“Europe’s Enlarged M&A Arena on Deregulation” U.S. Capital Targets Companies Crippled by Chinese Competition

Authored On

Modified

A sweeping shift is underway in Europe’s M&A landscape as deregulation gathers pace U.S. investment banks internalize deal-sourcing capabilities through acquisitions of local advisory firms Global capital inflows accelerate as European corporate valuations decline

U.S. investment banks are stepping up their push into Europe’s mergers and acquisitions market. Rather than merely competing for individual mandates, they are increasingly acquiring local M&A advisory firms to secure, in a single move, the talent and networks needed to originate deals. This aggressive expansion is gaining further momentum as the European Union’s regulatory easing converges with the growing vulnerability of European companies weakened by Chinese competition.

U.S. Mid-Sized Houses Acquire European M&A Advisory Firms

According to the financial investment industry on April 21, U.S. investment bank Perella Weinberg Partners recently acquired British M&A advisory firm Gleacher Shacklock. The transaction was structured as a mix of cash and stock. Through the acquisition, Perella Weinberg Partners simultaneously secured around 30 Europe-based deal-originators, a network of senior executives at major British corporations, and deal pipelines in core sectors including defense and finance. The transaction gave the firm more than the capacity to win mandates. It also provided the infrastructure to create deals from the ground up.

The same pattern is emerging across other U.S. investment banks. Wall Street advisory giant Evercore entered the European market last year by acquiring British boutique advisory firm Robey Warshaw. Robey Warshaw is not a large firm, but it is an organization with access to critical relationships tied to major deals. The move is widely seen as a strategy to preempt transaction opportunities by securing a small cadre of elite dealmakers.

Traditionally, Europe’s M&A market has been defined by competition between European advisory firms and global bulge-bracket investment banks. The market has long been fragmented by country, while corporate decision-making structures have remained relatively closed, producing a landscape dominated by European advisers with control over local networks and global banks armed with capital strength and structuring capabilities. In that environment, mid-sized U.S. investment banks faced obvious constraints in both network access and deal origination. Recently, however, those firms have also begun expanding rapidly by successively acquiring local advisory shops. In particular, as roll-up strategies aimed at securing talent and client networks in one stroke continue to spread, these banks are elevating their capabilities to a level that can rival large investment banks.

“While Europe Obsessed Over Fairness, China Took Everything” EU Moves to Sharply Ease Merger Controls

The single biggest reason U.S. investment banks are concentrating on Europe is the easing of M&A regulation. The European Commission recently said it plans to significantly relax its standards for merger reviews. The core of the shift is that consumer harm and monopoly concerns will no longer serve as the principal criteria for approving or blocking mergers. Instead, the bloc plans to weigh factors such as the scale of business combinations, innovation, and sustainability in merger reviews. In other words, if a merger can deliver economies of scale and reinforce innovation leadership, the EU is prepared to approve it using a fundamentally different yardstick from the past.

The EU’s new merger-guideline framework, which is awaiting formal announcement, is expected to become the most radical institutional overhaul since the 2000s. European Commission President Ursula von der Leyen said, “We will make it mandatory to assess the impact on EU competitiveness for all new legislation.” The aim is to ensure that EU companies do not bear unnecessary costs and administrative burdens because of new regulations. She added that “Europe must support the growth of its companies in line with the realities of the global market,” lending strong backing to the reform package.

The EU is lowering review barriers and encouraging M&A because it has come to recognize the need for European champion companies capable of confronting the giant corporations of the United States and China. European companies have fallen behind their American and Chinese rivals across global industries, particularly in technology. As a result, Europe has become an economic bloc struggling to preserve even the status quo despite possessing an enormous single market. According to Eurostat, the EU’s statistical office, not a single European company ranks among the world’s top 20 by market capitalization. Apart from French artificial intelligence startup Mistral, Europe has also failed to produce innovation companies of meaningful scale. The European economy has likewise exposed its fragility amid the reordering of supply chains and the energy shocks triggered by the wars in Ukraine and Iran.

Calls from industry for an overhaul of the EU’s merger review standards have been mounting for years. A representative example came in 2019, when the German and French governments reacted sharply after the EU blocked the proposed rail business merger between Germany’s Siemens and France’s Alstom, a tie-up intended to counter CRRC, the world’s No. 1 rail company and a Chinese state-owned giant. At the time, the failed merger drew criticism for having obstructed the rise of a European company that could have mounted a credible challenge to CRRC’s dominance.

