When AI Captures the Surplus: Business Gains, Shrinking Labour Income, and the Next Demand Shock

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI can raise business output while shrinking labour’s share of income That weakens household demand first in B2C sectors, then spreads across the wider economy Without broader distribution of AI gains, growth may continue, but it will become narrower and more fragile

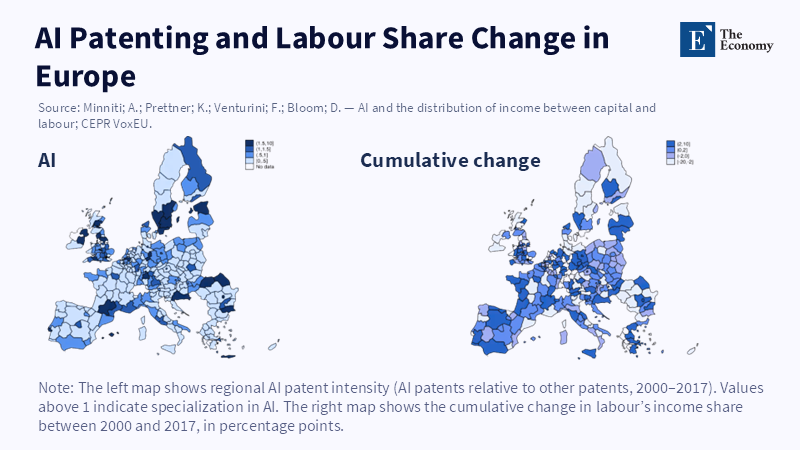

The discourse surrounding artificial intelligence (AI) frequently begins with a narrow focus, centering on whether AI will eliminate jobs so rapidly as to provoke immediate labor market panic. This perspective is overly narrow. A more fundamental issue concerns the distribution of surplus generated as machines increasingly perform not only routine manufacturing tasks but also cognitive, managerial, and service functions previously undertaken by humans. Recent empirical evidence from Europe suggests concerning trends. Regions exhibiting higher intensities of AI-related patenting have experienced more pronounced declines in labor's share of income, implying that AI functions less as a broadly distributed productivity enhancer and more as a capital-biased technology that reallocates returns toward firms and capital owners (Minniti et al., 2025). Such dynamics alter macroeconomic narratives significantly. While output and profits may rise, household purchasing power can concurrently diminish. This phenomenon represents a form of economic expansion accompanied by joblessness, characterized by aggregate growth that undermines the extensive consumer base critical to the social and fiscal sustainability of that growth.

From customary surplus notions to AI-induced surplus dynamics

Traditional introductory economics posits a clear framework: consumers and producers interact in markets where prices equilibrate supply and demand; both parties derive benefits from exchange. Workers receive wages, which they subsequently expend as consumers, maintaining a circular flow that integrates production, income, consumption, and tax revenue into a coherent system. This cycle underpins the legitimacy of market capitalism, whereby firms generate profits and invest, and households earn wages that fuel demand necessary for firm growth (Prato & Fleurbaey, 2024).

AI challenges this equilibrium not merely by enhancing the tools used by labor, but by directly substituting for labor in many contexts and diminishing workers' bargaining power, even when employment persists. The data from CEPR gains significance, not as conclusive evidence of future outcomes but as an indicator of trend direction. Analysis across 238 regions in 21 European countries reveals a correlation between intensified AI innovation and declining labor income shares, particularly pronounced in industrial areas. (Minniti et al., 2024) The researchers contend that AI is a capital-biased innovation, allocating a growing proportion of technological gains to capital rather than labor (Minniti et al., 2025). As GDP growth is expected to slow to 2.1 percent in 2026 before rebounding, it becomes harder to argue that productivity gains will automatically translate into higher wages for most workers (Autor & Kausik, 2026). According to the OECD Economic Outlook, higher business profits do not necessarily translate into greater demand among the broader population.

Firms may exhibit robust profit margins, expand market presence, and boost output while reducing employment or constraining compensation. Short-term assessments may interpret this as a success; however, medium-term implications include the erosion of the consumer base on which large segments of the economy depend. If AI enables a smaller cohort of firms to generate more output with fewer workers, the distribution of economic surplus will change before any noticeable shifts in headline unemployment figures. Disparities emerge initially in income distribution and subsequently manifest in demand patterns. Consequently, the pertinent business inquiry is not solely about productivity gains but whether firms appropriate a disproportionately large share of those gains, weakening the broader economic framework necessary to absorb their increased output.

