Tokenized Deposits vs Stablecoins: Why 24/7 Settlement Still Ends at the Same Gate

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Banks need 24/7 liquidity, not just new tokens For users, both still depend on institutions The real gap is in the payment system itself

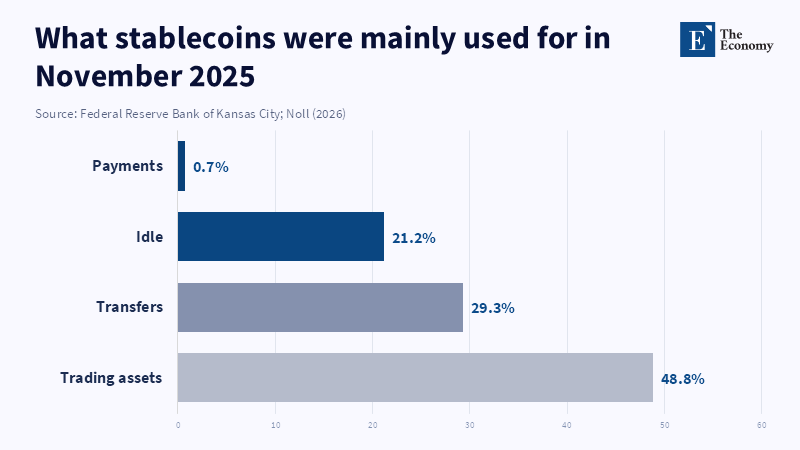

In November 2015, just 0.7 percent of stablecoins were being transacted on payment rails. That is the figure that should significantly dampen the current hysteria about stablecoins and tokenized deposits being fundamentally changing retail payments. The narrative currently sold to the market is far grander than that. Stock exchanges are pushing for more depth of trading hours. Platforms offering tokenized securities are reported to be following a buy-then-settle policy. Several large banks are said to be scaling up their plans for 24/7 trading. Stablecoins are being promoted as open, speedy, borderless cash. Tokenized deposits are being heralded as the safer, regulated cash of the next stage of finance. Those facts are relevant above all for issuers, exchanges, clearing platforms and treasurers; significantly less so for the ordinary consumer. For most households and small firms, both options still require a counterparty able to issue, redeem, exchange, verify and link back to regular money, just like the old system. The real innovation is not that money is moving away from middlemen; it's that they are now back in control in a new guise.

Settlement 24/7 is an institutional issue

And the strongest defense of digital asset settlement is, surprisingly, not user convenience but rather market structure. Home markets are growing. Settlement cycles are tightening. Tokenized assets are migrating from concept to reality. In January 2026, the owner of the NYSE, Intercontinental Exchange, announced that they are building a tokenized securities platform that will trade around the clock, settle instantly, facilitate dollar-sized trades and be funded by stablecoins and aims to launch. Banks are attracted to this space because, when markets are truly open 24/7, liquidity pressures do not follow branch hours and margin calls come before the weekend. As a result, many banks like BMO are issuing tokenized cash to clients who need to fund positions or pay in those off-hours.

It also explains why banks and credit unions may be attracted to tokenized deposits. They can offer a digital representation of bank money that stays on the books, preserves the deposit relationship and moves faster within a regulatory perimeter. This is a practical matter for banks; it would be preferable to update your own liability than to watch deposits walk out the door for stablecoin producers or exchanges. It's an even more compelling policy argument; tokenized deposits can more straightforwardly be brought under banking supervision, deposit insurance and central bank facilities. Stablecoins are outside that frame unless they are nudged toward it. This would seem in principle to be a clear difference: a stablecoin is a claim on a reserve-backed token; a tokenized deposit is a claim on a bank deposit.

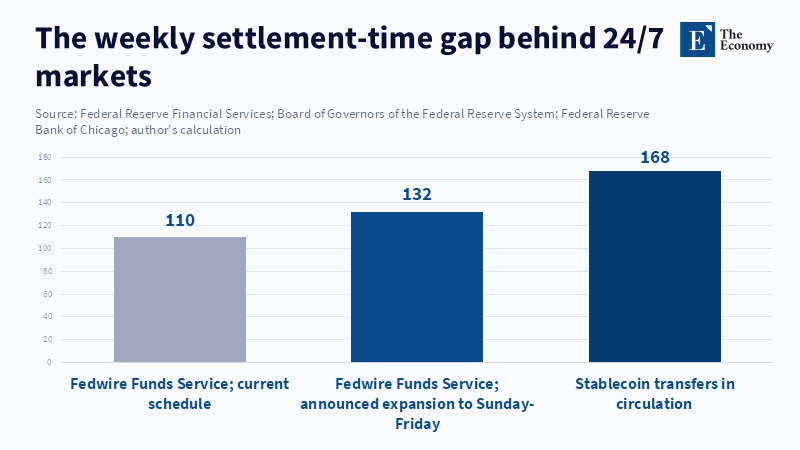

Nevertheless, it does not mask the reality that 24/7 settlement may not look anything like 24/7 final settlement. As the Chicago Fed has already commented, neither current instant payment networks nor existing stablecoin schemas can replace the Tier 1 settlement systems that play such an important role in the infrastructure of the capital markets. Some of the obligations settled using those systems total billions of dollars. While a tokenized transaction can settle on-chain in a matter of seconds, that does not necessarily mean it is final, redeemable at par, or has a robust, stable settlement asset in times of stress. The 24/7 settlement question we face is not just that, but whether the infrastructure can afford to provide 24/7 liquidity to satisfy the needs of the entire financial ecosystem.

