“Drop the Makino Deal” — MBK, Once Dominant in Japan, Blocked by Government’s Economic Security Barrier

Authored On

Modified

Japan urges MBK to halt acquisition of Makino Milling Machine Conservative stance mirroring U.S. CFIUS resurfaces after Line-Yahoo episode MBK’s Japan investment strategy faces disruption amid mounting regulatory pressure

The Japanese government has urged private equity firm MBK Partners to suspend its planned acquisition of local machine tool manufacturer Makino Milling Machine (hereafter Makino). Japan’s conservative economic security stance—previously evident during the Line-Yahoo controversy—has once again emerged as a key obstacle in the mergers and acquisitions (M&A) market. As a result, MBK’s aggressive investment strategy in Japan, which had generated substantial returns, is now facing a significant setback.

MBK Faces Risk of Deal Collapse

According to Nikkei on April 23, the Japanese government recently sent a letter to MM Holdings, a local special purpose company (SPC) established by MBK for the Makino acquisition, requesting that “non-Japanese entities refrain from acquiring domestic defense-related companies.” The government classified MBK as a non-Japanese entity on the grounds that MM Holdings was established in the Cayman Islands, a known tax haven. Japanese Finance Minister Satsuki Katayama stated at a press conference that “Makino manufactures globally competitive machine tools and supplies them extensively to Japan’s defense equipment manufacturers,” adding that “the government determined that this investment could potentially undermine national security.”

MBK began pursuing the Makino acquisition in June last year. At the time, Makino’s management, facing a hostile takeover attempt from Japanese motor manufacturer Nidec, aligned with MBK as a “white knight.” MBK planned to launch a tender offer to acquire all outstanding shares excluding treasury stock at a 40% premium to the previous closing price. If executed, the deal was estimated to reach up to $1.84 billion.

Nikkei assessed the government’s intervention as grounded in historical precedent rather than excessive caution, noting that MBK’s acquisition attempt evoked memories of the Toshiba Machine (now Shibaura Machine) CoCom violation incident. In 1987, during the Cold War, Toshiba Machine exported high-performance machine tools to the former Soviet Union in violation of the Coordinating Committee for Multilateral Export Controls (CoCom) regulations, which were designed to prevent technology transfers to communist states.

Machine tools are equipment used to cut and polish metal to manufacture precision components. They are integral not only to industrial applications such as automobiles, aircraft, and semiconductor manufacturing equipment, but also to defense systems including missiles, submarines, and fighter jets. This dual-use nature is why machine tool companies are classified as core industries under Japanese law. The Soviet Union leveraged Toshiba Machine’s technology to significantly reduce submarine noise, complicating U.S. detection capabilities. The incident escalated into a political controversy in the United States, leading to executive resignations at Toshiba and a three-year sales ban for Toshiba Machine in the U.S. Nikkei noted that “this case left a lasting imprint on Japan, underscoring how civilian technology exports can destabilize national security.”

Japan’s Conservative Policy Orientation

Some analysts interpret Japan’s decision as part of its broader internalization of a U.S.-style economic security framework. The United States has long blocked foreign acquisitions of strategic technology firms through the Committee on Foreign Investment in the United States (CFIUS). In 2024–2025, Nippon Steel’s attempted acquisition of U.S. Steel also faced strong resistance in the U.S. Japan has similarly strengthened its foreign investment screening regime since revising the Foreign Exchange and Foreign Trade Act in 2019, effectively benchmarking the CFIUS model. Last month, the Japanese government submitted further amendments to the law, expanding screening to indirect investments, mandating prior reviews for high-risk transactions, and enhancing government authority, including post-investment divestment orders—measures that collectively raise barriers to foreign capital.