Europe’s Broader Corporate Exhaustion Creates a “Bargain-Hunting” Window

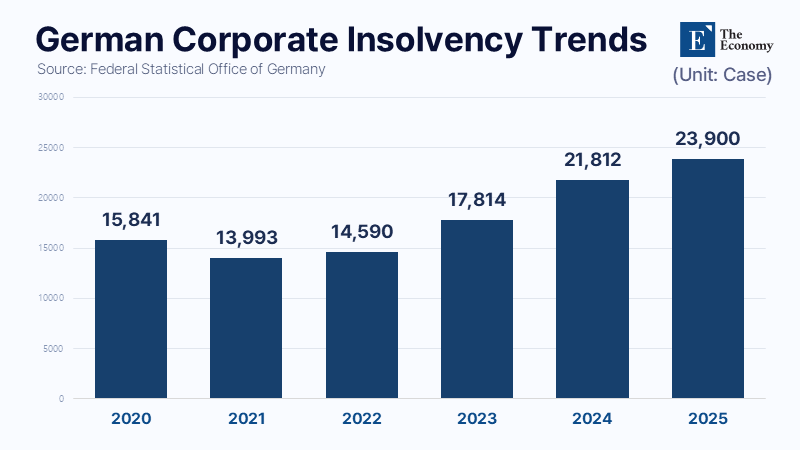

On top of that, the weakening financial stamina of European companies overall is also drawing in U.S. investment bank capital. According to Germany’s Federal Statistical Office, the number of corporate insolvencies in Germany rose 70%, from 13,993 in 2021 to 23,900 in 2025. As the fallout from those insolvencies spread, the number of unemployed people in Germany last year reached about 2.948 million, while the unemployment rate stood at 6.3%, the highest since 2013. In addition, roughly 107,000 jobs were affected at companies ranking in the top 10% by size among bankrupt firms. That figure was 164% higher than the pre-pandemic average, indicating that not only are insolvencies increasing, but distress among relatively large companies is also broadening.

By industry, bankruptcies were concentrated in construction and manufacturing. In construction, project financing became increasingly difficult under high interest rates, while rising raw material costs squeezed profitability, leading to a growing number of bankruptcies centered on small and mid-sized builders. In manufacturing, higher energy costs and weakening export demand worked in tandem, prompting a rising number of companies suffering simultaneous deterioration in profitability and liquidity to choose restructuring or formal insolvency proceedings.

Cracks in Germany’s Mittelstand model of powerful small and mid-sized industrial champions were first detected a decade ago. In 2016, KUKA, the world’s second-largest industrial robot maker, was sold to China’s Midea Group, while KraussMaffei, then the world leader in plastic processing machinery, was sold to China National Chemical Corp. After that, major manufacturing names including Getrag, Vossloh, Osram, and Viessmann were sold off to foreign buyers.

All of those companies commanded formidable market share in their respective niches, yet as competition intensified, they struggled to secure the capital they needed because of limited markets and closed governance structures. The manufacturing know-how that flowed out at that time has now returned like a boomerang a decade later. According to global consulting firm PwC, German auto-parts suppliers’ share of the global market fell to 23% in 2024, down 3 percentage points from a decade earlier. Over the same period, Chinese companies raised their share from 5% to 12%. China, once one of Germany’s most dependable export strongholds, has now become the most formidable competitive market eroding the position of German companies.

The sale of German companies is still continuing. Manz AG, the German automation equipment maker, went bankrupt last year in the aftermath of the contraction in Germany’s electric vehicle industry and was acquired by Tesla. Rema Tip Top, known as a hidden champion in tires and repair products, and Regent Feinbau, a core parts supplier to global automakers, have also been put on the market and are currently in acquisition talks with foreign capital.

The same conditions apply across other European companies. More recently, in particular, Europe’s M&A market has started moving again as interest-rate stabilization coincides with a rise in defense- and energy-focused transactions, alongside renewed private equity fund exit activity. These developments are expected to raise entry barriers in the European M&A market even further going forward. One investment banking industry official said, “It is becoming increasingly difficult to compete on deal-execution capability alone, and the number of dealmakers and depth of client networks a firm controls will emerge as the decisive variables determining success or failure,” adding, “The absorption of mid-sized advisory firms into large investment banks is likely to continue for the time being.”

Similar Post