A 24/7 settlement would't erase the middleman for the users

This is where the discourse often goes astray. Stablecoins have been hyped as close to Liquido, open and P2P; tokenized deposits have been hyped as programmable bank money. But the user will still have to live with a gatekeeper with each form of instrument. Stablecoins continue to require an exchange, a wallet, an onboarding with a bank and to be converted back into fiat for routine payments like wages, rent, or taxes. Tokenized deposits will require the banking system of the institution to meet standards, interoperate and have a settlement mechanism that settles conclusively between them, in order to allow customers to use tokens in different institutions. The gatekeeper has simply been renamed; the user chooses the identity of the intermediary to whom they hand over their claim, but they still need one.

Therefore, at the retail level, the distinctions between these instruments are almost always insignificant. Stablecoin supporters have the best of both worlds, arguing that bearer instrument-like use-cases benefit from being transferable without the issuer's prior approval for each transaction. Traders have the best of both worlds, noting that tokenized deposits lock the money into the bank's common, well-regulated system. The trade-off is revealed at the aggregate level of entire payment flows. A stable coin, like a tokenized deposit, is only useful if the recipient is prepared to accept it, the issuer is trustworthy and the holder has a practical, low-cost means to exchange or spend it. For the vast majority of retail consumers, what they end up with is not "liberation from their money," but the long, deliberate step-by-step journey through a closed and meticulously scheduled system.

This fact is again reflected in usage statistics that are too hard to ignore. As early as March 2026, Michael Barr from the Fed pointed out that the stablecoins still remained just for crypto trading and were not used for actual payments and the ECB came to similar observations at the end of 2025. For all practical terms, crypto trading seemed to be the stablecoins' main use and retail use was negligible when compared to total volumes. A research brief by the Kansas City Fed in April 2026 noted that out of the nearly US$3 billion worth of stablecoins that had been used in transactions, only 0.7 percent had been used for payments, while most of it had been used to trade, transfer between cryptosystems, or held idle. It doesn't mean that the stablecoins have no utility at all; it only means that the hype on the across-the-board payment revolution has long been recurring, without any empirical evidence!

24/7 settlement is mostly a bank liquidity issue and not a user experience issue

The difference is not, in contrast, in the way most people treat money. It is in the pressures on institutions, markets and regulators. Stablecoins, because they are not settled into bank reserves at each hop, may in some circumstances be the better approach, where global reach, continuous transfer and alignment with digital-asset markets are prioritized over being in a bank’s balance sheet. Tokenized deposits do the opposite; they retain the franchise for a bank and keep the money inside the institutional framework, giving treasuries greater visibility but preventing them from losing money to nonbank issuers. This is a crucial differentiation for the bankers; for the average person buying groceries or wiring funds domestically, it isn’t.

And this clarity is even more pronounced when being asserted in time. These stablecoins are being broadcast as persistent payments; a redemption to fiat still depends on an entity purchasing the product. During the Silicon Valley Bank's collapse in March 2023, the USDC fell to $0.86 and Circle acknowledged that the redemptions were 'subject to US banking hours'. This was not a technical failure but a clear declaration that this token is not unlike the traditional financial system without the logistical constraint. Although tokenized deposits sound like a safer story since they will always be bank liabilities and may therefore be supported by deposit insurance and the backing of the central bank, the system-wide tokenized deposit networks are still in debate. A BoE 2026 BIS working paper summarized a number of tokenized cross-border and wholesale transactions as "proofs of concept, prototypes or experiments" rather than functioning models. The safer approach is clearly the banking approach, but it also remains incomplete.

The counter comes quickly on these. They will cite the volume that stablecoins currently process, the potential reduction of costs for prefunding and reconciliation for tokenized deposits and the role they still offer consumers in poorly formed banking infrastructure. These are all relevant arguments. It is clear that some corridors, some firms and some regions may benefit significantly from increased access, faster settlement and the safeguards to local banking offered by these means. But this should not be confused with a net-beneficial difference for the average user within a well-formed banking system. The tools that offer an average consumer the things they want today are instant payment networks, cards, internet wallets and internet banking. In a well-formed banking system, the only remaining frictions are in cross-border flows, capital markets funding, collateral mobility and system interoperability. None of these are challenges a single new token can solve.

