China Real Estate Crisis: Why Japan’s Lost Decades Matter More Than the Official Growth Rate

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

China may be repeating Japan’s property crash The real risk is weak household demand Without reform, the slump may last years

The crisis in China's property market is now old enough for the correct policy mistake to become obvious. Too much discussion still centers on the question of when prices will trough, as if the only question were timing. A harder question: has China begun the long, slow adjustment that consumed Japan after 1990? The comparison is no longer academic. Kenneth Rogoff and Yuanchen Yang say China and Japan are "more alike than you might think." China's property sector, plus related infrastructure, once represented some one-third of demand and housing still sits at the heart of household wealth. In 2025, Chinese real estate investment was down 17.2%. In the first quarter of 2026, it fell another 11.2% year-on-year, even as headline GDP grew 5.0%. That is the danger. A nation can have acceptable top-line GDP growth while the household sector's balance sheet quietly sours. Japan taught us that a property bust does not have to explode like a banking panic to cripple demand. It can also just grind down the economy.

The Chinese real estate crisis is not a copy of Japan, but it rhymes in the same places

The similarities between Japan in the 1990s and the Chinese real estate crisis today do not begin with charts of falling prices. They begin with a growth model. Industrial expansion, heavy investment and belief in ever-rising land values, in both cases, push the real estate market beyond its economic role to become a passive store of wealth. Instead, it was a nationwide development machine. That machine churned out too much for too long for too far. Rogoff and Yang argue that the similarity is not just leverage but overbuilding and diminishing returns. Japan's housing and infrastructure sectors were overbuilt prior to the bust. China did likewise, particularly in non-tier-1 cities, where local governments treat land, construction and finance as a stable source of growth and revenue. When demand began to fade, it wasn't just a normal economic downturn. It was the realization that years of investment had generated a supply that could not earn enough to justify its cost.

The differences are real and they do not nullify the comparison. China possesses greater state control, higher household savings and a banking system less exposed to a classic open financial crisis than Japan's was. Rogoff and Yang stress this is precisely why many expected China to avoid a deep property crisis. But the same paper notes that real-side forces can be immensely damaging, even in the absence of a full-blown banking crisis. In this regard, China may be more dangerous than Japan to analyze. A visible banking panic would trigger immediate acknowledgment of the problem, while a managed downturn would allow the state to delay losses, selectively support developers and gloss over the headlines. However, this would not restore household confidence, which is not a peripheral factor in a property-dependent economy. Instead, confidence would remain a driving force of demand.

A second objection is that China remains a middle-income nation and thus has greater scope for urbanization compared with Japan in the early 1990s. While true in theory, this argument offers little solace when considering the reality on the ground. The issue isn't whether certain cities require more housing; it is whether existing housing stock, local government finance and pending or completed projects are aligned with actual household demand. China's particular problem is that the oversupply is not geographically concentrated in areas where demand will grow fastest. Rather, it is concentrated in locations linked to local government incentives, land finance, migration and the political impulse to overcome weakness with increased construction. That also reflects how urban development strategies shape investment flows. Japan's flaw was not just that it built too much, but that it continued to prioritize construction long after it was economically productive. China seems to be repeating this mistake.

Why China's real estate crisis may persist much longer than investors anticipate

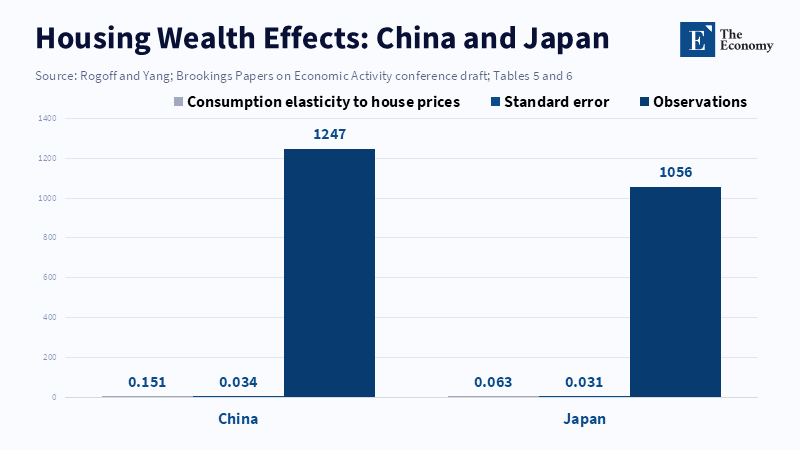

Japan's experience does not suggest recovery is unattainable, but rather that it is not guaranteed to happen rapidly following a real estate-led growth bust. Rogoff and Yang report that Japan's house prices began falling in the early 1990s, bottomed out mid-decade and took nearly twenty years to return to their pre-crisis levels. This does not mean that every sector of the market was frozen for thirty years. Japanese land prices, for instance, have been increasing for four years straight and in 2024, they posted their strongest nationwide growth in 34 years. Nevertheless, this recent rebound merely confirms the broader assertion; a visible rebound took decades and even then, it was uneven across different regions and asset classes. The bubble-era damage was absorbed over multiple generations of prices, demographics and expectations, not within one economic cycle.