The vulnerability of consumer-facing firms

The earliest and most apparent impacts of this shift are likely to affect businesses that rely on broad-based household spending. In response to job displacement, lower wages, or diminished bargaining strength, households typically curtail discretionary spending, defer significant purchases, and become more sensitive to pricing. This impact does not permeate the entire economy simultaneously; it first affects consumer-oriented sectors such as retail, hospitality, travel, low-margin services, and volume-based enterprises, before affecting upstream suppliers. The critical question here is not whether aggregate production remains sufficient, but whether a sufficient number of households maintain purchasing capacity.

The concept of a K-shaped economy proves instructive in this context (Ganuthula & Balaraman, 2025). According to the 2026 overview by U.S. Bank, a K-shaped economy involves divergent trajectories wherein certain groups, industries, and firms experience growth, while others stagnate or decline. According to the 2026 Report on Employer Firms, nearly half of businesses rely on international suppliers, and most firms have experienced rising input costs from year to year (2026 Report on Employer Firms: Findings from the 2025 Small Business Credit Survey, 2026). This dynamic may have implications for how firms serving different income communities manage revenue risks as AI-driven transitions reshape the economy. Firms oriented toward high-income consumers, enterprise software, infrastructure, finance, defense, or specialized digital services may continue their upward trajectory. Conversely, mass-market companies that depend on steady wage-based consumption among middle- and working-class populations face greater exposure. Consequently, the division extends beyond capital-labor differences to encompass disparities between firms serving concentrated wealth and those addressing broad consumer demand.

This divergence may unfold amid increasing output. AI enhances efficiency in logistics, administration, coding, design, forecasting, and customer operations, lowering labor costs and accelerating production cycles. Superficially, this suggests robust growth. Nevertheless, if income gains concentrate among top earners, productivity no longer reliably forecasts aggregate demand. Gross domestic product may rise even as demand in sectors serving typical consumers weakens. The economy thus unfolds dual narratives: one highlighting successful innovation, improved margins, and enhanced corporate capacity; the other detailing reduced wages, constrained household finances, and diminished demand in lower-productivity sectors that still employ the majority. This duality reflects not contradiction but a central characteristic of growth accompanied by underemployment.

The eventual vulnerability of business-to-business sectors

A common assumption holds that if consumer-facing sectors contract, business-to-business (B2B) firms can sustain growth through enterprise demand, automation investments, and infrastructure enhancements. This pattern may hold temporarily. According to the 2026 Report on Employer Firms, revenue and employment growth remained steady between 2024 and 2025, with firms slightly more likely to report a decrease in revenues over the prior year (2026 Report on Employer Firms: Findings from the 2025 Small Business Credit Survey, n.d.). However, this immunity is temporary; B2B revenues ultimately depend on the vitality of end markets. Manufacturers purchase from suppliers based on anticipated consumer orders; service firms rely on retail clients whose sales forecasts stem from consumer activity; cloud providers scale in response to clients' expectations of increased business volume. Prolonged weak household demand triggers backward propagation through production networks: order volumes decline, expansion plans stall, inventory accumulates, and investment shifts from growth to preservation (Pandemic-Era Demand Squeezed Housing Inventories, 2025). According to Tatsuru Kikuchi, sectors that appear insulated from broader economic changes, such as some B2B industries, can still be affected by declining wage-driven demand, though the impact may be delayed and not immediately visible, creating the mistaken impression that these sectors are more resilient than they actually are.

Hence, the issue of business surplus transcends a simplistic dichotomy between corporate winners and household losers. It is a macroeconomic concern. When firms collectively appropriate an increasing share of income while households' spending capacity weakens, systemic imbalances ensue. Although some firms and sectors may thrive, becoming larger, wealthier, and more technologically advanced, the overall system's stability deteriorates because it relies on concentrated demand rather than on pervasive consumer participation. In this scenario, the traditional circular economy weakens, with labor earning insufficient income to underpin consumption and businesses lacking corresponding broad-based demand, despite aggregate productivity improvements. According to Tatsuru Kikuchi, while overall economic growth metrics may look strong, they can hide underlying weaknesses in societal stability, particularly as GenAI adoption contributes to a K-shaped economic pattern where benefits are unevenly distributed. This uneven growth is often described as a temporary phase, but Kikuchi's analysis suggests it may persist as a structural feature of the economy.

Persistence of a K-shaped economy

There is a tendency to frame these developments as transitional. The optimistic narrative suggests temporary labor displacement followed by retraining and eventual reintegration into new roles, culminating in a new economic equilibrium. While this may occur in specific sectors, the current wave of AI adoption casts doubt on whether this adjustment will be timely, extensive, or socially smooth. AI’s reach now extends beyond automating simplistic, routine tasks to encompass white-collar, analytical, supervisory, and creative roles traditionally perceived as secure. Consequently, the shock permeates occupations foundational to middle-class consumption, intensifying demand-side repercussions by eroding the household segments historically sustaining tax bases and consumer markets.