The Line Yahoo controversy, which significantly strained Korea-Japan relations in recent years, exemplifies Japan’s conservative security posture. The issue originated in November 2023 when malware infiltrated a PC of a Naver Cloud partner, resulting in a data breach involving Japan’s dominant messaging platform, Line. In response, Japan’s Ministry of Internal Affairs and Communications issued administrative guidance twice in March and April 2024, urging Naver to divest its stake in Line Yahoo. The matter escalated into a diplomatic dispute in Korea over concerns of management control infringement, and the ministry withdrew its divestment request only after a bilateral summit in May.

The dispute was eventually resolved by structurally separating Line Yahoo’s servers and networks from those of Naver and Naver Cloud. As of March this year, Line Yahoo had effectively completed system, authentication, and network separation, along with broader structural segregation including domestic and overseas subsidiaries. Residual data retained for audit and backup purposes is scheduled for deletion by the end of June. This effectively eliminates any technical pathway for Naver’s involvement in Line Yahoo’s operations.

Emergency in Japan Investment Strategy

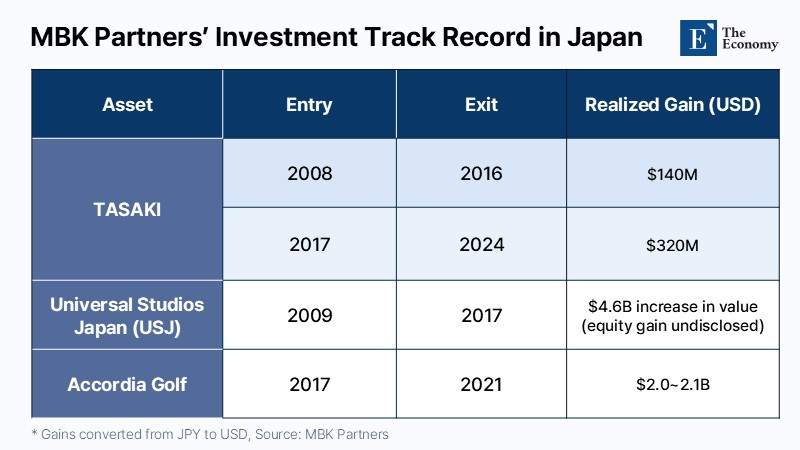

Amid Japan’s firm stance, MBK now finds itself in a difficult position. The firm has historically generated substantial returns through bold investments in Japan. A notable example is its investment in luxury jewelry brand Tasaki. In 2008, Tasaki sold approximately 80% of its shares to MBK for around $47 million in exchange for management control. MBK subsequently enhanced corporate value through measures such as partial closure of pearl farms, voluntary retirements, and asset sales, ultimately exiting in January 2016 with returns roughly double its initial investment. In 2017, MBK reacquired 100% of Tasaki through SPC Stardust for approximately $211 million, delisted the company, and later sold it in 2024 for about $670 million, securing another substantial gain.

Universal Studios Japan (USJ) also stands as a landmark transaction. MBK initially invested in USJ in May 2009 through its second blind fund and exited in April 2017 after 7 years and 11 months. USJ’s enterprise value surged from approximately $904 million at acquisition to around $5.02 billion at exit, representing nearly a sixfold increase. In 2021, MBK sold Japanese golf course operator Accordia Golf—acquired in 2017—to Fortress Investment Group, a SoftBank affiliate, for approximately $2.68 billion. At the time of acquisition, MBK and its co-investors deployed equity of roughly $536 million to $603 million, effectively achieving close to a fourfold return.

MBK’s aggressive investment trajectory in Japan has continued in recent years. The firm acquired Japanese semiconductor substrate and glass manufacturer FICT last year and is currently pursuing the acquisition of Japanese healthcare and nursing company Solasto. However, market participants believe that the effective suspension of the Makino deal could trigger adjustments in MBK’s broader investment strategy. Given that the Makino transaction accounted for a significant portion of its sixth buyout fund—valued at approximately $6 billion—there is a strong likelihood of revisions to capital allocation plans and investment timelines.

Similar Post