credit card loans at domestic commercial banks reached 4.1% in January, up 0.9 percentage points from 3.2% at the end of last year. This marks the highest level in approximately 20 years and eight months since May 2005 (5.0%), when delinquencies peaked following the card crisis. Credit card loans, which include cash advances and card loans, are typically short-term credit instruments and serve as early indicators of funding stress within the formal financial system. After hovering in the 1–2% range, delinquency rates rose to the 3% range in 2024 and have now exceeded 4% this year.

This trend reflects tighter lending conditions across both primary and secondary financial sectors. As of the end of March, outstanding household loans at the five major banks—KB Kookmin, Shinhan, Hana, Woori, and NH NongHyup—totaled $574.3 billion, down $102 million from the previous month. With loan supply contracting at savings banks and other secondary financial institutions, demand has increasingly shifted toward relatively more accessible card loans. The rise in refinancing loans—where borrowers take out new card loans to repay existing ones—adds to the burden, signaling deteriorating repayment capacity.

Delinquent debt recovery rates hit record lows, skepticism over card business model spreads

A more pressing concern is the rising cost of credit losses due to declining recovery rates on delinquent debt. According to the Financial Supervisory Service, the amount of delinquent debt overdue by more than six months at eight major card firms reached $404 million as of the end of September last year, up 78.1% from $227 million a year earlier. This marks the first time since 2003 that such delinquent balances have exceeded $375 million on a quarterly basis.

Considering that card companies have been selling off non-performing loans over the past three years, the actual level of distress is likely more severe than reported figures suggest. Rather than pursuing prolonged collection efforts, firms have opted to sell delinquent debt at discounted prices to manage delinquency ratios. In the third quarter of last year, six major card firms that sold loan portfolios recorded gains of $436 million from such transactions, more than double the level at the end of 2021. By company, Shinhan Card led with $126 million, followed by Lotte Card ($116 million), Hyundai Card ($68 million), and KB Kookmin Card ($62 million). Shinhan, Lotte, and KB Kookmin together accounted for about 70% of total gains.

Behind these developments lies the full implementation of the Personal Debtor Protection Act in the first half of last year. The law introduced a cap on collection contacts—limiting them to seven times per seven days—as well as provisions allowing temporary suspension of collection efforts during disasters or accidents and granting borrowers the right to restrict collection methods and timeframes. These measures have significantly tightened the operating environment for delinquent debt collection compared to the past.

At the same time, weakening repayment capacity amid an economic slowdown has increased the inherent difficulty of recovering delinquent debt. As of the third quarter last year, the average delinquency rate (over one month overdue) at eight major card firms stood at 1.45%, up 0.04 percentage points year-on-year. As uncollectible loans rise, the volume of actual write-offs has also increased. Cumulative loan loss provisions reached $2.57 billion over the same period, highlighting the growing burden of bad assets. The trajectory mirrors conditions seen during the card industry crisis in 2014.

As industry conditions deteriorate, card firms are intensifying cost-cutting efforts, including workforce reductions. Shinhan Card implemented voluntary retirement programs both in June last year and again earlier this year as part of workforce optimization. KB Kookmin Card also carried out voluntary retirements early last year, restructuring its high-cost labor base for the first time in three years. The combined workforce of Shinhan, KB Kookmin, Hana, and Woori Card stood at 5,658 employees at the end of last year, down 4% from 5,891 a year earlier. Market participants expect that, for the time being, the earnings capacity of financial groups will be driven by non-card affiliates such as banks, securities, and insurance. A financial group official said, “While card firms are expanding into new businesses such as stablecoins and artificial intelligence, prospects remain challenging.”

Some argue that card businesses should be reintegrated into banks. Following the 2002 card crisis, KB Kookmin Card, Korea Exchange Card (now Hana Card), and Woori Card were absorbed into banks as part of restructuring efforts. As the card market entered a growth phase in the 2010s, these units were spun off again to expand operations. Within the industry, however, skepticism is growing that organizational streamlining and cost reduction represent the only viable path forward. A financial group official stated, “There is a prevailing view that card firms have limited capacity to independently establish a stable earnings base in the near term. With new payment methods such as stablecoins emerging, skepticism is spreading that beyond organizational downsizing and cost efficiency, there are few clear response strategies available.”

Similar Post