The K-shaped pattern observed relates not solely to household income disparities but also to structural differences in productivity. High-productivity sectors intensive in AI technologies advance due to advantages such as scale, data access, capital availability, and low marginal labor requirements. In contrast, lower-productivity sectors—often reliant on face-to-face services or broad consumer spending—experience declining spending, heightened competition, and limited capacity to monetize AI innovations as effectively as leading firms do. These sectors do not merely lag growth but frequently constitute the margin through which the economy accommodates the social costs of concentrated technological gains. Sectoral divergence thus emerges as a fundamental component of the transition, rather than an incidental byproduct (Autor & Kausik, 2026).

For policymakers, educators, and administrators, these dynamics imply two main considerations. First, aggregate productivity growth should not be interpreted as indicative of equitable distributional outcomes; a society may advance technologically while becoming less balanced, resilient, and inclusive. Second, prioritizing the question of surplus allocation is imperative within education and labor policy frameworks. While workforce retraining retains significance, it cannot suffice if broader growth dynamics increasingly favor capital concentration. Labor cannot retrain its way out of a macroeconomic arrangement where fewer firms require less labor to produce more (Autor & Kausik, 2026). Therefore, education policy must be complemented by fiscal, competition, and labor-market strategies that determine whether AI-generated gains concentrate narrowly or are redistributed into wages, demand, and public investments.

The narrowing economic base under concentrated firm gains

The core issue transcends the question of whether firms will benefit from AI productivity. Many evidently will. The critical question concerns the extent to which firm gains, relative to labor income, constrain the economy’s breadth, exacerbate inequality, and undermine self-sustainability. Current data indicate a trend toward such distributional shifts. AI-intensive regions report decreasing labor shares, and K-shaped divergences become perceptible across both households and firms. Consumer-facing businesses demonstrate heightened vulnerability amid wage stagnation, while B2B entities maintain only temporary insulation (Minniti et al., 2025; U.S. Bank Economics Research Group, 2026). Should this pattern solidify, forthcoming macroeconomic challenges will relate less to productive capacity and more to the insufficiency of widely distributed purchasing power.

Accordingly, this discourse is more appropriately situated within public finance rather than confined to labor economics or corporate strategy. According to a 2026 analysis by Tatsuru Kikuchi, elevated firm surpluses not only contribute to inequality but also affect aggregate demand, fiscal health, economic stability, and public trust. When firms achieve high productivity while household finances weaken, the economy lacks a solid foundation for sustainable growth, highlighting underlying systemic risks. The policy imperative is not to resist productivity advancements but to manage their distribution. Should AI enable firms to generate greater output with diminished labor input, decisions must be made regarding whether these benefits remain concentrated at the apex or circulate back into the socioeconomic structures that underpin expansive markets. Absent such redistribution, even highly efficient firms risk long-term viability in an economy whose consumers are increasingly marginalized from participation.

References

Autor, D. and Kausik, B.N. (2026) Resolving the automation paradox: falling labor share, rising wages. arXiv preprint.

Bovino, B.A. and Schoeppner, M. (2026) The K-economy in 2026: Same story, new amplifiers. U.S. Bank Economic Commentary.

Delaney, S. (2025) ‘[K-shape labor market] U.S. Labor Market Enters a Once-in-a-Generation Inflection Point, AI Proficiency Accelerates Income Inequality’, The Economy, 22 December.

Federal Reserve Banks (2026) 2026 Report on Employer Firms: Findings from the 2025 Small Business Credit Survey. Small Business Credit Survey.

Fresquet Kohan, V., Mondragon, J. and Shapiro, A.H. (2025) ‘Pandemic-Era Demand Squeezed Housing Inventories’, FRBSF Economic Letter, 2025-01, 6 January.

Ganuthula, V.R. and Balaraman, K.K. (2025) Skill-Based Labor Market Polarization in the Age of AI: A Comparative Analysis of India and the United States. arXiv preprint arXiv:2501.15809.

Lee, K. (2026) ‘The AI Labor Divide: Who Wins, Who Survives, and Who Falls Away’, The Economy, 13 February.

Minniti, A., Prettner, K. and Venturini, F. (2024) AI Innovation and the Labor Share in European Regions. SSRN Working Paper 4971431.

Minniti, A., Prettner, K., Venturini, F. and Bloom, D. (2026) ‘AI and the distribution of income between capital and labour’, VoxEU, 3 March.

Prato, F.D. and Fleurbaey, M. (2024) Workers as Partners: a Theory of Responsible Firms in Labor Markets. arXiv preprint.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.