China is still in the early stages of this process. New home prices were still declining year-on-year in March 2026 at a rate of 3.4 percent, according to official figures. The property market has yet to stabilize. Real estate investment plunged 17.2% in 2025. During the first quarter of 2026, newly built commercial floor space sold plummeted 10.4% and sales value decreased 16.7%. Several independent forecasts now expect broader price stabilization only by 2027, rather than 2026. While this may appear to offer a faster recovery trajectory than Japan's experience, it should not be mistaken for a true rebound. A market can find its footing before recovering and recover in some core cities while the rest of the national economy remains impaired. The most relevant Japanese lesson is not the speed at which prices will bottom out, but the prolonged period in which weak property values, excessive supply and diminished confidence depressed domestic demand long after the initial shock had passed.

China's real estate crisis is essentially a household wealth crisis

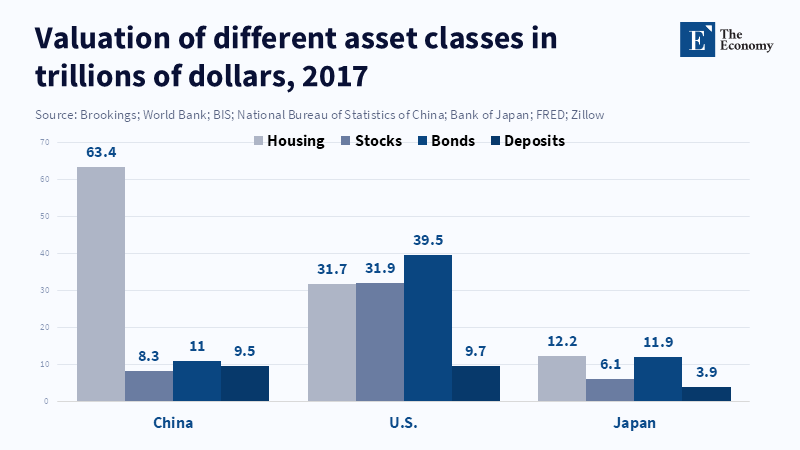

This aspect of the Japanese comparison is particularly crucial. While property crashes can damage banks, they can also hurt consumer spending. This latter mechanism may be more significant for China than many policymakers acknowledge. Rogoff and Yang estimate that housing represents approximately 70% of Chinese household wealth. Their analysis suggests a significant housing wealth effect on consumption and falling prices may further depress it given negative sentiment. Their model indicates that a cumulative decline of 20-40% in housing prices may lower consumption by 2-4% of GDP. This is important given that household consumption in China remains remarkably low as a percentage of GDP-around 40% in 2024, according to World Bank data. In such an economic context, a property bust is more than just a sectoral problem. It attacks the principal savings vehicle for the middle class in an already low-consumption economy.

Here, Japan rises above merely an historical analogy; it presents a warning about the mechanism. Japan's bust was exacerbated by, not solely caused by, bad loans; falling land values simultaneously eroded wealth, morale and investment. The new Brookings work suggests China suffers the same threefold drag: less investment, less consumption and less morale. This explains why official GDP figures can look stable while the domestic economy stagnates. China's CPI has been stagnant this year and the IMF indicates that private domestic demand remained stagnant while the GDP deflator has fallen. The current account surplus widened to an estimated 3.3% of GDP, suggesting foreign demand is shouldering much of the burden. Rogoff stated in a recent Brookings debate the obvious policy predicament China faces: it cannot "export its way out of its problems." The risks of lost growth stem from attempts to rebuild China's economy on factories, exports and headline stimulus without addressing the household demand slump.

The social element adds to the stickiness. Housing in China was never solely an asset. It was a primary savings vehicle, a sign of family status and often the linchpin of the safety net that spanned generations. As its value falters, households do not solely reduce spending due to weaker balance sheets. They also do it due to an erosion of confidence in the future. Rogoff and Yang postulate that this negative feedback effect could nearly double the impact of falling prices on consumption. Hence, policies that attempt to support developers, provide partial interest rate cuts, or bolster their liquidity are largely bound to fail; they address only a portion of the crisis and fail to alter the underlying psychology of housing as a reliable store of value. Japan has illustrated the persistent nature of this negative cycle once it gains momentum.