24/7 settlements: Re-necessitating the public plumbing; the new private tokens just aren't sufficient

The policy solution is clear. Regardless of whether branded as stablecoins or tokenized deposits, their substantive usefulness is best articulated in the proof points where the critical bottleneck is..) enabling continuous securities settlements, margin flows and treasury management processes by orchestrating liquidity with 24hr banking hours, live collateral treatment and just-in-time availability of Cash-in? Policymakers evaluating the value generated from the enhanced consumer payment capabilities enabled by the tokens should focus on transaction speed, required costs and security under crossing systems, whether branded as stablecoins or tokenized deposits, rather than on their branding; all systems working together should be worth more than their branding; no-speculation off-ramp costs should matter more than persist ideologies; certainty of redemption should matter more than the marketing claim of direct engagement,.

The need for public infrastructure is thus revealed. As bank and government debt become increasingly tokenized, the BIS argues that central bank money remains the core of the monetary future. Yet this is not a degenerate view. It is born out of the recognition that certainty of par, reliability and scaleability of money are all public goods that private issuers will fail to provide in times of stress. A 24/7 settlement system cannot be based merely on marketing pitches that promise stability, but on robust settlement infrastructure, shared standards, open access and that vital link back to central bank funds. Without it, speed will quickly turn into instability.

Thus, the wise attitude would be not to overstate the differences between stablecoins and tokenized deposits. It makes sense for banks and exchanges, for supervisors, funding policies and crisis plans. But for the normal user, the relevance of the issue must be secondary, since the two systems are still approached through intermediate gateways. Thus, the debate shouldn’t be on which coin gets more media attention, but rather on improving the systems of payments and settlement in a way that these differences are less relevant for the user and easier to handle for financial institutions. Only then, the idea of 24/7 settlements will be more than just a market dream or the result of the 21st-century daily finance.

Now the way forward is clear. Banks should trial tokenized deposits in the domains where they overcome important treasury and liquidity issues, while stablecoins should compete where they really contribute through cost reduction or broadening of access. But neither way should be mistaken for a consumer payments solution at the ready. Public interest is in settlement systems that provide for par value, are accessible on a wide variety of institutions and are readily equipped to handle failure. That is to say, infrastructure, glasnost and longer rounds of public operation. not to be mistaken for whitewashing a new label. The ordinary user will not need to pick between card and token, but will need a currency that is speedy, secure and stable when the market turns against it.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Aerts, S., Lambert, C. and Reinhold, E. (2025) ‘Stablecoins on the rise: still small in the euro area, but spillover risks loom’, Financial Stability Review, November. European Central Bank.

Alacriti (2026) ‘Tokenized Deposits vs. Stablecoins: What Banks Need to Know’, Knowledge Hub Blog, 15 April. Alacriti.

Bank for International Settlements (2025) ‘The next-generation monetary and financial system’, BIS Annual Economic Report 2025, Chapter III, 24 June. Bank for International Settlements.

Barr, M.S. (2026) ‘Brief remarks on stablecoins’, speech at The GENIUS Act in Practice: Key Questions for Stablecoin Regulation, Washington, DC, 31 March. Board of Governors of the Federal Reserve System.

BMO (2026) ‘BMO Introduces Tokenized Cash and Deposit Platform with CME Group and Google Cloud’, press release, 24 March. Bank of Montreal.

DeCarlo, D.W. (2026) ‘Could Instant Payments or Stablecoins Be the Answer to 24/7 Margin Calls?’, Chicago Fed Letter, No. 519, February. Federal Reserve Bank of Chicago.

Elledge, N. (2026) ‘Tokenized Deposits vs. Stablecoins: A Practical Guide for Financial Institutions’, Stablecore Insights, 2 March. Stablecore.

Garratt, R. and Shin, H.S. (2023) ‘Stablecoins versus tokenised deposits: implications for the singleness of money’, BIS Bulletin, No. 73, 11 April. Bank for International Settlements.

Intercontinental Exchange, Inc. (2026) ‘The New York Stock Exchange Develops Tokenized Securities Platform’, press release, 19 January. Intercontinental Exchange.

Liang, N. (2026) ‘What are the differences between payment stablecoins and tokenized bank deposits?’, Brookings, 14 April.

Muhn, J. (2025) ‘Tokenized Deposits vs. Stablecoins: What’s the Difference and Why It Matters’, Finovate, 2 July.

Noll, F. (2026) ‘What Are Stablecoins Used for Today? Estimating the Distribution of Stablecoins’, Payments System Research Briefing, 10 April. Federal Reserve Bank of Kansas City.

Watsky, C., Allen, J., Daud, H., Demuth, J., Little, D., Rodden, M. and Seira, A. (2024) ‘Primary and Secondary Markets for Stablecoins’, FEDS Notes, 23 February. Board of Governors of the Federal Reserve System.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.