What Japan's painful decade has taught China and what it must do going forward

While the Japan analogy may face objections on the grounds that China has stronger means of controlling its banking system than Japan did in the 1990s, the argument that these tools merely influence the manner of contraction, not its underlying cause, seems plausible. Indeed, the mechanisms in question appear capable of preventing systemic chaos rather than actively generating healthy demand on their own. In Japan's case, when property, local banks, demography and sentiment converged, the country's economy required more than targeted intervention. It requires a new paradigm of demand generation. The IMF is now stating this explicitly. Its report states that China's private domestic demand remains lackluster, warns that any significant contraction in property will further embed deflationary pressures and urges a reorientation of expenditure away from potentially inefficient investment and toward consumption and the necessary real estate adjustment. The IMF calculates that a comprehensive reform package could contribute an increase of approximately 4 percent to the consumption-to-GDP ratio over the next five years.

This shift to a consumption-oriented economy will prove politically challenging; it necessitates a decreased reliance on land sales and targets that reward sheer volume, greater state intervention through fiscal support mechanisms for both consumers and construction on incomplete housing projects and tolerance for the decline of the construction sector as an intrinsic part of rebalancing, not a policy mistake. The shift is particularly hard in light of years of government objectives that view investment volume as an indicator of policy success and local success and which have been linked directly to the performance of building and construction output. The Japanese experience indicates how long the economy can remain in a transitional phase of repair and renewal when the government mitigates some negative consequences of adjustment without directly addressing the fundamental cause of the problem. As China treats the crisis as a temporary slowdown in property values, the resemblance to Japan only grows stronger.

The true test for China will lie in policy decisions. Beijing should not attempt to recreate the bubble economy of the past; instead, it should recognize that the current real estate crisis is not primarily an issue of assisting troubled developers back into operation. It is fundamentally about shifting the risk away from household savings, expectations and future consumption, which have become irrevocably tied to land and apartments. The crisis demands finishing unfinished projects, absorbing excess supply using substantial fiscal support, diversifying local economies away from dependence on land finance and creating a more comprehensive social safety net that reduces households' dependence on real estate as their principal source of security. While there is no guarantee of a Japanese-style decade or two of stagnating growth, there is little doubt that delay, denial and superficial solutions are sure to prolong and deepen the nation's troubles. The paramount issue at hand has shifted beyond determining how China is similar to Japan, to assessing how quickly Beijing can avert that resemblance from becoming indistinguishable.

The importance of Japan at the core of China's predicament is straightforward; it forces discussion of what transpires following a crash, rather than solely the mechanics of the crash itself. Japan did not merely endure a bubble and a bust; it lacked a sustainable engine of growth after its property market collapsed. China faces this very same possibility now. Statistics indicate that China's property sector continues to contract, that household demand remains weak and that prices are still sliding. The aforementioned research from Rogoff and Yang provides a robust argument for the possibility that the current crisis could develop into a prolonged period of real adjustment, regardless of a systemic collapse in the banking sector. The real lesson is that China's property crisis will be assessed not by a short-term reversal in a few urban property markets, or a seemingly strong headline GDP figure; it will be determined by Beijing's ability to forge a robust foundation for domestic demand, which will take the place of the role that property once held. Without it, Japan will not simply serve as a metaphor, but as a foreboding guide to China's likely future.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Eberly, J.C., Milesi-Ferretti, G.M., Rogoff, K., Steinsson, J. and Yang, Y. (2026) ‘How long will China’s real estate crisis last?’, Brookings Podcast on Economic Activity, 16 April.

Gao, L. and Woo, R. (2026) ‘China’s home prices seen falling faster before stabilising in 2027: Reuters poll’, Reuters, 13 March.

Gao, L., Zhang, Y. and Woo, R. (2026) ‘China’s new home prices extend decline despite improvement in major cities’, Reuters, 16 April.

International Monetary Fund (2026) People’s Republic of China: 2025 Article IV Consultation—Press Release; Staff Report; and Statement by the Executive Director for the People’s Republic of China. IMF Country Report No. 26/044. Washington, DC: International Monetary Fund.

Kaneko, K. (2025) ‘Japan’s land prices rise at strongest pace in 34 years’, Reuters, 18 March.

National Bureau of Statistics of China (2026a) ‘Investment in Real Estate Development for 2025’, 20 January. Beijing: National Bureau of Statistics of China.

National Bureau of Statistics of China (2026b) ‘National Economy Got off to a Good Start in the First Quarter’, 16 April. Beijing: National Bureau of Statistics of China.

Rogoff, K. and Yang, Y. (2026) ‘A Tale of Two Countries: The Real Estate Crises in 1990s Japan and Contemporary China’, Brookings Papers on Economic Activity, Spring conference draft. Washington, DC: Brookings Institution.

World Bank (n.d.) Households and NPISHs final consumption expenditure (% of GDP) – China. World Development Indicators. Washington, DC: World Bank.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.